LD Capital: Changes and Impact of GMX V2

The GMX V2 version was officially launched on August 4, 2023. This article reviews the development of GMX V1 and the issues it faced, compares the modifications in V2, and analyzes the potential impacts.

The GMX V2 version was officially launched on August 4, 2023. This article reviews the development of GMX V1 and the issues it faced, compares the modifications in V2, and analyzes the potential impacts.Original Author: duoduo, LD Capital

The GMX V2 version officially launched on August 4, 2023. This article reviews the development of GMX V1 and the issues it faced, compares the modifications in V2, and analyzes the potential impacts.

GMX V1: An Effective Model for Derivatives DEX Protocols

The GMX V1 version was launched at the end of 2021, adopting the GLP model, which provided a simple and effective trading model, creating the narrative concept of "real yield," and holding an important position in the derivatives DEX protocol space. Many projects have forked the GMX V1 model.

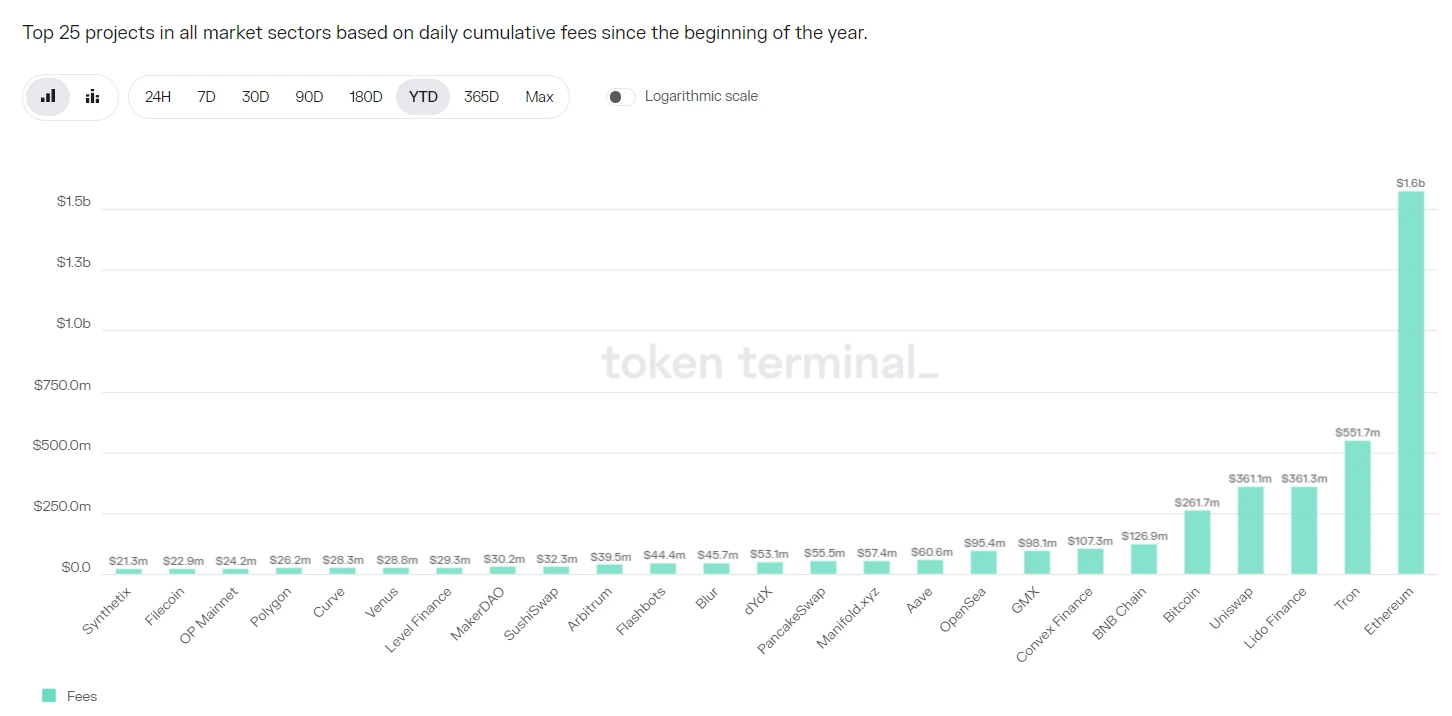

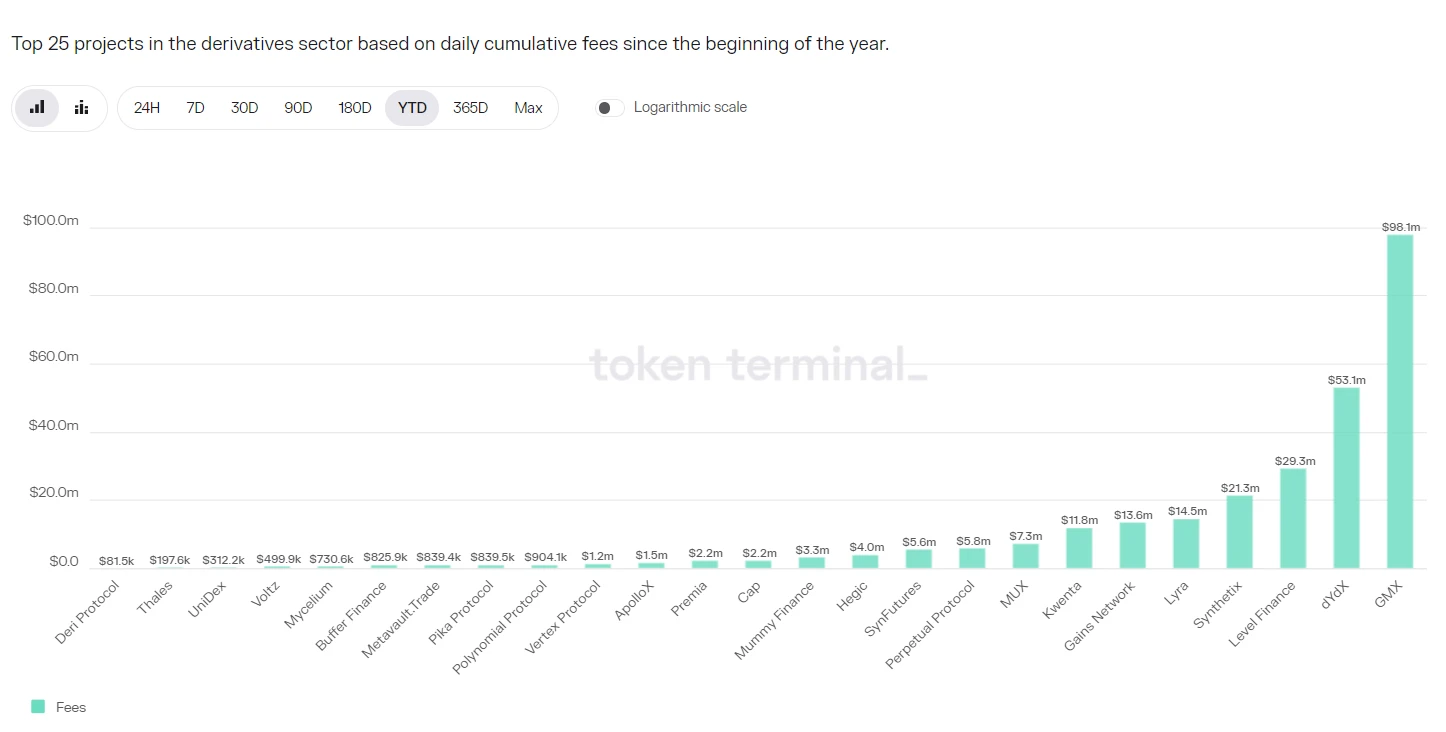

The GMX V1 protocol captured a significant amount of fees. Since 2023, GMX V1's revenue has reached $98.1 million, ranking eighth among all projects and first in the derivatives DEX sector.

Source: token terminal

However, GMX V1 also had limitations, mainly including:

- The imbalance of open interest (OI) poses significant risks to LP providers.

The fees for GMX V1 consist of opening/closing fees and borrowing fees, with no funding rates. Borrowing fees create a cost for holding positions, thus preventing liquidity from being indefinitely consumed. Additionally, the dominant side must pay more fees; however, since both long and short sides are charged fees, there is no arbitrage space, and open interest cannot quickly restore balance through arbitrage.

If this imbalance is not addressed, in extreme cases, the GLP pool may face significant losses, causing LP providers to incur losses and leading to the collapse of the protocol.

