"Islamic Coin" has attracted attention; what are the secrets of Islamic finance?

The blockchain project Islamic Coin, compliant with Islamic law, announced a significant investment of $200 million, bringing the total funding to a record scale of $400 million. Among the project's advisors are several members of the royal families of Abu Dhabi and Dubai, as well as Islamic finance experts.

The blockchain project Islamic Coin, compliant with Islamic law, announced a significant investment of $200 million, bringing the total funding to a record scale of $400 million. Among the project's advisors are several members of the royal families of Abu Dhabi and Dubai, as well as Islamic finance experts.Author: The Dark Side of the Moon, PANews

Recently, the blockchain project Islamic Coin, compliant with Islamic law, announced it has secured a substantial investment of $200 million. Combined with the $200 million funding it received in 2022, its total financing has reached a record $400 million. The project is actively promoting itself in Islamic regions such as the UAE, launching a large number of advertisements targeting Twitter users. According to its official website, several members of the royal families from Abu Dhabi and Dubai, as well as Islamic finance experts, are among its advisors.

Islamic Coin is built on the Haqq blockchain, and due to its adherence to Islamic financial laws, it cannot use conventional means such as interest. Instead, it will allocate 10% of the token issuance to the Evergreen DAO to support Islamic charitable causes. Although the Haqq blockchain does not require projects to be halal to use it, they must comply with Islamic principles and obtain certification through community voting.

What are the Islamic financial laws emphasized by Islamic Coin, and how do they differ from contemporary financial laws? This article will briefly introduce some knowledge related to Islamic finance to help readers and entrepreneurs explore the possibilities of adhering to Islamic laws in the cryptocurrency field.

Prohibition of Interest, Allowing Profit Sharing

Before delving into the definition and discussion of Islamic finance, it is essential to lay the groundwork with relevant knowledge about Islam and Islamic law, ultimately leading to Islamic finance. Islam is widely distributed around the world, with approximately 1.9 billion Muslims (followers of Islam) as of 2020, accounting for 25% of the global population.

Muslims are divided into two major sects: the Sunni, which constitutes 70%-80% of the population, represented by countries such as Saudi Arabia, and the smaller Shia sect, which accounts for 10%-15%, represented by Iran. Beyond these two mainstream sects, there are smaller sects, such as the Ibadis represented by Oman, which is currently the third largest sect. However, there are many smaller sects, and even within Sunni and Shia, more refined divisions can be identified. For instance, the version of Sunni Islam practiced in Saudi Arabia is actually Wahhabism, which is the mandatory belief of all royal family members and is the state religion of Saudi Arabia.

These sects all adhere to the Quran, but their specific interpretations of Islamic law are not uniform. For example, Islamic Coin claims to comply with Islamic law, which can actually be understood as Sharia law, closer to what we refer to as "law" rather than more specific concepts like criminal law or civil law.

Due to the lack of complete consistency between Islam and so-called Islamic law, major Islamic countries around the world engage in some degree of consultation to establish a financial standard that can be universally applied within Islam.

Islamic finance, in a narrow sense, refers to banking that operates in accordance with Islamic law as its main characteristic. Muslim countries have both Islamic banks and modern banks from Europe and America. For example, Dubai has both Dubai Islamic Bank and HSBC.

In addition, Islamic bonds, Islamic insurance, and Islamic funds are also developing, but their scale is significantly smaller than that of Islamic banks. It is important to note that the sovereign wealth funds of oil-rich Middle Eastern countries operate entirely on a Western model and cannot be included in the Islamic finance system simply because of their large scale.

According to the principles of Sharia law, all products that comply with Islamic finance share the following common points:

- Absolute prohibition of interest. Even when depositing in an Islamic bank, one cannot earn returns in the name of interest.

- Profit-sharing mechanism. Unlike the aversion to interest, Islamic finance allows for profit through investment.

- Focus on tangible assets. Financial products need to be based on physical assets, making gold the most popular investment.

- Prohibition of speculative activities. This mainly targets restrictions on gambling, options, derivatives, etc.

- Sharia law as the foundational principle. However, due to the lack of consensus and standards within Sharia law itself, it needs to be established through practice.

Current State of the Islamic Finance Market, Crypto Begins to Penetrate

In practice, a broad consensus and standard have been established for gold trading, which is the most sought-after investment among Muslims globally. The "AAOIFI Islamic Law Gold Standard" was introduced in 2016, jointly developed by the World Gold Council and AAOIFI (Accounting and Auditing Organization for Islamic Financial Institutions). This standard includes the following five most important principles:

- Gold must be traded on a spot (hand-to-hand) basis;

- Gold holdings can be in physical or deemed form;

- In the case of deemed holdings, all gold must be allocated;

- Allocation can be conducted through T+0 settlement or by receiving a certificate/confirmation of ownership of designated gold bars;

- Joint ownership is allowed, meaning each partner has an indivisible beneficial interest in the trust.

