Cregis Research: 2023 Blockchain Industry Panorama Review and Analysis

This article will deeply analyze the core developments and main trends in the blockchain industry over the past year.

This article will deeply analyze the core developments and main trends in the blockchain industry over the past year.Author: Cregis

## 1. Introduction

The cryptocurrency market in 2023 has exhibited a paradoxical phenomenon: despite lukewarm investor activity, market prices have seen significant increases. Most financial institutions remain cautious about providing services to cryptocurrency users, yet recent ETF applications mark a significant advancement in institutional adoption within the cryptocurrency space. Regulatory bodies have issued warnings about market risks and taken corresponding enforcement actions, while the judiciary has pushed back against this regulatory overreach. Meanwhile, Ethereum's upgrade has allowed staked assets to be withdrawn, which has instead promoted an increase in the total amount of ETH staked.

In terms of blockchain platforms, Ethereum continues to solidify its leadership as a Layer 1 blockchain, focusing on developing scalability strategies centered around Rollups. Concurrently, competitive blockchains like Solana, Avalanche, and Cosmos have gradually expanded their market shares through their unique scaling strategies, with Solana's integrated approach achieving notable results by year-end.

In the realm of on-chain applications, while blue-chip lending and trading protocols have shown stable performance, liquidity staking providers like Lido have dominated the market. DeFi has made substantial progress in areas such as the tokenization of physical assets. The non-fungible token (NFT) market has experienced fierce competition, leading to a significant decline in market share for platforms like OpenSea, while the introduction of Ordinals on the Bitcoin network has spurred growth in NFTs and meme tokens. Additionally, the rise of decentralized social protocols heralds a new era of blockchain application development.

In this year full of contradictions, the blockchain industry has presented a series of compelling innovations and growth. This article will delve into the core developments and major trends in the blockchain industry over the year, providing readers with a comprehensive and profound industry perspective.

## 2. Blockchain Platforms and Scaling

(1) Layer 1

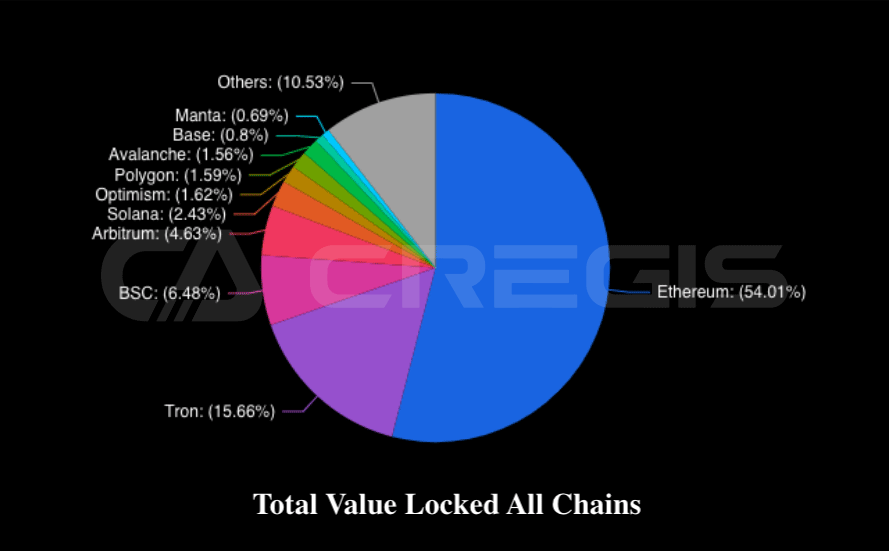

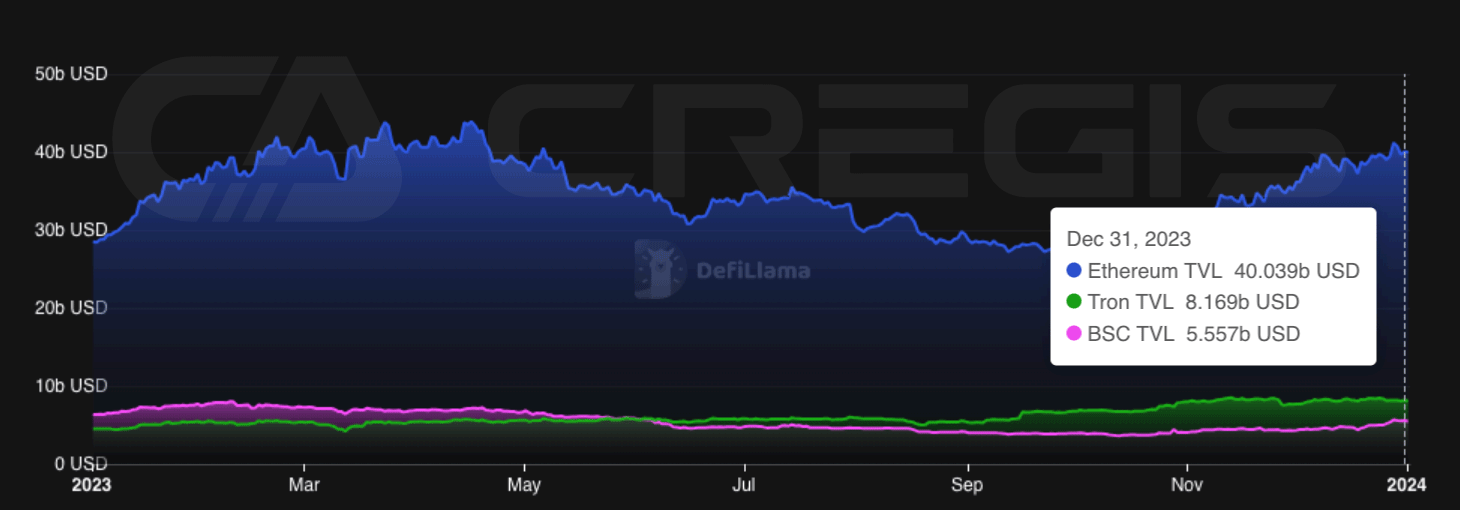

In 2023, Ethereum continued to lead the market as the premier Layer 1 network based on smart contracts. Whether in terms of total value locked (TVL), transaction volume, or transaction fees, Ethereum has maintained a dominant position compared to other Layer 1 networks based on smart contracts. By observing the highs and lows of transaction fees, we can gauge user demand for different blockchain networks. Clearly, in 2023, most demand was concentrated on the Ethereum network, as evidenced by its higher transaction fees.

(Source: DefiLlama)

Tron and BNB Chain

In 2023, Ethereum's main competitors underwent some noticeable changes. From the beginning of the year to the end, Tron’s total value locked (TVL) grew by approximately 100%, while BNB Chain's TVL decreased by about 38% during the same period. The primary reasons for these changes stem from macroeconomic factors and regulatory events. For instance, the growth in Tron's TVL can largely be attributed to stablecoin users shifting from USDC and BUSD to USDT, while the decline in BNB Chain's TVL is related to regulatory policies affecting the market.

(Source: DeFiLlama)

In 2023, as stablecoin users shifted from USDC to USDT, Ethereum's market share in the stablecoin market declined, while Tron gained a larger market share. By December 2023, Ethereum's share of the total stablecoin supply fell from 62.1% at the beginning of the year to 51.6%.

At the same time, BNB Chain faced a series of regulatory issues in 2023, including lawsuits from the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC). Following the suspension of Binance USD (BUSD), the supply of stablecoins on BNB Chain continued to decrease. By November, regulatory issues surrounding Binance reached a peak, leading to CEO Changpeng Zhao (CZ) reaching a plea agreement with the U.S. and resigning. From the beginning of 2023 to year-end, BNB's market capitalization fell by over $4.5 billion.