- Limited tradable assets.

GMX V1 only allows trading of five assets: BTC, ETH, UNI, LINK, and AVAX. In contrast, DYDX and Synthetix can offer dozens of trading varieties. Gains provides forex trading options. The new platform HMX offers commodities and US stock varieties.

- High fees for small and medium-sized traders.

The opening and closing fees for GMX V1 are both 0.1%, which is relatively high. In a competitive derivatives DEX space, many protocols have fees below 0.05%.

GMX V2: Ensuring the Security and Balance of the Protocol

1. Core

The core of GMX V2 is to ensure the security and balance of the protocol by modifying the fee mechanism to maintain balance between long and short positions, thereby reducing the probability of systemic risk for GMX during extreme market fluctuations. By setting up isolated pools, it increases high-risk trading assets while controlling overall risk. Collaborating with Chainlink provides more timely and effective oracle services, reducing the likelihood of price attacks. The project team also considered the relationships among traders, liquidity providers, GMX token holders, and the sustainable development of the project, ultimately adjusting and balancing the distribution of protocol revenue.

2. Fee Model Adjustment: Increasing Funding Rates and Price Impact Fees

The fee model of GMX V2 has undergone significant adjustments, focusing on how to promote balance between long and short positions and improve capital efficiency. The specific fee model is as follows:

- Lower opening/closing fees.

Reduced from 0.1% to 0.05% or 0.07%, depending on whether the opening is beneficial for balancing long and short positions; if beneficial, a lower fee is charged.

