LD Capital: THORChain Lending Reveals the Shadow of Terra LUNA

In-depth analysis of the THORChain lending module, is it an upgraded version of the LUNA model?

In-depth analysis of the THORChain lending module, is it an upgraded version of the LUNA model?Original Author: Yilan, LD Capital

Introduction

In-depth exploration of the new lending module launched by Thorchain on August 22 reveals the shadow of Terra LUNA. The similarity with LUNA mainly lies in the fact that the collateral deposited by users is exchanged for RUNE. The actual inflation and deflation of RUNE are determined by the fluctuations in the RUNE-collateral exchange rate, meaning RUNE absorbs the volatility of the RUNE-collateral exchange rate through inflation and deflation, similar to how LUNA absorbed the volatility of UST. However, the forms of expression (RUNE participates in lending, being burned and minted during loan opening and closing, while LUNA participates in stablecoin anchoring, being burned and minted through arbitrage when UST unpegs) and the underlying risk dimensions (LUNA has no upper limit on minting, while RUNE has inflation and deflation limits, with only 50% of the collateral for synthetic assets being RUNE) are different. Furthermore, the lending protocol has implemented strict risk control and risk isolation measures, thus the overall risk is relatively small and will not produce systemic risks similar to Terra LUNA. Even in the event of a negative spiral, it will not affect other functions of Thorchain.

I. Understanding Thorchain's Lending Mechanism

The characteristics of Thorchain lending are that there are no interest rates, no liquidation risks, and no time limits (the minimum loan term is 30 days during the initial period). For users, it essentially involves empty USD and collateral assets of BTC/ETH; for the protocol, it essentially involves empty BTC/ETH and more USD. Debt is denominated in TOR (the USD equivalent of Thornchain), so users are similar to purchasing an out-of-the-money call option on BTC with a gold standard. The holders of the protocol/RUNE are the counterparties.

Opening a new loan will have a deflationary effect on $RUNE assets, while closing a loan will have an inflationary effect on $RUNE assets. BTC collateral will first be exchanged for RUNE, then burned, and finally, RUNE will be minted to exchange for the required assets. In this process, the difference between the value of the collateral and the debt, minus transaction fees, corresponds to the net destruction value of RUNE.

If the collateral rises at the time of repayment, while the price of RUNE remains unchanged, more RUNE needs to be minted to exchange for the required assets, leading to inflation; if the price of RUNE rises, it is ideal not to mint so much RUNE; if the price of RUNE falls, inflation will be more severe. If the collateral falls at the time of repayment and the price of RUNE remains unchanged, the user may choose not to repay (resulting in no minting).

If the value of RUNE relative to $BTC remains unchanged when the loan is opened and closed, then $RUNE will not produce a net inflation effect (the amount burned equals the amount minted minus transaction fees). However, if the value of the collateral relative to RUNE increases between the opening and closing of the loan, then the supply of $RUNE will experience net inflation.

