LD Capital: An In-Depth Analysis of the Cryptocurrency Market's Response and Impact Facing SEC Crackdown

Being defined as securities may fundamentally change the way the cryptocurrency industry operates.

Being defined as securities may fundamentally change the way the cryptocurrency industry operates.Original Title: "Binance and Coinbase Face SEC Charges: Analyzing Market Reactions and Impacts"

Written by: @jinzejiang0x0, LD Capital

Abstract:

a. The U.S. Securities and Exchange Commission (SEC) has filed formal lawsuits against cryptocurrency exchanges Binance and Coinbase, triggering a massive market sell-off and a series of chain reactions, including the delisting of tokens involved in the definition of securities;

b. The charges against Binance are more severe, including fraud, cross-entity mixed assets, and trading against customers;

c. The market reacted sharply, with the average price of 18 tokens defined as "securities" by the SEC dropping by 28.8%, compared to a 7.4% drop in BTC during the same period. However, even after being sued by the SEC for the first time, BNB's market cap share slightly increased, indicating its price has relative resilience;

d. Among the tokens defined as securities by the SEC, public chains dominate, accounting for 13 out of 18, followed by entertainment and the metaverse with 4 out of 18, the latter experiencing larger declines;

e. The report predicts possible future scenarios for the SEC lawsuits, including potential legal impacts and market reactions, and discusses the progress of legislation in the crypto industry;

f. The report summarizes precedents in crypto cases, including illegal token issuance and unregistered investment management cases.

On June 5 and 6, the SEC accused 19 tokens of being securities in lawsuits against cryptocurrency exchanges Binance and Coinbase, leading to a sharp sell-off across the market.

1. SEC's Charges

The SEC accuses Coinbase of operating an unregistered securities exchange, broker, and clearing agency, as well as not registering its crypto asset staking services. However, the charges against Binance differ significantly; in addition to being accused of operating an unregistered securities exchange, broker, and clearing agency like Coinbase, the SEC also accuses it of engaging in more activities similar to FTX: deception, cross-entity mixed assets, and trading against customers, with no similar accusations made against Coinbase.

The SEC has issued a warning to the financial markets: most crypto digital assets are securities, a stance that may impose strict regulatory requirements on digital asset exchanges.

Since Gary Gensler was sworn in as SEC Chairman in 2021, the industry has been predicting stricter cryptocurrency regulations. Gensler mentioned during his tenure as a blockchain professor at MIT that many cryptocurrencies are likely securities, meaning they should be regulated by the SEC and fall under U.S. government jurisdiction.

The SEC has already taken enforcement actions against several industry companies and projects, such as Ripple Labs, LBRY, Kraken, and Bittrex. It now seems that before targeting the two largest exchanges, the SEC likely used smaller companies to "practice."

1.1. Chain Reaction

These lawsuits and their subsequent impacts have triggered a chain reaction within the industry. Binance.US announced the suspension of USD deposits and withdrawals in response to the SEC's actions. Binance stated that challenges imposed by the SEC on its banking partners led to disruptions in fiat deposit and withdrawal channels.

The well-known brokerage Robinhood decided to delist cryptocurrencies classified by the SEC as unregistered securities. After June 27, the platform will no longer support tokens such as Cardano (ADA), Polygon (MATIC), and Solana (SOL). It is reported that before the SEC took action, it held MATIC, SOL, and ADA worth $583 million.

Crypto.com announced the closure of its institutional exchange, citing insufficient demand due to the U.S. market landscape. This decision reflects the challenges faced by crypto companies as institutional investors, including pension funds, mutual funds, and university endowments, become cautious in a turbulent market environment and under regulatory scrutiny.

On June 16, Binance was under investigation by French authorities for allegedly providing illegal digital asset services and serious money laundering activities. On the same day, Binance also announced its exit from the Dutch market, stating that it would stop providing services to users residing in the Netherlands due to its inability to register there.

