Bankless: The Tokenization of National Debt and the RWA Revolution

This article uses MakerDAO as a case study to validate the bullish argument behind putting U.S. Treasury bonds on-chain, revealing why upgrading Uncle Sam's debt to a financial product will stimulate the next wave of RWA adoption, and contemplating what will happen next with tokenization.

This article uses MakerDAO as a case study to validate the bullish argument behind putting U.S. Treasury bonds on-chain, revealing why upgrading Uncle Sam's debt to a financial product will stimulate the next wave of RWA adoption, and contemplating what will happen next with tokenization.Original Title: 《Tokenized Treasuries and an RWA Revolution》

Author: Jack Inabinet

Compiled by: Kate, Marsbit

Why upgrading Uncle Sam's debt to a financial product will stimulate the next wave of RWA adoption and what to expect from the upcoming tokenization. Bankless delves into the world of real-world assets (RWA) and discusses the potential of tokenizing U.S. Treasuries to drive more cryptocurrency adoption, full compilation by MarsBit:

BlackRock CEO Larry Fink boldly referred to this crypto industry as the "next generation market," while the Boston Consulting Group predicts that the scale of this opportunity will be 42 times larger than the current DeFi TVL in just seven years.

Which crypto phenomenon is TradFi excited about? Of course, it's tokenized assets! RWA enthusiasts have long hinted at an impending bull market led by tokenization; however, until recently, the industry struggled to gain traction in the cryptocurrency space.

While protocols like RealT and Centrifuge have successfully created on-chain representations of real-world assets, they have struggled to attract a sufficiently sized market. Due to regulatory uncertainty, TradFi institutions capable of underwriting these transactions have been hesitant to lend, and the opaque off-chain nature of these types of products (along with relatively low returns) has hindered crypto enthusiasts from participating in these markets.

Tokenization has progressed slowly for a long time, but fortunately, there is an asset class emerging as a champion capable of triggering mass adoption: U.S. Treasuries!

Today, we will use MakerDAO as a case study to validate the bullish argument behind bringing U.S. Treasuries on-chain, revealing why upgrading Uncle Sam's debt to a financial product will stimulate the next wave of RWA adoption and what to expect from the upcoming tokenization.

?MakerDAO's RWA Journey

MakerDAO is no stranger to real-world assets. Since April 2021, its stablecoin DAI has been partially backed by RWAs.

In the early days, Maker procured RWAs through customized credit agreements; however, the protocol quickly realized the limitations of this facility. Customized credit is extremely difficult to scale and carries high risks, with each loan requiring a time-consuming due diligence process and backed by relatively illiquid assets (i.e., real estate deeds or receivables).

In pursuit of scale and risk reduction, Maker chose to completely bypass the difficulties of customized credit by becoming a lender to the U.S. government!

First was the Maker-backed Monetalis Clydesdale vault, which generates returns by investing in liquid U.S. Treasury exchange-traded funds (ETFs). Following closely were the BlockTower Andromeda vault (a similar investment vehicle) and the Coinbase Custody vault, which helps funnel a portion of U.S. Treasury yields back to Maker's USDC.

The introduction of these vaults ultimately enabled Maker to deploy idle stablecoins into RWAs at scale, and their high liquidity allowed Maker to expand like traditional financial entities, reducing positions to manage duration as stablecoin reserves grew.

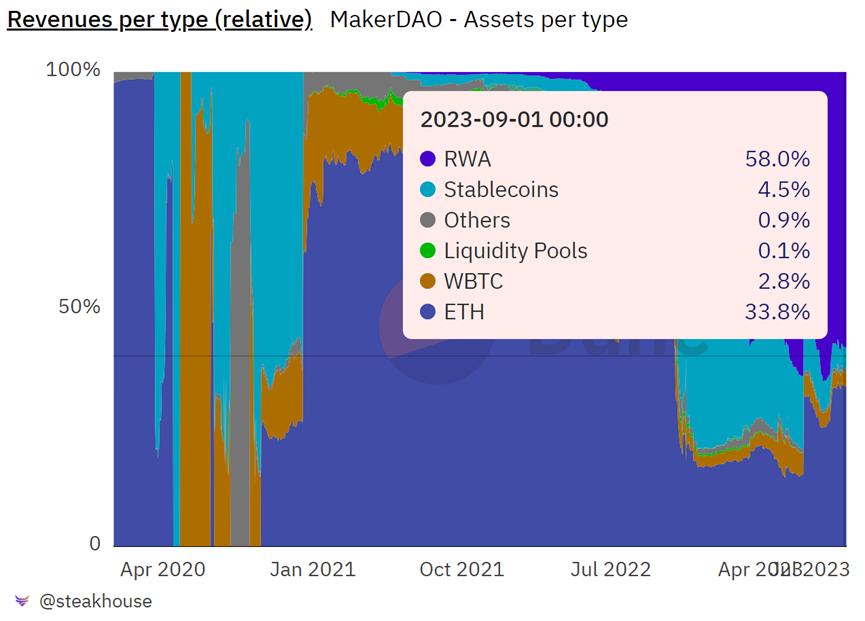

Before the launch of Monetalis Clydesdale in October 2022, only 2% of DAI was backed by RWAs, but in the 10 months since its introduction, the composition of Maker's balance sheet has fundamentally changed.

Currently, 47% of outstanding DAI is backed by RWAs, and these vaults generate 58% of Maker's revenue?

With the significant revenue inflow from RWAs in 2023, Maker is able to provide returns to MKR and DAI holders by restarting MKR burns and increasing the DAI Savings Rate (DSR)!

Since July 19, the marginal buyback pressure from the burns has undoubtedly contributed to the token's 40% rise against ETH.