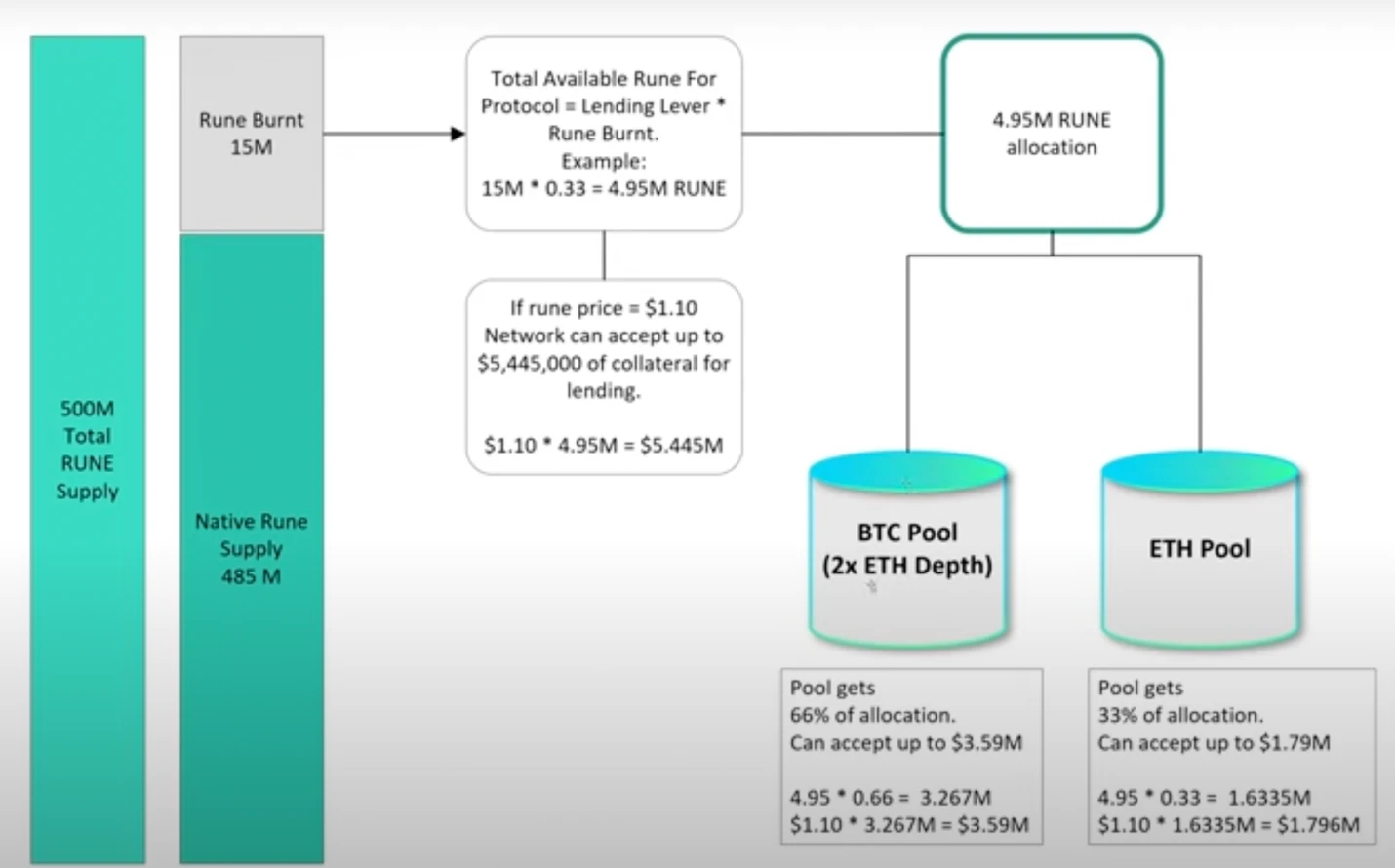

To address the inflation issue, lending control measures are in place—if minting causes total supply to exceed 5 million RUNE, there is a circuit breaker design. In this case, reserves will intervene to redeem loans (instead of further minting), and the entire lending design will stop and exit use, but other aspects of THORChain will continue to operate normally.

Therefore, the entire lending process has a significant impact on the inflation and deflation of RUNE, but under the overall low cap of lending, both inflation and deflation are capped. When the RUNE-collateral exchange rate rises indefinitely, the maximum deflation is currently 15 million * 0.33 (0.33 is the lending lever, which might change), i.e., 4.95 million (which may increase in the future). In the case of an indefinite decline in the RUNE-collateral exchange rate, inflation is also controlled by the circuit breaker to remain below 5 million.

Specifically, if a user over-collateralizes 200% to borrow 50% of the required assets, the other 50% will be minted based on the RUNE-collateral exchange rate at the time of redemption. This step is essentially very similar to LUNA; however, under the mechanism of Thorchain Lending, since only 50% is backed by RUNE, the product capacity is smaller, thus the overall risk is relatively small and will not produce systemic risks similar to Terra LUNA. This part of the risk is isolated, and even in the event of a negative spiral, it will not affect other functions of Thorchain.

1. How to Understand the Design of Lending as a Deep Out-of-the-Money, Resettable Strike Price Bullish Option for Users

When Alice provides 1 BTC, she also receives 50% cash (in the case of a CR of 200%) and the opportunity to purchase 1 BTC with this cash.

If at the time of repayment (assuming one month later) BTC rises, Alice repays her debt (i.e., the equivalent of 50% of the value of BTC one month ago) and buys this one BTC at the price of BTC one month ago. If it falls significantly, exceeding 50%, Alice may choose not to repay, and the protocol will not incur inflation from minting RUNE (for Alice, her bullish position fails).

