The MEV landscape one year after the Ethereum merge

The transition from POS to MEV-Boost fundamentally reshapes the pattern of the transaction lifecycle, with more refined elements leading to intense competition among participants.

The transition from POS to MEV-Boost fundamentally reshapes the pattern of the transaction lifecycle, with more refined elements leading to intense competition among participants.Author: Shisi Jun

Since the Ethereum merge a year ago, the market share of MEV-Boost has remained steady at 90%. This is the Flashbots, valued at $1 billion. The complexity of MEV today is extremely high, involving non-user roles such as Searcher, Builder, Relayer, Validator, and Proposer. These parties engage in a complex interplay of interests during the 12-second block time, all seeking to maximize their respective profits.

This article attempts to compare the changes in profit margins before and after MEV, outline the MEV lifecycle post-merge, and share personal insights on cutting-edge issues.

In previous research titled "Interpretation of the UniswapX Protocol," I summarized the profit sources of UniswapX's operational process and aimed to fully depict the specific yield of MEV, as this is the source against which it competes and distributes profits to users (essentially sacrificing the real-time nature of transactions for better exchange rates).

Therefore, I recently conducted a detailed analysis of several types of MEV and compared multiple data sources to calculate the MEV profit situation before and after the Ethereum merge. The complete reasoning process can be found in the research report: "MEV Landscape One Year After the Ethereum Merge" (https://research.web3caff.com/zh/archives/11824?ref=shisi). Here are some key data conclusions:

1. Significant Drop in MEV Profits Post-Merge

- In the year before the merge, the average profit calculated from MEV-Explore was 22MU/M (from September 2021 to September 2022, just before the merge, the values included Arbitrage and liquidation modes).

- In the year after the merge, the average profit calculated from Eigenphi was 8.3MU/M (from December 2022 to the end of September 2023, the values included Arbitrage and Sandwich modes).

The conclusion regarding the change in final profits is:

After excluding hacker events that should not be attributed to MEV, the overall yield comparison shows a significant decline of 62%.

Note that the statistics from MEV-Explore do not actually cover data on sandwich attacks and include liquidation profits, so if we only look at pure Arbitrage comparisons, the decline may be even greater.

Supplementary note: Due to differences in statistical methods across platforms (and none including Cex arbitrage and mixed modes), only macro verification can be made, which is not absolutely precise. Additionally, another research report also compared different data sources regarding profits before and after the merge; see the appendix link.

Is the drastic drop in on-chain MEV profits caused by the merge? This needs to be examined from the MEV processes before and after the merge.

2. Traditional MEV Models

The term MEV can be misleading, as many people think it refers to miners extracting this value. In fact, the current MEV on Ethereum is primarily captured by DeFi traders through various structural arbitrage trading strategies, while miners only profit indirectly from the transaction fees of these traders.

This classic introductory article on MEV, "Escaping the Dark Forest" (https://www.paradigm.xyz/2020/08/ethereum-is-a-dark-forest), posits that there are very clever hackers on-chain continuously exploiting contract vulnerabilities. However, when they discover a vulnerability, they face another dilemma: how to profit without being outpaced by others.

After all, their transaction signatures will enter the Ethereum mempool, spreading publicly, and then be sorted and mined by miners. This process may take only 3 seconds or a few minutes, but in that brief time, the signed transaction content can be targeted by countless hunters, who can simulate and deduce it again.

If a hacker is foolish and directly executes a profit-seeking method, they will be outbid by hunters at a high price.

If a hacker is clever, they might adopt a method similar to that of the article's author, using contract-to-contract (i.e., internal transactions) to hide their final profit-seeking transaction logic. Unfortunately, the outcome is not like that described in "Escaping the Dark Forest" (https://samczsun.com/escaping-the-dark-forest/), where success was achieved; instead, they are still outpaced.

This also means that hunters analyze not only the parent transactions on-chain but also each child transaction, simulating profit deductions. They even further inspect the deployment logic of gateway contracts and replicate it, and this is done automatically within seconds.

The so-called dark forest is not limited to this.

In my previous tests on BSC nodes, I found that many rogue nodes only accepted P2P connections but did not actively transmit TxPool data. Moreover, based on the exposed IPs of these nodes, one could even argue that they surrounded the main core block-producing nodes of BSC.

Motivated by this, these nodes occupy P2P connections but do not provide data, only allowing communication among whitelisted nodes. This way, they can monetize by using resource scale to enhance MEV profit margins, as BSC has a standard block time of 3 seconds. The later ordinary players see transaction information, the later they can deduce suitable MEV strategies. When ordinary players engage in MEV transactions that need to be packaged, due to BSC's supernode model, the latency will be lower than that of the top MEV players who have surrounded BSC based on their geographical location.

In addition to the encirclement of supernodes, exchange servers can also be surrounded. After all, the interest rate differential between CeFi and DeFi is larger, and exchanges themselves are the largest arbitrage bots. This is very similar to the early web2 ticket-buying scenarios, where black and gray industries would ambush near servers and use DoS attacks to curb the normal activities of ordinary users.