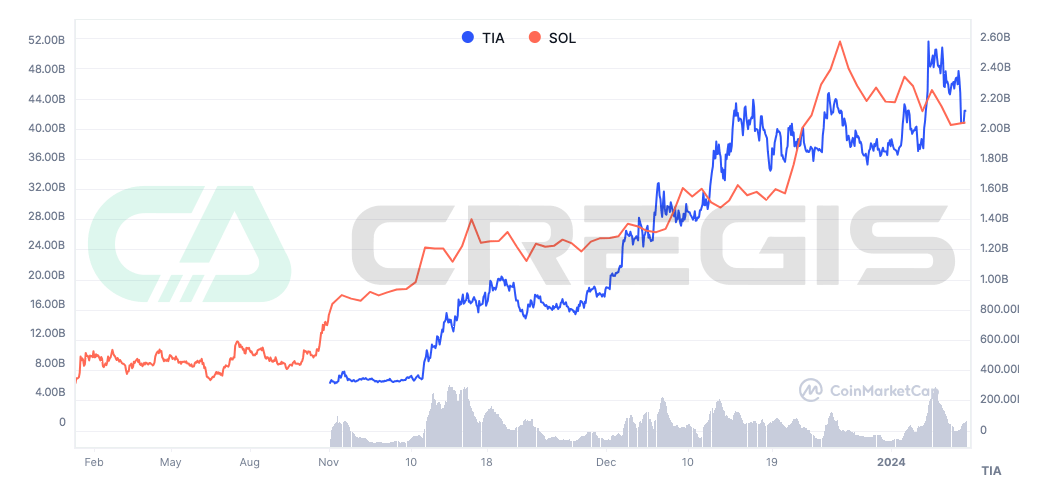

Solana and Celestia

One of the market hotspots in 2023 was the discussion around two opposing blockchain scaling solutions: modularity and integration. The market valuation of Layer 1 network tokens reflects the health of their ecosystems. By observing the historical prices of modular blockchain Celestia (TIA) and integrated blockchain Solana (SOL), we can see that Celestia's market cap surged by approximately 300% within a month after launching its TIA token in November, while Solana's market cap grew by about 800% in 2023.

(Source: CoinMarketCap)

One of the most significant trends in 2023 was the resurgence of Solana, both in terms of its valuation and the market's acceptance of its integrated scaling approach. Among the smart contract protocols with the highest total value locked (TVL), Solana stands out for its use of a customized execution environment—the Solana Virtual Machine (SVM)—which enables the network to execute transactions in parallel. To achieve high throughput and scalability while reducing user costs, Solana validators must coordinate with other validators in the network to complete complex processing tasks. This is made possible through a series of custom technologies, such as the Proof of History synchronization mechanism and the Turbine block propagation protocol, all of which ultimately lead to higher requirements for Solana validators compared to other Layer 1 networks.

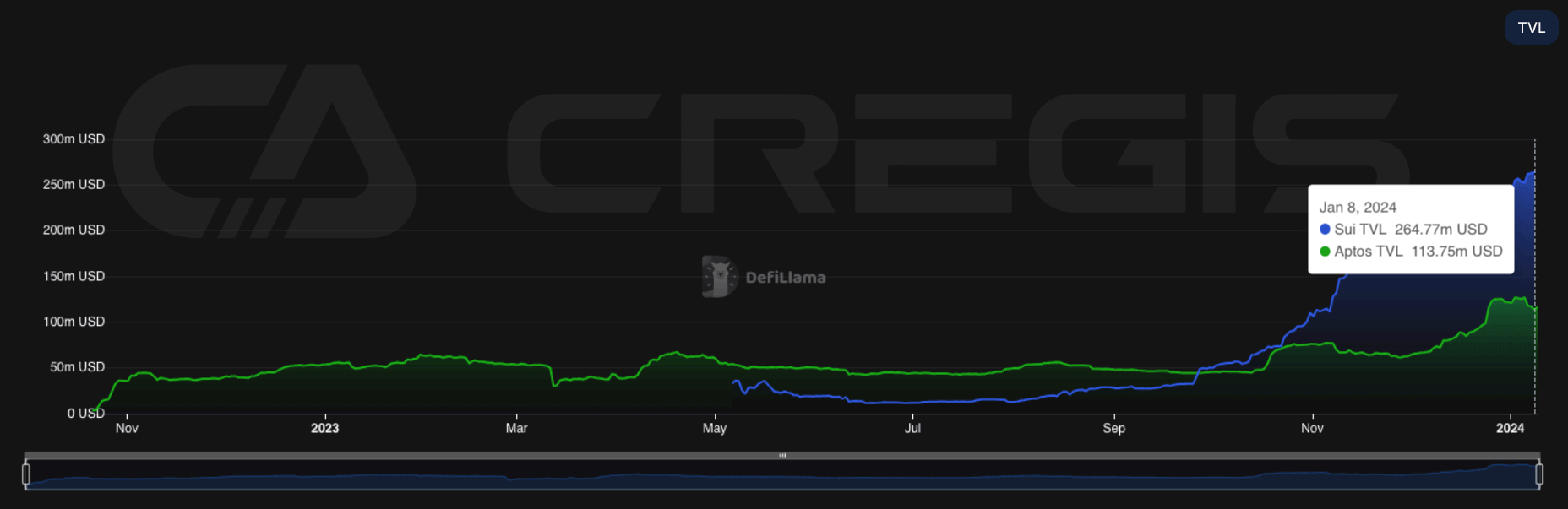

Sui and Aptos

In 2023, Solana became one of the most widely used integrated architecture blockchains. Over the past two years, several Layer 1 blockchains that adopt integrated architectures and achieve low-cost parallel execution have begun to emerge. Among them, Aptos and Sui are particularly notable, both originating from Meta's Diem project and using the Move virtual machine as their execution environment. By December 2023, the total value locked (TVL) of these two chains was approximately $377 million.

Notably, Sui demonstrated a faster growth rate compared to Aptos over the past year, with its TVL by the end of December being nearly twice that of Aptos. The trend in 2023 indicates that integrated architecture Layer 1 blockchains may play an increasingly important role in the smart contract platform space. However, these emerging platforms still have a long way to go to surpass the dominance of the Ethereum Virtual Machine (EVM).

(Source: DeFiLlama)

Cosmos and Avalanche

Since its inception, the Cosmos community has embraced the concept of modularity. In the Cosmos ecosystem, launching new blockchains is easier than in any other blockchain ecosystem, thanks to its native infrastructure and tools like the Inter-Blockchain Communication (IBC) protocol and Cosmos SDK. Developers can customize chain parameters according to their needs, such as inflation rates, staking unbonding periods, validator rewards, governance voting parameters, and more. At the same time, the IBC protocol allows for interoperability between different Cosmos chains.

The inherent advantage of modular blockchains comes at the cost of fragmented user attention and liquidity between Cosmos chains. Although IBC allows assets to be transferred between Cosmos chains, these assets must go through the same IBC channel. If not, these assets remain non-interchangeable. For example, ATOM sent from Osmosis to Canto via IBC is different from ATOM sent from Cosmos Hub to Canto. Therefore, in terms of composability and liquidity, Cosmos's application chains still face certain disadvantages compared to general Layer 1 blockchains.

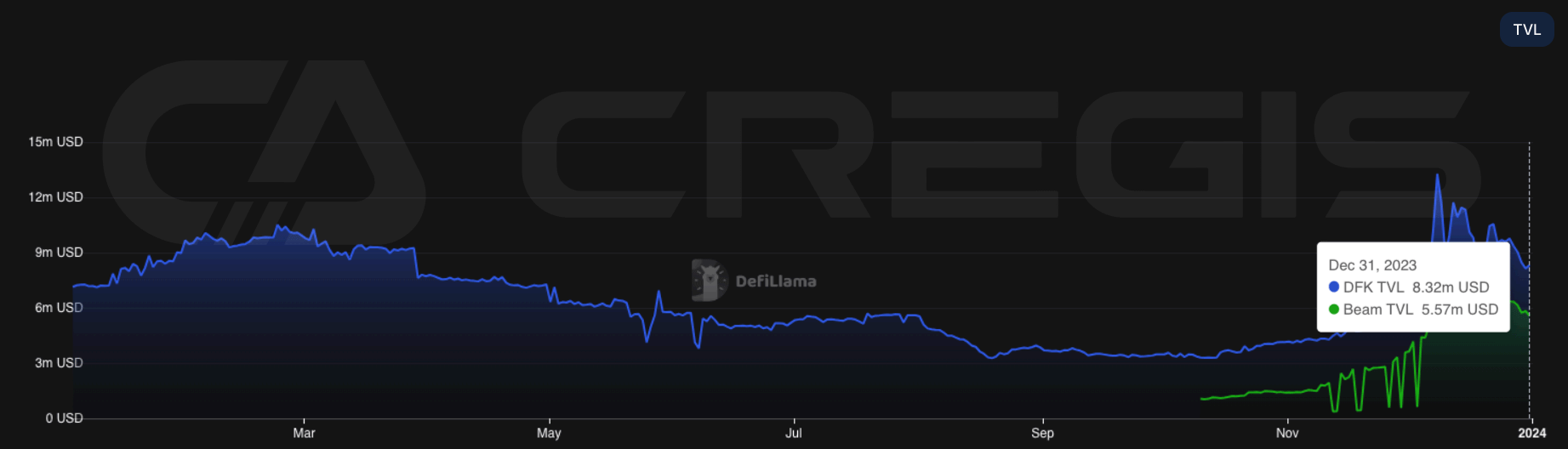

In 2023, the number of active subnets in the Avalanche ecosystem continued to grow, but user activity remained low compared to the main Avalanche C chain. By year-end, the total TVL of the two active subnets, DFK Chain and Beam, reached approximately $13.8 million.

