Galaxy: Will selling block space be a good business?

The key objective of this article is to evaluate block space as a commodity product, as well as the production of block space as an economic model.

The key objective of this article is to evaluate block space as a commodity product, as well as the production of block space as an economic model.Author: Will Nuelle

Compiled by: Deep Tide TechFlow

Introduction

New technologies give rise to new business models. Over the past thirty years, many renowned investment firms have established their practices around software investments. Software is primarily a technological revolution, but it is also a revolution in business models driven by technology. "Software as a Service" (SaaS) is a model derived from the replicability of bits, characterized by zero marginal cost of replication, annual recurring revenue, and high switching costs. Investment firms like Insight Partners claim that SaaS is the best business model ever, and their success stems from their deeper understanding of this model than anyone else.

New technology platforms create powerful new business models and entirely new markets. These are often good places to seek excess investment returns. So far, there are only four business models in the crypto space that can produce deep and lasting product-market fit—two of which are existing (SaaS and exchanges), one is a familiar model fork (stablecoins), and one is entirely new (block space):

Software as a Service (SaaS): Software companies like Fireblocks and Chainalysis sell their software through subscriptions. Other companies, such as Alchemy, sell their software services using a usage-based pricing model. Anchorage, Figment, and Blockdaemon are primarily software companies with asset management-related business models.

Exchanges: Crypto tends to financialize everything, meaning that revenue from trading volume has become a stable and viable business model. This includes centralized (off-chain) exchanges, decentralized (on-chain) exchanges, NFT marketplaces, and more.

Stablecoins/Lending: Stablecoins are an example of a familiar net interest margin business model, with the unique limitation that they create an exogenous incentive (on-chain utility) for holders to deposit with the issuer without expecting deposit returns. Over time, tokenized assets should also belong to this broader category.

Block Space: The business model of selling computational resources as a special commodity on an operational basis leads to a price * quantity = quantity model. Block space has persistent demand network effects, creating a defensible moat for winners.

The key goal of this article is to assess block space as a commodity product and the production of block space as an economic model. We cover pricing, metrics, fees, L1, L2, call data and compression, EIP-4844, and more.

Even if you don't believe that block space has a "business model," the sales of block space (e.g., total transaction fees) are the purest signal of product demand and should be used to differentiate between different block spaces.

Block Space as a Product Purchased by Consumers

Block space as a product. It is important to clarify that the producers of block space are not necessarily individual enterprises or companies. They can be decentralized networks composed of individuals and companies that execute the rules of public blockchains like Bitcoin or Ethereum. Whether centralized companies or decentralized blockchains, block space is a product sold to consumers globally every 12 seconds.

A blockchain is a new type of computer that produces a unique form of computation—one in which global consistency exists. Blockchains are the infrastructure solution to the problem of value duplication on the internet (the internet is better at handling text, JPGs, etc., than currency), and block space is the commodity sold to consumers to alleviate this problem. And consumers do pay for it, with annual payments ranging from $3 billion to $10 billion from 2021 to 2023.

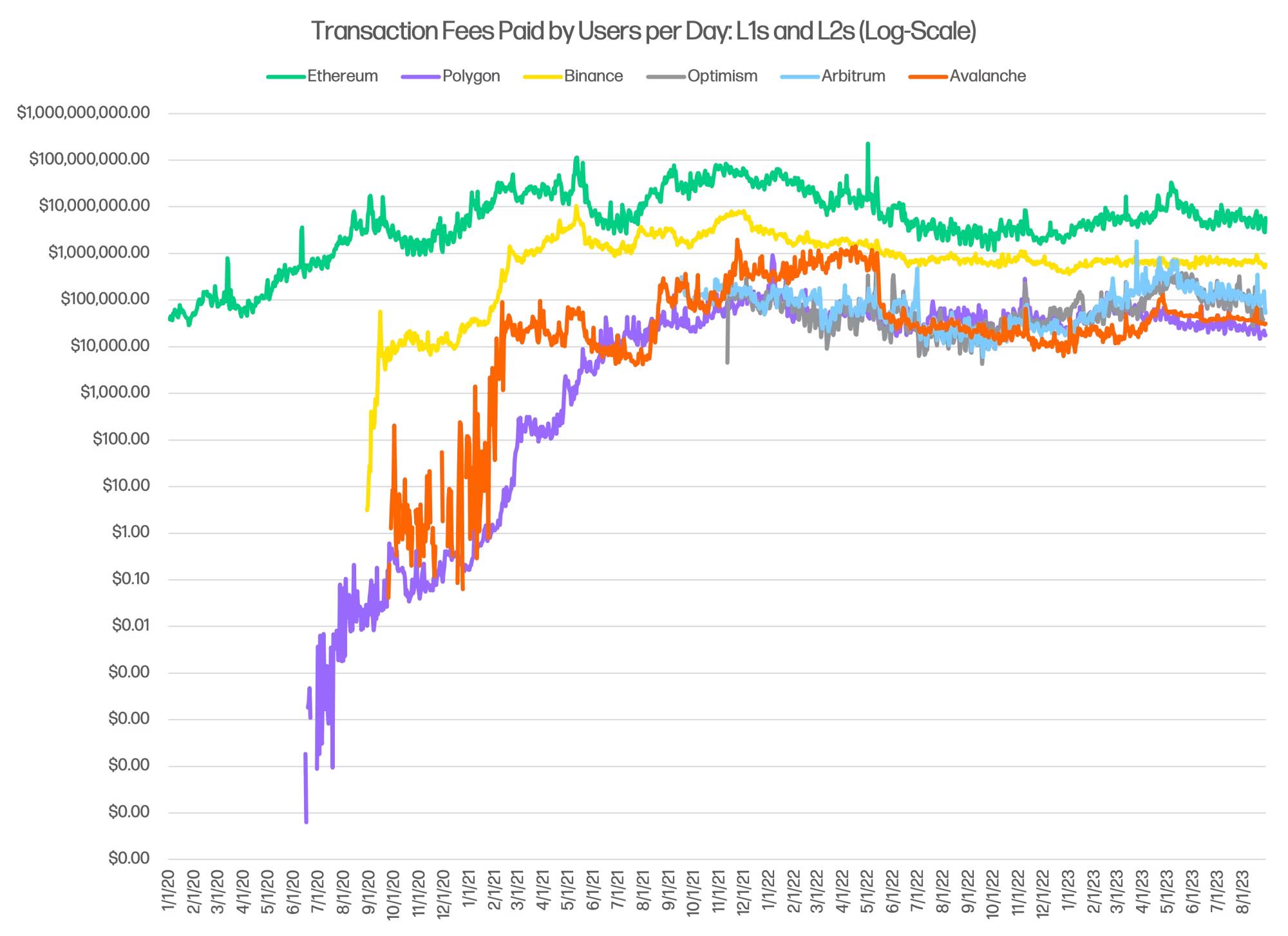

Gas prices are a signal of demand for block space (block space itself is a fusion of computational, storage, and bandwidth resources). There are multiple sellers of block space in this market—all L1s, L2s, sidechains, etc., are producers and sellers of block space. Ethereum, Avalanche, Arbitrum, Optimism, Polygon, and Binance Smart Chain are all producers and sellers of block space.