In summary, although traditional trading also has many hidden competitions in the dark forest, it is relatively a clear profit model. However, after the Ethereum merge, the complex system architecture quickly broke the traditional MEV model, and the head effect became increasingly pronounced.

3. MEV Models Post-Merge

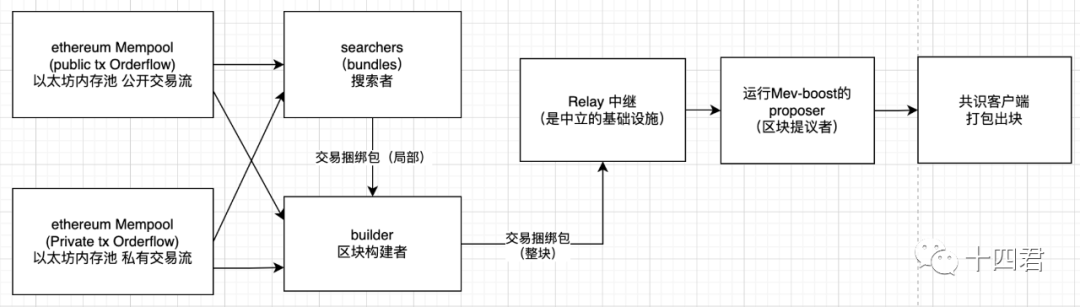

The Ethereum merge refers to the upgrade of its consensus mechanism from POW to POS. The final merge plan was based on reusing the lightweight infrastructure of pre-merge Ethereum while separately isolating the consensus module for block decision-making. For POS, each block occurs every 12 seconds, rather than the previous fluctuating values. Block mining rewards have decreased by about 90%, from 2 ETH to 0.22 ETH. This is very important for MEV for two reasons: 1. The block interval of Ethereum has become stable. It is no longer the previous random situation of 3-30 seconds, which has both pros and cons for MEV. Although Searchers no longer need to rush to see slightly profitable transactions and can directly send them out, they can continuously accumulate a better total transaction sequence to hand over to validators before the block is produced, but this also intensifies competition among Searchers. 2. The reduction in miner incentives encourages validators to be more willing to accept MEV transaction auctions, achieving a 90% market share for MEV in just 2-3 months. 3.1. Lifecycle of Transactions Post-Merge After the merge, the roles involved include Searcher, Builder, Relay, Proposer, and Validator, where the latter two belong to the system roles in POS, while the former three belong to MEV-Boost, achieving a separation of block responsibilities and block ordering.

- Searcher: They are various entities searching for profitable transactions in the mempool, arranging transaction sequences into local bundles delivered to Builders.

- Builder: They collect various bundles of transaction sequences sent by Searchers, selecting the most profitable sequences, which can be combinations of multiple bundles or their own restructured sequences.

- Relay: A neutral facility responsible for verifying the validity of transaction sequences and recalculating profits, providing several block sequence packages for validators to choose from.

- Proposer and Validator: They are the miners of post-merge Ethereum, selecting the maximum profit transaction sequence combinations provided by Relays to complete the block work, earning both consensus rewards (block rewards) and execution rewards (MEV + Tips).

《Block Production Process After Ethereum Merge》 Self-made

《Block Production Process After Ethereum Merge》 Self-made

Integrating these roles, the lifecycle of each block today is:

- Builders create a block by receiving transactions from users, Searchers, or other (private or public) order flows.

- Builders submit the block to the Relay (i.e., there are multiple Builders).

- The Relay verifies the block's validity and calculates the amount it should pay to the block producer.

- The Relay sends the transaction sequence package and profit price (also the auction bid) to the current slot's block producer.

- The block producer evaluates all the bids they receive and selects the sequence package that maximizes their profit.

- The block producer sends this signed header back to the Relay (completing this round of the auction).

- After the block is published, rewards are distributed to Builders and Proposers through the transactions within the block and block rewards.

4. Conclusion

1) What is the ecological impact of the merge on MEV?

This article organizes the comparison of profit data before and after the merge, as well as the MEV mining process of transactions on-chain before and after the merge. It can be said that the rise of MEV-Boost fundamentally reshaped the transaction lifecycle model, splitting it into more refined segments that create competition among various participants. If Searchers fail to conduct research on the latest strategies, they will earn nothing; if they do well, they can gradually expand their profits and become Builders.

Setting aside the shrinkage of on-chain transaction volume, there is a high level of internal competition between Searchers and Builders, as they can substitute for each other in the system structure. Ultimately, order flow reigns supreme; Searchers will hope to gradually expand their profit margins, which requires a large enough volume of private orders (resulting in higher profits for the constructed block), thus gradually becoming Builders.

For example, during the attack event in Curve caused by a compiler vulnerability that led to the failure of reentrancy protection, a single transaction fee even reached 570 ETH, marking the second-highest transaction fee for an MEV transaction in Ethereum's history, illustrating the competitive landscape.