1.2. Market Changes

Table 1: Overview of tokens mentioned in the SEC lawsuit in June that may be securities and their price changes. Source: Coinmarketcap, Coingecko, TrendResearch

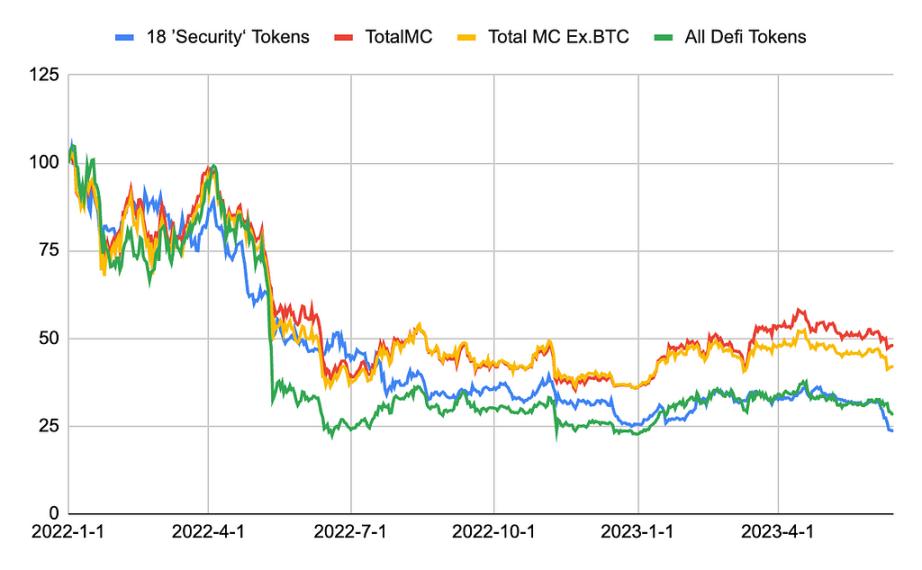

Figure 1: Comparison of the total market cap of 18 tokens defined as "securities" by the SEC with the total cryptocurrency market cap, Altcoins (total market cap excluding BTC), and total market cap of DeFi tokens since 2023. Source: Coinmarketcap, Coingecko, TrendResearch

Figure 2: Comparison of the total market cap of 18 tokens defined as "securities" by the SEC with the total cryptocurrency market cap, total market cap excluding BTC, and total market cap of DeFi tokens since 2022. Source: Coinmarketcap, Coingecko, TrendResearch

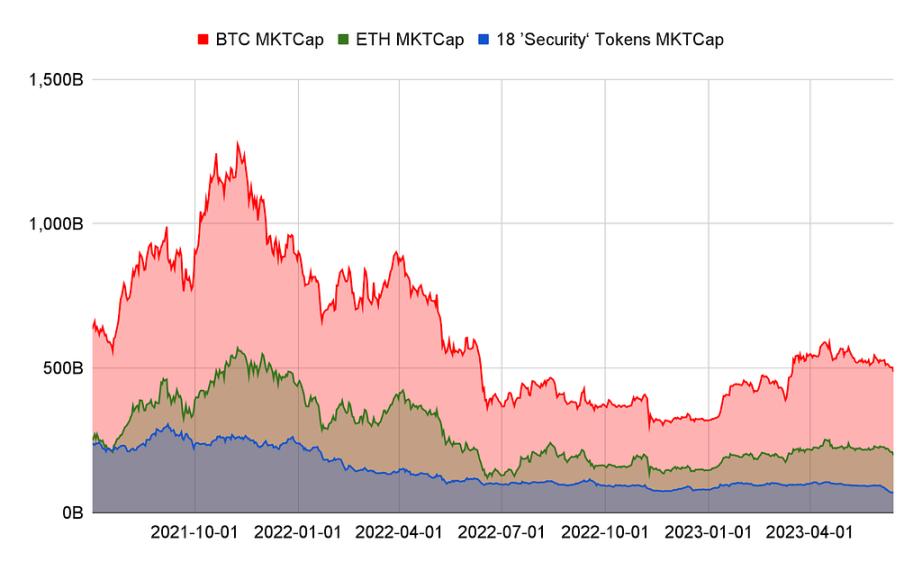

Figure 3: Comparison of the total market cap of 18 tokens defined as "securities" by the SEC with the market caps of BTC and ETH. Source: Coinmarketcap, Coingecko, TrendResearch

