Wintermute OTC Annual Report: Trading volume in the second half increased fourfold, TradFi resurgence

Apart from BTC and ETH, payment-related assets are the largest category by trading volume, with TradFi shifting more trades to altcoins.

Apart from BTC and ETH, payment-related assets are the largest category by trading volume, with TradFi shifting more trades to altcoins.Author: Wintermute

Compiled by: Felix, PANews

The cryptocurrency market in 2023 experienced a series of peaks and troughs. From the rebound at the beginning of the year to the fluctuations in the middle of the year, it ultimately ended with an optimistic market sentiment (driven by expectations of spot ETF approvals). As market activity slowed down, the industry narrative shifted to Build. Last year, Wintermute focused on expanding its OTC business and developing new products.

Recent milestones include the integration of Wintermute Asia with CME, significant upgrades to over-the-counter options products, and the development of more derivative products. Since its launch in November last year, Wintermute Asia's options trading volume has reached $210 million, with counterparties showing exponential growth in demand for the product.

As the new year begins, Wintermute shares business dynamics and reflects on some trends observed in OTC throughout 2023.

OTC trading volume grew over 400% in the second half of the year as trading volume shifted off-exchange

Despite the market downturn in 2023, all verticals of Wintermute continued to grow. In the spot market, although total on-exchange trading volume decreased by about 13% from the first half to the second half of the year, off-exchange trading volume grew over 400% during the same period.

Although the off-exchange trading volume in the first half of 2023 was comparable to that of the second half of 2022, it initially showed a decline. This indicates that while the scale of trading decreased, counterparties' crypto trading strategies remained steadfast. As the market warmed up in the second half of 2023, trading activity significantly increased, with the number of trades growing over sixfold, exceeding 29 million trades. During this period, a record weekly off-exchange trading volume of over $2 billion was observed.

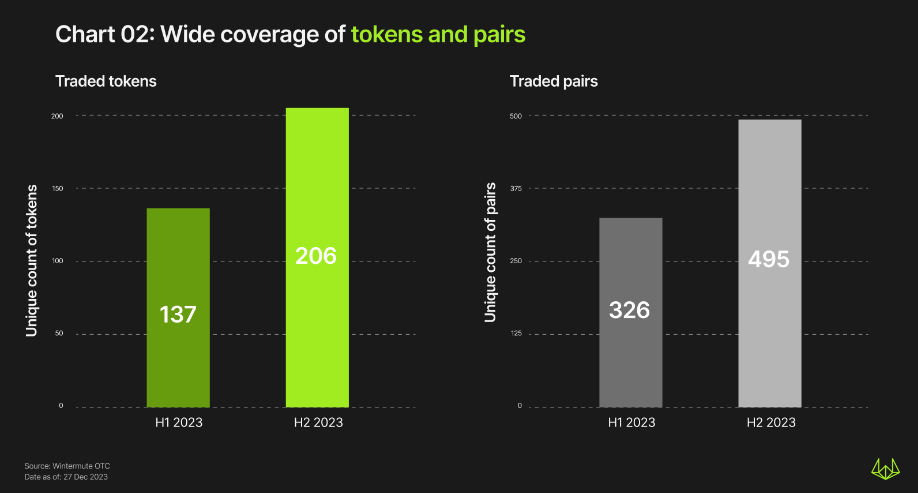

In 2023, Wintermute provided OTC trading for 206 assets and 495 trading pairs. Below are the overall asset trading trends observed by Wintermute.