Moreover, this standard has been recognized by the Sharia law committee, which consists of 20 scholars from various countries, marking a significant theoretical level for the standard.

- In addition to the aforementioned AAOIFI, other international standard-setting organizations for Islamic finance include the Islamic Financial Services Board (IFSB) and the International Islamic Financial Market (IIFM).

Currently, Islamic finance practice is highly concentrated in the banking sector, and it is difficult to say that there are truly successful products in cryptocurrency practice. However, like other financial products, as long as they comply with Islamic law, it means there is a vast market.

From a segmented classification perspective, Islamic finance can be divided into Islamic banking, Islamic insurance, Islamic bonds, Islamic funds, and other Islamic financial institutions (OIFI), such as cryptocurrencies.

In terms of market value and scale, there are two imbalances: first, Islamic finance is primarily concentrated in banking, with a total value of around $2 trillion, accounting for nearly 70%, while other parts account for a very small proportion; second, Islamic banking only occupies about 6% of the global banking market share.

This is mainly because Islamic banks cannot attract depositors' assets with high interest rates, nor can they engage in speculative activities or enter the derivatives market. While this limits their significance in the global banking sector, it also brings extremely high security. The main investment targets of Islamic banks are tangible assets such as real estate and leasing, which have strong resilience.

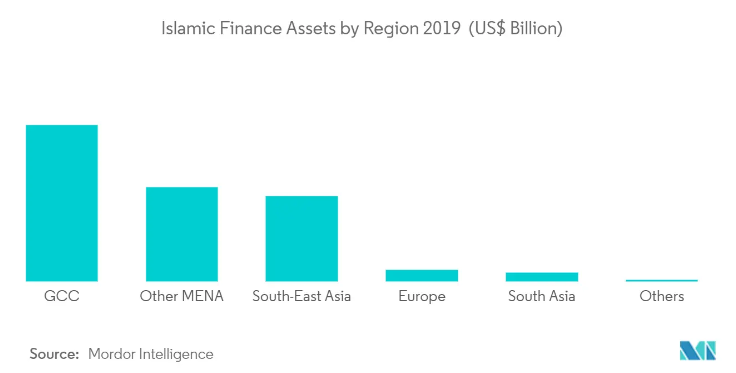

Geographically, due to the oil wealth effect of Gulf countries, the six Gulf Cooperation Council (GCC) countries (Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain) also have the highest asset proportion, but their population does not account for a high percentage in the Islamic world, with the 35 million scale largely covered by Saudi Arabia.

As of 2019, the Islamic financial assets of the GCC reached $1.253 trillion, accounting for 44% of total assets, followed by other regions in the Middle East and North Africa (MENA) with a combined $755 billion, accounting for 26.3%, and Southeast Asia (Malaysia and Indonesia) at 24%. Europe, Asia, the Americas, and Africa account for very small proportions.

Beyond traditional Islamic finance, various new financial technology products, including cryptocurrencies, are gradually penetrating the Muslim world. In principle, most of these innovations belong to other Islamic financial institutions (OIFI), while Bitcoin and cryptocurrency trading have been growing robustly despite ongoing crackdowns.

If it operates smoothly, Islamic Coin will be the first cryptocurrency issued in compliance with Islamic law. As a blockchain that claims to have raised $400 million, its coin price is entirely determined by the market to comply with Islamic law and is available for use by Muslims worldwide, which is a positive development for the current cryptocurrency market that urgently needs to expand its user base.

It is important to note that not all blockchain projects that are fully compliant with Islamic law can operate in the Islamic world. For example, Ripple has been actively engaging with the Saudi Arabian Monetary Authority (SAMA), and commercial banks in the country are also participating in the Ripple enterprise network to explore its use cases in cross-border remittances.

Additionally, Dubai is actively attracting various cryptocurrency companies to set up operations, such as Binance, which has already opened an office in Dubai.

Conclusion

Islamic Coin attracts market attention with its dual selling points of substantial financing and compliance with Islamic law. This article aims to introduce relevant knowledge of Islamic finance to Chinese readers. At least in the case of wealthy Middle Eastern countries, their attitude towards blockchain is not entirely closed or prohibitive; rather, they are examining the opportunities within it. Even if it does not fully comply with Islamic law, there are still potential collaboration points in other areas.