2. How to Understand No Borrowing Interest?

It can be seen as users paying multiple swap fees instead of an interest rate; it is essentially a CDP product. If borrowing interest were charged, the attractiveness of this product to users would be reduced.

The entire lending process is as follows:

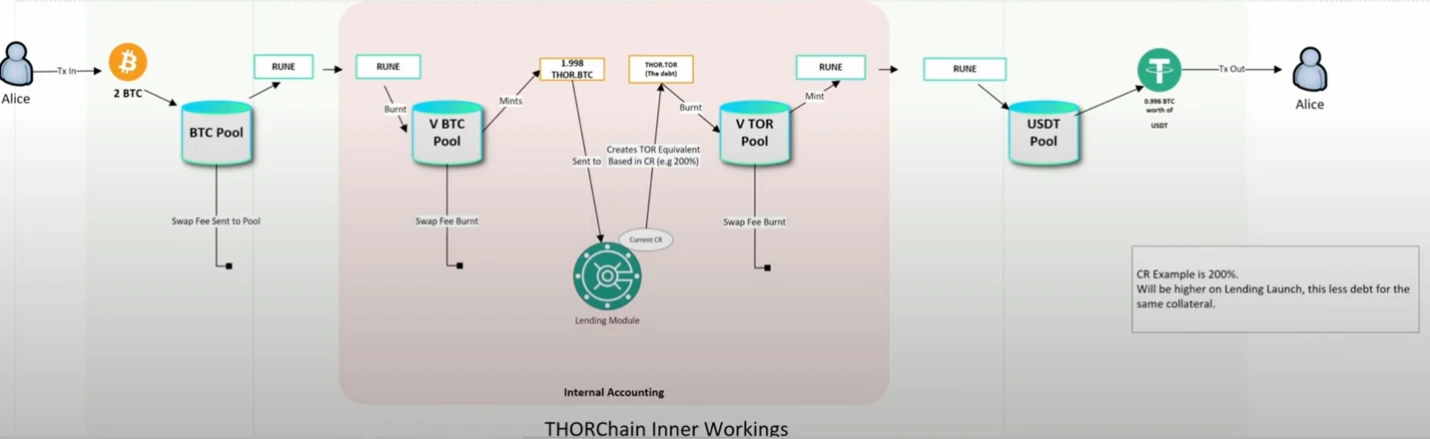

Users deposit native asset collateral (BTC, ETH, BNB, ATOM, AVAX, LTC, BCH, DOGE). In the initial phase, collateral is limited to BTC and ETH. The amount of collateral each debt position can accept (debt position cap) is determined by the hard cap (15 million), lending lever, and pool depth coefficient. Over-collateralization generates debt, and the proportion of debt obtained is determined by CR.

Borrowing: Alice deposits 1 BTC, which will first be exchanged for RUNE in the BTC-RUNE swap pool. These RUNE enter a V BTC pool, are burned, and simultaneously converted into a derivative asset Thor.BTC. The collateral for synthetic assets is a constant product liquidity, always 50% of the asset, with the remaining 50% being RUNE. Then the derivative asset Thor.BTC is sent to an internal module, where a dynamic CR (collateral ratio) determines how much loan can be obtained, and another token Thor.Tor (similar to USD) is generated as a bookkeeping measure for the loan. The steps that occur here are entirely for internal accounting purposes, subsequently generating USDT loans for Alice to use.

Repaying the Loan: When Alice repays, she sends all USDT or other Thorchain-supported assets to the protocol, which are converted into RUNE. RUNE will mint Tor, and the protocol checks whether the user has repaid all loans denominated in Tor. If fully repaid, the collateral will be released and converted into derived collateral (Thor.BTC), and then this derived asset will be reminted into RUNE, swapped back to L1 BTC. RUNE is minted during this process.

It is important to note that these swap and convert processes incur transaction fees (a single loan generates at least 4 swap fees), so the total repayment amount needs to be slightly higher than the actual amount to cover these swap fees. Although there is no interest, this collection of multiple transaction fees can actually be seen as a substitute for interest. Although the wear and tear are significant, the RUNE generated in the form of transaction fees is burned, which is a tangible deflation.

