LD Capital: A Perspective on Crypto Asset Management with Enhanced Return Strategies for US Stock Indices

The enhanced index fund can help investors with different risk preferences achieve corresponding risk exposure and excess returns through these yield-enhancing methods, including multi-factor quantitative stock selection models, subjective timing models, sector rotation models, or equity index futures derivative yield enhancement models.

The enhanced index fund can help investors with different risk preferences achieve corresponding risk exposure and excess returns through these yield-enhancing methods, including multi-factor quantitative stock selection models, subjective timing models, sector rotation models, or equity index futures derivative yield enhancement models.Author: LD Capital Research

Introduction

In recent years, traditional financial markets have seen rapid development of index products represented by ETFs, showing characteristics where Smart Beta ETFs and actively managed ETFs have higher capital inflow growth rates than ordinary index ETFs. The asset management industry is gradually shifting its focus from ordinary index products to more innovative index product series, such as ESG ETFs, actively managed ETFs, and thematic ETFs. Among them, actively managed ETFs in the equity market have made new breakthroughs, attracting off-exchange products to actively transform, becoming a hot topic in the development of active products in recent years.

Global index providers continuously innovate and improve index systems to meet new market demands, driving the industry towards refined and diversified deep development, while promoting continuous innovation in index products. Compared to traditional financial markets, crypto index-enhanced products are still in a very early stage. As the overall market capitalization of cryptocurrencies grows, the market for structured index-enhanced products should also increase rapidly.

We believe that the market size and current status of index funds and index-enhanced funds/ETFs in the US stock market provide valuable references for the development path of index-enhanced funds in the crypto market. We also believe that crypto index-enhanced funds can achieve excess returns that meet the needs of different risk-tolerant investors through these return-enhancing methods, whether through multi-factor quantitative stock selection models, subjective timing models, sector rotation models, or stock index futures derivative return enhancement models.

Scale and Development Trends of Ordinary Index ETFs and Index Enhanced Funds/ETFs in Hong Kong and US Stocks

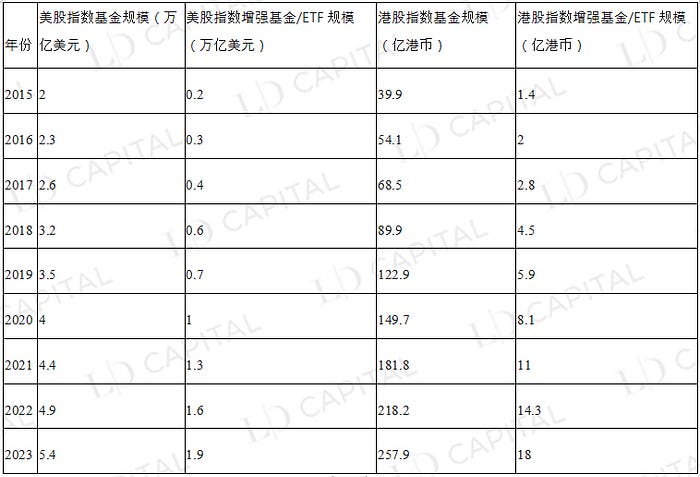

From 2015 to 2023, the scale of index funds and index-enhanced funds/ETFs in both the US and Hong Kong stock markets has shown steady growth, with the scale of index-enhanced funds/ETFs, i.e., actively managed ETFs, growing even faster, increasing tenfold over eight years, and reaching nearly one-third of ordinary index funds by 2023.