Block space is a network effect-based business, where network effects can form around applications, developers, capital, and users, driving sustainable increases in unit prices. Generally, when there are network effects around a seller's block space, consumers are willing to pay more for each transaction; consumers need to use block space that other applications and users are also using.

Every dollar of capital deployed on Ethereum attracts more application developers, who then attract more users through interesting applications, and so on, leading to viral growth for social media applications. In short, if users can do more with block space on Ethereum compared to Avalanche, as Chris Ahn of Haun Ventures wrote, "becoming more efficient through scale is the ultimate form of defensiveness."

Network effects partially explain the persistent differences in block space sales prices among sellers:

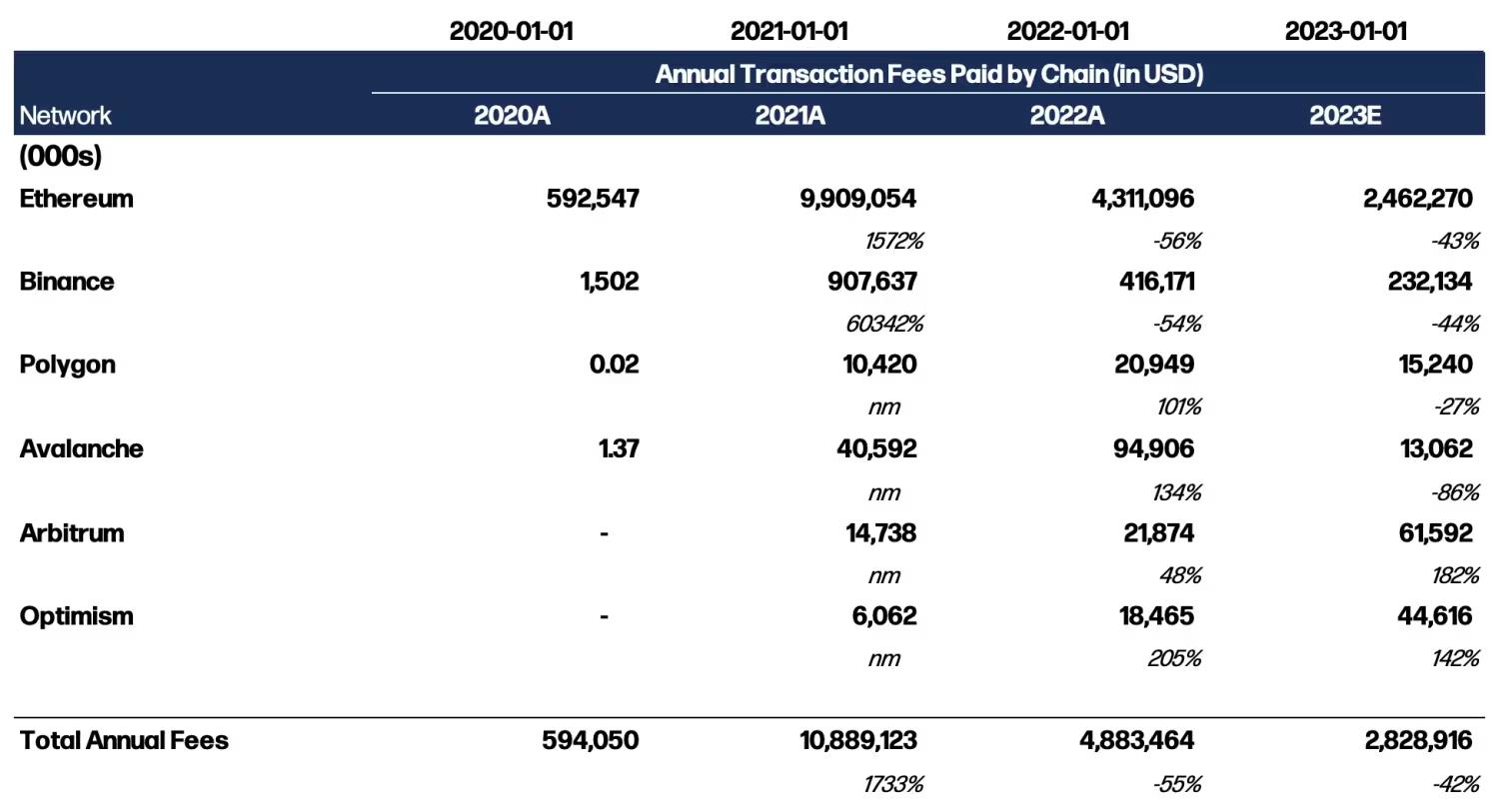

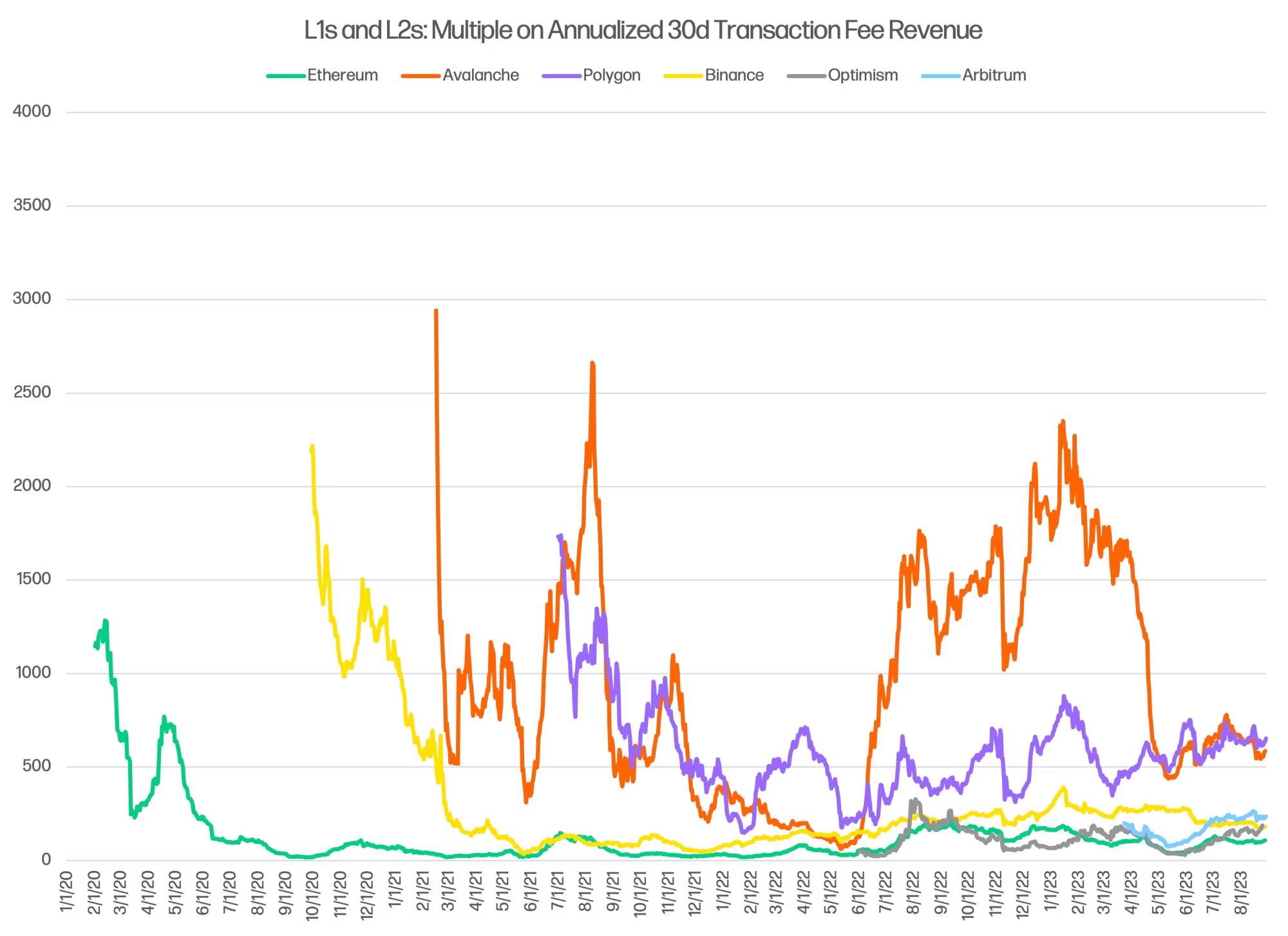

The amount of transaction fees paid by consumers is a measure of total demand for block space. As blockchain network effects expand (e.g., Polygon at the end of 2020), daily fees paid follow an exponential growth trajectory. While network effects exist, the market share of block space is affected by ongoing internal rotations. For example, in the table below, fees for Avalanche and Polygon grew by over 100% year-on-year in 2022, while fees for Arbitrum and Optimism grew by over 142% year-on-year in 2023, indicating a market sensitive to changes in applications, developers, and users. In Ethereum, pricing was initially done through first-price auctions (consumers bidding to join the most recent block) and is now done using a PID controller with EIP-1559 (prices dynamically adjust up and down based on recent demand signals).