3. How to Understand No Liquidation and No Repayment Time Limit?

Since the debt denominated in TOR stablecoin is fixed, borrowers can choose to repay with any asset, but in practice, they will all be exchanged for RUNE through the market, and liquidity providers and depositors will not directly lend their assets to borrowers. The pool merely serves as a medium for exchanging between collateral and debt, making the entire process a betting behavior, which is the reason for no liquidation. The protocol needs to use RUNE to repay enough TOR (complete repayment) to help users reclaim their collateral. If the price of the collateral drops significantly, users may choose not to repay (and the portion of RUNE will not be reminted, resulting in net destruction). In fact, the protocol does not wish for users to repay; if the price of the collateral rises and the price of RUNE falls, user repayment will lead to inflation.

4. How to Understand RUNE as a Transaction Medium's Deflation and Inflation?

First, the total upper limit of all lending pools is determined by the RUNE Burnt portion in the gray area of the diagram multiplied by the lending lever, and the 15 million RUNE Burnt is the result of the protocol burning non-upgraded BEP 2/ERC 20 RUNE previously. Therefore, it can be seen that the protocol currently has a space of 15 million RUNE before reaching the maximum supply of 500 million RUNE.

The above text also introduced the role of RUNE in the entire borrowing process (which can be reviewed in the mechanism section above). Opening a new loan will have a deflationary effect on RUNE assets, while closing a loan will have an inflationary effect on RUNE assets.

If the collateral rises at the time of repayment, while the price of RUNE remains unchanged, more RUNE needs to be minted to exchange for the required assets, leading to inflation; if the price of RUNE rises, it is ideal not to mint so much RUNE; if the price of RUNE falls, inflation will be more severe. If the collateral falls at the time of repayment, and the price of RUNE remains unchanged, the user may choose not to repay (resulting in no minting).

If the value of RUNE relative to BTC remains unchanged when the loan is opened and closed, then RUNE will not produce a net inflation effect (the amount burned equals the amount minted minus transaction fees). However, if the value of the collateral relative to RUNE increases between the opening and closing of the loan, then the supply of RUNE will experience net inflation.

To address the inflation issue, lending control measures are in place—if minting causes total supply to exceed 5 million RUNE, there is a circuit breaker design. In this case, reserves will intervene to redeem loans (instead of further minting), and the entire lending design will stop and exit use, but other aspects of THORChain will continue to operate normally.

If calculated with the parameters in the diagram, currently, all debt positions combined amount to only 4.95 million RUNE in total. That is, all debt positions can accept collateral equivalent to 4.95 million RUNE.

Source: GrassRoots Crypto

The total RUNE Burnt in the entire Reserve serves as the buffer for all debt positions and the last resort for inflation. The total amount of RUNE Burnt * Lending lever of 4.95 million (currently) will be allocated according to the depth of each debt position pool. The deeper the pool, the more reserve buffer it receives. For example, if the depth of the BTC Lending pool is twice that of the ETH Lending pool, then the value of RUNE Burnt * Lending lever * depth coefficient in the reserve is the maximum collateral limit that this lending pool can bear. Therefore, when the price of RUNE rises, the amount of collateral that this pool can accommodate also increases. It can also be seen that the lending lever and the price of RUNE jointly determine the upper limit of collateral that the lending pool can accommodate.

The THORChain protocol and all RUNE holders are the counterparties for each loan. The burn/mint mechanism of RUNE means that RUNE condenses/dilutes during the opening and closing of debt (among all RUNE holders). When the RUNE-collateral exchange rate falls, inflation occurs; conversely, deflation occurs.

5. Is the CDP Protocol a Good On-Chain Capital Accumulation Model?

For the lending launched by Thorchain, it is a form of capital accumulation that uses RUNE as an essential medium in the borrowing and repayment process, increasing the scenarios for burning and minting.

So, is this accumulation model advantageous? Let's first look at some other accumulation models in different sectors.

CEX is the most obvious beneficiary of the accumulation model, as it also acts as a custodian. In many cases, this portion of funds can generate more returns (the requirement for reserves to be disclosed has significantly reduced these returns compared to before). How to protect users' custodial funds is also something that regulatory frameworks need to clarify, as regulators typically want exchanges to be fully reserved.