Table 1 Comparison of Total Scale of Ordinary Index Funds and Index Enhanced Funds/ETFs in US and Hong Kong Stocks from 2015 to 2023

Source: VettaFi, Statista

Source: VettaFi, Statista

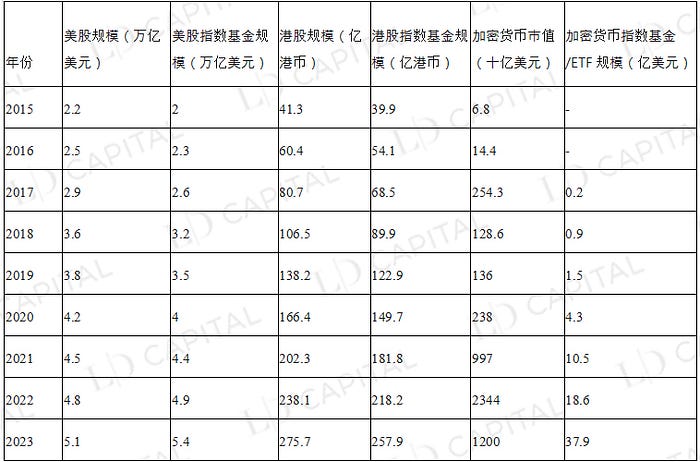

In the traditional financial market, the scale of index funds in the US and Hong Kong even shows a trend of exceeding their corresponding market capitalization, while the scale of index funds/ETFs in the crypto market is far from reaching its market capitalization. As traditional investors' interest in crypto asset management products continues to rise, the development prospects for cryptocurrency index funds and exchange-traded funds (ETFs) are broad.

Table 2 Comparison of US Stocks, Hong Kong Stocks, Crypto Market Capitalization, and Corresponding Index Funds/ETFs Scale

Source: VettaFi, Statista

Source: VettaFi, Statista

Active Management Characteristics of Index Enhanced Funds

Index funds can achieve returns (β returns) by tracking the characteristics of an index, such as tracking error, market capitalization style, valuation style, industry weight distribution, and individual stock weight distribution.

In contrast, enhanced index funds strive to achieve additional returns (α returns) that exceed the market through active management by fund managers, thereby experiencing smaller declines than the benchmark index during market downturns and obtaining more returns compared to the tracked index during market upswings, aiming for relatively stable compound performance over the long term.

Regarding the tracked index, the range of indices that enhanced index funds can track is quite broad, including both broad-based indices and single-industry indices or other thematic indices. From the current market environment of US and Hong Kong stocks, broad-based indices such as S&P 500, Nasdaq-100, Russell 2000, DJIA, HSI, and HSCEI are mainstream choices for enhanced index funds on the β side.

Ways to Enhance Index Fund Returns

With continuous innovation in the financial market, index-enhanced funds can achieve excess returns through various methods, thus achieving the effect of "enhanced" returns. The "enhanced" portion of returns in index-enhanced funds can be realized through methods such as multi-factor quantitative stock selection models, subjective timing models, sector rotation models, and stock index futures derivative return enhancement models, which are currently common avenues for enhancing returns in index-enhanced products.

Quantitative Multi-Factor Enhancement Strategy Products

The goal of a quantitative multi-factor enhancement strategy is to select stocks by simultaneously using multiple factors to achieve better returns. These factors can be categorized into various dimensions, such as technical factors (market momentum and technical indicators), macro factors, statistical data mining (machine learning, deep learning), and fundamental factors, including company financial stability, dividend yield, and valuation.

Table 3 Common Multi-Factor Stock Selection Enhanced Index Funds in US Stocks

Taking the Invesco S&P 500 High Dividend Low Volatility ETF (SPHD) as an example. SPHD tracks the S&P 500 High Dividend Low Volatility Index and employs a multi-factor stock selection strategy, focusing on high dividend yield and low volatility stocks. It selects the 50 securities with the highest dividend yields and lowest volatility from the S&P 500 index.

The constituent stocks are weighted by dividend yield, with a maximum weight of 3% for individual stocks to ensure diversification. To maintain its low volatility target, the fund rebalances every six months, reassessing stock selection based on updated dividend yield and volatility indicators. Due to its low volatility, this ETF typically outperforms the broader S&P 500 index during bear markets but may lag in strong bull markets.

