RWA Talk: Underlying Assets, Business Structure, and Development Path

The narrative of RWA includes a rich variety of asset types and covers a wide range of yields.

The narrative of RWA includes a rich variety of asset types and covers a wide range of yields.Author: Colin Lee, Mint Ventures

Since the beginning of the year, discussions around RWA (real world assets) have become increasingly frequent in the market, with some viewpoints suggesting that RWA will trigger the next bull market. Some entrepreneurs have also adjusted their focus to RWA-related tracks, hoping to leverage the gradually warming narrative to accelerate business growth.

RWA refers to the mapping of assets from traditional markets onto the blockchain in the form of tokens, allowing web3.0 users to buy and sell these assets. RWA tokens possess the rights to the income generated by the underlying assets. A few years ago, STOs primarily focused on corporate bond financing, while the scope of RWA is now much broader: it is not limited to the primary market of traditional assets; any asset circulating in the primary and secondary markets can be tokenized and brought onto the blockchain, enabling web3.0 users to participate in investment. Thus, the narrative around RWA encompasses a rich variety of asset types and a wide range of yields.

The increasing market attention on RWA may be attributed to several factors: First, the current crypto market lacks low-risk USD-denominated assets, while in the traditional financial market, the risk-free interest rates of major economies have risen to 4% or even higher amid the interest rate hike wave, which is sufficiently attractive to investors in the crypto-native market. Correspondingly, during the bull market of 2020-2021, many traditional funds entered the crypto market, earning low-risk returns through arbitrage and other strategies. Introducing low-risk, high-yield products from the traditional market through RWA may appeal to some investors; secondly, the crypto market is not currently in a bull market, and even within the crypto-native market, there is a lack of sufficient narratives. RWA is one of the few tracks currently observed with solid yield support, potentially leading to explosive business growth; finally, RWA serves as one of the bridges connecting the traditional market and the crypto market, providing opportunities to attract incremental users from the traditional market and inject new liquidity, which is undoubtedly beneficial for the development of the blockchain industry.

However, from the RWA projects currently observed, their business metrics, such as TVL, have not seen rapid growth, suggesting that the market may have overly high short-term expectations for RWA. For an RWA project, several dimensions need to be considered:

- Underlying assets. This is the core issue of the RWA track. Choosing suitable underlying assets greatly aids subsequent management.

- Standardization of underlying assets. Due to the varying "heterogeneity" of different underlying assets, the difficulty of standardizing these assets also differs. The more heterogeneous the asset, the higher the standardization requirements and the more complex the processes involved.

- Off-chain cooperation institutions and forms of collaboration. High-quality off-chain cooperation institutions can not only fulfill their obligations smoothly but also allow the value of the underlying assets to be fully realized.

- Risk management. The maintenance of underlying assets, asset tokenization, and income distribution all involve risk management. If the assets are debt-type, it also involves risk management in the event of debtor default, including asset liquidation and collection.

I. Underlying Assets

Underlying assets are the most critical element.

At this stage, the RWA track primarily categorizes underlying assets into the following types:

- Bond-type assets, mainly short-term U.S. Treasury bonds or bond ETFs. Typical representatives include stablecoins like USDT and USDC. Some lending projects, such as Aave and Maple Finance, have also joined this camp. Treasury bonds/bond ETFs currently represent the largest share of RWA;

- Gold, with PAX Gold as a typical representative. Still under the overarching narrative of "stablecoins," but developing slowly with weak market demand;

- Real estate-type RWA, with typical representatives like RealT and LABS Group. Similar to packaging real estate into REITs and then tokenizing them. The sources of real estate for these types of projects are diverse, and project teams often choose their own cities as the primary source of assets;

- Loan-type assets. Typical examples include USDT and Polytrade. The types of assets are quite broad, including personal home mortgages, corporate loans, structured financing instruments, auto loans, etc.;

- Equity-type assets, with typical projects including Backed Finance and Sologenic. The trading of these types of assets seeks to exist in reality but is greatly limited by legal issues. An important development direction for crypto-native "synthetic assets" is publicly listed stocks, which overlap significantly with this field;

- Others, including farms, artworks, etc., which are larger in scale (individual asset amounts are larger) but have a lower degree of standardization.