The situation on-chain is entirely different.

DEX requires high incentives for LP after accumulation, so the purpose of accumulation is to deepen liquidity, and it cannot directly utilize the "deposits" provided by LP to generate profits. Instead, it forms a liquidity moat through a large reserve.

Pure lending, similar to Aave or Compound, requires paying interest costs for accumulation, and the entire model is not much different from traditional lending, such as needing to actively manage borrowing positions and having repayment time limits.

In contrast, the CDP model is a healthier accumulation model. Due to the high volatility of collateral assets, most over-collateralized CDPs in the current market involve users over-collateralizing a certain asset to obtain stablecoins/other assets. In this process, the CDP protocol effectively gains more "deposits." Moreover, it does not need to pay interest on these deposits.

Thorchain also belongs to this CDP model, so where is the collateral held? In fact, the collateral is exchanged for RUNE through liquidity pools. Therefore, no one "stores" the collateral. As long as the THORChain pool is healthy and operating normally, any deposited collateral will be exchanged for RUNE, and then arbitrageurs will rebalance the pool as usual. This can be seen as the collateral being settled in the RUNE pairs of other currencies in the Thorchain ecosystem. Because collateral like BTC has entered the circulating market rather than being held in the protocol, although the generated debt is 100% collateralized, the difference in value between the collateral and the debt is determined by the value of RUNE, thus casting a shadow similar to Terra LUNA over the entire mechanism.

Capital sink may be one of the goals Thorchain lending aims to achieve, using users' collateral assets to settle as liquidity in the swap pool. As long as users do not close their loans and the price of RUNE does not drop significantly, the protocol retains assets, RUNE generates deflation, forming a positive cycle. Of course, the opposite could lead to a negative spiral.

6. Risks

Collateral like BTC enters the circulating market rather than being held in the protocol, so although the generated debt is 100% collateralized, the difference in value between the collateral and the debt is determined by the value of RUNE, thus casting a shadow similar to Terra LUNA over the entire mechanism. Since the RUNE burned when opening loans and the RUNE minted when closing loans may not be equal, both deflation and inflation can occur. It can also be understood that if the price of RUNE rises at the time of repayment, deflation occurs; conversely, inflation occurs. If the price of RUNE falls below the price multiplied by the lending lever at the time of opening, the circuit breaker will be triggered. Throughout the lending process, the price of RUNE plays a decisive role in deflation and inflation. When the price of RUNE declines, a significant number of users choosing to close loans poses a high risk of inflation. However, the protocol has implemented strict risk control and risk isolation measures, so the overall risk is relatively small and will not produce systemic risks similar to Terra LUNA. Even in the event of a negative spiral, it will not affect other functions of Thorchain.

The lending lever, CR, and whether to open different collateral debt positions are the three main pillars of Thorchain lending risk control.

Additionally, Thorchain has a history of being hacked, and its code is complex, so Thorchain Lending may also have vulnerabilities that need to be paused or fixed.

II. Conclusion

The launch of the Thorchain Lending product generates network synergy benefits, additional trading volume, and higher pool capital efficiency, driving the system to generate real profits and increasing the total bonded amount, allowing Thorchain to gain potential upward space by reducing the total circulating amount (when the RUNE-collateral exchange rate rises).

Capital sink may be one of the goals Thorchain lending aims to achieve, using users' collateral assets to settle as liquidity in the swap pool. As long as users do not close their loans and the price of RUNE does not drop significantly, the protocol retains assets, RUNE generates deflation, forming a positive cycle.

However, in reality, the reverse market trend could lead to inflation and a negative spiral. To control risks, the use of Thorchain lending is limited, and its capacity is small. Overall, inflation and deflation, given the current capped volume, will not fundamentally impact the price of RUNE (at most a 5 million RUNE impact).

Moreover, for users, the capital efficiency of Thorchain is not high, with CR fluctuating between 200% and 500%, ultimately likely floating between 300% and 400%. From a pure leverage perspective, it is not the best product. Additionally, although there are no borrowing fees, the multiple internal transaction fees can be unfriendly to users.

Evaluating only the lending product does not represent the overall development of the Thorchain DeFi product matrix. There will be a series of analyses on other Thorchain products in the future.