The Contest of Securities Regulatory Power: How Do the Regulatory Paths of the U.S. SEC and Hong Kong SFC Differ?

For the U.S. SEC, forfeiture revenue has become a form of "pillar income."

For the U.S. SEC, forfeiture revenue has become a form of "pillar income."Author: 0xLoki

Previously, Space discussed a topic: Will the Hong Kong SFC go crazy like the US SEC in defining securities and then regulating, investigating, and imposing fines? The key to this question is that we cannot only look at what they say (organizational goals), but also at what they do (actual behavior). A simple way to answer this question is to understand the business and personnel composition of the SEC and SFC.

US Securities and Exchange Commission (SEC)

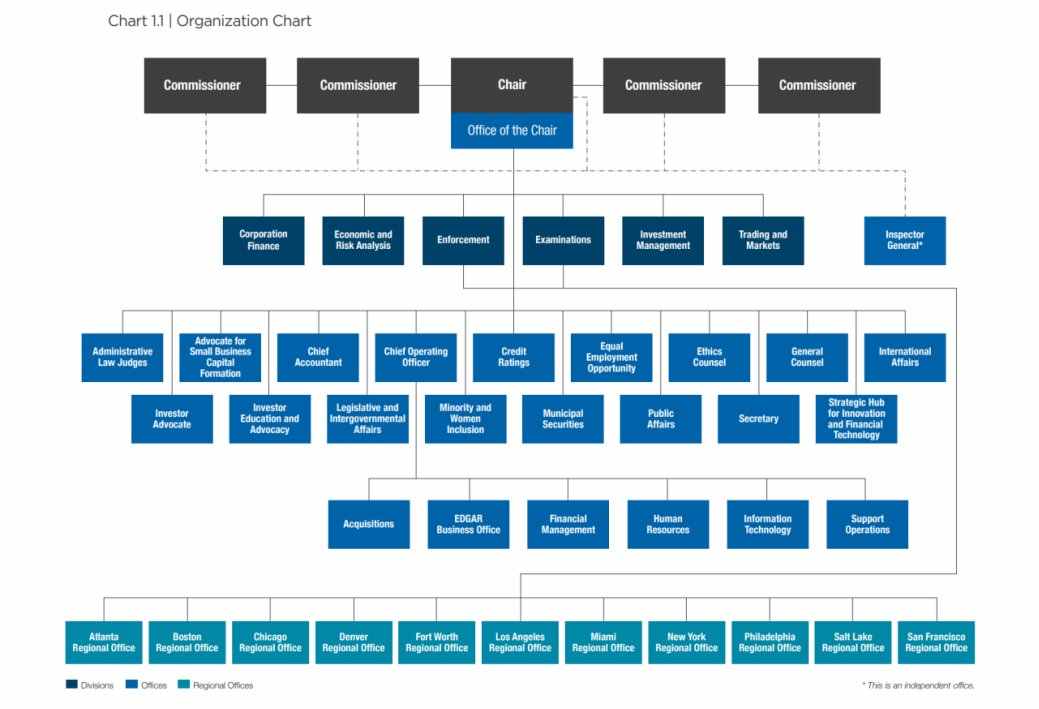

First, let's take a look at the structure of the SEC. At the top is a commission consisting of the chairman and four commissioners, with six divisions, one office of the inspector general, and eleven offices underneath. In addition, there are eleven regional offices. It is important to note that these eleven regional offices report to both the Division of Enforcement and the Division of Examinations.

From the organizational structure, we can see that the Division of Enforcement and the Division of Examinations seem to be the most important among all divisions. In the descriptions of the various departments that follow, we can also see that the Division of Enforcement and the Division of Examinations are listed first and second.

Additionally, there is a more convincing piece of data: financial situation. The SEC's funding comes from three main sources:

1) Federal budget;

2) Securities transaction fees and application fees;

3) Forfeiture income.

Among the forfeiture income, it is further divided into two parts:

A. For amounts that need to be compensated to victims, the forfeiture income will compensate victims and be injected into the General Fund of the US Treasury.

