Galaxy Research Report: How Much Capital Inflow Can We Expect if Bitcoin Spot ETF is Approved?

Why is a Bitcoin ETF a more ideal solution than current investment tools?

Why is a Bitcoin ETF a more ideal solution than current investment tools?Original Title: " Sizing the Market for a Bitcoin ETF"

Original Author: Charles Yu, Galaxy

Translation: Odaily Planet Daily Translator | Nian Yinsitang

The approval of a spot Bitcoin ETF by U.S. regulators will be one of the most influential catalysts for the adoption of Bitcoin (and cryptocurrencies as an asset class).

Significance of Bitcoin ETF

Why is a Bitcoin ETF a more ideal solution than current investment tools?

As of September 30, 2023, the total amount of Bitcoin held by Bitcoin investment products (including ETPs and closed-end funds) is 842,000 BTC (approximately $21.7 billion).

The drawbacks of these Bitcoin investment products for investors are obvious—beyond high fees, low liquidity, and tracking errors, these products are inaccessible to a broad investor base that represents a significant portion of wealth. Other investment options that increase indirect exposure to Bitcoin (such as stocks, high-frequency trading funds, and futures ETFs) also suffer from similar tracking inefficiencies. Many investors are unwilling to deal with the administrative burden of directly owning Bitcoin, which involves wallet/private key management, self-custody, and tax reporting.

A spot ETF may be suitable for anyone looking to invest directly in Bitcoin without having to self-custody and manage Bitcoin, offering many benefits compared to current Bitcoin investment products and options, such as:

Improved efficiency through fees, liquidity, and price tracking. While Bitcoin ETF applicants have not yet listed fees, ETFs typically have lower fees compared to hedge funds or closed-end funds, and many ETF applicants may aim to keep fees low to remain competitive. A spot ETF will also provide stronger liquidity as it can be traded on major exchanges, allowing it to better track the price of Bitcoin compared to futures products or proxies, thus gaining exposure to Bitcoin.

Convenience. A spot ETF can provide investors with exposure to Bitcoin through a wider range of channels and platforms, including a variety of established providers that investors are already familiar with. It offers a more accessible channel for retail and institutional investors compared to direct ownership, which requires a certain level of self-education and incurs higher management costs.

Compliance. Compared to existing Bitcoin investment products, a spot ETF may meet stricter compliance requirements set by regulators regarding custody arrangements, oversight, and bankruptcy protection. Additionally, ETFs can provide better price transparency and discovery for market participants, which may help reduce market volatility for Bitcoin.

Why is a Bitcoin ETF important?

Two main factors that may particularly impact the market adoption of Bitcoin through a spot ETF are: (i) expanding accessibility to wealth segments; (ii) greater acceptance of Bitcoin through formal recognition by regulators and trusted financial service brands;

Accessibility

Expanding reach to retail and institutional investors. The range of currently available Bitcoin investment funds is limited, primarily consisting of products driven by wealth advisors or offered through institutional platforms. ETFs are a more direct compliant product that will increase investment opportunities for more investors (including retail and high-net-worth individuals). Unlike relying on wealth management firms, ETFs can be used by a broader client base, including investments made directly through brokerage firms or RIAs (which are prohibited from directly purchasing spot Bitcoin).

Distribution through more investment channels. Without Bitcoin investment solutions like a spot ETF, financial advisors/trustees cannot consider Bitcoin in their wealth management strategies. Wealth management departments hold a significant amount of capital that has been inaccessible for direct Bitcoin investment through traditional channels—once a spot ETF is approved, financial advisors can begin guiding their wealth clients to invest in Bitcoin.

More wealth opportunities. The Baby Boomer generation and earlier generations (aged 59 and above) hold 62% of U.S. wealth, but only 8% of adults over 50 invest in cryptocurrencies, compared to 25% of adults aged 18-49 (data from the Federal Reserve, Pew Research Center). Offering Bitcoin ETF products through familiar, trusted brands may help attract more older, high-net-worth individuals who have not yet participated.

Acceptance

Formal recognition/legitimacy from trusted brands. Bitcoin ETF applications have been submitted by numerous established financial firms—formal recognition/validation from these mainstream companies can enhance perceptions of the legitimacy of Bitcoin/cryptocurrencies as an asset class and attract greater acceptance and adoption. According to Pew Research data, among the 88% of Americans who have heard of cryptocurrencies, 75% lack confidence in the current ways of investing, trading, or using cryptocurrencies.

Addressing compliance issues; regulatory clarity will attract more investment and development. SEC approval of ETFs can alleviate many security and compliance concerns for investors, as ETFs are regulated investment products with more comprehensive risk disclosures. It will also provide market participants with the long-desired regulatory transparency needed to operate in the crypto industry. A more developed regulatory framework will attract more investment and development, enhancing the competitiveness of the U.S. in the crypto industry.