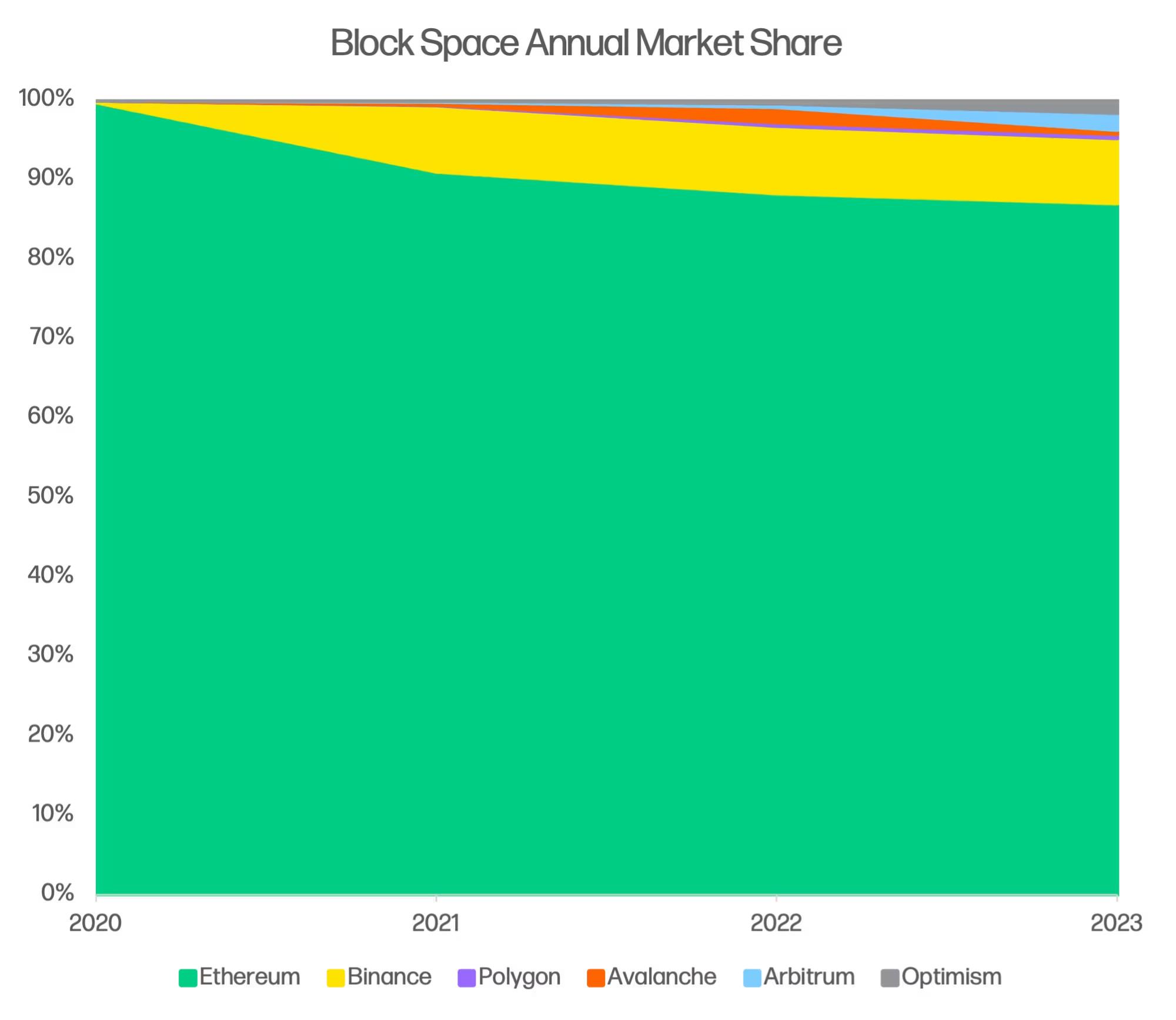

The table "Annual Market Share of Block Space" shows the annual transaction fees of six major fee-charging blockchains (e.g., Solana). Since 2021, total fees have been consistently declining, with Ethereum being the dominant factor, but the entire block space market has achieved a 47.7% compound annual growth rate (CAGR) since 2020. The table notes some significant "rotation trades," such as the Alt-L1 rotation in 2022 (and Polygon), as well as the rollup rotation in 2023.

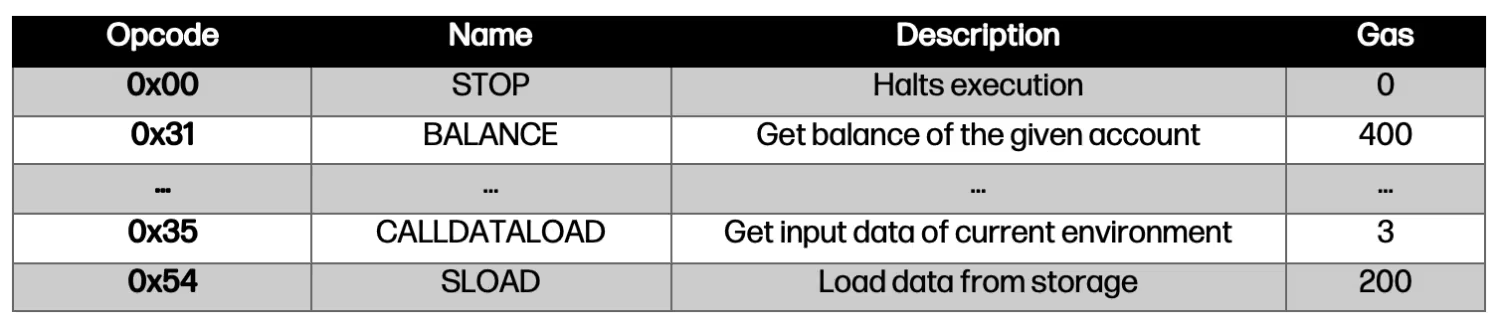

Consumers purchase access to resources on a per-transaction basis—essentially buying per operation ("opcode") at the moment of execution. They purchase the right to computing and bandwidth resources for a fixed term, as well as indefinite storage rights. In the Ethereum Virtual Machine, each operation has a resource cost (Gas), which is assigned a price at execution. The chart below shows some notable EVM operations and their resource costs:

Another point to note is that under this arrangement, we see the emergence of a new paradigm of business models. The uniqueness lies in the fact that consumers bear the cost of accessing block space, reversing the decades-long tradition of companies and startups purchasing rack space or paying AWS bills to provide products to customers. Today, applications on the blockchain can run with zero additional costs once deployed, as users pay for the operational costs. Account abstraction may lead to future applications covering users' Gas fees, returning block space costs to startups and enterprises, similar to the models we see today with rack space and AWS.

Does the Market Trust Long-Tail Block Space More, and Is It Justified?

The ratio of market capitalization to annual transaction fees shows the market's valuation of each dollar of fees generated by blockchain networks. A higher multiple indicates that the market assigns more trust to each dollar of fees in the market capitalization. Generally, higher multiples are assigned to assets that are perceived to have (i) stronger long-term growth prospects, (ii) better conversion of total revenue into profit (i.e., higher profit margins), and (iii) more stable and predictable future growth and profits.

Using this multiple chart, the market's valuation of Ethereum's "paid fees" is the lowest among the six blockchains, at about 100 times its annual fees. At first glance, this seems somewhat counterintuitive: Ethereum is striving to become a "macro asset," like Bitcoin, and should command a store of value premium as a "currency," in addition to the monetary premium from its deep liquidity, used for staking in the protocol and as collateral on-chain. The store of value premium should be higher compared to Avalanche, Polygon, Arbitrum, etc. Qualitatively, Ethereum also possesses stronger and more enduring network effects, which should support a relative premium.

On the other hand, the market may also reflect that Ethereum has a larger capacity limitation of 15 transactions per second, and over time, the growth of Ethereum fees may be discounted. The growth of Ethereum fees can only come from rising Gas costs, while Optimism and Arbitrum can earn more by scaling and increasing demand. Additionally, Ethereum is currently at a disadvantage as other chains capture market share from it. The rotation to new alternatives will bring growth to other chains that can support higher scales.

Production Costs of Block Space

The deeper question is not how much each unit of block space earns but rather what the cost of producing each unit of block space is. This is where the interesting differences lie.

Layer-1 blockchains like Ethereum and Avalanche use physical token incentives to produce the consensus-required anti-sybil mechanisms—proof of work and proof of stake. As discussed above, consensus and data availability are what differentiate block space from ordinary computation. The incentives that produce this effect are the costs of creating block space for L1s.