(Source: DeFiLlama)

Avalanche subnets and newly launched Cosmos chains face similar challenges regarding network security. In the initial stages, these networks need to accumulate sufficient funds as a moat to prevent economic attacks. On Avalanche, validators need to stake 2,000 AVAX at a price of approximately $35 per AVAX. However, currently, the total number of validators on most Avalanche subnets does not exceed 10. Among these subnets, the largest, MELD, has only 16 validators. A lower number of validators could potentially impact the network's security and decentralization.

(2) Layer 2

As demand for Ethereum transactions continues to grow, its scaling issues have become increasingly urgent. Currently, Ethereum's processing capacity is about 15 transactions per second (tps), which clearly cannot meet the growing demand for large-scale usage. This limitation may become a key obstacle to Ethereum's future development.

Ethereum's scaling issues have always been a contentious topic. Its core dilemma lies in the so-called "impossible triangle" theory, which states that decentralization, security, and scalability are difficult to optimize simultaneously in a distributed network, and typically only two aspects can be optimized. Enhancing scalability often requires sacrificing some degree of decentralization or security. However, the Ethereum community is cautious about making such trade-offs and is reluctant to easily sacrifice decentralization or security.

(Source: DeFiLlama)

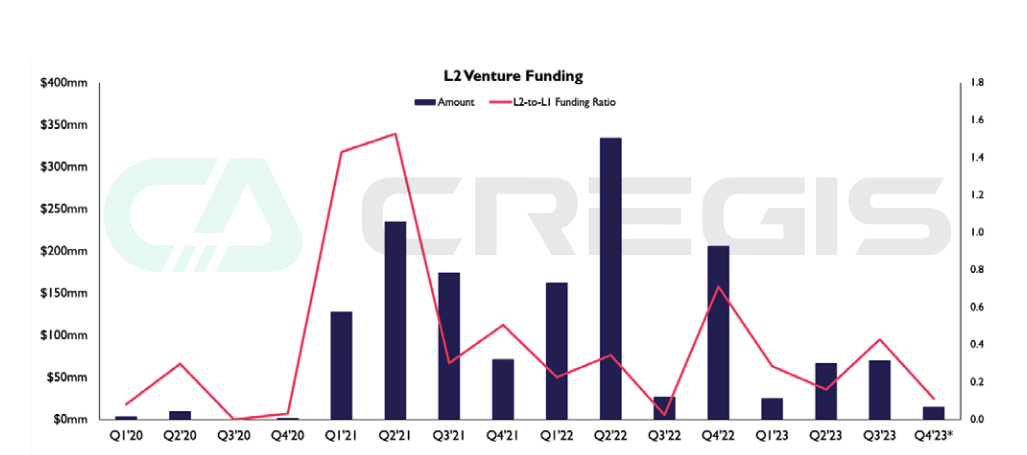

Ethereum's scaling methods are mainly divided into on-chain and off-chain solutions. On-chain scaling involves modifications to the core Ethereum protocol, while off-chain scaling builds additional protocols and infrastructure on top of Ethereum. Currently, off-chain scaling is developing faster than on-chain scaling. Particularly, during most of 2021 and 2022, off-chain scaling solutions based on optimism and rollups received sustained attention in the venture capital market.

(Source: The Block)

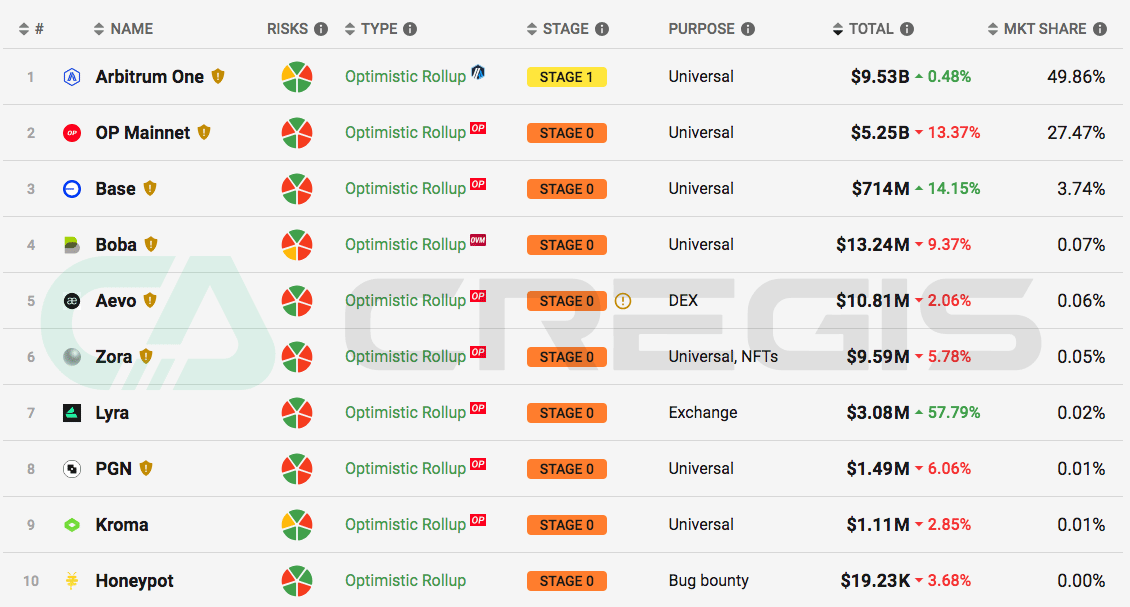

Optimistic Rollups

Arbitrum One

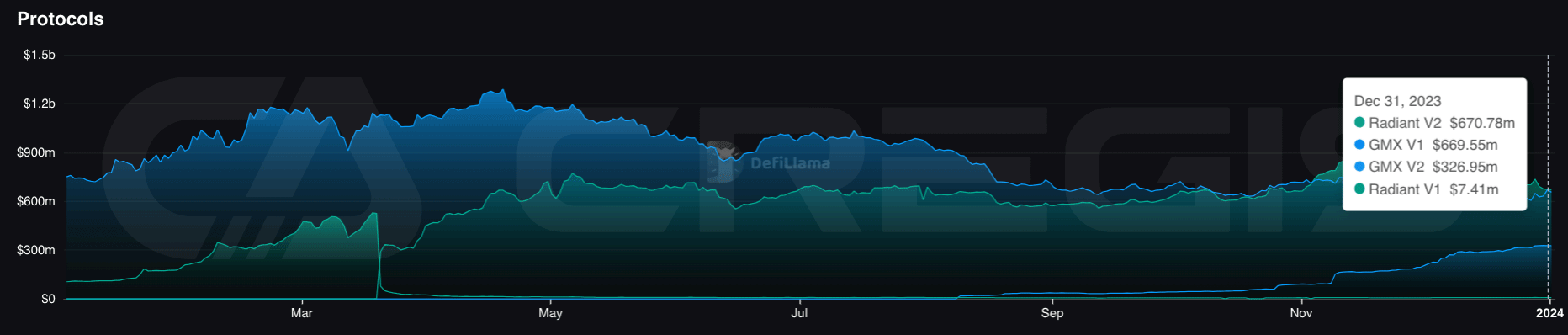

Among the four major Layer 2 solutions currently on Ethereum, Optimistic Rollups (ORs) have the largest total value locked (TVL), with Arbitrum One ranking first. Before the launch of the ARB governance token, Arbitrum One was already the Layer 2 platform with the highest TVL. After the release of the ARB token, over $2 billion in liquidity was introduced into the Arbitrum One ecosystem, with approximately $1.25 billion of that already unlocked, further solidifying Arbitrum One's leading position among all Layer 2 platforms.