Returns/acceptance of BTC investment portfolios as an asset class. Bitcoin can provide diversification benefits and higher returns for portfolios, regardless of where the portfolio allocation is derived. To help guide investment management decisions, an increasing number of retail investors and financial advisors are turning to model portfolios and automated solutions that increasingly utilize ETFs and incorporate other asset classes to provide investors with more risk-optimized returns. A longer performance record can support the rationale for using Bitcoin in portfolios for more investment strategies.

How much capital inflow will the approval of a Bitcoin ETF bring?

Given the accessibility reasons mentioned above, the U.S. wealth management industry may be the most accessible and direct market, and the approval of a Bitcoin ETF will gain the most net new accessibility from it. As of October 2023, the total assets managed by broker-dealers ($27 trillion), banks ($11 trillion), and RIAs ($9 trillion) amount to $48.3 trillion.

In our analysis, we applied $48.3 trillion as the benchmark TAM (excluding the family office channel managing approximately $2 trillion) among selected U.S. wealth management integrators, although the target market for Bitcoin ETFs and the indirect impact of Bitcoin ETF approval may extend far beyond U.S. wealth management channels (e.g., international, retail, other investment products, and other channels), potentially attracting more capital inflow into the Bitcoin spot market and investment products.

(Note: While we use a TAM-style analysis to estimate capital inflow into Bitcoin ETFs, we acknowledge that the funds flowing into Bitcoin ETFs may also drive new net inflows rather than simply shifting from existing allocations—thus applying percentage capture assumptions to the estimated TAM figures does not fully reflect our view on how Bitcoin ETFs will be adopted, as it does not capture this new demand flow.)

As channels open up, the access cycle for Bitcoin ETFs in these areas may last for several years. The RIA channel is primarily composed of more seasoned independent registered investment advisors, who may allow access earlier than advisors at banks and broker-dealers, thus having a larger initial access share in our analysis. For banks and broker-dealer channels, each individual platform will decide when to unlock access to Bitcoin ETF products for their advisors—except for some exceptions, bank-affiliated financial advisors cannot offer or recommend specific investment products without platform approval. Platforms may have specific requirements (e.g., a track record of over 1 year or AUM reaching a certain scale, general applicability issues, etc.) before offering new investment products, which will affect the entry cycle.

We assume that the RIA channel will start growing at 50% in the first year and increase to 100% by the third year. For broker-dealers and bank channels, we assume a slower growth rate in the first year, starting at 25%, and steadily increasing to 75% by the third year. Based on these assumptions, we estimate the target market size for Bitcoin ETFs in the U.S. to be approximately $14 trillion in the first year post-launch, about $26 trillion in the second year, and $39 trillion in the third year.

According to these market size estimates, if we assume that 10% of the available assets in each wealth channel adopt Bitcoin, with an average allocation of 1%, we estimate that there will be $14 billion inflow in the first year after the Bitcoin ETF launches, increasing to $27 billion in the second year and $39 billion in the third year. Of course, if the approval of the spot Bitcoin ETF is delayed or rejected, our analysis will change due to timing and entry restrictions. Alternatively, if poor price performance or any other factors lead to lower-than-expected access or adoption of Bitcoin ETFs, our estimates may be overly aggressive. On the other hand, we believe our assumptions regarding investment channels, exposure, and allocations are conservative, so capital inflows may also exceed expectations.