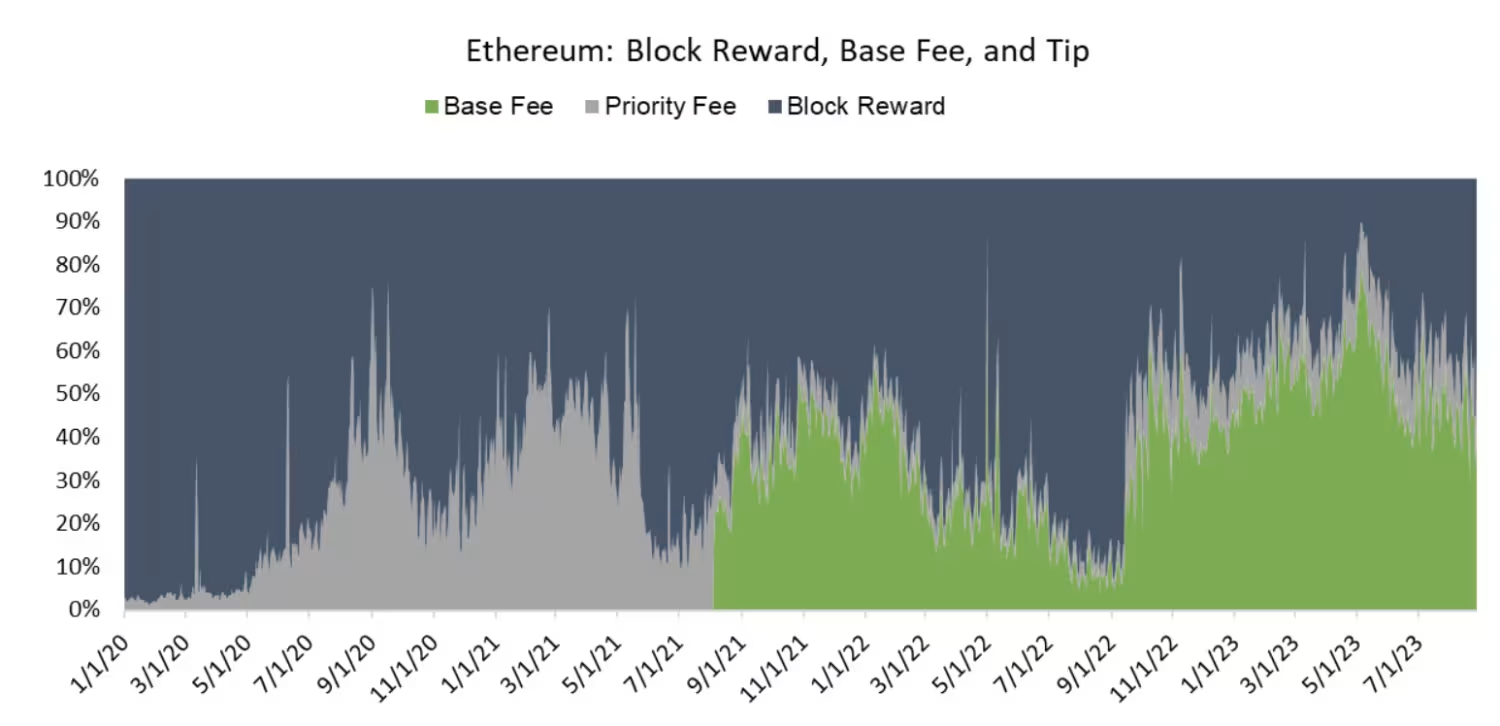

Each Ethereum block consists of a base fee, priority fee, and block reward. The base fee and priority fee are components of transaction fees under EIP-1559. The base fee is burned by the protocol, reducing the supply of ETH, while the priority fee is paid to validators. The block reward is the new primary issuance.

To incentivize block production under proof of work, Ethereum pays an average block reward of about 12,600 ETH daily, with new primary issuance reaching up to $60 million daily at market peaks to incentivize the creation of block space. In proof of stake, the situation is more complex: incentives are determined by a complex function, under which Ethereum pays about 1,850 ETH daily (proportional to the number of validators) since the merge. In either case, these incentives paid to miners/validators are the sales costs of block space (cost of goods sold).

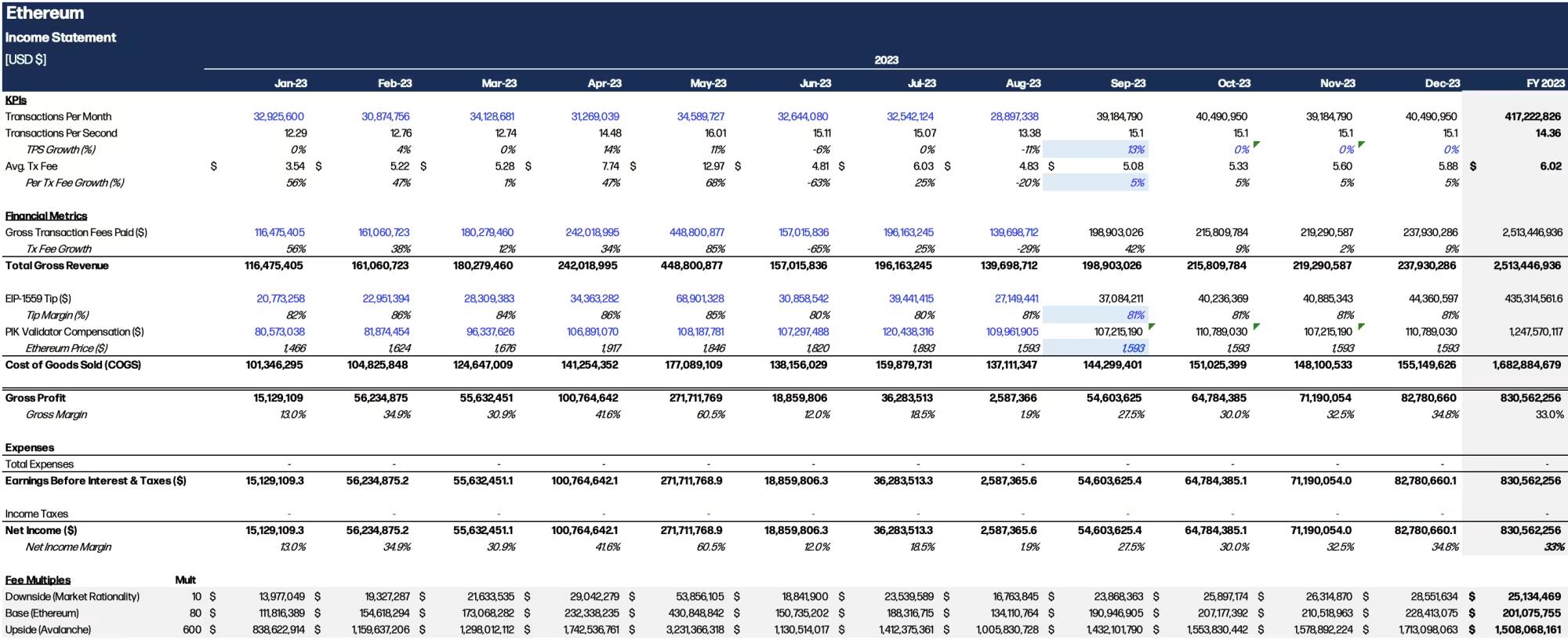

Describing Ethereum's block space sales in the form of an income statement. The income statement below converts transaction fees and costs (cost of goods sold) into dollars for proper analysis, as consumers often still price their transactions in dollars. It is important to note that the Ethereum Foundation and related researchers are not concerned with optimizing transaction fees paid, nor is it a clear goal of the community. The goal is clearly the opposite: to provide cheap and scalable block space.