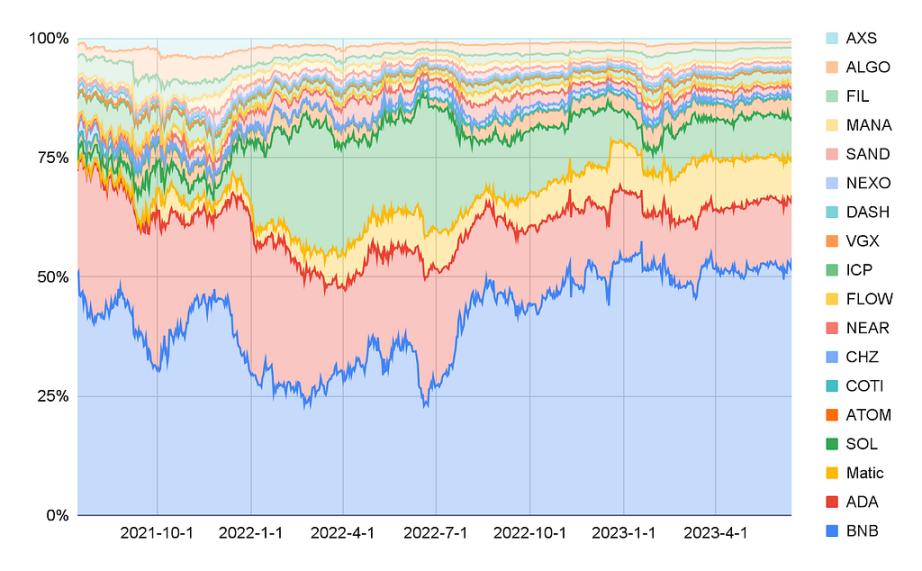

Figure 4: Comparison of the market cap changes of 18 tokens defined as "securities" by the SEC. Source: Coinmarketcap, Coingecko, TrendResearch

We have compiled the price changes of the crypto tokens mentioned by the SEC as securities over the past period, excluding BUSD. Among the 18 tokens named, we can see:

Table 1 shows that public chains dominate the industry with 13 out of 18, followed by entertainment and the metaverse with 4 out of 18, and asset management and lending with 2 out of 18;

Figure 4 shows that BNB has accounted for over 50% this year. Even after being sued by the SEC for the first time, its market cap share slightly increased, indicating its price has relative resilience; since early June, the average price has dropped by 28.8%, compared to a 7.4% drop in BTC during the same period, indicating a significant decline;

Figure 3 shows that the market cap peak for the 18 tokens occurred in September 2021, exceeding $300 billion, while the market cap low occurred this month after the SEC's regulatory actions, dropping to only $70 billion;

Since early June, the top three tokens with the largest declines are FLOW (-37.1%), SAND (-37.4%), and CHZ (-35.0%), indicating that entertainment-related tokens have experienced larger declines;

Since early June, the tokens with the smallest declines are NEXO (-8.4%), ATOM (-21.1%), and BNB (-22.2%). NEXO has experienced the least impact because it settled with the SEC earlier this year by paying fines, while BNB is the largest token by market cap among those charged (close to $50 billion before the drop), showing relatively low volatility, but ATOM's market cap is only over $3 billion, and its limited decline indicates its resilience;