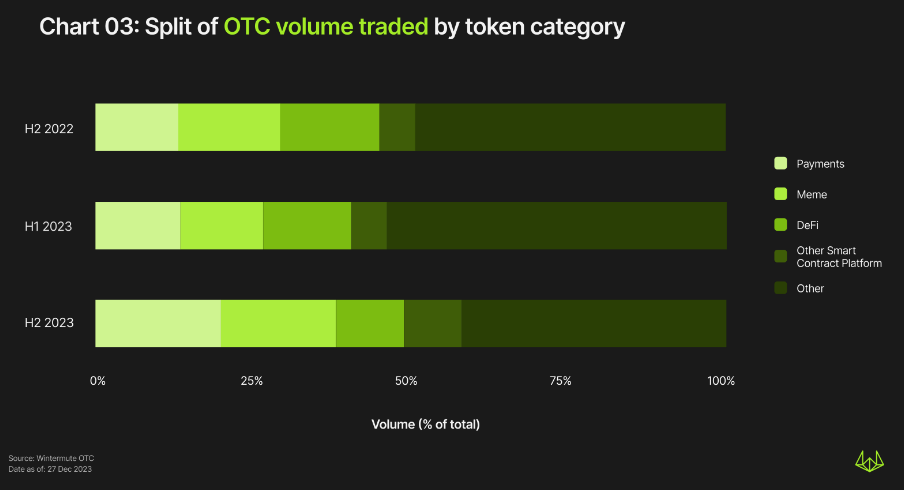

Payment-related assets are the largest category of cryptocurrencies by trading volume, second only to BTC and ETH

Excluding BTC and ETH (which consistently hold the first and second positions), payment-related assets have the highest trading volume and market share. The market share of payment-related assets grew from 13% in the second half of 2022 to 20% in the second half of 2023.

The outcome of the SEC-Ripple case has somewhat driven the growth of payment-related assets, particularly XRP.

Other categories in the second half of 2023 include Meme, DeFi, and other smart contract platforms. These categories have maintained strong market shares, accounting for 37% and 38% in the second half of 2022 and the second half of 2023, respectively.

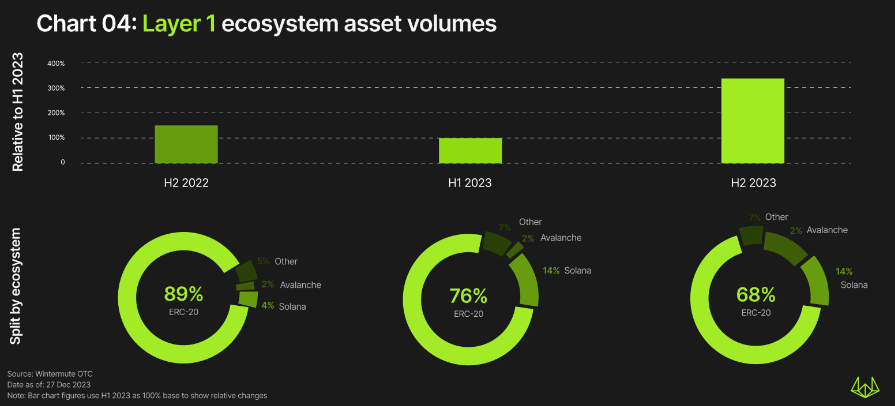

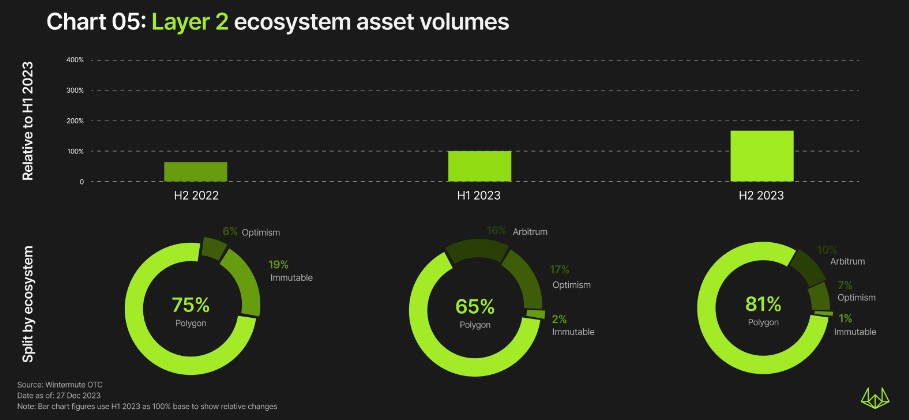

L1 and L2 trading volumes continue to grow, with ETH and MATIC leading the way

The off-exchange trading volume of L1 assets followed the overall trend of off-exchange trading volume, decreasing by about half from the second half of 2022 to the first half of 2023, then skyrocketing by 350% in the second half of 2023. Ethereum had the largest trading volume, accounting for 68% of the market share.

It is noteworthy that Ethereum's market dominance has gradually declined from the second half of 2022 to the second half of 2023.

In the second half of 2023, Solana, Avalanche, Cardano, and Polkadot made it into the top five by trading volume. Compared to Ethereum, most other L1 assets maintained strong trading volumes in the first half of 2023, but Polkadot was an exception, experiencing a slight decline.