B. For amounts that do not need to be compensated to victims, the forfeiture income will be allocated to the Investor Protection Fund, whistleblowers (providers of investigative leads), and funding investigations by the office of the inspector general.

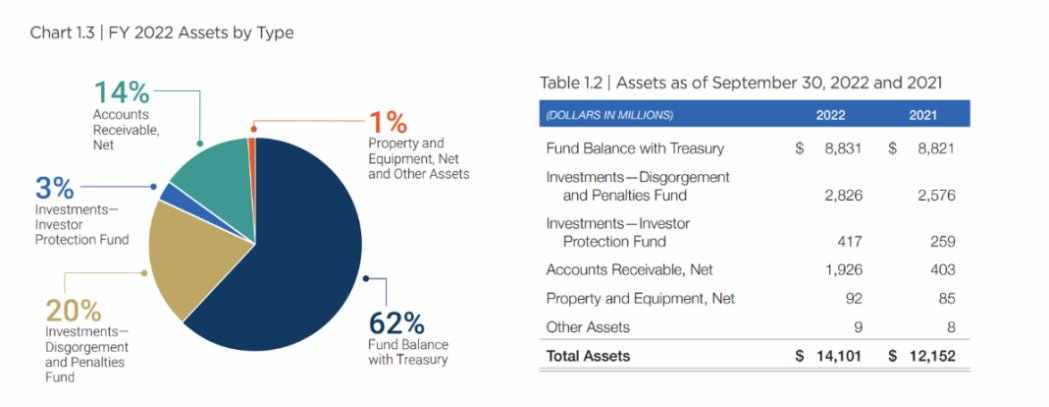

Next, let's look at the SEC's balance sheet. According to the fiscal year 2022 annual report, the SEC's total assets grew from $12.2 billion to $14.1 billion, an increase of $1.9 billion. Among these, investment items increased by $400 million; accounts receivable increased by $1.5 billion, with the vast majority of these two items being composed of forfeiture income, and the investment items have already deducted expenses incurred during the regulatory process.

In addition to forfeiture income, the OMB allocated a reserve budget of $50 million to the SEC for 2022, with an investor protection fund budget of $390 million; SEC transaction fees were about $1.8 billion; application fees were $640 million. It can be seen that forfeiture income has become a form of "pillar income."