Since their respective historical price peaks, these tokens have averaged a 91% decline, with the smallest declines being BNB (-58.4%), MATIC (-78.6%), and ATOM (-81.0%). BNB and ATOM are also among the tokens with lower declines since early June, indicating continuity in their price resilience;

Since their respective historical price peaks, the largest declines are ICP (-99.5%), FLOW (-99%), and FIL (-98.5%), with ICP only down 5.6% this year and FIL still up 14.6%, indicating that after significant adjustments, the price decline momentum has slowed;

Figure 1 shows that before the regulatory events in June, the performance of the 18 tokens in 2023 lagged behind the broader market, and after the regulatory events, the lag widened, with all gains for the year being reversed;

Figure 2 shows that extending the timeline to early 2022, the performance of the 18 tokens still lagged behind the broader market, but performed better than DeFi tokens for most of 2022.

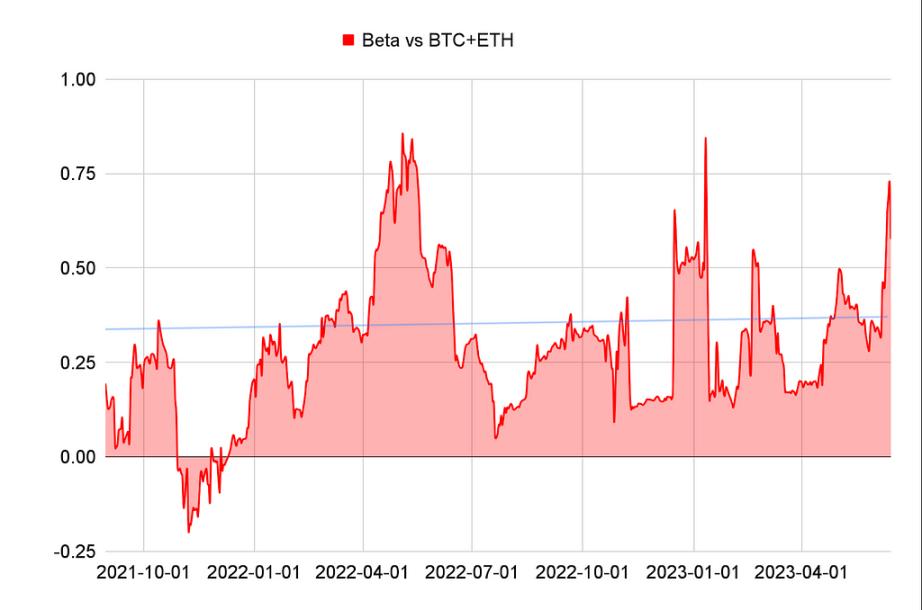

Figure 5: 30-day rolling beta values of the 18 tokens defined as "securities" by the SEC compared to BTC+ETH. Source: Coinmarketcap, Coingecko, TrendResearch

Figure 6: 30-day rolling correlation of the 18 tokens defined as "securities" by the SEC compared to BTC+ETH. Source: Coinmarketcap, Coingecko, TrendResearch

Beta represents the systematic risk or market risk of security tokens relative to a benchmark index. If beta is greater than 1, the price volatility of the security token may exceed that of the benchmark index; if beta is less than 1, the price volatility of the security token may be lower than that of the benchmark index.

From the rolling beta values, the market cap volatility of this "security" token portfolio is actually lower than the blue-chip volatility based on BTC and ETH. This result is not surprising, mainly considering that under a diversified allocation, the rise and fall cycles of each token due to project factors do not completely overlap, which also lowers the overall portfolio's beta relative to the benchmark index.

From the data, we can see that beta values and correlations have changed significantly at different points in time, which may relate to market conditions, the fundamentals of the tokens, or macroeconomic factors. When beta values are high, it indicates that the price movements of security tokens are more influenced by the market; when industry sentiment is extremely optimistic or pessimistic, both correlation and beta tend to rise, which means the benefits of diversified allocation diminish.