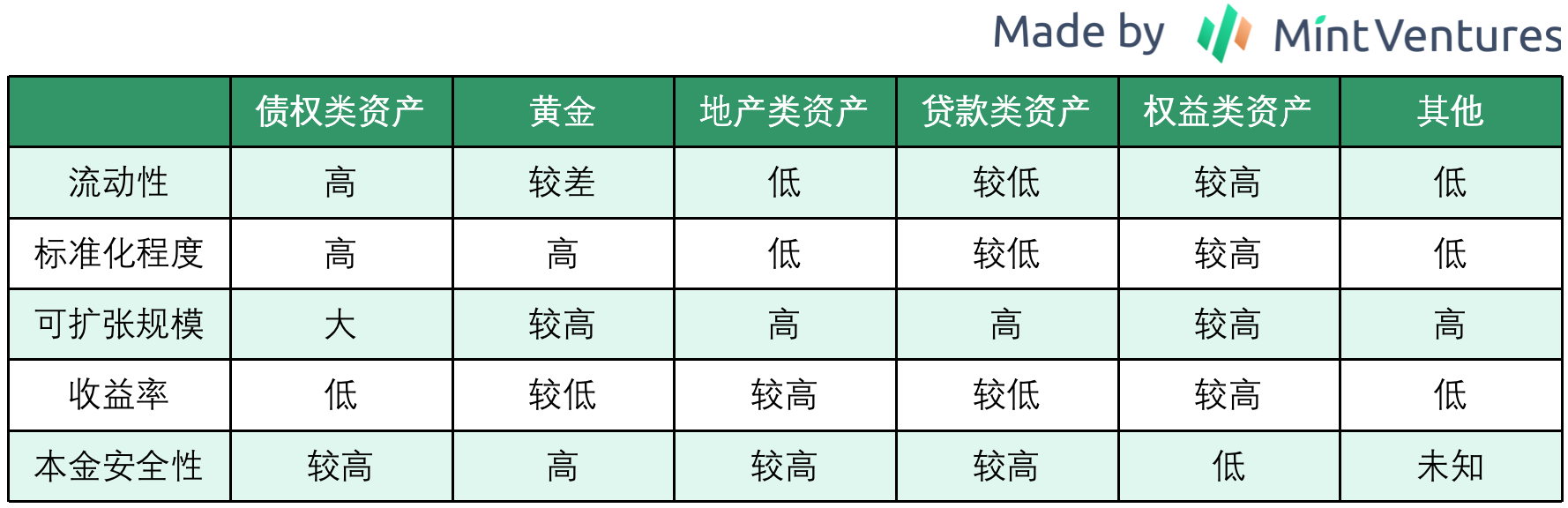

Choosing which assets to serve as underlying assets requires consideration of five dimensions: liquidity, degree of standardization, principal safety, scalability, and yield. From these five dimensions, we can roughly outline the attributes of the aforementioned assets.

From the perspective of underlying assets, debt-type assets currently appear to be the most promising category to explore, seeking differentiated routes based on their positioning: anchoring fiat stablecoins, crypto market money market funds, etc. Although the stablecoin track anchored to fiat currency is already dominated by oligopolies, with major projects forming ecological collaborations with numerous projects, the "crypto market money market fund" track still has room for exploration.

For real estate-type assets, although REITs solutions are already mature, if project teams decide to choose assets themselves and manage regional and property diversification, it will undoubtedly increase costs significantly: for instance, in project maintenance, if the geographical distribution is too dispersed, the number of people needed for property management will increase, and procurement costs for property maintenance and personnel transportation will also need to rise. During my review of projects, I encountered a project team that wanted to keep the value of individual properties under $100,000, distributed across more than five countries, and not limited to residential and commercial properties. While this may achieve sufficient diversification, it poses significant challenges in terms of information disclosure and property management. Achieving rapid growth of underlying assets in the future will also be difficult.