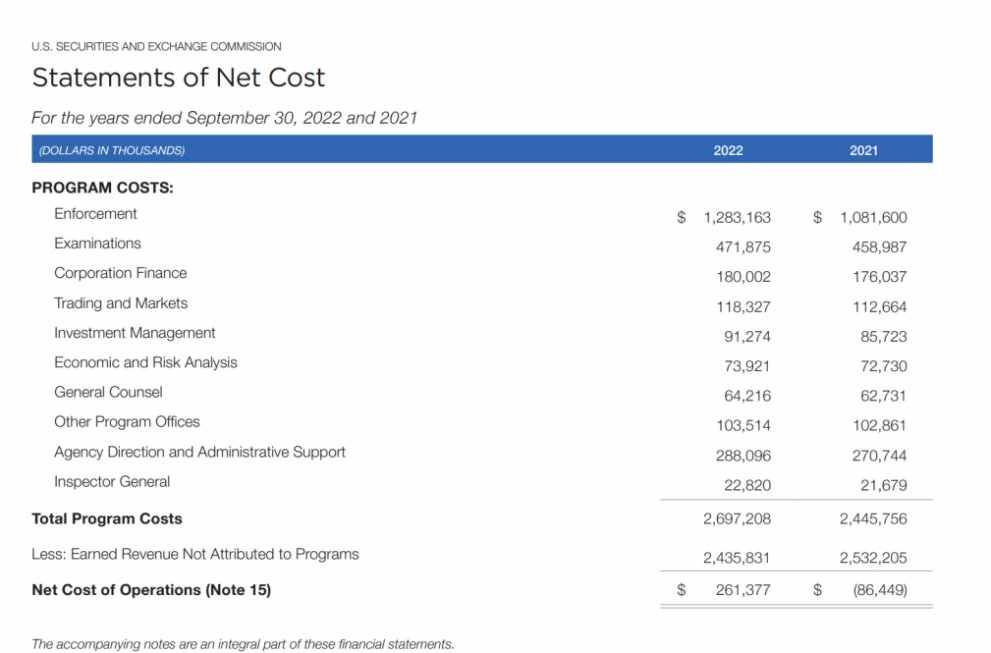

Looking at expenditures, we can see that the net expenditure of the Division of Enforcement and the Division of Examinations is the highest, totaling $1.75 billion, accounting for 65% of total expenditures. These expenditures ultimately translate into enforcement actions: according to another public article from the SEC, the SEC initiated a total of 760 enforcement actions in fiscal year 2022, an increase of 9% from the previous year. This includes 462 new or "independent" enforcement actions.

These enforcement actions brought in substantial income: the total amount ordered to be paid was $6.439 billion, including civil penalties, forfeited gains, and pre-judgment interest, marking the highest record in SEC history, surpassing the $3.852 billion from fiscal year 2021. Among the total amount ordered, civil penalties amounted to $419.4 million, also a historical high.

Under this system, the SEC provides generous rewards for whistleblowers. In fiscal year 2022, the SEC awarded approximately $229 million across 103 awards, ranking second in both amount and number of awards in history. Meanwhile, the number of whistleblower reports in fiscal year 2022 also reached a historical high, with the SEC receiving a total of 12,300 reports. Gensler's request during the hearing for the SEC to obtain resources to increase its staff from 4,685 to 5,139 also became quite reasonable.

In summary, the SEC's behavioral path is not difficult to understand; it is a form of post-event enforcement. First, let as many people as possible come in and act, then investigate, collect evidence, prosecute, and impose penalties as much as possible. Therefore, it is not difficult to understand the SEC's statement that "everything is a security except for BTC"; expanding enforcement targets is the first step. Of course, whether to choose enforcement in the end and whether the prosecution is established also depends on many factors.

Hong Kong Securities and Futures Commission (SFC)

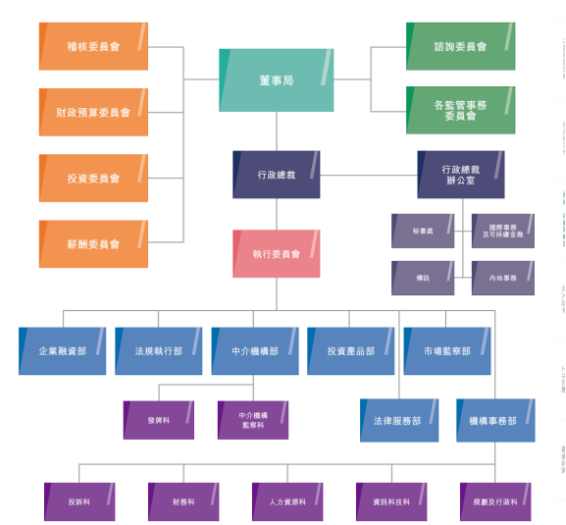

After discussing the SEC, let's look at the SFC. The structure of the SFC is significantly different from that of the SEC, with only the Market Surveillance Division and the Intermediaries Supervision Division under the Intermediaries Division potentially involved in regulation. Additionally, the Intermediaries Division has a Licensing Division, which is closely related to the familiar licensing system.

According to the SFC's 2021-2022 annual work summary, the SFC conducted a total of 220 case investigations and initiated 168 civil lawsuits, imposing fines totaling HKD 410.1 million on licensed institutions and individuals. In addition to enforcement, another important figure is that the SFC received 7,163 license applications during the year and processed over 38,000 license document reviews through WING.

In specific enforcement categories, although the SFC mentioned that "in appropriate circumstances, we will decisively take enforcement action against unlicensed platform operators," the enforcement cases still mainly focus on traditional financial violations such as insider trading, market manipulation, corporate fraud and misconduct, intermediary negligence, and inadequate internal controls.