There is a fundamental paradox in block space as a business model: supply constraints raise transaction fees but hinder the core objective of L1 systems, which is low-latency and cheap computation.

There are many points worth discussing regarding this Ethereum profit and loss statement, but I will simplify it into a few key points:

1. Throughput stability requires fee growth: In the foreseeable future, Ethereum's transaction throughput will not exceed 16 transactions per second, so the only way for its revenue to grow is to increase transaction fees. This may happen as the economic density brought by batching on L2 will push fees higher.

2. Fees are highly cyclical: Block space is not a business with fixed income (yet). It is influenced by users.

3. Net income margin equals gross margin: The uniqueness of Ethereum and other blockchain networks is that they do not require operating expenses (OpEx). All costs are borne as direct costs of producing the product.

Rollups—the primary form of second-layer solutions—do not require external token incentives to produce block space but instead purchase it on-demand from Ethereum. Rollups move transaction execution off-chain and batch transaction data into Ethereum's calldata. Calldata is simply a storage location used alongside EVM transactions.

By moving transaction execution off-chain and batching results, rollups can achieve greater scale. They are effectively unlimited in throughput, constrained only by demand and the amount of data that Ethereum or similar systems like Celestia can provide for rollups.

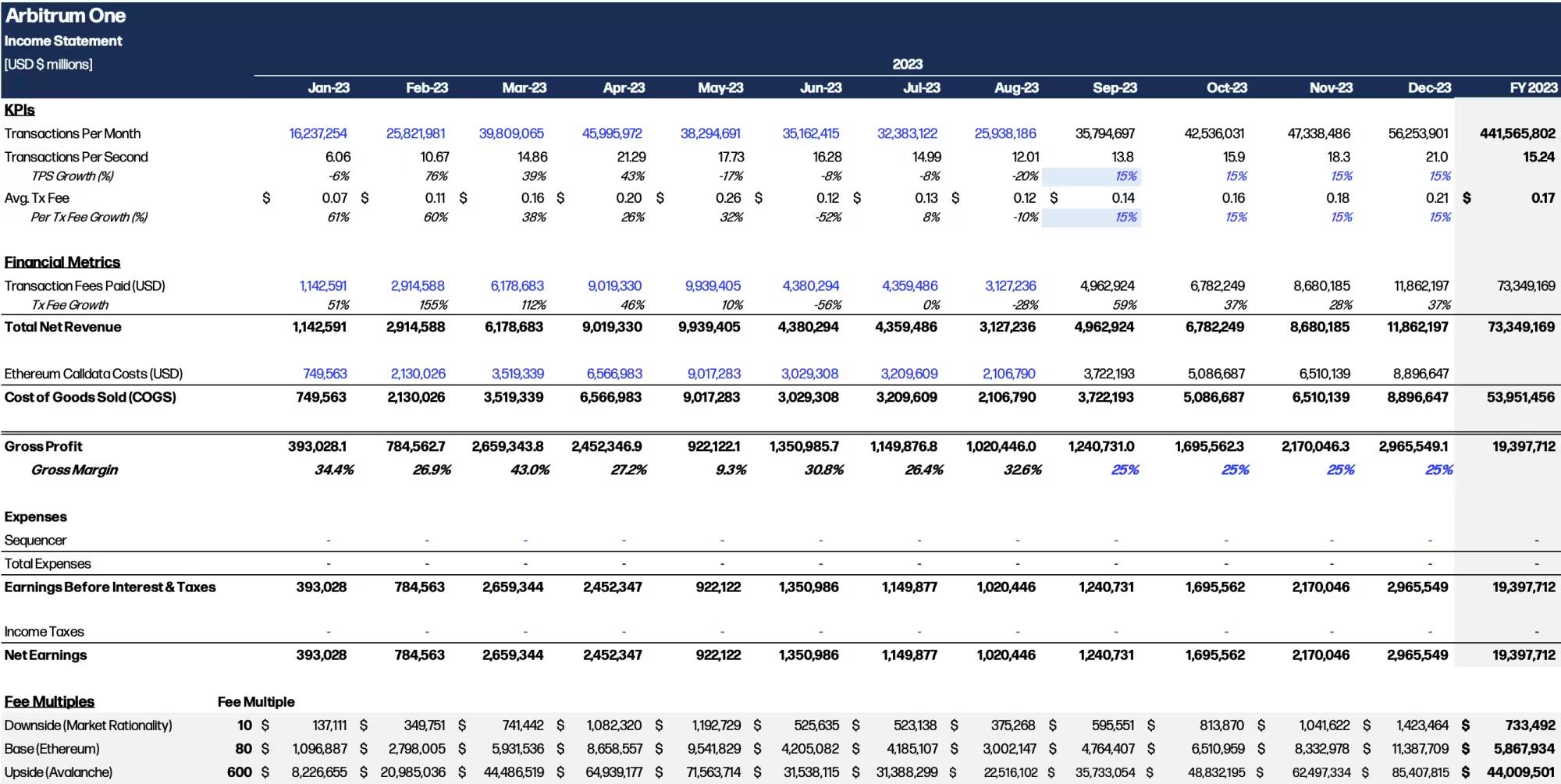

Arbitrum Income Statement

Arbitrum, like Ethereum, has a lower gross margin, with transaction throughput showing monthly growth of over 30%, reaching 21.3 transactions per second. Here are some notes on Arbitrum's profit and loss statement:

Arbitrum, like Ethereum, has a lower gross margin, with transaction throughput showing monthly growth of over 30%, reaching 21.3 transactions per second. Here are some notes on Arbitrum's profit and loss statement:

1. Unlimited upward scale: Rollups have no upper limit on scale, at least within multiples of their current transaction throughput. Throughput is a function of application demand.