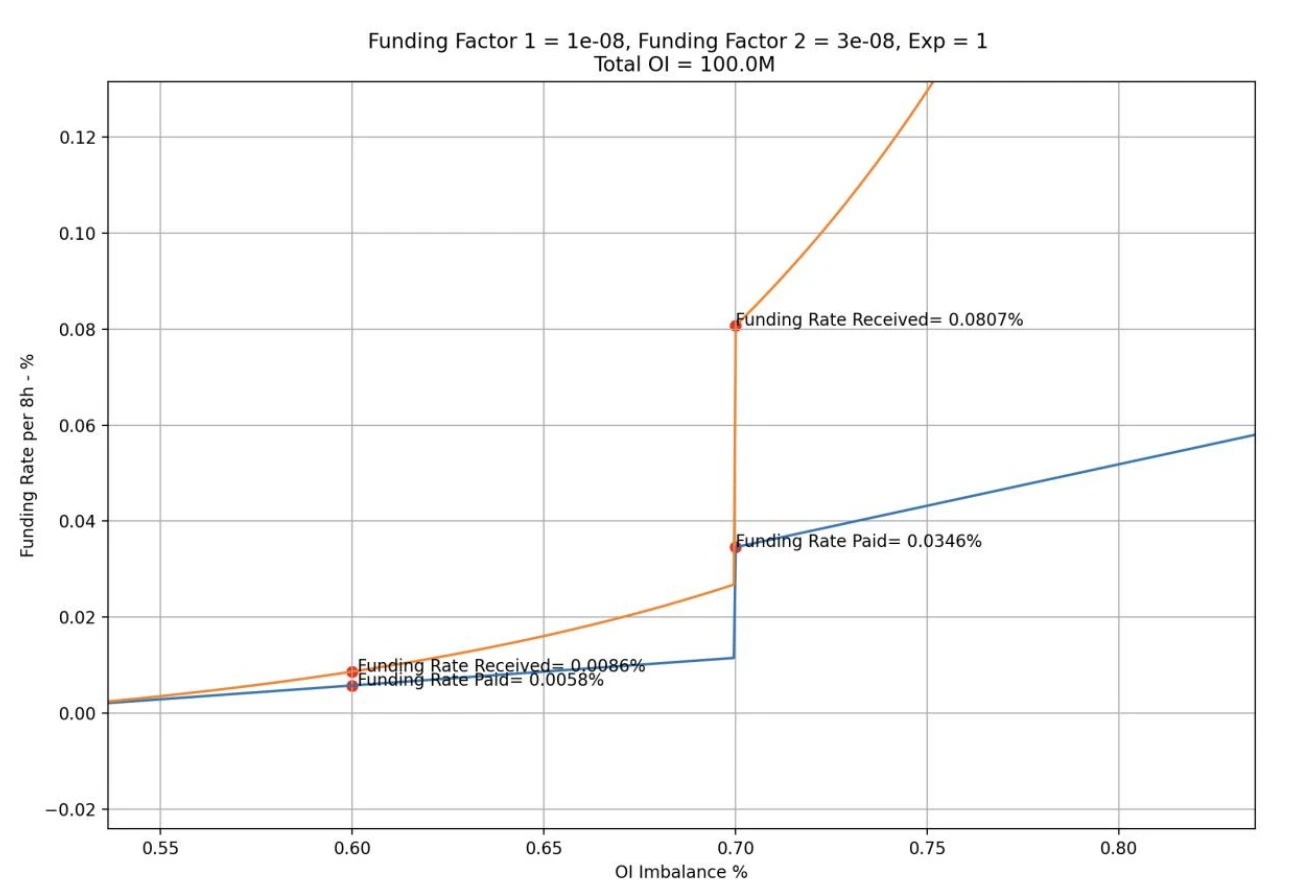

- Increase funding rates, with the strong side paying funding rates to the weak side.

Funding rates will be adjusted in segments; when the strong side's position/full position is between 0.5 and 0.7, the funding rate will be at a lower level; when it reaches 0.7, it will increase to a higher level, expanding arbitrage opportunities and encouraging arbitrage capital to enter, thus restoring the balance between long and short positions.

Source: chaos labs

Retain borrowing fees to prevent liquidity from being indefinitely consumed.