Overall, if invested based on market cap weighting, such a portfolio has underperformed BTC and ETH over the past two years, indicating that the price resilience of altcoins in a bear market is not as strong as that of BTC and ETH.

2. What is a Security?

According to U.S. regulations, whether something is a security primarily depends on whether it resembles shares issued by a company to raise funds. The SEC currently mainly applies the Howey Test established by the Supreme Court in 1946. Under this framework, when investors put in money with the intention of profiting from the efforts of the organization's leaders, the asset may fall under the SEC's jurisdiction.

2.1. What are the Implications of Being Defined as a Security?

Labeling tokens as securities makes operating a cryptocurrency trading platform more expensive and complex. According to U.S. rules, this label imposes strict investor protection requirements on platforms and issuers. This means exchanges will face ongoing scrutiny from regulators, which may lead to penalties, and in the worst-case scenario, if criminal authorities get involved, it could lead to criminal charges.

If a large number of cryptocurrencies are classified as securities, it will fundamentally change the way the cryptocurrency industry operates. First, compliance with securities laws becomes crucial, requiring these altcoins and their issuers to adhere to strict regulatory requirements. This includes registering with the SEC, providing necessary disclosures, and complying with reporting obligations.

Additionally, classification may lead to potential trading restrictions. If most altcoins are viewed as securities, they can only be traded on registered securities exchanges subject to specific rules and regulations. This may limit retail investors' liquidity and accessibility to these assets and introduce additional barriers to market participation.

For POS public chains like Polygon or Binance Smart Chain, being labeled as securities raises many issues, such as financial accounting for users paying transaction fees, KYC for validators, taxation, and whether any DeFi applications on-chain are legally authorized. These labels could be more damaging to the industry's long-term health than the closure or exit of a few exchanges from the U.S. market.

2.2. Future Scenarios of SEC Lawsuits

The lawsuits against Binance and Coinbase reflect the increasingly tense relationship between the government and the cryptocurrency industry. SEC Chairman Gary Gensler has made it clear that there is no need for more digital currencies, emphasizing that the U.S. already has a digital currency called the dollar. U.S. Treasury Secretary Janet Yellen has also expressed support for the SEC's actions, advocating for the use of regulatory tools to protect consumers and investors. This reflects that regulators are sending a clearer stance against cryptocurrencies or the foundational principles of the traditional financial system.

In the future, we may see the following four developments:

a. Expansion of regulatory enforcement, targeting more blockchain projects, especially large-cap public chains with direct lawsuits. Recently, the SEC has mainly initiated lawsuits against exchanges, and among the 19 tokens mentioned in related documents, the SEC has not yet directly issued warnings or lawsuits against any except BUSD and NEXO, which may indicate that more enforcement actions could be forthcoming.

b. Transition from civil to criminal charges. Since the SEC and CFTC do not have the authority to initiate criminal charges, related accusations may not have arrived yet. Criminal charges against cryptocurrency exchanges or projects typically involve fraud, money laundering, or other illegal activities. Such cases are usually handled by law enforcement agencies like the FBI or the U.S. Department of Justice. For example, last year, the DoJ announced criminal charges against six defendants in four cryptocurrency issuance cases, alleging involvement in cryptocurrency-related fraud.

For instance, Sam Bankman-Fried (SBF) faces 12 criminal charges in connection with the FTX and Alameda cases, including conspiracy to commit bank fraud and conspiracy to operate an unlicensed money transfer business, as well as wire fraud against FTX customers, securities fraud against FTX investors, and conspiracy to make illegal political donations and defraud the Federal Election Commission.

c. The authority of the SEC or Gensler may be stripped. Many U.S. politicians do not endorse the SEC's tough regulations.

For example:

U.S. Senator Bill Hagerty tweeted, "The SEC is using their role to eliminate an industry. Allowing one company (Coinbase) to go public and then obstructing their registration as a compliant exchange."