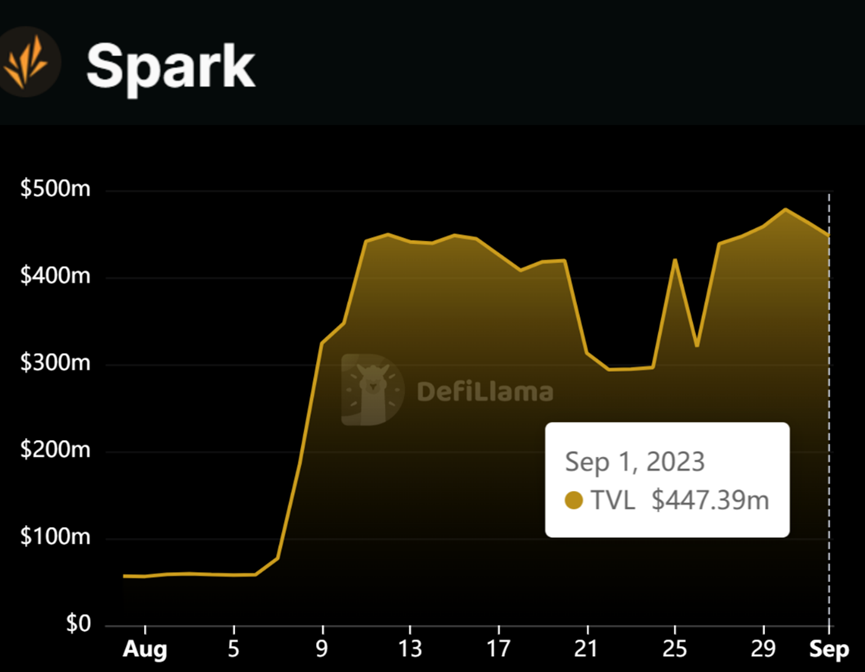

The soaring DSR yields have not been successful in combating the decline of outstanding DAI debt—this fate has tragically befallen nearly all stablecoins except USDT—but they certainly incentivize users to engage with Maker's money market—the Spark Protocol.

Since the DSR was first launched, the TVL of the Spark Protocol has surged significantly, currently nearing $450 million.

Maker is the fifth best-performing cryptocurrency among the top 100 so far this year, and the differentiating factor that has undoubtedly set it apart in 2023 is its RWA investment portfolio's yield-generating machine.

?Why U.S. Treasuries?

In TradFi, U.S. Treasuries are the optimal collateral, and their adoption within a decentralized financial system seems quite natural (to some extent).

Unlike other types of securities such as corporate bonds or receivables, U.S. Treasuries have almost zero default risk and are dubbed "risk-free" because the government has the ability to print new money to pay off old debts. In practice, this means that a portfolio holding short-term U.S. Treasuries has a risk profile similar to holding dollars while earning additional returns.

Tokenized stablecoins, such as USDT, serve well as settlement payment tools, but the current stablecoin model is not feasible for consumers seeking returns!

With TradFi yields at levels not seen in decades and cryptocurrency yields far below bull market peaks, now is the time for protocols to leverage RWAs. Maker is just one of the protocols trying to gain a competitive edge by using U.S. Treasuries as collateral.

Ondo Finance has attracted nearly $160 million in deposits for its Ondo Short-Term U.S. Government Bond Fund (OUSG). The associated money market Flux Finance has a TVL nearing $40 million, with outstanding loans of $25 million, and its fUSDC deposit receipts even consist of DeFi protocols like Pendle.

Credit-based RWA protocols have also not shied away from the tokenization game of the U.S. Treasury! Maple Finance recently launched its own cash management pool, putting funds to work by investing in U.S. Treasuries and reverse repurchase agreements (another type of ultra-low-risk security).

Frax Finance is another stablecoin issuer looking to expand its V3 product range by launching FraxBonds. A recent governance vote approved FinresPBC as a financial channel for V3, which will provide access to U.S. Treasuries, establishing high-quality yield sources for FraxBonds and offering infinite scalability.

The Future of Tokenization

U.S. Treasuries may be the starting point for mass adoption of tokenization, but the adoption of other forms of high-quality debt securities, which will be accepted by money markets and require little scrutiny or management, such as AAA-rated mortgage bonds and certificates of deposit, will not lag behind! Their secure yield streams can easily be converted into various financial products, helping to meet the endless demand for passive returns from market participants.

Undoubtedly, the biggest obstacle to future tokenization is the current lack of regulation. Large financial institutions are simply waiting for clearer regulations around cryptocurrencies before entering, and the success of tokenization depends on unresolved regulatory and legal issues in the cryptocurrency space.

The globally inconsistent regulatory framework is also a major risk for tokenization. While cryptocurrencies may be a global phenomenon, differing regulations across countries will only isolate markets. This will pose significant challenges for companies forced to navigate the different characteristics of digital asset frameworks and hinder the formation of a truly global asset market, thus limiting the full potential of tokenization.

Once cryptocurrencies gain clear regulations paving the way for institutions, our initial tokenized products will occupy traditional financial markets with no turning back!

Businesses love to create operational and cost efficiencies, and once they realize they can save costs through tokenization, they will quickly shift everything on-chain. Everyone will flee the traditional financial system in exchange for the liquidity of the global blockchain market, where they can achieve instant settlement and complete transparency.

Despite the regulatory hurdles, one thing is certain: tokenization will continue to exist!

As we await clarity, remember that the increasing popularity of U.S. Treasuries in the crypto space (and the specific types of securities that money markets will accept) is laying the groundwork for an inevitable asset tokenization-led bull market?