Currently, I do not recommend overly focusing on "other" types of underlying assets, primarily due to liquidity and standardization concerns. For example, agricultural-related underlying assets, due to their high degree of non-standardization, add considerable difficulty in determining the quality of the underlying assets. Taking a single farmland as an example, the quality of the crops produced can vary, and storage, transportation, and sales are relatively specialized processes. To ensure that the agricultural asset's returns ultimately reach investors, one would need to have deep industry experience over many years. The cyclical fluctuations in production capacity and weather factors faced by cash crops are also difficult to predict. Ultimately, monetization presents significant challenges.

If the project team seeks assets and packages them independently, the project's growth potential will also be significantly affected, making rapid growth even more challenging.

Regarding underlying assets, focusing on bond-type assets as the core direction and using REIT-like assets as a means to enhance yields may be a more practical and feasible approach.

II. Business Structure

If there were significant issues in bringing RWA onto the blockchain in previous years, a clearer path has now emerged under the exploration of leading projects like MakerDAO.

First, to facilitate the convenience of bringing RWA onto the blockchain, an RWA Foundation structure could be established. Under this structure, MakerDAO can manage multiple RWAs through the RWA Foundation, with new RWAs being directly initiated by the RWA Foundation to create SPVs (Special Purpose Vehicles).

Source: https://forum.makerdao.com/t/pre-mip-discussion-rwa-foundations/9510

Secondly, for individual SPVs, a management model similar to that of ABS (Asset Backed Securitization) projects can be adopted, where the assets serve as the basis for securitized financing:

Source: https://forum.makerdao.com/t/poll-rwa-working-group-covenant-structure/4836

Source: https://forum.makerdao.com/t/poll-rwa-working-group-covenant-structure/4836

To ensure the safety of funds, MakerDAO chooses to invest in priority assets, while other investors can become investors in subordinate shares. For other project parties, the risk level of the held assets can be determined based on the risk preferences of their target user groups.

Unlike traditional asset securitization steps, in MakerDAO's individual SPVs, there are no roles for settlement or fund custody, but a tokenization issuance platform is added. In the future, as regulatory frameworks become clearer, settlement and fund custody may still be essential participants in RWA.

III. Risk Management

Risk management for RWA primarily consists of three dimensions:

- Risk management of underlying assets. The lower the degree of standardization of an asset, the higher the required risk management capability. Compared to forests and farms, Treasury bonds have a high degree of standardization, better liquidity, and stronger price discovery capabilities. Therefore, managing Treasury bonds is less challenging. However, even within the same type of asset, the difficulty of management varies across different regions and countries. For example, in some developing countries, the level of digitization is low, and debt-type assets may still exist in paper form. This requires the project team to find a location to store large amounts of bonds that cannot be destroyed during the holding period. Assets existing in paper form also carry a significant risk of being "switched," with large-scale incidents occurring in many regions.

In summary, for risk management of underlying assets, the most fundamental requirement is to ensure that the underlying assets are real and effective during the project's duration. Secondly, it is essential to ensure that the value of the underlying assets is not subject to loss due to human factors. Thirdly, it should ensure that the underlying assets can be liquidated at a fair market price, and finally, it should ensure that income and principal can be safely and smoothly delivered to investors. These types of risks overlap significantly with the attributes of traditional assets, allowing for reference to existing risk management measures.

- On-chain risk management. Since this involves data being brought onto the blockchain, if off-chain institutions are not adequately managed, there may be instances of data falsification. Similar negative cases frequently occur in traditional finance, such as in commercial paper, supply chain finance, and commodities, where significant fraud has been reported. Even with real-time monitoring through sensors and fixed delivery locations, it is still impossible to completely avoid risks.

For the currently nascent RWA industry, I believe similar situations will arise, especially given the lack of corresponding regulatory details and the low cost of legal violations, making the risk of data falsification on-chain non-negligible.