(Source: l2 beat)

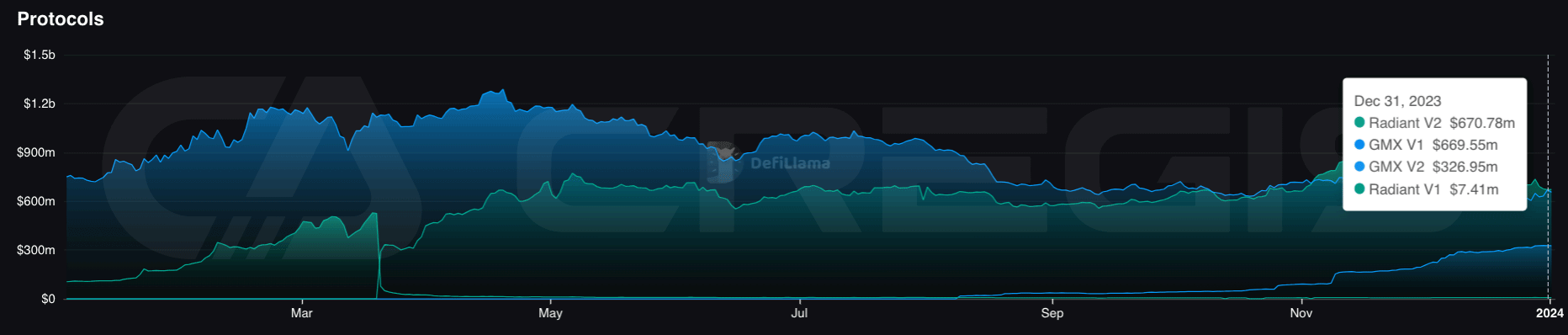

The liquidity introduced by the ARB token has facilitated the growth of decentralized applications (Dapps) on Arbitrum One. The Dapp with the highest total value locked (TVL) on the Arbitrum One platform is the exchange GMX, followed closely by the lending platform Radiant. These two applications account for a significant portion of the TVL market share on Arbitrum One.

(Source: DeFiLlama)

OP Mainnet

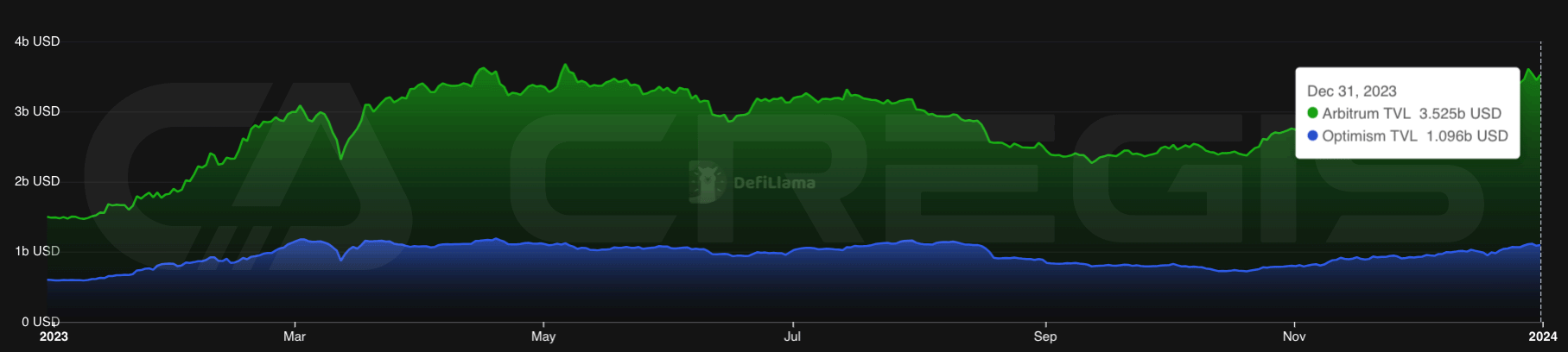

In the realm of Optimistic Rollups (ORs), OP Mainnet, previously known as Optimism, ranks second in total value locked (TVL), with assets exceeding $3.4 billion. The governance token OP for OP Mainnet was airdropped in May 2022, a year earlier than Arbitrum One's airdrop. Although OP Mainnet's TVL growth rate is slower than that of Arbitrum One, its growth trend has been relatively stable.

In July 2023, with the launch of WorldCoin's WLD token on OP Mainnet, the network's TVL saw a significant increase. WorldCoin, co-founded by OpenAI's Sam Altman, aims to create the largest digital identity and financial network. The WLD airdrop is designed to guide network development and incentivize new users to register for the application. To date, over 700,000 users have claimed the WLD airdrop.

(Source: DeFiLlama)

An important milestone for the OP Mainnet was the open-sourcing of OP Stack in August 2022. OP Stack is a development stack that supports OP Mainnet, built and maintained by the Optimism Collective. The current version of OP Stack, also known as Optimism Bedrock, allows developers to use the same technology as OP Mainnet to develop their own optimistic rollup projects.

With the open-sourcing of OP Stack, many projects based on OP Stack have emerged, the most notable being Coinbase's Base mainnet launched in August 2023. Base aims to provide decentralized application (Dapp) services for exchange users. Based on total value locked (TVL), Base has rapidly grown to become the third-largest Layer 2 network.

(Source: l2 beat)

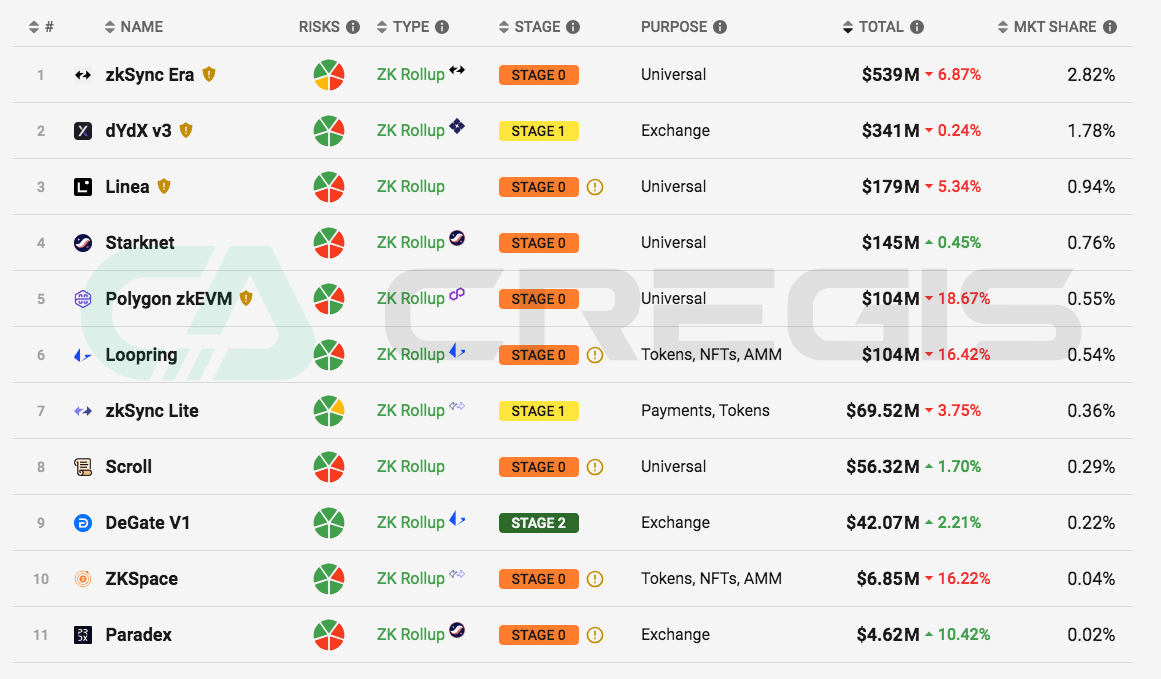

Zero-Knowledge Rollups

Currently, there is no clear leader in the Zero-Knowledge Rollups (ZKR) space. While dYdX previously held the largest TVL share among ZKRs, it has begun transitioning to Layer 1 Cosmos. Currently, the TVLs of zkSync Era and Starknet are $539 million and $145 million, respectively. Although zkSync Era's TVL is significantly higher than Starknet's, part of its TVL comes from the initial zkStnc Lite.

(Source: l2 beat)

Rollups as a Service

As the Rollup ecosystem matures, we are beginning to see rollups used as a versatile tool, not just as a scaling solution. Applications that wish to have a custom execution layer can choose to launch their own rollup, gaining ample block space at the cost of some degree of decentralization and security. Based on this demand, Rollups-as-a-Service (RaaS) applications have started to emerge, providing decentralized application (Dapp) developers with the ability to quickly launch new rollups for deployment. Notable examples include Altlayer, a RaaS framework focused on the Ethereum Virtual Machine (EVM), and dYmension, a RaaS framework focused on Cosmos.

Layer 3

Currently, Layer 2 networks are also beginning to experiment with Layer 3 technologies. For example, Starknet and zkSync Era have both mentioned that theoretically they could build Layer 3 networks on top of existing Layer 2 infrastructure, utilizing the recursive nature of validity proofs. However, these solutions are not currently a priority, as both Starknet and zkSync Era are focused on developing their Layer 2 technologies. Additionally, the use of Layer 3 technologies aims to allow developers to quickly deploy customizable execution environments, similar to the services offered by Rollups-as-a-Service (RaaS).