The return enhancement portion of SPHD comes from its overweighting of high dividend and low volatility stocks. However, SPHD has significantly underperformed the benchmark S&P 500 in the recent interest rate hike environment, mainly due to high dividend sectors such as finance, energy, aviation, and tourism being adversely affected during the pandemic, leading to poor performance of high dividend stocks in these sectors.

Particularly, the financial sector, which accounts for 26% of SPHD's portfolio, has been severely impacted by the recent banking crisis. The underperformance relative to the benchmark has led to a significant decline in its AUM.

Strictly speaking, SPHD and QUAL are considered passive management funds that partially employ enhancement methods. These enhancement methods aim to optimize specific factors of the portfolio, but the overall investment strategy of the fund still primarily focuses on tracking a specific index. In contrast, QARP not only uses passive management methods to track the index but also employs some enhancement methods and active management strategies to select the constituent stocks of the portfolio, making it a typical active management fund.

When implementing a quantitative multi-factor enhancement strategy, it is essential to consider the weights of different factors and the number of holdings in the portfolio. Depending on the actual situation, different factor weights and holding numbers can be used to achieve various investment objectives. For example, using more financial stability and profitability stability factors to invest in defensive stocks or using more market momentum and technical indicator factors to invest in growth stocks.

Subjective Timing Enhancement Strategy

Subjective timing, as an investment strategy, can be subdivided into several methods, including technical timing, fundamental timing, macro timing, sentiment timing, and event-driven timing. These methods are based on different analysis and decision-making factors, aiming to identify market trends, values, and opportunities to better decide when to buy, sell, or adjust the portfolio.

1. Technical Analysis Timing: Technical analysis is a method of identifying potential market trends by studying historical price and volume data. Investors can use technical analysis tools (such as trend lines, moving averages, relative strength index, etc.) to determine the market's direction, strength, and turning points, thus identifying the timing for buying or selling.

2. Fundamental Analysis Timing: Fundamental analysis focuses on factors such as a company's financial condition, competitive advantages, and industry position. Investors can assess a company's value and growth potential through in-depth research on its fundamentals. When the market price undervalues the company's true value, investors can buy; when the market price overvalues the company's true value, investors can sell.

3. Macroeconomic Analysis Timing: Macro timing enhancement strategies are based on the impact of macroeconomic data on market trends to make timing judgments for more precise asset allocation. These strategies typically involve analyzing factors such as interest rates, inflation, monetary policy, and geopolitical events. For example, during economic expansions, investors may increase stock investments; during economic recessions, investors may reduce stock investments or shift to safer assets. Fund managers make strategic decisions to adjust portfolios based on their outlook and expectations for the global macroeconomic situation. This can yield excess returns from macro timing compared to passive index funds that only track benchmarks.

4. Market Sentiment Analysis Timing: Market sentiment analysis focuses on the impact of investor sentiment and psychological factors on market prices. Investors can use market sentiment indicators (such as the Fear/Greed Index, Investor Confidence Index, etc.) to determine whether the market is overly pessimistic or overly optimistic and make timing decisions accordingly. Buying when the market is overly pessimistic and selling when the market is overly optimistic may help investors achieve excess returns. Sentiment strategies are becoming increasingly popular, with other sentiment strategy indicators including the AAII Sentiment Index, VIX, market barometers, and put/call ratios.

5. Event-Driven Strategy Timing: Event-driven strategies focus on specific events that affect company value (such as mergers, spin-offs, restructurings, etc.). Timing for buying or selling can be determined based on expectations and analyses of these events.

Taking the Pacer Trendpilot US Large Cap ETF (PTLC) as an example, the Pacer Trendpilot US Large Cap ETF (PTLC) is an exchange-traded fund (ETF) based on the US stock market that employs an active timing strategy. Its goal is to adjust exposure to US large-cap stocks based on market trends to achieve relatively stable investment returns.