2. Sequencers: Currently, Arbitrum's centralized sequencer—run by Offchain Labs—does not charge any revenue and passes the protocol's profits to the DAO (it contributed 3,350 ETH to the DAO in May). The dynamics of sequencers will evolve and will impact the profitability of selling L2 block space.

3. Future profit margins: In the following sections, we will discuss changes to the Ethereum protocol and Celestia, which will reduce L2's cost of goods sold by lowering calldata costs and will reduce Ethereum's fees.

We can see that L1 and L2 have fundamentally different costs for producing block space. L1 has variable revenue (transaction fees) and fixed costs (block rewards), while L2 has variable revenue and variable costs. L1's scale is limited (e.g., 15 transactions per second), with inconsistent gross margins (10% - 60%), while L2 scales based on user demand and has a consistent gross margin of 25%, potentially rising to over 75%.

How will the public market evaluate a company with 3x year-on-year growth and a net profit margin of 25%? What if I consider that the company can achieve structural improvements that raise net profit margins above 75%?

This is precisely where new developments like Arbitrum, Optimism, and ZKSync find themselves, such as data compression, EIP-4844, and Celestia, which will significantly reduce the data costs of rollups.

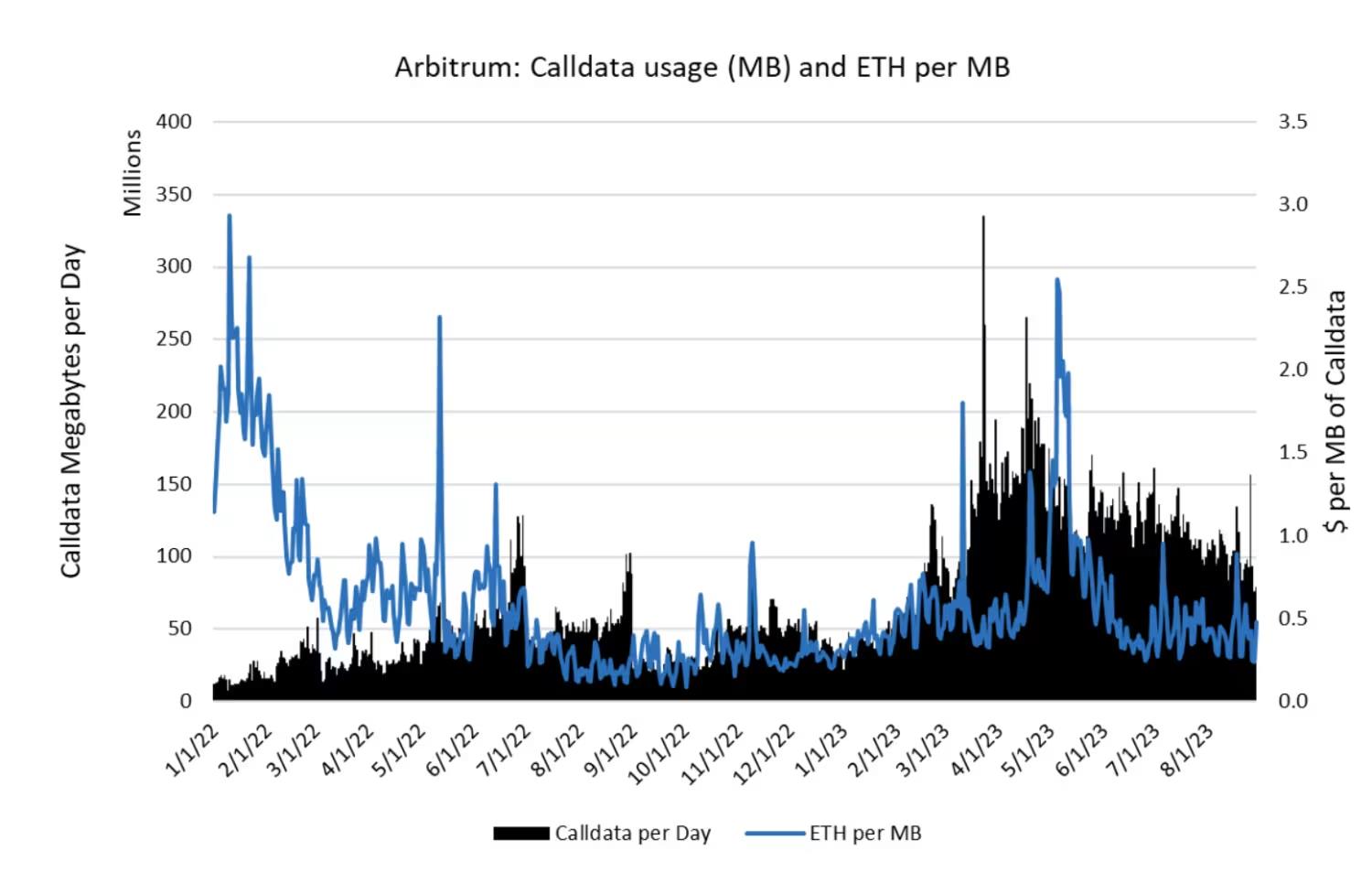

Calldata and Compression. Calldata is the data storage location attached to transactions, which rollups use to obtain data from Ethereum, storing state data on L1.

In August 2023, Arbitrum deposited 3.0 GB of data into Ethereum L1 calldata, peaking at 5.4 GB in May 2023, with prices of $1,144 and $1,840 per MB, respectively. The amount of calldata used daily is naturally closely related to daily transaction volume, while the price of calldata fluctuates with market demand. Arbitrum's throughput in May corresponded to 2.2 kb per second, while August's throughput corresponded to 1.2 kb per second.