(4) Cross-Chain Bridges

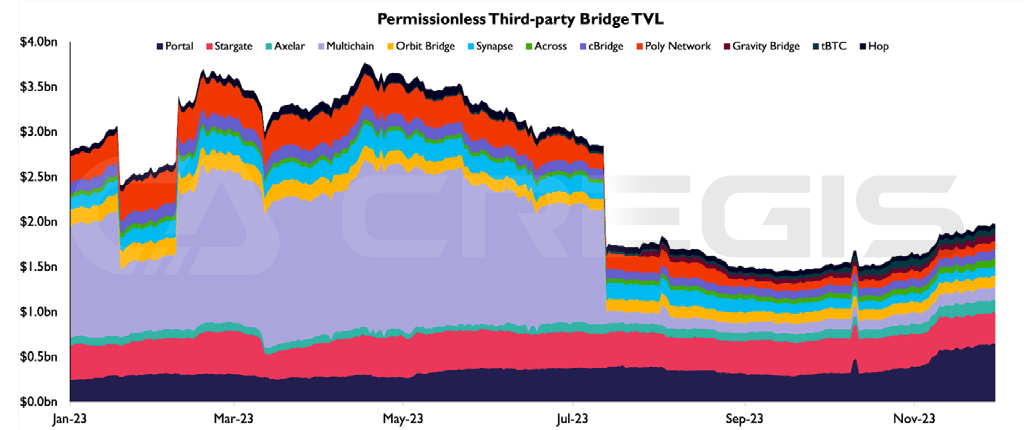

Although Multichain faced security issues in July, bridging technology has maintained its importance throughout 2023. In particular, the Portal bridge, which employs a locking and minting mechanism, has seen steady growth and has become the cross-chain bridge platform with the highest total value locked (TVL). This growth is primarily driven by Solana's resurgence in the fourth quarter, making Portal the main gateway into the Solana ecosystem.

Additionally, the Stargate bridge, based on LayerZero technology and a liquidity pool model, follows closely behind as the second-largest cross-chain bridge platform, maintaining stable total value locked (TVL). Throughout 2023, the cross-chain ecosystem has shown a growth trend, largely due to the ongoing development of Layer-2 technologies.

(Source: The Block)

(5) BTC Layer 2

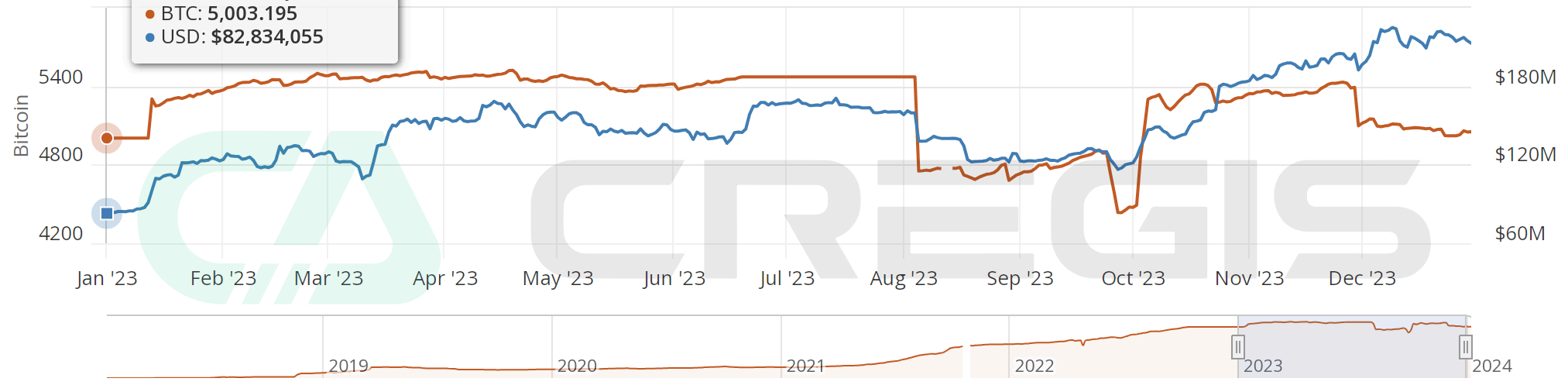

Lightning Network

Bitcoin's Lightning Network is its most well-known scaling solution. Starting from the beginning of 2023, the total amount of Bitcoin in the Lightning Network increased from about 5,000 to a peak of around 5,400. In the same year, its total value locked (TVL) grew from an initial $80 million to about $200 million by year-end, an increase of approximately 150%. The growth in TVL was primarily driven by the rise in Bitcoin prices.

(Source: bitcoinvisuals)

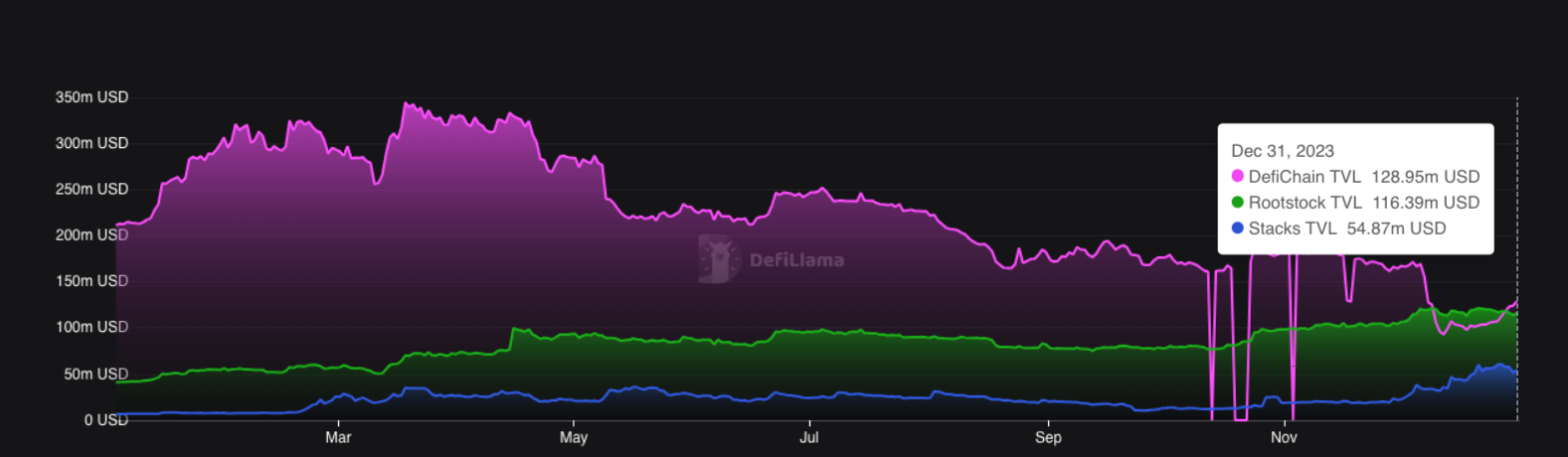

Rootstock, Stacks, and DeFiChain

In addition to the Lightning Network, Bitcoin has several other scaling solutions, primarily based on sidechain Layer 2 technologies. For example, Rootstock, Stacks, and DeFiChain had total values locked (TVL) of $116 million, $54 million, and $128 million, respectively, by the end of 2023, all significantly lower than the Lightning Network's $200 million. Notably, the TVLs of DeFiChain and Rootstock also include the values of their respective native tokens DFI and RSK. From these figures, it is evident that the adoption rates of these sidechain solutions are significantly lower compared to the Lightning Network.

(Source: DeFiLlama)

Ordinals and BRC-20

Bitcoin's Ordinals protocol allows unique identifiers to be assigned to satoshis (the smallest unit of Bitcoin) and utilizes SegWit and Taproot upgrades to reduce transaction fees for storing metadata in satoshis. This protocol enables users to publish non-fungible tokens (NFTs) on the Bitcoin network. Subsequently, the BRC-20 standard, based on the Ordinals protocol, further expanded its functionality to enable token minting. BRC-20 tokens and Bitcoin NFTs have sparked a wave of speculation, increasing on-chain activity on the Bitcoin blockchain and significantly raising the portion of miner fees derived from transaction fees.

(Source: bitinfocharts)

Although the technical architecture of Ordinal NFTs and BRC-20 tokens is not designed to expand Bitcoin's functionality, they do showcase the potential for innovation on the Bitcoin blockchain. Given the limitations of Bitcoin's scripting language, we look forward to seeing more innovations on the Bitcoin blockchain in the future.