The fund primarily tracks the S&P 500 index and employs a timing strategy based on moving averages. When the S&P 500 is above its 200-day moving average and the closing price of the last five trading days is above the five-day moving average, the fund fully invests in the S&P 500 index; when the S&P 500 is below its 200-day moving average, the fund allocates 50% of its assets to the S&P 500 index and the other 50% to short-term US Treasury bonds; when the five-day moving average of the S&P 500 is below the 200-day moving average for five consecutive trading days, the fund invests entirely in short-term US Treasury bonds.

Observing the performance of the Pacer Trendpilot US Large Cap ETF (PTLC) in specific market environments, such as the bull market in 2017, the volatile market in 2018, and the market turbulence caused by the COVID-19 pandemic in 2020, reveals characteristics of timing-enhanced funds. In 2017, the S&P 500 index achieved a high annual return, increasing by about 21.8%.

In that year, the PTLC fund's return was approximately 20.4%, slightly below the benchmark index. Although PTLC captured some returns in the rising market, its performance was slightly inferior to the S&P 500 index in this market environment due to management fees and trading costs.

In 2018, the market environment was highly volatile, with the S&P 500 index experiencing significant gains at the beginning of the year but then showing a notable decline by the end of the year, ultimately falling about 4.4% for the year. In contrast, PTLC performed better in 2018, with an annual return of about -3.7%, achieving a certain degree of loss reduction relative to the benchmark index.

At the beginning of 2020, the COVID-19 pandemic triggered significant turbulence in global stock markets. The S&P 500 index fell about 34% in a short period but then rebounded strongly, achieving an annual increase of about 16%. PTLC's performance that year was relatively weak, with an annual return of about 11.5%. Although the fund achieved some degree of loss reduction during the market downturn through its timing strategy, its performance during the subsequent rebound was relatively poor, leading to an annual return below the benchmark index.

Therefore, in rising markets, PTLC's performance is similar to the benchmark index; while in declining markets, the fund's timing strategy may help mitigate losses, but due to tracking errors, it does not outperform the benchmark in all market conditions.

Sector Rotation Enhancement Strategy

The sector rotation enhancement strategy involves determining which sectors are likely to lead based on their position in the business cycle before the market starts to rise, increasing allocations to upward-trending industries or reducing allocations to sluggish industries (i.e., sector "overweight" or "underweight"), achieving excess returns that exceed the tracked index's fluctuations through deviations in sector allocations.

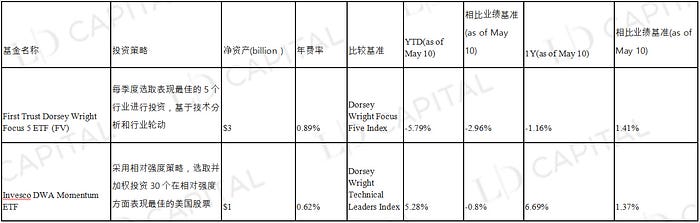

Table 4 Common Sector Rotation Stock Selection Enhanced Index Funds in US Stocks

Taking PDP (Invesco DWA Momentum ETF) as an example, PDP aims to track the performance of the Dorsey Wright Technical Leaders Index, employing a relative strength strategy to select and weight 30 US stocks that perform best in terms of relative strength. Assuming that technology sector stocks perform best in the market, exhibiting high relative strength, PDP will select the best-performing stocks within the technology sector.

To execute the strategy, PDP regularly rebalances its holdings to ensure continued investment in the technology stocks with the highest relative strength. If market conditions change and relative strength in other sectors begins to rise, such as the consumer goods sector, PDP may adjust its holdings and weight investments in the newly best-performing sector based on new relative strength data and market trends.

Overall, PDP's strategy execution method is based on relative strength stock selection and adjusts according to market performance and trends. The basis for selecting stocks is relative strength, i.e., performance relative to other stocks or sectors. By regularly rebalancing holdings, the two funds in the table have outperformed the benchmark over a one-year time frame, but their YTD performance is relatively poor.

Derivative Enhancement Strategy

The derivative enhancement strategy enhances portfolio performance through the use of options, futures, swaps, and other derivatives. These strategies typically involve considerations of leverage, risk hedging, and speculation.