U.S. Senator Cynthia Lummis also tweeted, "The SEC has failed to provide a path for digital asset exchanges to register, and even worse, has failed to provide adequate legal guidance to distinguish between what is a security and what is a commodity."

On June 16, two Republican House members, Warren Davidson and Tom Emmer, introduced a bill called the "SEC Stabilization Act," aimed at restructuring the SEC and removing current Chairman Gary Gensler. This bill proposes increasing the number of SEC commissioners and adding directors to oversee the commission, to prevent regulatory policies from being influenced by the personal views of the SEC chairman or political struggles.

d. Legal tug-of-war or quick rectification fines. The sued teams and individuals actively respond, and legal battles may last for years, for example, the lawsuit between Ripple and the SEC has been ongoing since December 2020 without a final decision. Of course, if the sued teams and individuals quickly compromise, rectify their businesses, and accept fines, cases may settle quickly, as was the case earlier this year when Kraken and the SEC reached a settlement in less than a month.

3. Progress of Legislation in the Crypto Industry

Congress may pass a regulatory framework for cryptocurrencies, providing clearer rules for the operation of cryptocurrencies and their related businesses in the U.S. This clarity could stimulate further development and innovation in the industry. A legislative draft initiated by Representatives Patrick McHenry and Glenn Thompson in the House Financial Services Committee is considered the most viable legislation. This legislation attempts to clarify the jurisdiction of various agencies over certain digital assets and "strike an appropriate balance" between protecting consumers and encouraging responsible innovation.

This 162-page draft was published in early June, suggesting that digital assets initially classified as securities could ultimately be regulated as commodities. Whether an asset is classified as a security or a commodity largely depends on the degree of decentralization of the underlying blockchain network.

The draft suggests that if a network meets certain requirements, it will be considered decentralized, and tokens meeting commodity conditions will be regulated by the Commodity Futures Trading Commission (CFTC).

Specific determinations include that no one has unilateral authority to "control or materially change" the network's functions or operations in the past 12 months, and no token issuer or affiliate holds more than 20% of the token supply.

However, this draft legislation is expected to face significant opposition from Congressional Democrats. SEC Chairman Gary Gensler and some Democrats believe that most digital assets should be classified as securities, and that existing regulations are sufficient.

It is unclear when this bill might enter the Congressional voting agenda, but it represents an important step in the ongoing discussion about digital asset regulation.

3.1. Precedents in Crypto Cases

Ripple (XRP): In 2020, the SEC filed a lawsuit against Ripple Labs Inc. and its two executives, accusing them of conducting an unregistered securities offering worth $1.3 billion through a digital asset called XRP. The SEC's claim is that although Ripple positions XRP as a cryptocurrency, its issuance process is closer to that of a traditional securities offering, and therefore should be regulated under securities law. This is the largest lawsuit related to cryptocurrency that the SEC has filed to date. As of my last knowledge update (September 2021), this case is still ongoing without a final decision.

Block.one (EOS): In 2019, the SEC announced a settlement with Block.one, which agreed to pay a $24 million fine to resolve SEC allegations that its initial coin offering (ICO) of EOS between 2017 and 2018 violated securities laws. This is an important case as it demonstrates that the SEC may impose substantial fines for ICOs that violate securities laws.

Telegram (Grams): In 2020, the SEC successfully blocked the issuance of Telegram's Grams token. The SEC's argument in this case was that Grams tokens were unregistered securities, and therefore their issuance violated securities laws. Ultimately, Telegram agreed to pay a fine and refund investors.

Kik (Kin): In 2020, the SEC successfully sued Kik Interactive Inc., which conducted an unregistered securities offering through a digital asset called Kin. Kik ultimately agreed to pay a $5 million fine to resolve the SEC's allegations.