BitVM

BitVM is a newly proposed Bitcoin upgrade scheme introduced at the end of 2023, aimed at bringing Turing completeness to Bitcoin. According to BitVM's white paper, the described technical implementation involves "bit-value commitments" and constructing logical gate commitments, allowing Bitcoin contracts to possess Turing-complete expressive capabilities. This approach enables Turing completeness to be achieved without altering Bitcoin's consensus mechanism.

(Source: BitVM White Paper)

Under the BitVM architecture, any logic can be encapsulated and published to the Bitcoin chain, while its execution occurs off-chain. During the off-chain execution process, a "fraud proof" mechanism will be employed to verify the execution results. If an entity wishes to challenge the on-chain publisher's proposal, they can implement a fraud proof on-chain. This mechanism allows the logic of any smart contract to be expressed and verified on-chain while being executed off-chain. Although this method is more complex compared to Ethereum's smart contracts, it brings tremendous potential for Turing completeness to Bitcoin, surpassing the limitations currently exhibited by Bitcoin. Over time, BitVM may usher in a new wave of innovation for Bitcoin.

## 3. On-Chain Applications

(1) Decentralized Finance (DeFi)

Decentralized finance (DeFi) is a form of financial service that does not rely on traditional financial institutions, such as banks or exchanges. It offers users an open and borderless financial service experience, allowing them to access these services without the approval of traditional financial institutions. Since 2020, DeFi has garnered widespread attention and has experienced a series of peaks and troughs. During the previous bull market, DeFi showcased its immense potential as an alternative financial system.

However, events like the collapse of Luna have revealed the potential risks within the DeFi system. Currently, DeFi is still in its early development stage, with many aspects remaining immature and unstable. Additionally, since DeFi operates outside the regulatory framework of traditional markets, it also brings inherent risks.

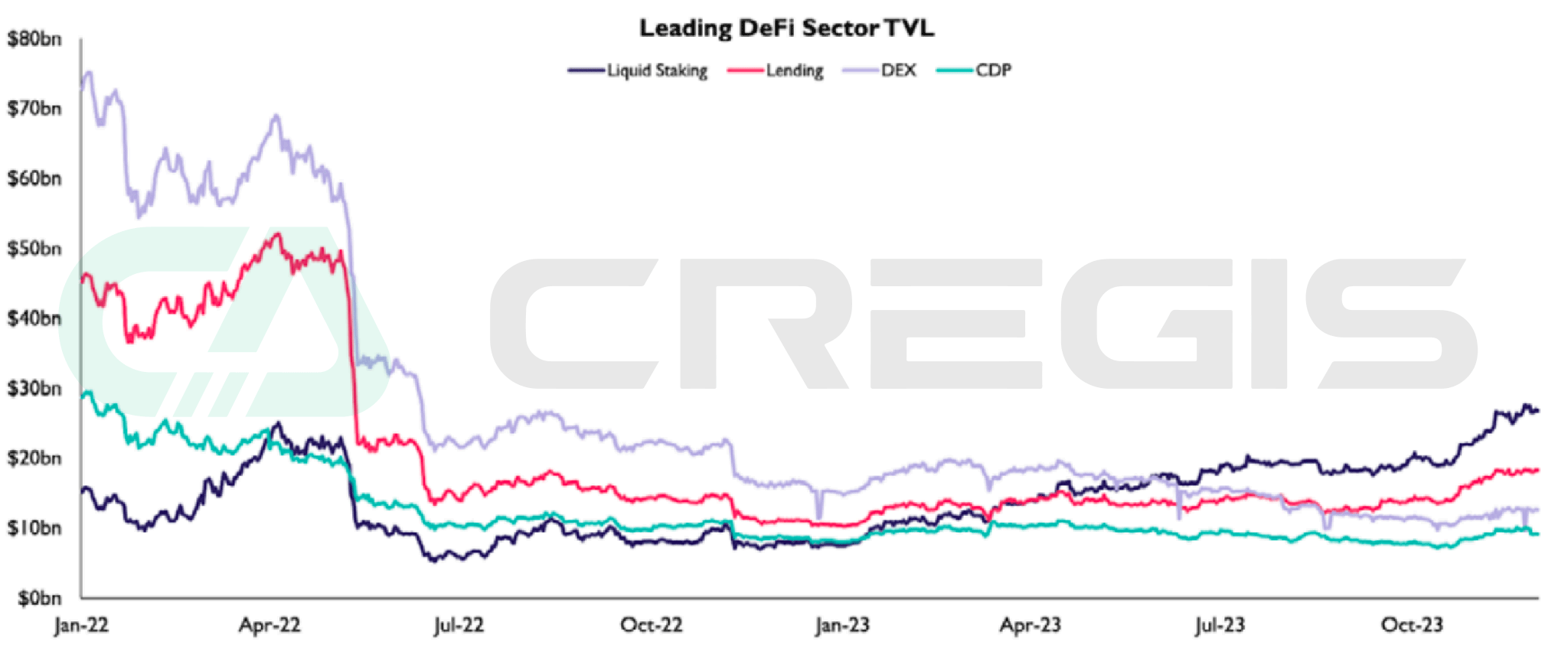

Despite the cryptocurrency market experiencing a winter-like bear market in 2022, the DeFi ecosystem in 2023 has been characterized by integration and resilience. This year witnessed the consolidation of major areas within DeFi, covering key components such as decentralized exchanges (DEX), lending markets, liquidity staking, and collateralized debt positions. Notably, liquidity staking occupies the largest total value locked (TVL) in the DeFi ecosystem, highlighting both the stability of liquidity staking yields and its strong performance in competition.

(Source: DefiLlama)

Decentralized Exchanges

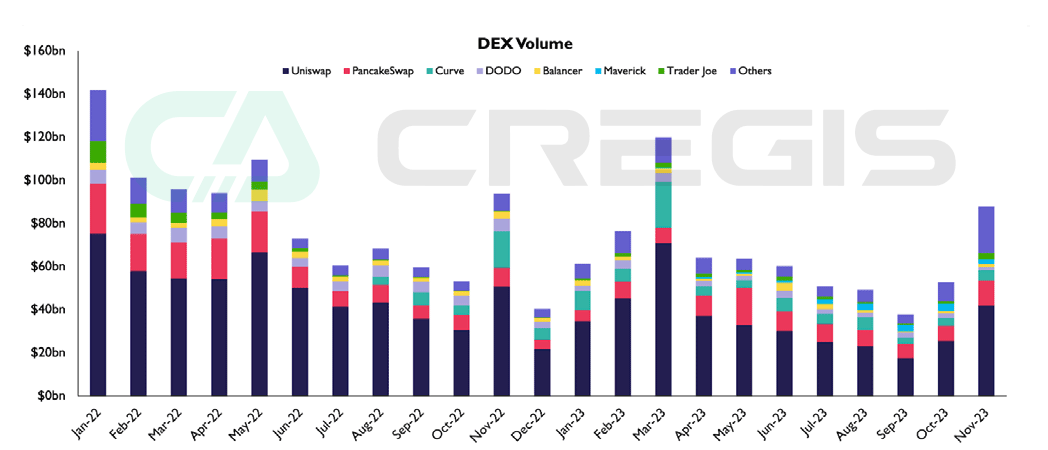

In the first half of 2023, the bankruptcy of FTX heightened concerns about the reliability of centralized custodial institutions, prompting many spot traders to flee from centralized exchanges (CEX) to decentralized exchanges (DEX). The collapse of centralized cryptocurrency projects in 2022 underscored the importance of decentralization and highlighted the unique advantages offered by DeFi.

Affected by the bear market, market interest remained low, leading to fluctuations in DEX spot trading volume in 2023, followed by signs of recovery in the fourth quarter. Throughout 2023, Uniswap maintained its leading position, capturing 53% of the trading share for the year, with most trading volume coming from Ethereum and Arbitrum One.

In contrast, Curve's market share declined from 10% last year to 3.7% this year. The primary reason for this decline is that market contraction hindered the diversity of stablecoins, thereby reducing market demand for stablecoin swap DEXs.

(Source: The Block)

Lending

In the lending sector, Aave continues to dominate, holding over 60% of the total outstanding debt market share, followed closely by Compound in second place. In 2023, lending activity gradually recovered from the deleveraging seen in 2022, showing a steady upward trend.

A noteworthy development occurred in May when SparkLend, a lending platform under the Maker brand, entered the lending market. Meanwhile, a fork project of Aave quickly gained market attention and rapidly grew to become the third-largest lending protocol by total outstanding debt, surpassing $600 million just six months after its launch. SparkLend's uniqueness lies in its provision of predictable interest rates for DAI borrowers, which is the largest decentralized stablecoin by market capitalization, achieved through direct utilization of Maker's credit lines.