Some derivative enhancement strategies based on US stocks include:

If index futures contracts are trading at a discount to the spot index, one can simulate part of the index position by investing in index futures while obtaining enhanced returns from negative premium convergence. If the futures contract's price is lower than the actual spot index price, one buys the futures contract. Theoretically, by the time the contract expires, the two prices will be very close, allowing the long position in the futures contract to earn slightly more than the spot index during this period. This method tracks the underlying index by allocating part of the funds to index futures, while the remaining idle funds can be invested in fixed income or arbitrage strategies to obtain relatively stable returns.

Calendar Spread: This strategy involves arbitraging the price difference between futures contracts of the same index with different expiration months. When the forward contract is priced significantly higher than the near-term contract, one can establish a long position in the near-term contract while establishing a short position in the forward contract. Over time, the price difference between these two contracts may converge, resulting in excess returns.

Inter-market Arbitrage: When there are pricing discrepancies between two highly correlated markets (such as commodities, interest rates, exchange rates, etc.), one can establish a long position in one market while establishing a short position in another market. Over time, the pricing differences between these two markets may converge, leading to enhanced returns.

Options Strategy: Options are another common derivative. For example, one can enhance returns on existing stock investments by selling covered calls. In this strategy, the fund holds a certain number of stocks and sells an equivalent number of call options. This allows the fund to collect option premiums, thereby increasing overall investment returns. However, the risk of this strategy is that if the stock price rises above the option's strike price, the fund may miss out on some potential gains.

Pairs Trading: This strategy involves two stocks within the same industry or highly correlated stocks. When the price difference between the two stocks exceeds historical normal levels, one can establish a long position in the relatively undervalued stock while establishing a short position in the relatively overvalued stock. Over time, the price difference between these two stocks may converge, resulting in excess returns.

Taking the ProShares UltraPro Short QQQ ETF (SQQQ), which employs derivative enhancement strategies based on US stocks, as an example,

ProShares UltraPro Short QQQ ETF (SQQQ) aims to provide returns that are -3 times the daily performance of the Nasdaq-100 index using market timing and derivative enhancement strategies. This inverse leveraged ETF is designed for experienced investors who believe that technology and large-cap stocks in the Nasdaq-100 will decline in the short term. To achieve investment objectives, SQQQ uses swaps, futures contracts, and options to gain short exposure to the Nasdaq-100 index. Therefore, SQQQ can amplify returns when the underlying index declines but can also amplify losses when the index rises.

Specifically, in the swap strategy, SQQQ obtains short exposure by entering into swap agreements with other financial institutions. In the swap agreement, SQQQ agrees to exchange the returns of the underlying asset (e.g., the Nasdaq-100 index) at a fixed price over a specified period. This allows SQQQ to gain short exposure to the Nasdaq-100 index without actually holding the stocks.

In the futures contract strategy, SQQQ gains short exposure by selling Nasdaq-100 index futures contracts. Through this method, SQQQ agrees to sell the underlying asset (the Nasdaq-100 index) at a specific price on a future date. This strategy allows SQQQ to short the Nasdaq-100 index without actually holding the stocks.

In the options strategy, SQQQ uses put options to achieve short exposure. Put options give SQQQ the right to sell the underlying asset (the Nasdaq-100 index) at a specific price on a future date. Purchasing put options allows SQQQ to profit when the underlying asset declines, thus achieving short exposure to the Nasdaq-100 index. SQQQ executes these trades across multiple trading platforms and venues to ensure liquidity and optimal pricing. However, this ETF is generally considered a high-risk short-term investment and is not recommended for long-term holding.

Multiple Enhancement Strategies Tracking the Same Index Provide Suitable Risk Exposure for Investors

Even when tracking the same index, by offering different index tracking strategies and leveraged products, investors can choose index fund investments that suit their risk tolerance, investment goals, and expected returns. Below is an introduction to some series of products tracking the Nasdaq-100, most of which belong to passive management and aim to provide investors with different strategies for tracking the Nasdaq-100 index to obtain corresponding exposure and returns.

