"Non-custodial" "Retail investors", Five points to understand the new EDX compliance framework

How does EDX avoid the regulatory pitfalls encountered by Binance and Coinbase?

How does EDX avoid the regulatory pitfalls encountered by Binance and Coinbase?Author: Leo, LeftOfCenter, BlockBeats

On the morning of June 21, BTC surged dramatically, one of the key reasons being Wall Street's entry into crypto, as the U.S. is launching its own cryptocurrency trading platform, EDX Markets. In recent weeks, the SEC has frequently intervened, putting regulatory pressure on Binance and Coinbase, leading to various FUD in the industry and a crypto crash. Many believed that under the SEC's crackdown, crypto would become stagnant, but is that really the case? The SEC seems to have other intentions.

Just last night, a very "new" cryptocurrency trading platform, EDX Markets, announced its entry, attracting significant attention. Unlike previous crypto trading platforms, EDX is entirely backed by Wall Street forces, including Citadel Securities, Fidelity Investments, and Charles Schwab. As of the time of writing, the platform has already provided services to industry giants such as Charles Schwab, Citadel Securities, Fidelity Digital Assets, Paradigm, Sequoia Capital, and Virtu Financial. This cryptocurrency trading platform represents a "compliant" entry of traditional finance into the crypto space. So how does EDX achieve compliance?

1. Non-Custodial

Unlike mainstream cryptocurrency exchanges, EDX is a non-custodial exchange, meaning it does not directly handle customers' digital assets but merely provides a trading platform for institutional users to execute cryptocurrency and fiat transactions, settling externally.

Ram Ahluwalia, CEO of LumidaWealth (@ramahluwalia), believes that EDX may aim to develop into a regulated ATS and eventually become a "national securities exchange" (think Nasdaq or the New York Stock Exchange), which would benefit the crypto market. EDX is applying federal securities laws to cryptocurrencies by utilizing third-party banks and cryptocurrency custodians for asset custody, thereby minimizing conflicts of interest and preventing asset misuse, as seen in issues with FTX, Celsius, and DCG/Genesis.

The so-called non-custodial trading refers to the settlement process. Unlike mainstream crypto exchanges that "require customers to deposit crypto assets into wallets controlled by the exchange," EDX plans to have third-party banks and cryptocurrency custodians hold customer assets. Actual asset trading occurs directly between these third-party companies.

During the settlement phase, EDX Markets will act as an agent, calculating the settlement obligations between parties and notifying each member and authorized custodian of which counterparty a member has traded with and the transaction amount. Members will independently own their trading data to verify the settlement data conducted by EDX Markets. EDX Markets does not participate in the transfer of any fiat currency (cash) or tokens—this is solely done through authorized custodians. Similarly, EDX Markets does not engage in the flow of funds. Settlements will occur based on legal agreements between members and their authorized custodians, with no recourse to EDX Markets. In the event of a dispute, EDX Markets will recalculate, but any resolution of disputes will depend on the terms of the agreement between the member and their authorized custodian.

Additionally, EDX plans to launch its own clearinghouse later this year to streamline the settlement process.

2. Non-Security Tokens and Trading Rules

According to information provided on the EDX official website, the platform currently supports trading of only four tokens: BTC, ETH, LTC, and BCH, all of which are not classified as securities by the SEC. For EDX, this conservative selection of tradable tokens helps avoid conflicts with the SEC and is part of EDX's compliance framework. As definitions and interpretations of securities and crypto tokens evolve, EDX may add more crypto tokens in the future. Currently, only institutional trading is supported, and institutions must pass a "membership screening" to trade on EDX; retail investors cannot trade through this platform.

In terms of trading rules, some of EDX's rules differ from traditional crypto trading platforms. BlockBeats has summarized the trading rules currently disclosed by EDX as follows:

The trading platform is open 365 days a year, 24/7, unless otherwise notified, such as for maintenance or system upgrades, in which case platform users will be informed in advance;

The trading platform has the right to stop or suspend trading of any or all tokens on the platform to maintain market fairness, protect investor interests, or take other actions, such as canceling all unprocessed and open (unexecuted) order instructions or limiting orders to certain types (e.g., limit orders). The trading platform has the right to decide the duration of such "suspension, interruption, closure," etc., and will notify institutional members; the system will reject all orders regarding suspended trading tokens.

Regarding the rules for listing new tokens, they differ significantly from traditional crypto platforms, as follows:

If the trading platform lists a new token, it will suspend all orders related to the new token and then initiate a quoting period for that token, with the duration of the quoting period determined by the trading platform. During the quoting period, members can submit orders to the system, but these orders will not be executed;

After the quoting period ends, the trading platform will initiate a limit order trading period, during which the system will only accept limit orders. The trading platform will determine the duration of the limit order trading period. Token limit orders submitted during the market order period will be accepted, but regular token market orders will be rejected by the system;

After the limit order period ends, the trading platform will transition to the official trading period, at which point the system will open for trading, and all eligible orders will be accepted by the system.

The system should be accessible for members authorized to input and execute orders. All members screened by EDX Markets can use the system in a fair, transparent, equitable, and non-discriminatory manner.

It is evident that compared to other trading platforms, EDX is very cautious in token trading, with numerous processes in place to avoid falling into the "non-compliant" category.

3. No Direct Services for Retail Investors

With the precedents set by Coinbase and Binance, to avoid conflicts with regulators, EDX Markets does not directly provide services to individual investors. Instead, EDX will rely on retail brokers to provide order routing services, sending retail investors' buy and sell orders to the trading platform.