- Risk management of partners. This type of risk still leans towards traditional concerns, but the issue is that there are currently no regulatory details specifically targeting RWA. For example, in the custody phase, what type of custody institution is compliant? In the auditing phase, can current accounting and financial standards accurately and completely reflect the characteristics of RWA? During the project's operation, if a risk event occurs, what type of risk disposal methods and processes can better protect investors? These questions still lack very precise answers. Therefore, partners still have opportunities to act maliciously.

IV. Current User Structure and User Needs

In the previous article "Outlook on the 'Native Bond Market' in the Crypto World," it was mentioned that due to the extreme volatility and cyclicality of the crypto market, relatively low-risk and conservatively risk-averse investors find it challenging to achieve sustained and stable returns in the market. In such a market, a large number of users also exhibit a strong risk appetite:

In a survey report released by the team at dex.blue in 2020, half of the surveyed crypto market users had invested 50% or more of their total savings into the crypto market; reports from Pew Research and Binance also noted that the current user base in the crypto market is predominantly young. In this market structure, crypto market investors tend to have a higher risk appetite than traditional market investors.

Source: https://medium.com/dexdotblue/defi-usage-survey-the-results-insights-b3481275019b

Source: https://medium.com/dexdotblue/defi-usage-survey-the-results-insights-b3481275019b

In the current market dominated by "arbitrageurs and high-risk investors," its volatility exhibits similar characteristics: research from K33 Research shows that from early 2017 to October 2022, Bitcoin's volatility was higher than that of the Nasdaq and S&P 500 for most periods, with only during extremely quiet market conditions did U.S. stocks' volatility occasionally exceed that of Bitcoin.

Source: https://k33.com/research/archive/articles/volatility-near-6-year-lows

Source: https://k33.com/research/archive/articles/volatility-near-6-year-lows

The two main investor groups in the crypto market may have different yield demands: for arbitrageurs, "low-risk" investment opportunities are more accessible, and such trading opportunities, exemplified by the funding rates of Bitcoin perpetual contracts, have yielded an annualized return of 15%-20% since the product's inception, a figure that far exceeds the 5% long-term return level of the global stock market and is higher than the long-term yields of various types of bonds. For high-risk investors, their expected returns are even higher than those of arbitrage investors.

Therefore, even tokenizing stocks may struggle to meet the current market's user structure and expected yield levels. In the short term, the risk-return positioning of many RWA products is rather awkward.

V. Regulation: Perhaps a Potential Opportunity

In early June this year, the U.S. SEC announced that it would classify several tokens, including BNB, BUSD, and MATIC, as securities, raising market concerns about regulation, which correspondingly led to noticeable declines in the relevant assets.

If the SEC's regulatory measures are recognized by other G20 or more countries, leading to more tokens being classified as securities and incorporated into traditional regulatory frameworks, future on-chain token issuance may also fall under regulatory oversight. From the current regulatory policies, we see similar trends: whether in the U.S., Japan, or EU countries, regulatory measures for stablecoins are increasingly aligning with traditional banking practices, suggesting that future regulations regarding tokens may also draw on securities regulatory measures to some extent.

If such a scenario occurs, some practitioners currently in traditional finance may feel more at ease bringing assets onto the blockchain: the benefit lies in that assets are local but can attract global liquidity. This idea has already been recognized by some RWA project entrepreneurs: although limited by geographical factors, blockchain allows them to access global investors. For these practitioners, asset tokenization under regulation would bring two benefits: 1. It provides access to global liquidity, meaning funding will not be affected by geographical factors, potentially allowing for cheaper capital; 2. It may help find investors with lower yield requirements than local ones, increasing the project's selection range.

Meanwhile, regulatory measures on the user side are also advancing: KYC. Crypto-native projects only require a wallet for access, but some startups raising funds in the primary market now require KYC assistance to determine whether users are qualified investors. Some projects introducing RWA, such as Maple Finance, also consider KYC an indispensable part of their customer acquisition process. If KYC processes gradually become implemented in more new projects, a blockchain industry with clearer regulations coexisting with KYC may bring an additional benefit: more ordinary investors can enter the market with greater confidence.

This type of user has a risk preference that favors familiar assets while also showing some interest in emerging crypto-native assets. At this point, RWA can serve as an important investment direction for these more ordinary investors.