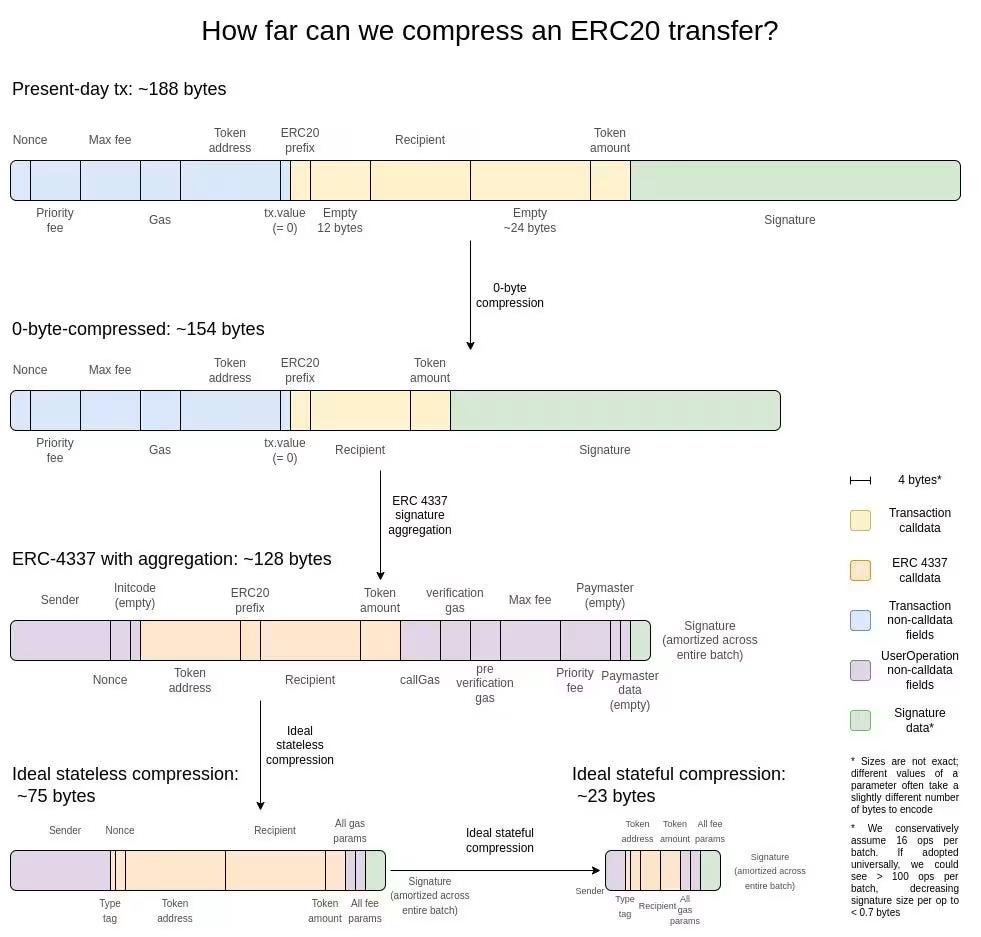

Poorer compression means higher data costs for rollups, reflected in the cost of goods sold in the profit statement. From an economic unit perspective, rollups can (i) pass higher costs onto consumers or (ii) accept lower gross margins in the face of higher sales costs. For rollups, there are still abundant further compression opportunities available, including zero-byte compression, signature aggregation, and eventually stateless compression technologies.

There are limits to the compression of rollup data, which is why Ethereum and other blockchains, like Celestia, are trying to lower the costs of data availability. EIP-4844 is an Ethereum upgrade that will significantly reduce the data availability costs for rollups. The original design of EIP-4488 aimed to reduce the cost of calldata from 16 gas per byte in its predecessor EIP-4488 to 3 gas per byte.

Ethereum researchers opted for a more complex EIP-4844, which has two main adjustments:

1. Blob space: EIP-4844 no longer directly places rollup state into calldata but opens a new "blob space" for rollup data, with each block being 262 kB, or 21.8 kb/s. Currently, Ethereum provides about 175 kB per block, or 14.7 kB/s, so in the short term, rollups will gain 1.5 times the data availability capacity. Over time, "blob space" will grow to 1 MB per block, increasing by five times.

2. Multi-dimensional fee markets: EIP-4844 will also introduce different pricing schemes for blob and gas (i.e., normal Ethereum execution), meaning rollups will use different Gas prices depending on rollup demand.

The exact impact of EIP-4844 on L2 data costs is difficult to predict, but by isolating the resource pricing model, capacity could increase by 1.5 to 5 times, and over time, the cost of goods sold for rollups could decrease by more than 4 times. A 4x reduction in data costs would bring Arbitrum's gross margin to 81%. In this scenario, rollups represent a very exciting business model.

Conclusion: Block Space as a Business Model

In summary, consumers are purchasing over $8 million worth of block space daily. The way blockchains coordinate the production of this commodity resource has unique characteristics in its business model: (i) high cyclicality and high correlation with market fluctuations, (ii) poor gross margin conditions but attractive operating profits, (iii) a business based on network effects, and (iv) software scale.

Is this a good business or a bad business? My current intuition is that the sale of block space is a very exciting business model, with some clear advantages (network effect-based moats) and clear disadvantages (poor revenue quality due to cyclicality). Another obvious negative factor is that existing regulations do not allow these networks to receive excess cash flow, and it is generally difficult to fit them into existing asset frameworks. If the industry can continue to add stable application layer use cases, blockchains with the strongest network effects, such as Ethereum, Binance, Arbitrum, and Optimism, may ultimately be able to generate hundreds of billions of dollars in total annual revenue from 'Fees Paid' while maintaining positive gross and net profit margins. The way to capture this excess value will be to allocate revenue to DAOs, as Arbitrum does today.

There is a completely different perspective on the economic models of L1, L2, and DA layers: the goal is not transaction fee revenue but to provide the cheapest block space, thereby achieving optimal application layers. The theory suggests that users will ultimately rally around the base assets of the winning platforms (ETH, MATIC, AVAX, etc.) as a store of value.

While blockchains may compete for this, it does not seem to be the right framework because (a) stablecoins exist, and mainstream users are more likely to store value in stablecoins rather than AVAX, etc.; (b) it seems self-evident that not every L1 token can become a SoV asset; and (c) L2s clearly do not participate in this race. The SoV play is only relevant for a few assets (BTC, ETH, TIA, possibly SOL/other L1 tokens) and will manifest as a premium for their inherent economic value.

Finally, there are several further avenues to explore:

1. The relationship between MEV and the total value of block space: One exercise is to evaluate the distribution of transaction fees to understand how much revenue can be attributed to MEV activities. As a quick rough analysis, as of April 30, the annualized revenue in the Proposer-Builder Separation (PBS) system was $247 million.

2. Value accumulation and competition among L2s: Currently, there are nearly 100 rollups, but due to reduced startup costs, we expect this number to increase from hundreds to thousands. Given that the near-term capacity with Ethereum DA is only 22 kb/s, we are seriously considering how competition among L2s will unfold, potentially requiring a long tail of rollups to utilize Celestia and EigenDA over time. We expect this to be achieved through competitive pricing of cost of goods sold. The key goal of this article is to assess block space as a commodity product and the production of block space as an economic model.