BlockFi: The SEC believes that investors lending crypto assets to BlockFi in exchange for the company's promise of variable monthly interest payments fall under securities law; additionally, the SEC claims that BlockFi issued securities and that over 40% of its total assets (excluding cash) are investment securities, and that it violated the registration provisions of the Investment Company Act of 1940 by not registering as an investment company. Ultimately, BlockFi will pay a $50 million fine directly to the SEC and another $50 million in fines to 32 states in the U.S. to settle similar allegations. This settlement represents the largest recorded fine imposed on a crypto company at that time.

NEXO: The SEC accused Nexo Capital of issuing and selling unregistered retail crypto asset lending products called Earn Interest Product (EIP). On January 20, 2023, crypto lending platform Nexo reached a settlement with the SEC and state regulators, agreeing to pay a total of $45 million in fines and cease offering lending products. The SEC agreed to settle with Nexo considering the company's prompt remedial actions and cooperation with commission staff.

Kraken: In February 2023, the SEC filed securities violation charges against cryptocurrency exchange Kraken due to concerns over the transparency of its staking token interest services. That month, the SEC reached a $30 million settlement with Kraken, which will discontinue its "crypto staking" program that offered investment returns.

3.2. Crypto Interest Business

U.S. regulation is not only aimed at the issuance and trading of securities tokens but also involves financial management businesses, such as BlockFi and NEXO mentioned above.

If a company provides a platform for users to store funds and pays a certain interest, this business model is closer to the deposit business of banks or financial institutions. In this case, the company needs to register and obtain licensing as a bank or financial institution according to the laws and regulations of its location.

In the U.S., such companies may need to obtain licenses from the Federal Reserve System, the Federal Deposit Insurance Corporation (FDIC), the Office of the Comptroller of the Currency (OCC), or state banking regulators. These agencies are responsible for overseeing banks and financial institutions to ensure their operations comply with laws and regulations.

In other countries and regions, companies may need to obtain licenses from the corresponding banking and financial services regulatory agencies. For example, in Europe, this may include the European Central Bank and national banking regulatory agencies.

It is important to note that such licensing typically requires meeting a series of requirements, including capital requirements, risk management requirements, corporate governance requirements, etc. Additionally, companies must comply with anti-money laundering (AML) and know your customer (KYC) regulations.

4. Is Regulation Outdated?

Supporters of more regulation argue that the designation of securities will provide investors with more information and transparency due to applicable SEC disclosure requirements. However, cryptocurrency advocates argue that their projects are decentralized to some extent, making old rules unsuitable. Crypto trading platforms believe that the assets they list should be viewed as commodities rather than securities. In the U.S., the rules governing the trading of commodities and their derivatives focus more on ensuring that companies, producers, and farmers can effectively hedge against the risks of commodity price fluctuations.

Despite increased scrutiny from regulators, the crypto industry still hopes that Congress will ultimately pass new laws to legitimize the industry. Last year, both Democrats and Republicans proposed several bills that would bring cryptocurrencies under the jurisdiction of the Commodity Futures Trading Commission and make other products, including stablecoins, more legitimate by regulating the assets they can hold.

Due to the unique properties of crypto assets, which can encompass multiple sources of value beyond traditional securities, regulating them solely under a ninety-year-old securities regulatory framework may be outdated.

Table 2: Classification of Sources of Value for Crypto Digital Assets. Source: TrendResearch

Table 3: Crypto Assets Defined as Securities by the SEC in Various Lawsuits Before June Lawsuit Documents. Source: SEC, TrendResearch

Reference:

https://beincrypto.com/full-list-cryptos-securities-sec-lawsuit-binance-coinbase/ https://www.bloomberg.com/news/articles/2023-06-13/these-are-the-19-cryptocurrencies-are-securities-the-sec-says

https://mp.weixin.qq.com/s/DSytFWfcnlA2FdWhTQt2IQ

https://www.sec.gov/files/litigation/complaints/2023/comp-pr2023-101.pdf

https://www.sec.gov/litigation/complaints/2023/comp-pr2023-102.pdf

Risk warning

Risk warning Risk warning

Risk warning