Potential Impact on Physical BTC

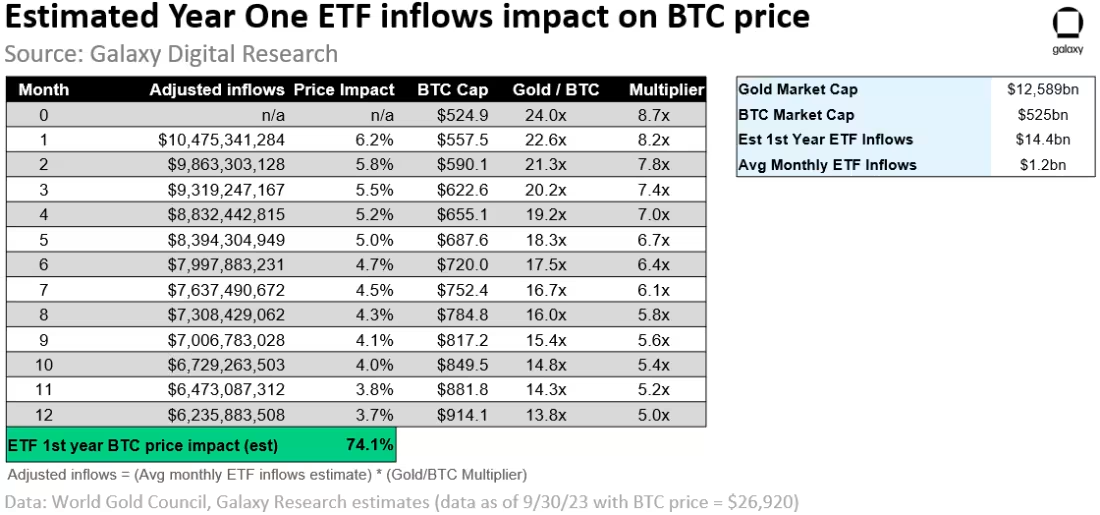

According to the World Gold Council, as of September 30, 2023, global gold ETFs hold approximately 3,282 tons (AUM approximately $198 billion), accounting for about 1.7% of the gold supply.

As of September 30, 2023, investment products (including ETPs and closed-end funds) hold a total of 842,000 BTC (AUM approximately $21.7 billion), accounting for 4.3% of the total Bitcoin issuance.

Compared to Bitcoin, gold's market capitalization is approximately 24 times that of Bitcoin, while the supply of investment tools has decreased by 36%, so we assume that the impact of equivalent dollar inflows on the Bitcoin market is about 8.8 times that of the gold market.

If we apply the estimated inflow of $14.4 billion in the first year (approximately $1.2 billion per month, or about $10.5 billion adjusted using the 8.8 times multiplier) to the historical relationship between gold ETF fund flows and changes in gold prices, we estimate that the price impact of the first month of the spot ETF on Bitcoin will be +6.2%.

Keeping the inflow constant, but adjusting the multiplier downward each month based on the changes in the gold/Bitcoin market capitalization ratio due to the increase in Bitcoin prices, we can see that the monthly return gradually declines from +6.2% in the first month to +3.7% in the last month of the first year, resulting in an estimated growth of 74% in Bitcoin prices in the first year after the ETF approval (using the Bitcoin price of $26,920 on September 30, 2023, as the starting point).

Keeping the inflow constant, but adjusting the multiplier downward each month based on the changes in the gold/Bitcoin market capitalization ratio due to the increase in Bitcoin prices, we can see that the monthly return gradually declines from +6.2% in the first month to +3.7% in the last month of the first year, resulting in an estimated growth of 74% in Bitcoin prices in the first year after the ETF approval (using the Bitcoin price of $26,920 on September 30, 2023, as the starting point).

Broader Financial Impact of ETFs on the Bitcoin Market

The above analysis estimates the potential capital inflow into U.S. Bitcoin ETF products. However, the second-order effects of the approval of Bitcoin ETFs may have a greater impact on Bitcoin demand.

In the short term, we expect other global/international markets to follow the U.S. in approving and offering similar Bitcoin ETF products to a broader range of investors. In addition to ETF products, various other investment tools may add Bitcoin to their investment strategies (e.g., mutual funds, closed-end funds, and private equity funds), spanning investment objectives and strategies. For example, Bitcoin exposure can be increased through alternative funds (such as currency, commodities, and other alternative funds) and thematic funds (such as disruptive technology, ESG, and social impact).

In the long term, the target market for Bitcoin investment products may further expand to all third-party managed assets (approximately $126 trillion AUM according to McKinsey) and even more broadly to global wealth (approximately $454 trillion according to UBS). Some believe that as Bitcoin becomes monetized, it will systematically reduce the monetary premium applicable to other assets such as real estate or precious metals, significantly expanding Bitcoin's TAM.

Based on these market sizes and keeping our adoption/allocation assumptions unchanged (10% of funds adopting Bitcoin, with an average allocation of 1%), we estimate that the potential new inflows into Bitcoin investment products over a long period will range between $125 billion and $450 billion.

Conclusion

For a decade, applicants have been seeking to list a spot-based Bitcoin ETF. During this period, Bitcoin's market capitalization has risen from less than $1 billion to today's $600 billion (peaking at $1.27 trillion in 2021). During this time, global Bitcoin holdings and usage have surged, with many different types of wallets, cryptocurrency exchanges, and custodians emerging worldwide, along with traditional market access tools. However, the largest capital market in the world, the United States, still lacks the most effective market access tool for Bitcoin—a spot-based ETF. The market's expectations for the imminent approval of ETFs are rising, and our analysis indicates that these products may see significant capital inflows, primarily driven by wealth management channels that currently lack large-scale access to secure and efficient Bitcoin exposure.

The capital inflow from ETFs, the market narrative surrounding Bitcoin's upcoming halving (April 2024), and the possibility that interest rates have already peaked or will peak in the short term all suggest that 2024 could be a significant year for Bitcoin.