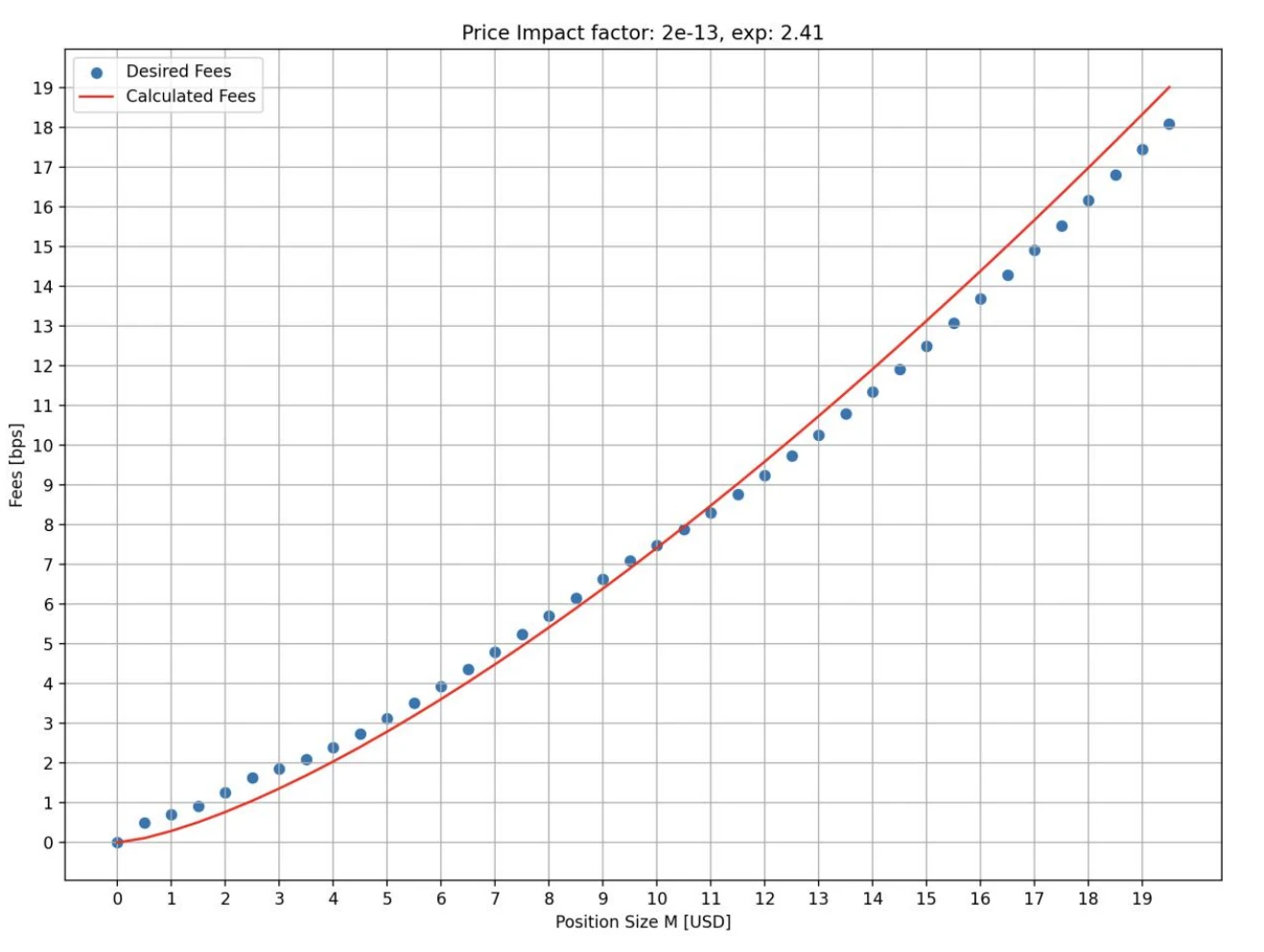

Increase price impact fees; the larger the position and the more unfavorable it is for the balance between long and short positions, the higher the fee charged.

Price impact fees simulate the dynamic process of price changes in the order book trading market, meaning that the larger the position, the greater the impact on price. This design can increase the cost of price manipulation, reduce the likelihood of price manipulation attacks, prevent price flash crashes or spikes, and maintain balanced long and short positions, ensuring good liquidity.

The following chart shows the price impact fee rates faced by different opening sizes in a simulated state, indicating that the larger the position, the higher the rate. The horizontal axis represents the opening size (in millions of dollars), and the vertical axis represents the rate (in bps).

Source: chaos labs

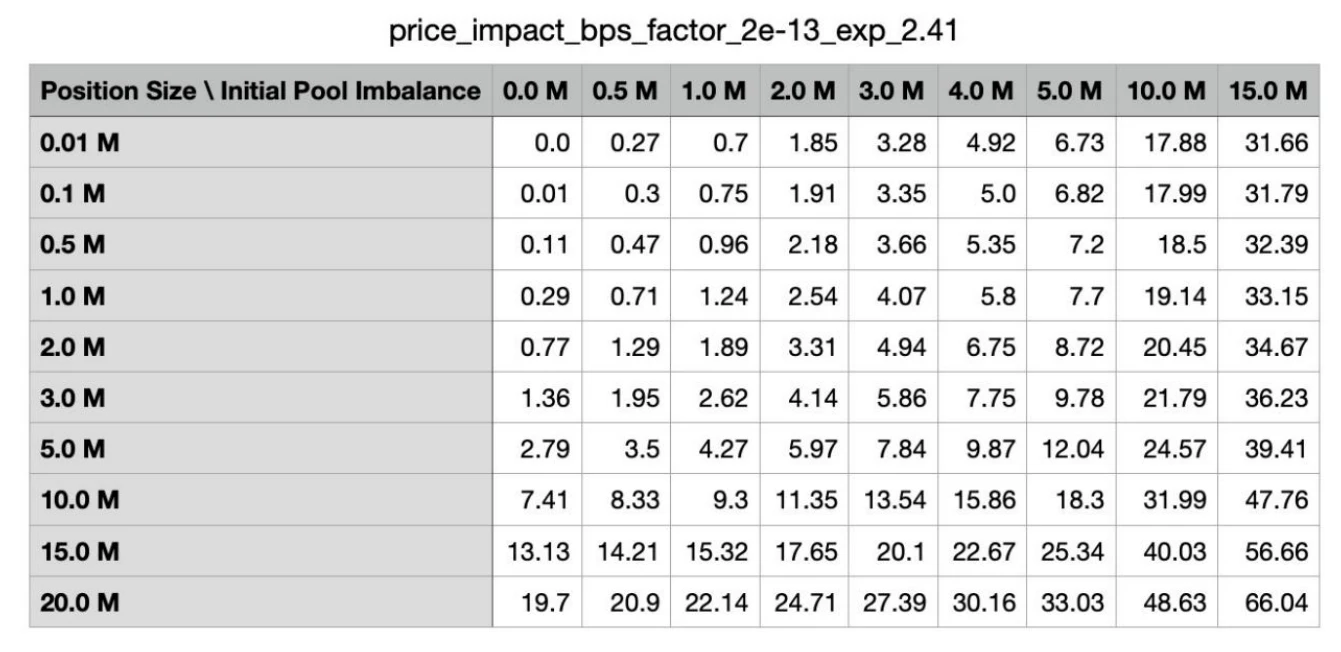

Additionally, if the opening is more unfavorable for the balance between long and short positions, the fees will also be higher. The following table shows the fees charged under different long and short balance states in a simulated environment. The first column represents the opening size, and the first row represents the scale of the initial pool's imbalance.