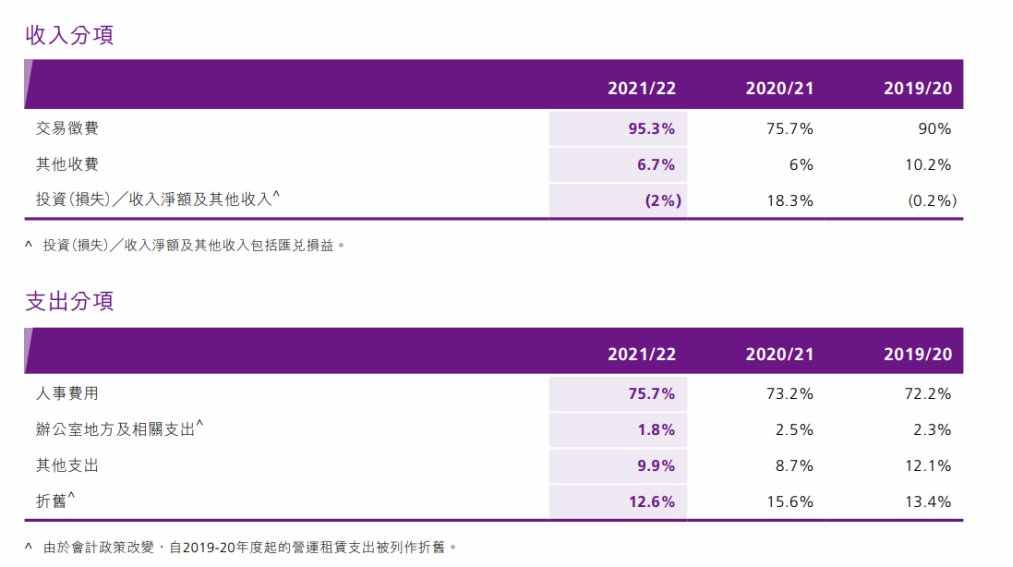

In terms of income and expenditure, the SFC's composition is very simple. For the 2021-2022 fiscal year, the SFC's total income was HKD 2.247 billion, of which transaction levies accounted for 95.3%, and other income was 6.7% (mainly collected from market participants). Forfeiture income did not appear in the SFC's income share. Among expenditures, 75.7% were personnel costs. According to the annual report data, as of 2022, the SFC had a total of 913 employees.

Furthermore, based on this data, the notion that the SFC makes money from "licensing" is not accurate; market trading contributes the vast majority of income to the SFC. According to the application fees/annual fees for licensed entities, which range from HKD 47,000 to HKD 129,700 per activity, and for licensed representatives, which range from HKD 1,790 to HKD 5,370 per activity, the 323 licensed institutions and over 40,000 licensed personnel do not contribute much income.

From past data, it can be seen that the SFC does not have the same motivation as the SEC. On the other hand, the SFC also lacks the enforcement capability of the SEC; the SFC has only 903 employees, who also need to handle the complex business of the stock exchange and futures exchange, process a large number of license applications, maintain and inspect, and even promote goodwill and make the world a better place, making it difficult to allocate so many human and material resources for proactive enforcement.

From the above data, it can be seen that the SFC does not have the same policy inclination as the SEC, and both the SFC and SEC essentially operate under the principle of "same business, same principles, same risks"; the SEC has a very strong regulatory inclination towards cryptocurrencies, but it also has the same inclination towards other financial institutions; and the SFC is unlikely to treat cryptocurrencies specially.

In summary, I believe the likelihood of the SFC engaging in large-scale enforcement like the SEC is very low. For entrepreneurs, as long as they do not clearly violate current Hong Kong laws and regulations, there is no need to worry about regulatory pressure. However, I do not believe that the "Hong Kong market" and "proactive licensing" are suitable for every project, as applying for and maintaining a license also requires considerable costs. Even without a license, many other Web3-related activities can still be conducted in Hong Kong.

Although there is no need to worry about regulatory pressure like that from the SEC, I still want to say here that every eager participant should calmly ask themselves one question—do we really need a "license"?