QQQ (Invesco QQQ Trust): As Invesco's core product, QQQ is the most popular and well-known ETF tracking the Nasdaq-100 index (AUM 175780mln). It aims to replicate the performance of the index by investing in the same securities in the same proportion, which includes the 100 largest non-financial companies listed on the Nasdaq stock market. QQQ is a market-cap-weighted ETF, meaning the holdings are weighted according to their market capitalization.

QTR (Global X NASDAQ 100 Tail Risk ETF) aims to track the performance of the Nasdaq-100 index while reducing tail risk. This ETF invests in the same securities as QQQ but also holds put options on the Nasdaq-100 index to hedge against significant market declines.

QQQM (Invesco Nasdaq-100 ETF): QQQM is a low-cost alternative to QQQ. It also tracks the Nasdaq-100 index but has a lower expense ratio. The investment strategy and holdings are similar to QQQ, but with lower fees, making it more cost-effective for long-term investors.

QQQN (Invesco NASDAQ-100 Triple Q Disruptive Innovators ETF) is an exchange-traded fund (ETF) launched by Invesco. This fund aims to track the Nasdaq Q-50 index, which includes non-financial companies ranked 101 to 150 by market capitalization on the Nasdaq. These companies are typically considered to be in a growth phase with innovative capabilities and disruptive technologies. QQQN provides investors with exposure to a group of potential growth companies.

QQQA (ProShares Nasdaq-100 Dorsey Wright Momentum ETF) aims to track the performance of the Dorsey Wright NASDAQ OMX CTA Momentum Index, with enhancement strategies that include momentum strategies based on relative strength signals to select stocks. Relative strength refers to the performance of individual stocks relative to the market or industry.

Based on relative strength signals, it selects Nasdaq-100 index constituents that perform well in the short term. Based on momentum investment strategies, it selects stocks according to their relative strength and adjusts weights accordingly. Strong-performing stocks will receive higher weights, while weaker-performing stocks will receive lower weights or be excluded from the portfolio.

TQQQ (ProShares UltraPro QQQ): TQQQ aims to track the Nasdaq-100 High Beta Index and is a leveraged ETF designed to provide three times the performance of the Nasdaq-100 index. It aims to track the overall performance of the Nasdaq-100 index. Due to its leverage effect, TQQQ typically exhibits higher volatility and risk than the index.

QQQX (Nuveen NASDAQ 100 Dynamic Overwrite Fund): QQQX is an actively managed fund based on the Nasdaq-100 index. It employs a covered call strategy, which involves simultaneously holding the Nasdaq-100 index constituent stocks and selling call options. The covered call strategy aims to increase portfolio income, where the fund holds stocks of the Nasdaq-100 index while simultaneously selling corresponding call option contracts.

If, at expiration, the Nasdaq-100 index price is below the strike price of the call options, the call options will expire unexercised, allowing the fund to retain the premiums collected. This way, the fund can earn additional income by selling call options when the market is stable or declining.

The goal of the covered call strategy is to enhance portfolio returns through this additional income while partially hedging against market downturns. However, the simultaneous sale of call options also limits the potential gains of the portfolio in rising markets, as the fund may be restricted from benefiting from price increases when the call options are exercised.

Conclusion

Compared to the equity ETFs/Index Fund market based on US stocks, the crypto index enhancement product market is still in a very early stage. As the overall market capitalization of cryptocurrencies grows, the market for structured index-enhanced products should also increase rapidly. We believe that various enhancement strategies of index funds and index-enhanced funds/ETFs in the US stock market can correspond to the strategy construction of index-enhanced funds in the crypto market.

Crypto index-enhanced funds can help different risk-tolerant investors achieve corresponding risk exposure and excess returns through these return-enhancing methods, including multi-factor quantitative stock selection models, subjective timing models, sector rotation models, or stock index futures derivative return enhancement models.