Overview of the current development status of NFT lending protocols: What innovations and unresolved issues exist?

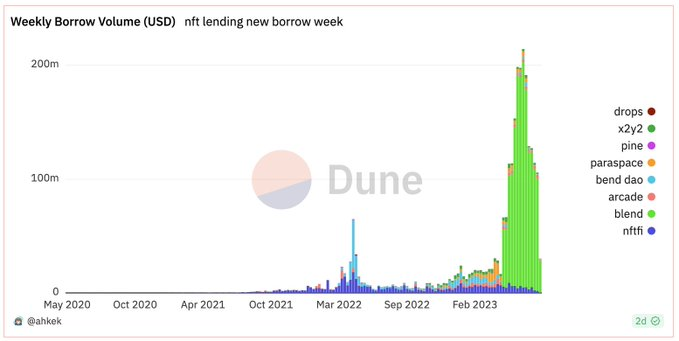

The price of NFTs may decline, but the NFT lending market is thriving, with over $2.1 billion in loans issued on Ethereum (ETH) NFTs this year, bringing new opportunities to the art lending market.

The price of NFTs may decline, but the NFT lending market is thriving, with over $2.1 billion in loans issued on Ethereum (ETH) NFTs this year, bringing new opportunities to the art lending market.Original Title: How does NFT lending work today? and why you should pay attention?

Original Author: mitchelljhammer

Compiled by: 火火,白话区块链

The price of NFTs may have dropped, but NFT lending is booming. Over $2.1 billion in loans have been issued on Ethereum (ETH) NFTs this year.

This is equivalent to twice the art loan portfolio of Sotheby's and about 10% of the total art loan market. How does NFT lending work now? Why should we pay attention to it?

1. The Current State of NFT Lending

NFT lending protocols allow holders to gain liquidity without selling their NFTs. Users lock their NFTs as collateral in smart contracts and then withdraw liquidity funds.

There are currently two main lending models in the market: Peer-to-Peer (P2P) and Peer-to-Pool (P2Pool).

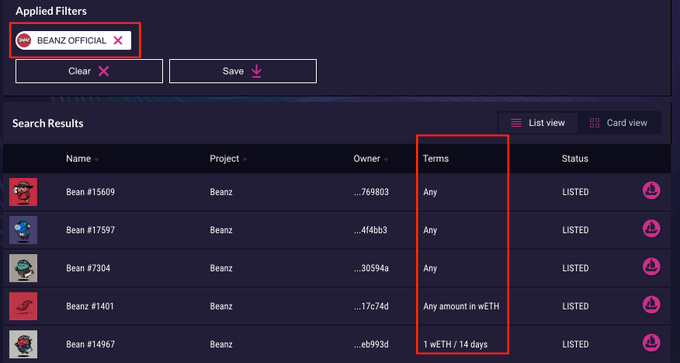

Peer-to-Peer (P2P) Lending: Peer-to-peer lending protocols include @Arcadexyz, @NFTfi, and @thex2y2. These protocols match individual lenders with individual borrowers based on preferences. For example, if I want to lend to a holder of Beanz, I can search for loan terms that meet my risk/return requirements on @NFTfi.

Peer-to-Pool (P2Pool) Lending: Peer-to-pool lending protocols include @BendDAO, @ParaSpace_NFT, @TheBNNFT, and @dropsnft. These protocols allow borrowers to instantly withdraw liquidity from existing pools, similar to how @AaveAave and @compoundfinance operate with fungible tokens.

Both models have their pros and cons:

The Peer-to-Peer (P2P) model is more suitable for niche/long-tail NFTs. However, loan matching takes time, loan terms are fixed, and lenders face higher risks.

The Peer-to-Pool (P2Pool) model is more suitable for mainstream NFTs, offering instant liquidity and distributed risk. However, interest rates/collateral ratios do not consider characteristics and rely on oracles.

2. Improvements in the Current Market

New models are emerging to improve the existing Peer-to-Peer (P2P)/Peer-to-Pool (P2Pool) paradigm.