Source: chaos labs

A brief comparison of the fees of several major derivatives DEX protocols:

DYDX: maker 0.02%, taker 0.05%, with larger trading volumes resulting in greater discounts;

Kwenta: maker 0.02%, taker 0.06%-0.1%;

Gains Network: 0.08% opening/closing fee + 0.04% spread + price impact fee.

It can be seen that GMX V2's fees are still relatively high, but they have been reduced from a higher level to a medium level, with opening/closing fees decreasing by nearly 50%. For small and medium-sized traders, the fees in V2 are more friendly.

3. Liquidity Provision: Increasing Isolated Pool Model and Synthetic Assets

The liquidity pools in GMX V2 are called GM pools, and each pool operates independently. The website displays the fund amount, funding rate, and capital utilization rate for each pool.

Source: GMX

The advantage of isolated pools is that different token markets can have different underlying supports and parameter settings, achieving their own risk control with a high degree of flexibility, thus expanding trading assets while keeping risks controllable. For liquidity providers, they can also choose their risk exposure based on risk preference/return expectations. The issue with isolated pools, however, is the fragmentation of liquidity. Some liquidity pools may not attract sufficient liquidity.

Currently, GMX V2 has divided into three different types of markets:

Blue-chip: BTC and ETH. These two tokens have a lower likelihood of price manipulation, so the price impact fees can be set at lower rates, making them more competitive than CEX. Both are supported by native tokens.

Mid-cap assets: Assets with a market cap between $1 billion and $10 billion, which have significant liquidity and trading volume on CEX but are susceptible to external factors causing sharp price fluctuations, such as regulatory news leading to significant price drops. For such assets, the price impact fees will be set at a higher ratio, and liquidity will not exceed that of other external markets, increasing the cost of attacks. LINK, UNI, AVAX, ARB, and SOL fall into this category. They are supported by native tokens.

Mid-cap synthetic assets: These do not use native tokens but use ETH as the underlying liquidity support. DOGE and LTC belong to this category.

The issue with these assets is that if the related tokens experience a significant short-term increase, the ETH in the pool may struggle to cover all profits.

For example, if there are 1,000 ETH and 1 million USDC in the pool, the maximum long DOGE position limit is 300 ETH, but if DOGE's price rises tenfold while ETH's price only rises twofold, the profit will exceed the value of ETH in the pool.

To avoid this situation, an ADL (Automatic Deleveraging) function has been introduced. When the profit exceeds the threshold set by the market, the profitable position may be partially or fully liquidated. This helps ensure that the market always has solvency and that all profits at the time of closing can be fully paid. However, for traders, automatic deleveraging may lead to the loss of advantageous positions, resulting in missed subsequent profits.

According to the report issued by Chaos Labs, it is recommended that during the initial operation of V2, the upper limit of open interest for BTC and ETH be set at $256 million each, and $4 million for AVAX/LINK, while the limit for other tokens is $1 million. Adjustments can be made based on actual operational conditions. Currently, the total TVL of the GM pool is approximately $20 million, which is still far from the upper limit.

4. Enhancing User Experience: Adding Coin-Margined Contracts, Faster Execution Speed, and Lower Slippage

In GMX V1, traders could only open USDC-margined contracts. Regardless of the asset used by the trader to open a position, the position value was calculated in USD at the opening price, and the profit equaled the USD value at closing minus the USD value at opening.

In GMX V2, coin-margined contracts have been added. Traders can deposit the relevant trading assets as collateral without converting to USD. This will meet more of the traders' needs and provide a richer investment portfolio.

Additionally, GMX V2's oracle system will price every block, executing orders as close to the latest price as possible, resulting in faster execution speeds and lower slippage.