Although MEV is not an issue that the Ethereum merge itself aims to solve, the enhancement of systemic game-theoretic confrontations combined with various environmental factors ultimately led to a reduction in the total profit margin of MEV. This does not mean that the amount involved in MEV has decreased, but rather that the reduction in profit margins means more revenue flows to validators (https://writings.flashbots.net/open-sourcing-the-flashbots-builder). For users, this is a good thing; lower profits will reduce the motivation for some on-chain transaction attacks.

2) What are the cutting-edge exploration points surrounding MEV?

Starting from privacy transactions: There are Threshold Encryption and Delayed Encryption, as well as SGX encryption, which fundamentally require encryption of transaction information and conditions for decryption, such as time locks, multi-signatures, or trusted hardware models.

From the perspective of fair transactions: There are Fair Sequencing Services (FSS) and MEV Auctions for order flow auctions, as well as MEV-Share, Mev-Blocker, etc. The difference lies in moving from completely no profit to sharing profits to weighing profits, allowing users to decide what cost they are willing to pay for relative fairness in transactions.

Protocol-level improvement of PBS: Currently, PBS is a proposal from the Ethereum Foundation, but its implementation has been achieved through MEV-Boost, achieving separation. In the future, this core mechanism will transition to Ethereum's own protocol mechanism.

3) Does Ethereum have resistance to OFAC scrutiny?

With the maturation of the cryptocurrency industry, regulation is inevitable. All entities registered in the U.S. and their operations of Ethereum POS validators must comply with OFAC requirements. However, the system mechanism of blockchain ensures that it does not exist solely in the U.S.; as long as there are other relays that comply with local policies, it can ensure that at some point, it can be propagated on-chain.

Even if over 90% of Validators review transactions routed through MEV, those resistant transactions can still be on-chain within an hour. Therefore, as long as it is not 100%, it is equivalent to 0%.

4) Do relays lacking incentives have sustainability?

This currently appears to be an invisible problem. Without profits, maintaining complex relay services will ultimately lead to a shift towards strong centralization. Recently, Blocknative also stopped its MEV-Boost relay service, meaning that over 90% of Ethereum's block settlements will be controlled by four companies. It can be said that the current MEV-Boost relay is 100% risk with 0% return. Since relays aggregate txs reported by various Builders as a data aggregation point, they may gradually obtain profits through systems like MEV-Share and MEV Auction, such as directly receiving users' privacy transaction requests. Previously, map software apps were also trapped in such services; as public relations items, they could not charge on a membership basis, but they still thrived under pilot models that integrated exposure ranking ads and diverse ride-hailing services. In summary, as long as there is traffic, users, and fairness, there will be no lack of profits.

5) How will ERC4337 bundled transactions affect MEV?

Currently, there are over 687,000 AA (Account Abstraction) wallets and over 2 million user operations (UserOps). The overall trend represents explosive growth compared to the slow growth of CA wallets in the past. ERC-4337 has a complex operational mechanism, especially since the propagation of transaction signatures does not share Ethereum's own mempool. Although it will initially increase the difficulty of MEV, it is unstoppable in the long run.

For further reading, see the previous research report: "Research Report on the Latest Approved Plan for Account Abstraction ERC-4337" https://research.web3caff.com/zh/archives/6900?ref=shisi.

6) Can DeFi catch up with CeFi in the face of MEV threats?

Although many current solutions aim to make DeFi smoother from an experience perspective, such as using meta-transactions or cross-chain swaps or ERC-4337 to reduce the requirement for users to have transaction fees to execute trades, or enhancing account security through multi-layered, multi-tiered, and social response features of contract wallets, in my view, no matter how DeFi tries to catch up with CeFi, it will always have unique, incomparable advantages, from speed to experience. However, DeFi also has unique advantages that CeFi cannot compare to, each with its own audience and development cycle.

7) What is the current state of MEV in Layer-2?

In Optimism, there exists a unique module called Sequencer, which generates signed receipts to ensure transaction execution and ordering. The Sequencer will be checked by a group of validators with the authority to impose penalties, and it uses the MEVA (MEV Auction) scheme to select a unique Sequencer through an auction process.

In Arbitrum, regarding the Sequencer structure, Arbitrum uses the FSS (Fair Sequencing Services) scheme developed by Chainlink to determine the order.

These methods eliminate MEV from miners to a certain extent due to the uniqueness of L2, but sidechains that do not interoperate with the Ethereum mainnet still present MEV opportunities, such as BSC, BASE, etc.

Finally, this article is a 1/3 excerpt, and further data and conclusion reasoning can be found in the complete research report: "MEV Landscape One Year After the Ethereum Merge: How Are the Beneficiary Chains Presenting Under High Complexity Game Theory Confrontation?" https://research.web3caff.com/zh/archives/11824?ref=shisi.