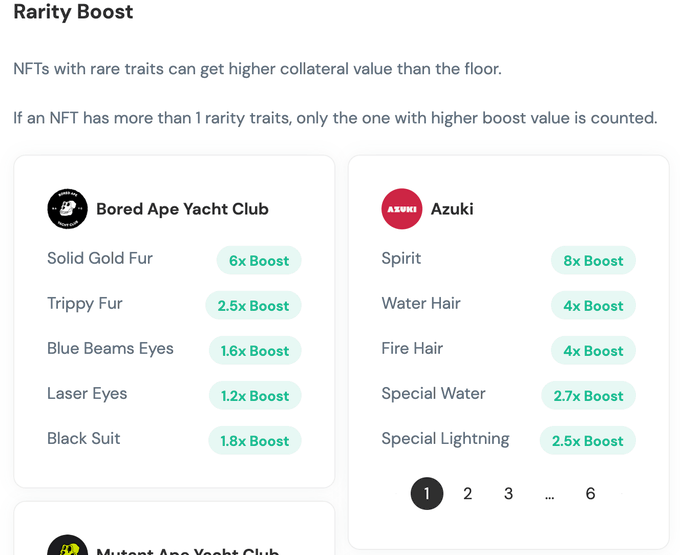

Blend (@blurio) uses an order book to aggregate lender offers, thereby increasing liquidity and enabling efficient refinancing. @ParaSpaceNFT offers rarity boosts to lower the collateral ratios for higher-value NFTs.

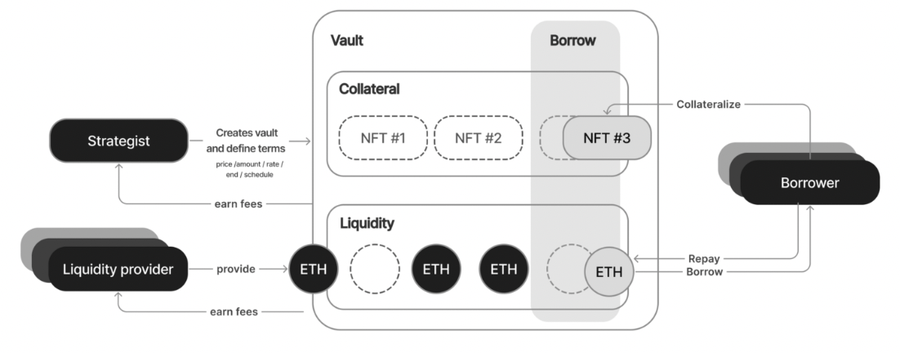

@AstariaXYZ employs a three-party system. Liquidity providers pool funds into a vault and delegate the loan underwriting process to strategists.

@metastreetxyz uses layered lending. Borrowers can specify their lending risk preferences. Risks are segmented, but liquidity is shared among borrowers.

3. The Future of NFT Lending

These protocols are building key foundational components for NFT lending. However, we still need to address some major issues, including:

- Better balancing the interests of borrowers and lenders

- Easier position management

- Improved protocol interoperability.

1) Balancing Borrower/Lender Interests

Lenders should receive appropriate risk compensation, while borrowers should obtain reasonable loan terms. Achieving this in the volatile NFT market is not easy. Prices can drop rapidly, leading to borrower liquidations and bad debts.

Moreover, current lending protocols pay interest at maturity, which means that lender risks increase over the loan term.

As a result, current NFT loans are characterized by short terms and high interest rates, adding friction and costs for both sides of the market.

Implementing repayment plans, as seen in traditional finance, would help reduce lender risks during the loan period.

The reduction of lender risk would be passed on to borrowers in the form of longer terms and lower interest rates.

2) Easier Position Management

Today, managing your NFT lending or borrowing positions requires a full-time job. You need to constantly monitor prices and act quickly to avoid liquidation or holding worthless collateral.

This is a poor user experience for most people.

Telegram and email alerts are a good first step to help people manage their loan positions.

More advanced features, such as automatic repayments, liquidation insurance, and hedging tools, could further enhance the user experience for both lenders and borrowers.

3) Improved Interoperability

To borrow against your NFT, you need to deposit it into a smart contract. This operationally means that the utility associated with your NFT (airdrops, governance) will also be transferred.

But this is not the case in traditional secured loans. Even if your house is mortgaged, you can still continue to live in it!

Using your NFT as collateral should not mean you have to stop using it!

We need to establish standards and build in a way that allows borrowers to access the underlying utility of their NFTs while they are used for lending or other financial protocols.

4. Why Should We Care?

The lending market is a key financial infrastructure for all major markets. It enhances market efficiency, promotes growth, and expands market access.

Building the right lending mechanisms ensures that protocols can handle trillions of dollars in demand once most assets are encoded as NFTs.