5. Distribution Model

To maintain the long-term development of the project, the protocol revenue of GMX V2 has also been adjusted. 8.2% will be allocated to the protocol treasury for project operations and other matters.

GMX V1: 30% allocated to GMX stakers, 70% allocated to GLP providers.

GMX V2: 27% allocated to GMX stakers, 63% allocated to GLP providers, 8.2% allocated to the protocol treasury, and 1.2% allocated to Chainlink. This allocation has been approved by community vote.

GMX V2 Operational Status

GMX V2 has been operational for about two weeks, with a TVL of approximately $20 million, an average daily trading volume of $23 million, an average daily protocol revenue of $15,000, open interest of $10.38 million, and daily active users ranging from 300 to 500. As a starting phase, the performance is acceptable without trading incentives.

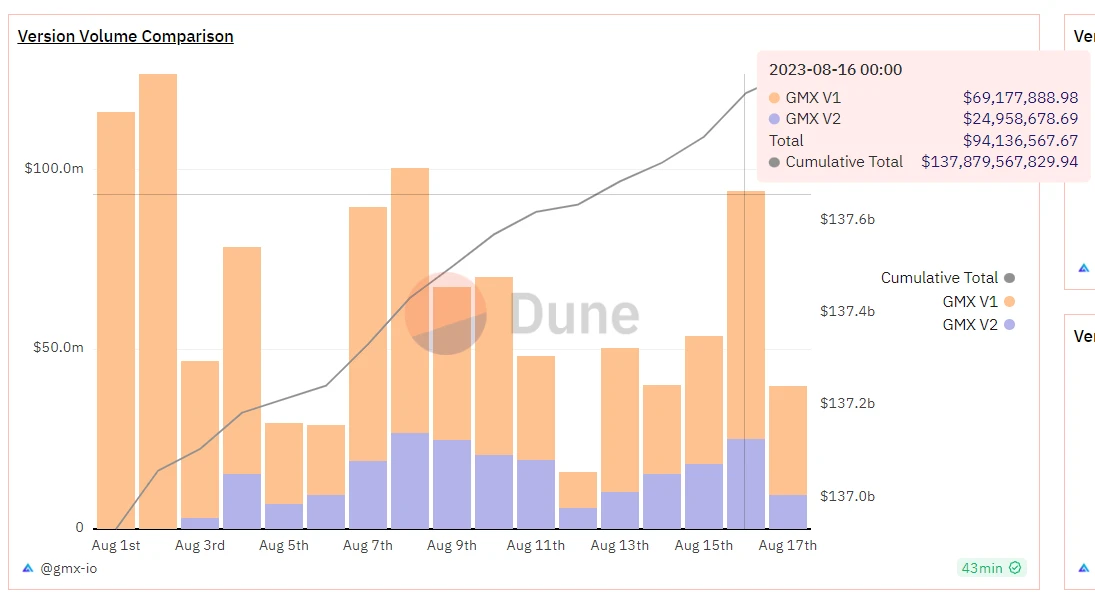

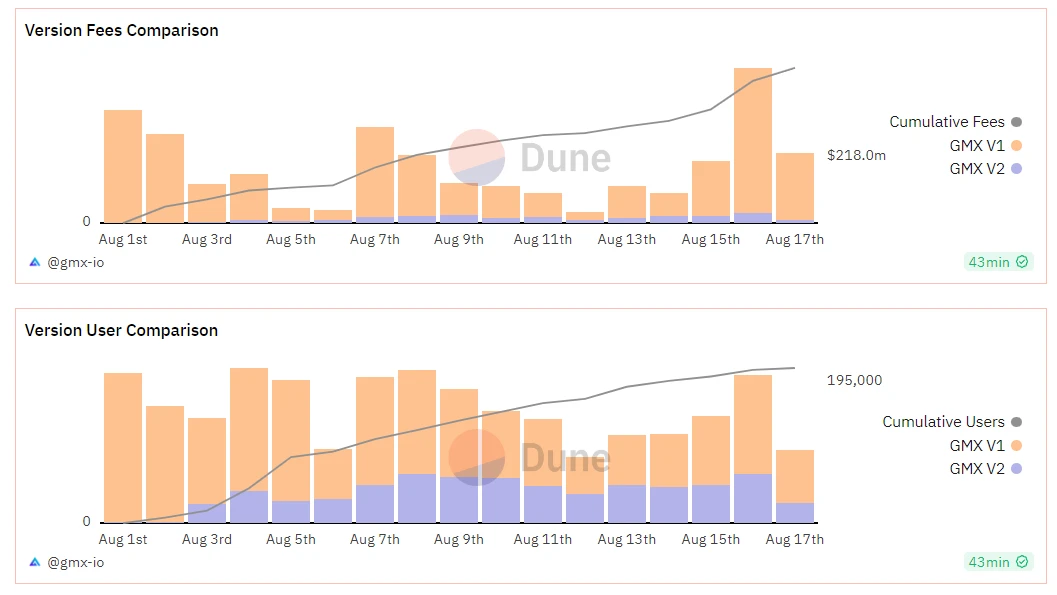

Some users from V1 have already migrated to V2. The trading volume and daily active users of V2 are roughly equivalent to 40%-50% of V1's trading volume. The comparison of trading volume, protocol revenue, and users between V1 and V2 is shown in the following charts:

Source: dune

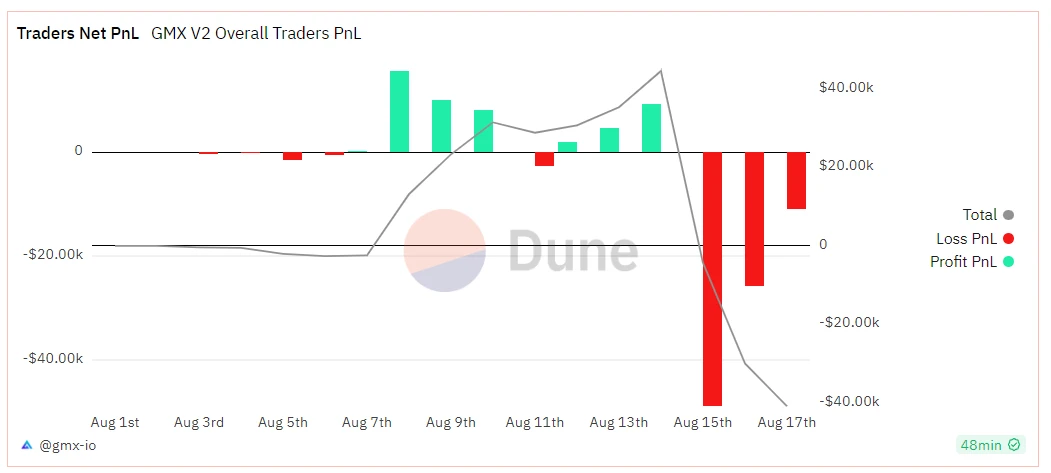

Currently, GMX V2 traders are in a net loss position, with a cumulative net loss of $40,000.

Source: dune

In terms of yield, GMX V1's recent yield has remained sluggish, with this week's GMX staking yield at 1.44%, GLP (Arbitrum) at 3.18%, and GLP (Avalanche) at 8.09%. In contrast, GMX V2's yield is higher, as shown in the following list:

Source: GMX

After the launch of GMX V2, market enthusiasm has been low, and the response from funds has been average. The main reason is that recent market volatility has dropped to historically low levels, overall trading volume has shrunk, and the sector is highly competitive, leading to sluggish growth in protocol revenue.

Conclusion

GMX V1 is a successful model in the derivatives DEX space, with many followers. The delivery of GMX V2 also largely meets market expectations, demonstrating the GMX team's strong protocol design capabilities. Mechanically, V2 has increased the balance of liquidity pools, expanded the types of trading assets, and provided various collateral positions. For liquidity providers and traders, investment methods are richer, risk balance is better, and fees are lower.

However, from the initial phase, due to the adoption of independent pools, there is a problem of liquidity fragmentation, and some assets may suffer from insufficient liquidity. Additionally, the GM project team has not taken significant marketing actions or trading incentive measures, which have not had a noticeable impact on new users and trading volume in the short term.

Essentially, GMX V2 focuses more on protocol infrastructure, security, and balance. In the current bear market environment, concentrating on building the underlying architecture, ensuring protocol security, and utilizing accumulated data for better risk parameter design may be more beneficial for the project's future development in a bull market. At that time, it could provide higher open interest capacity, a richer trading market, and launch more marketing measures to attract new users in line with market enthusiasm.