In simple terms, EDX Markets is a non-custodial trading platform that does not directly handle customers' digital assets or provide direct services to individual investors. It will offer API-based trading access rather than a traditional front-end user interface. Additionally, EDX Markets will not directly hold customer funds but will manage customer funds through third-party banks and professional custodians, with fund transfers not "passing through" EDX Markets but completed solely between the relevant service providers.

This is similar to the operation model of traditional stock markets, where investors do not directly enter the New York Stock Exchange or Nasdaq but submit orders through brokers like Fidelity and Charles Schwab.

4. Market Making Must Be Third-Party

Among the 13 charges brought by the U.S. Securities and Exchange Commission (SEC) against the world's largest cryptocurrency exchange, Binance, one of the charges is "conflict of interest," based on the fact that a trading company under Binance CEO Changpeng Zhao engaged in "artificially inflating trading volumes and manipulating trades."

In most traditional financial markets, exchanges generally match buyers and sellers at the most competitive transparent prices, with market-making typically operated by independent private companies, thus avoiding "conflicts of interest."

Although this internal market-making model has been a common practice in centralized exchanges, it clearly does not meet the SEC's ideal compliance conditions, which is one of the charges listed by the SEC in its frequent lawsuits against crypto exchanges.

According to SEC Chairman Gary Gensler, "These crypto trading platforms that claim to be exchanges are mixing multiple functions, whereas in traditional finance, we do not see the New York Stock Exchange operating hedge funds and market-making." In other words, he does not recognize the current model of crypto exchanges that combines trading, market-making, and custody.

The Financial Times cites reports from anonymous insiders stating that Crypto.com has always had its own market-making team and privately prohibited employees from disclosing the existence of internal market makers. Coincidentally, shortly after the SEC filed a lawsuit against Binance, Crypto.com shut down its institutional trading services for the U.S.

This time, the new compliant trading platform created by EDX Markets seems to aim to separate market-making from custody, existing purely as a trading platform. By introducing third-party banks and cryptocurrency custodians, EDX minimizes conflicts of interest and prevents asset misuse.

It is worth mentioning that among the consortium supporting EDX Markets, two firms (Citadel and Virtu) are themselves professional market makers on Wall Street, so we have reason to speculate that EDX Markets' future market-making services may be provided by these two leading Wall Street market makers.

5. Strong Support from Traditional Financial Institutions

Similarly, the supporters behind EDX are traditional financial giants from Wall Street, which is another point of significant attention for the platform. The supporters behind this institution include Charles Schwab, Citadel Securities, Fidelity Investments, Sequoia Capital, and Paradigm.

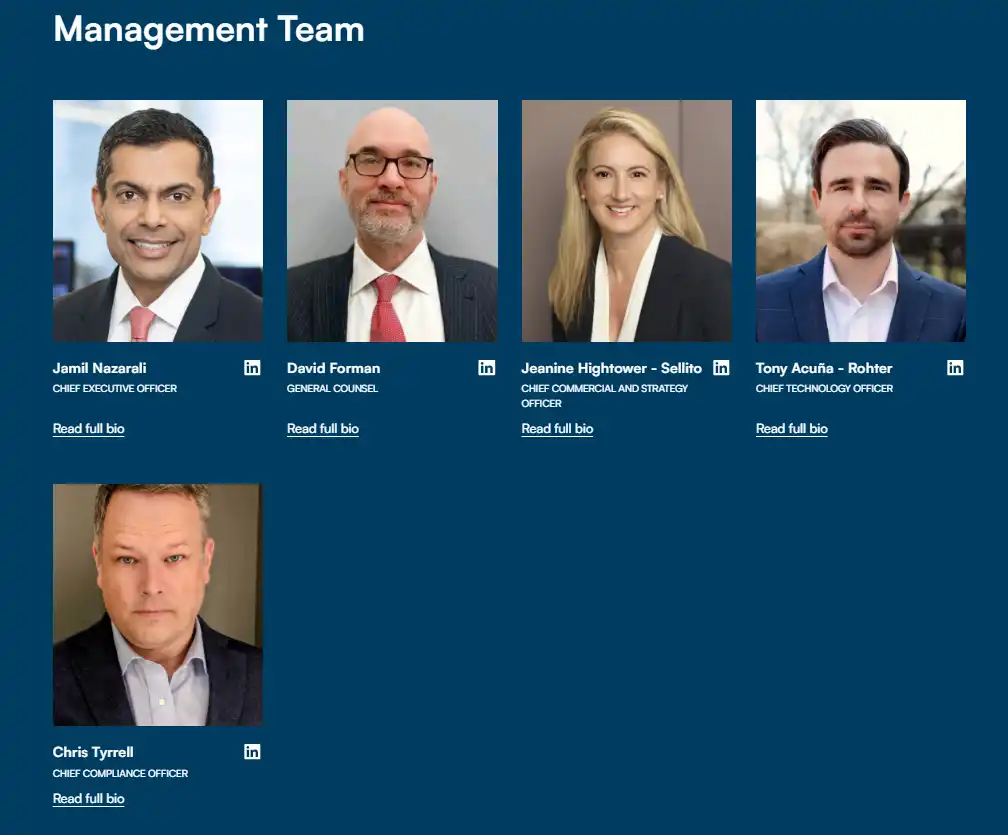

EDX Markets boasts a luxurious founding team, gathering former executives from major financial institutions. EDX Markets founder Jamil Nazarali, before joining EDX, served as the global head of business development at Citadel Securities for a long time. EDX Markets CTO Tony Acua-Rohter previously served as the technical director at ErisX. The chief legal counsel is David Forman, who previously held the position of chief legal officer at Fidelity Brokerage Services and general counsel at Fidelity Digital Assets.