VI. Possible Development Paths for RWA

In the short term, RWA offers three benefits to investors in the crypto industry:

- Low-risk investment targets denominated in fiat currency: Currently, the risk-free interest rates of major economies, led by the U.S., have reached levels above 3%, significantly higher than the borrowing yields in various USD-denominated lending protocols in the crypto market. Without the need to cycle leverage, this presents investors with extremely low-risk investment opportunities. Currently, projects like Ondo Finance, Maple Finance, and MakerDAO have launched investment projects based on U.S. Treasury bond yields, which are highly attractive to investors settling in fiat currency. In this track, we may see the emergence of a "money market fund" project in the crypto market.

Source: https://fred.stlouisfed.org/series/FEDFUNDS

Source: https://fred.stlouisfed.org/series/FEDFUNDS

- Risk diversification of assets: Taking Bitcoin as an example, in different market phases, its correlation with gold and U.S. stocks has shown varying degrees of volatility.

Even after 2020, during the macro factor-driven boom, different asset classes still exhibit a certain degree of diversification advantage.

Source: https://www.swanglobalinvestments.com/the-correlation-conundrum/

Source: https://www.swanglobalinvestments.com/the-correlation-conundrum/

For allocation-type investors, mixing crypto-native assets with various types of RWA can achieve greater asset risk diversification.

- A means for investors in developing countries to hedge against fluctuations in their local currency values: In some developing countries, such as Argentina and Turkey, where inflation is persistently high, RWA can assist investors in these regions in hedging against local currency fluctuations to achieve global asset allocation.

From these three dimensions, RWA that can be widely accepted in the medium to short term is more likely to be the high-yield, low-risk RWA based on government bonds from major economies due to interest rate hikes.

In the long term, as regulatory frameworks become clearer, more mainstream investors gradually enter the crypto market, and operations in the crypto industry become more convenient, RWA has the opportunity to replicate the boom seen in China's internet finance explosion a decade ago:

1. Blockchain-based RWA assets provide unprecedented "accessibility" for global mainstream investors: As assets that mainstream investors are most familiar with, RWA may become the primary on-chain investment target for non-Web3 natives. For them, the borderless nature of on-chain assets and permissionless access and operation open the door to investing in and utilizing a wider range of global assets. Conversely, for entrepreneurs in the field, this also offers unprecedented user breadth, scale, and extremely low customer acquisition costs. The rapid development and widespread use of USDT and USDC as "on-chain dollars" have already preliminarily validated this trend.

RWA assets may give rise to new DeFi business models: LSDs as a new type of underlying asset have stimulated the rapid development of LSD-Fi. In this context, not only have existing business paradigms such as asset management, spot trading, and stablecoins been re-emphasized, but there are also directions related to yield volatility that, while previously present, had not received attention. If RWA becomes an important type of underlying asset, the introduction of new and substantial off-chain yields may nurture new DeFi business models. In the future, RWA could also combine with crypto-native assets and strategies to form hybrid assets, allowing more users willing to explore crypto-native assets to understand them through more familiar means. From this perspective, the next high TVL RWA+DeFi project may be a "money market fund on-chain."

The industry's regulatory game will eventually yield answers, allowing practitioners to seek compliant customer acquisition methods: Whether in Western countries or in Eastern regions like Hong Kong, the gradual implementation of regulation is an inevitable trend. The crypto industry is expected to grow to a scale of $10 trillion, and regulation will not overlook it. As regulatory policies gradually clarify, we can see that some regions are able to implement previously unachievable business operations: in Hong Kong, stablecoins can now be issued through compliant channels, and in the Middle East, explorations are underway to combine the blockchain industry with traditional sectors.

In the long run, one of the crucial factors for the robust development of the crypto industry is ample liquidity. With the implementation of regulations, RWA, led by fiat-collateralized stablecoins, is bound to grow rapidly. Especially under the stimulus of the next round of global liquidity easing, if new entrants can receive strong support in terms of ecosystems and channels, compliant fiat-collateralized stablecoins may also replicate the explosive growth path of USDT.