Ethereum Liquidity Staking

In 2023, the liquidity staking sector of Ethereum demonstrated significant resilience, becoming a major highlight in the DeFi space. This can be attributed to two main factors: first, in a bear market characterized by low volatility, liquidity staking yields have proven more attractive compared to other DeFi activities. Second, the development of "liquidity staking finance" protocols has enhanced the utility of liquidity staking tokens.

Although liquidity staking demand for ETH appeared to peak in the second half of 2022, it exhibited a rapid growth trend in 2023, and this growth was not affected by the Ethereum Shanghai upgrade and staking withdrawal functionality implemented in April. In the liquidity staking space, Lido continues to lead with a 78% market share, while Rocket Pool holds a solid second place with a 10% market share.

With the increasing development of liquidity staking finance, several other sub-sectors within DeFi began to emerge in 2023. Notably, the tokenization market for real-world assets (RWA) experienced explosive growth. RWA collateralized debt positions have issued 2.8 billion DAI, accounting for over half of the total supply of 5.4 billion DAI. The fees generated from these RWA positions account for 80% of Maker's revenue.

Derivatives

In 2023, decentralized perpetual contract (perps) exchanges exhibited a vibrant development trend, especially in November when perpetual contract trading volume reached its highest point of the year. Although dYdX saw a decrease in market share, it still maintained its leading position as a mature decentralized perpetual contract exchange (DEX). The competition for second place became exceptionally fierce, with platforms such as Vertex, GMX, Synthetix, and ApeX vying for attention. dYdX is gradually migrating from its Ethereum-based StarkEx ZKR to a Cosmos sidechain, introducing new competitive factors into the perpetual contract DEX market.

Meanwhile, with the launch of Aevo in the third quarter, decentralized options trading began to gain momentum. Aevo quickly became the leading decentralized options exchange, with trading volume far exceeding that of Lyra. The dynamics of decentralized derivatives trading throughout the year showcase the early characteristics of the industry and suggest that there is immense potential within the market as it continues to develop and mature.

(2) Non-Fungible Tokens (NFT)

In 2023, the non-fungible token (NFT) market is undergoing a pivotal transformation, indicating that NFT assets are moving towards financialization.

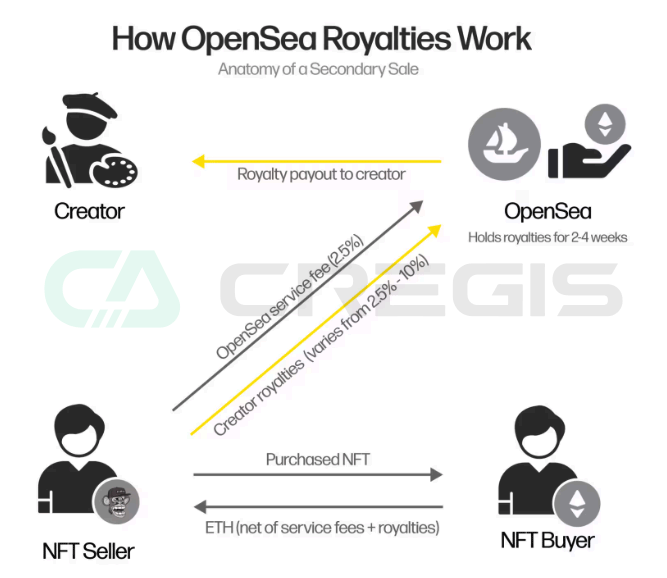

OpenSea and Blur are two active platforms in the NFT market, each with different business models. OpenSea's business model relies on transaction fees, charging a percentage fee from each NFT transaction as its revenue source. However, this model has the drawback of impacting market liquidity. In contrast, Blur's business model prioritizes efficiency and liquidity over the traditional creator reward fee structure, thereby disrupting the entire industry.

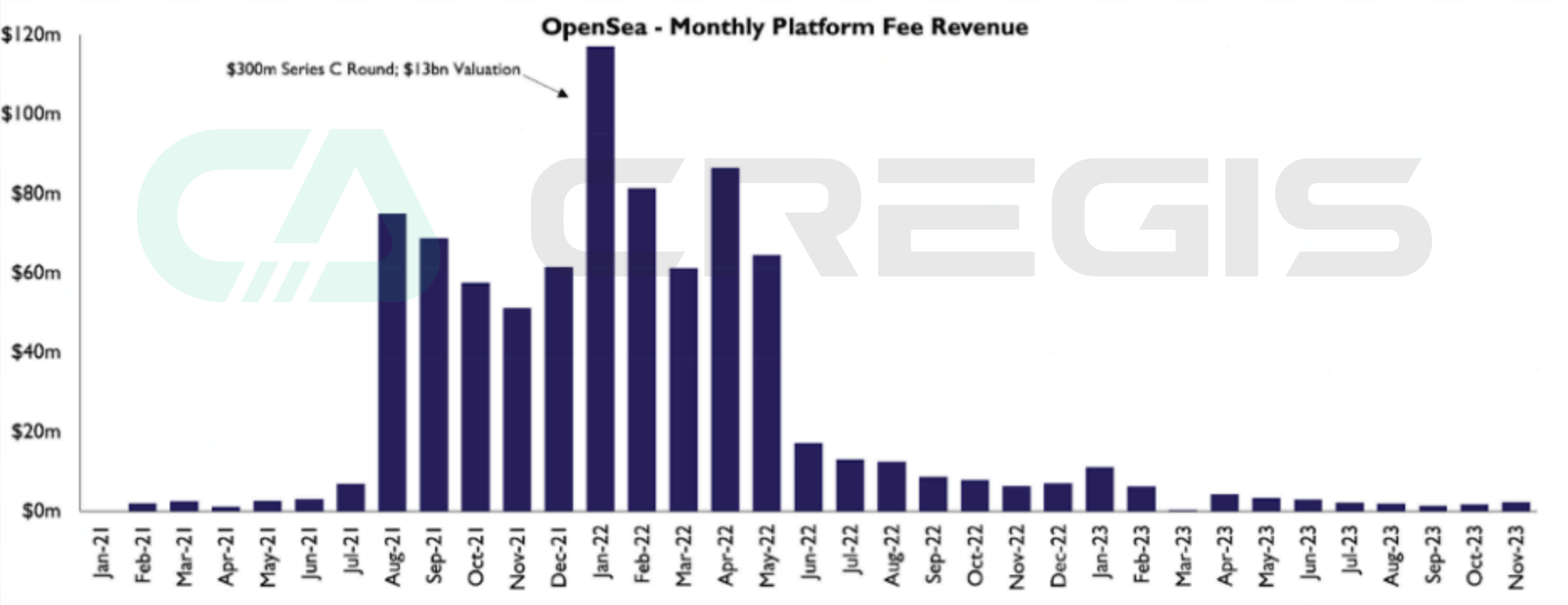

At the beginning of 2022, OpenSea became a giant in the NFT ecosystem, achieving a valuation of $13.3 billion after completing a $300 million Series C funding round, capturing over 80% of the trading volume in all secondary markets. Its revenue model heavily depended on platform fees, with monthly revenues ranging from $5 million to $120 million, and by early 2022, its annual revenue was expected to exceed $1 billion.

However, by mid-2023, the situation reversed, and their platform revenue decreased to less than $2 million per month. This significant decline (nearly a 90% drop from previous earnings) was primarily due to the rise of "zero-fee platforms," with users shifting transactions from platforms like OpenSea to zero-fee platforms like Blur. The NFT market is reevaluating traditional fee structures in favor of liquidity-focused strategies.

(Source: The Block)

In OpenSea's fee structure, NFT royalties typically range from 2.5% to 10% of the final sale amount. Sellers are required to pay royalties along with the transaction fees charged by OpenSea for each transaction. While Blur's business model has improved liquidity and trading volume, it has significantly reduced the royalty compensation for NFT creators, raising concerns about sustainability in the market.

(Source: Galaxy)

NFT Finance

2023 marks a critical turning point for the non-fungible token (NFT) market, signifying a shift towards innovative liquidity solutions. NFT lending platforms have played a crucial role in this transformation, providing asset holders with a new capability to unlock the value of their digital assets. This represents a significant advancement in the financialization of NFTs, particularly for traditionally illiquid non-PFP collectibles.