Compared to L1, L2 trading activity decreased by about 30 times, with the largest declines seen in Polygon, Arbitrum, and Optimism. However, overall L2 trading activity continued to grow, increasing by about 160% from the second half of 2022 to the second half of 2023.

DeFi remains strong, with a slight increase in market share and a significant increase in nominal trading volume

While the nominal trading volume of DeFi grew by about seven times from the second half of 2022 to the second half of 2023, its market share decreased from 16% to 11%. In DeFi, Yield Farming had the largest trading volume, followed by Oracles, Lending, and DEX assets.

Throughout 2023, Yield Farming maintained a strong dominance, accounting for about 35% of overall DeFi trading volume, with nominal trading volume increasing more than ninefold during the same period.

From the second half of 2022 to the first half of 2023, the trading volume of oracle-related assets saw a slight decline (about 30%), and market share decreased from 11% to 8%, but rebounded in the second half of 2023, accounting for 26% of overall DeFi trading volume. This was mainly at the expense of DEX asset share. Despite DEX assets' nominal trading volume increasing by over 3.4 times, their market share in DeFi significantly decreased (from 31% to 13.5%).

From the first half to the second half of 2023, the market share of lending-related assets increased by 10 percentage points (from 13% to 23%).

From the second half of 2022 to the first half of 2023, the nominal trading volume of derivative assets initially surged tenfold, with market share increasing from 0.6% to 6.9%. However, by the second half of 2023, the market share of derivative assets fell to 0.5%.

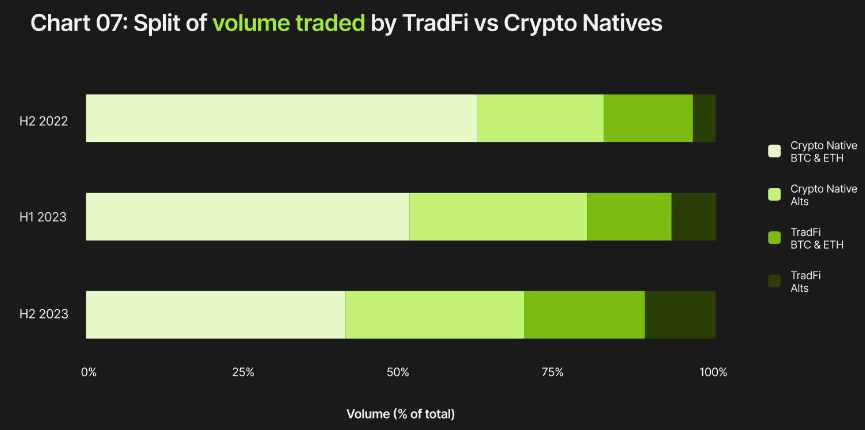

TradFi resurges and shifts towards altcoin trading

In terms of overall trading volume between Crypto Native and TradFi, the market share ratio was 81%:19% in the second half of 2022. In the second half of 2023, TradFi made a comeback, adjusting the ratio to 72%:28%. This indicates that TradFi's interest rebounded again in the second half of 2023, and this interest is expected to continue growing into 2024.

In each period, BTC and ETH dominated trading volume among both TradFi and Crypto Native counterparties.

However, a deeper analysis reveals some interesting phenomena. In the second half of 2022, BTC and ETH's dominance in both counterparty categories was evident, with Crypto Natives' trading volume market share totaling 82.7% (BTC at 44.9%, ETH at 32.8%), and TradFi's trading volume market share at 94% (BTC at 62%, ETH at 32%).

This phenomenon changed in the second half of 2023, with both counterparty categories seeing BTC and ETH market shares decline by over 15%. Crypto Natives' trading volume market share accounted for 65.3% (BTC at 49.9%, ETH at 15.4%), while TradFi's decline was more significant at 72.1% (BTC at 50.3%, ETH at 21.8%). An increasing proportion of trading volume in non-BTC and non-ETH assets indicates a growing interest in altcoin trading.

These trends suggest that TradFi's interest has not only resurfaced but is also becoming more diversified.

Aside from BTC and ETH, the trading volume of Crypto Native counterparties in Solana and payment-related assets grew the fastest. In contrast, for TradFi counterparties, DeFi-related assets saw the most significant growth.