In the NFT trading space, platforms like OpenSea primarily cater to retail trading. In contrast, NFT lending platforms focus on serving risk-averse and infrequent trading user groups, introducing new leverage mechanisms akin to traditional asset backing, thereby enriching the ecosystem. This market shift has led to a significant increase in lending volume, surpassing $3.3 billion.

In the NFT finance sector, the Blend platform launched by Blur has taken the lead, with lending volume reaching $197 million in the second quarter of 2023. With over 6,100 borrowers and 3,300 lenders joining, Blend's activity has significantly driven overall lending volume growth, increasing by 270% since the beginning of the year. However, in-depth analysis shows that 10% of lenders and 26% of borrowers contributed to the majority of the trading volume.

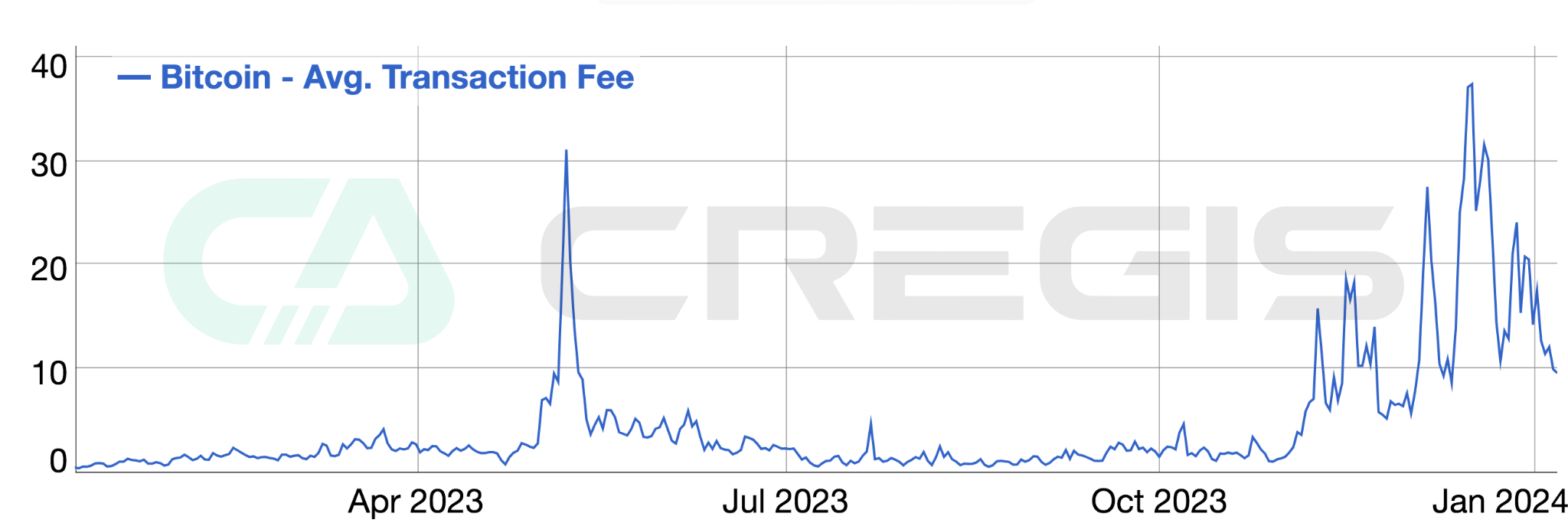

Bitcoin NFTs

The Ordinals protocol developed by Casey Rodarmor allows data to be directly embedded into the Bitcoin blockchain. This protocol numbers the smallest unit of Bitcoin—satoshis (Sats)—and allows various content to be inscribed on these satoshis, from images to code, thus creating a new type of Bitcoin NFT. During the approximately 10 months of Ordinals development, Bitcoin developers built NFT tools similar to those on other major Layer 1 blockchains like Ethereum, Polygon, and Solana.

Throughout 2023, the Bitcoin ecosystem underwent significant changes due to the development of inscriptions. Since the beginning of the year, miners have cumulatively earned over $530 million in total fees, with approximately $90 million stemming from Ordinals-related activities. These inscription activities have led to increased fees and congestion in the Bitcoin mempool (transaction pool), with the total byte size of transactions waiting for confirmation reaching historical highs.

To achieve faster transaction confirmations, users began paying higher fees, intensifying competition for the limited space in each block. At the beginning of 2023, transaction fees began to rise significantly, peaking around April, primarily driven by the creation of BRC-20 meme tokens.

(Source: Blockchain)

(3) Decentralized Social

FriendTech & SoFi

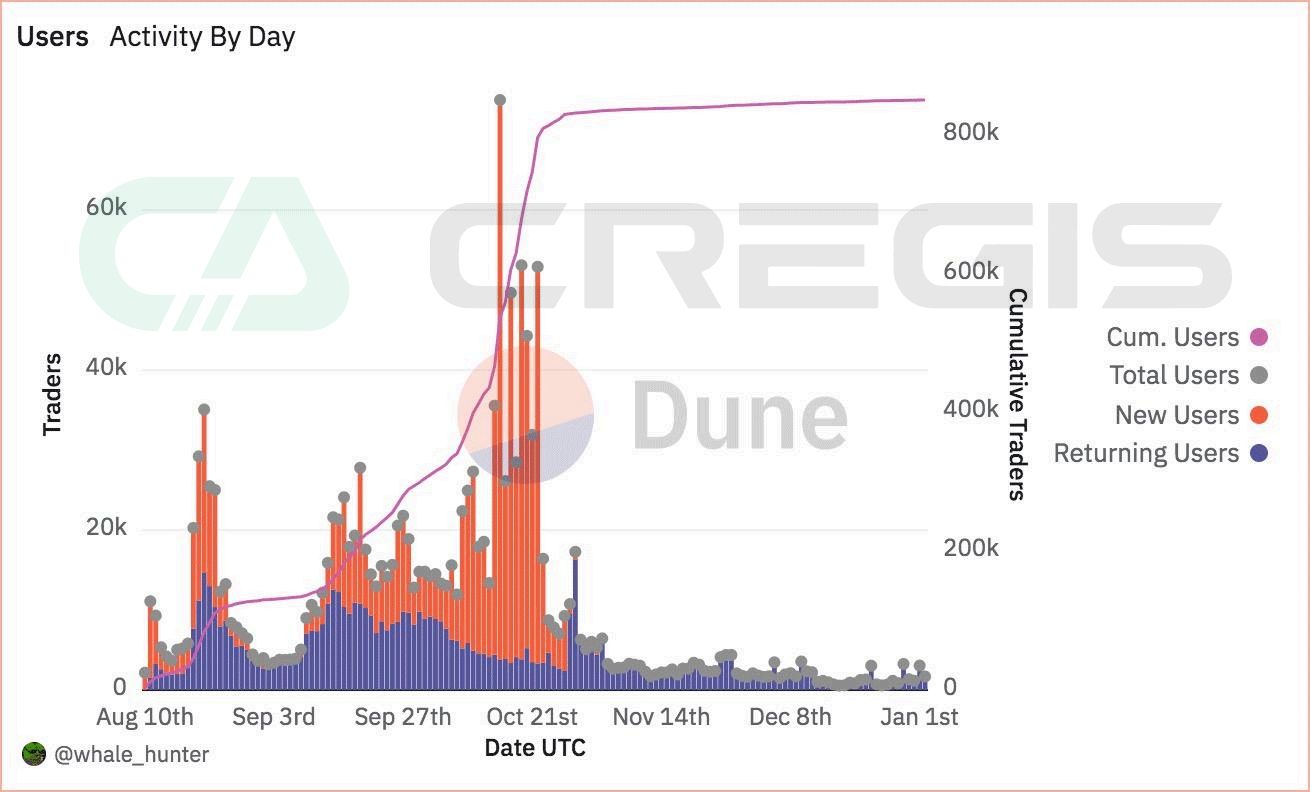

FriendTech is a social media platform that integrates cryptocurrency features, branding itself as a "friend marketplace." Similar to other non-crypto social media platforms still in testing phases, Friend.tech implements an invitation code system, requiring users to register by obtaining invitation codes from existing users. The platform has introduced a unique mechanism that allows users to purchase "keys" to send messages to other users. This novel feature has attracted a large number of users. Since its launch less than three months ago, Friend.tech has garnered significant attention from the community, with over 900,000 users and a trading volume of $475 million.

(Source: Dune)

The success of FriendTech is rooted in the fundamental human need for social interaction. On this platform, users can publicly display their "scores" or values, gaining recognition and respect from other users. This not only satisfies users' intrinsic desires for social validation and affirmation but also enhances their sense of participation and belonging on the platform.

## Contact Us

Official Website

Discord

Risk warning Risk warning

Risk warning Risk warning