A Detailed Explanation of the Sui and Aptos Ecosystem Dex Platform Cetus

Cetus is a Dex and liquidity protocol based on the Move ecosystem.

Cetus is a Dex and liquidity protocol based on the Move ecosystem.Author: AC Capital

On May 2, Cetus announced the completion of its seed round financing. OKX Ventures and KuCoin Ventures led the round, with participation from AC Capital, Comma3 Ventures, NGC Ventures, Jump Crypto, Animoca Ventures, IDG Capital, Leland Ventures, Adaverse, Coin98 Ventures, and others. The new funding will be used to support the initial development and growth of the platform, as well as to expand its market share and customer base.

Cetus is a Dex and liquidity protocol based on the Move ecosystem, using an algorithm similar to Uniswap V3 to build a centralized liquidity protocol and a series of ancillary functions, providing DeFi users with the best trading experience and higher capital efficiency. At the same time, it leverages the unique ecological characteristics of SUI to create composable features different from Uniswap.

01 DEX Who Does It Serve?

The on-chain crypto trading market is relatively small in size but is growing rapidly. The biggest characteristic of such a market is that the vast majority (and still being generated in large quantities every day) of asset types belong to low liquidity and low market cap assets, with a strong demand for price discovery. In such market conditions, how to better achieve price discovery to attract liquidity is the premise for the prosperity of on-chain trading. Therefore, we believe that DEX should primarily serve LPs.

What Are the Demands of LPs? In different trading scenarios, the demands of LPs vary. Earlier this year, we proposed the idea that the audience determines liquidity and categorized on-chain assets into mainstream assets (the top ten assets by trading volume on major public chains) and long-tail assets. Their LP demands are not consistent:

Mainstream LPs: To earn more transaction fee income and incur less impermanent loss (Uni V3 is better)

Long-tail asset LPs: Cheaper, controllable, and flexible market cap strategies (Uni V2 is more convenient, with lower liquidity management costs)

In the long run, the capital-efficient V3 is the trend, but due to these differing demands, Uni V2 and V3 can coexist in data. However, the market will inevitably give rise to players that cater to both demands. In the emerging ecosystem of SUI, Cetus is a stronger candidate.

02 Cetus: The First Centralized Liquidity Protocol Dex in the Move Ecosystem

Cetus currently has a complete product suite including Swap, permissionless liquidity pools, and cross-chain bridges.

Centralized Liquidity

Cetus uses a centralized liquidity market-making algorithm similar to Uniswap V3, allowing an LP to create multiple positions within the same pool. By setting different price ranges, LPs can simulate different price curves to implement their custom strategies. As prices change with the execution of new swaps, the smart contract will consume all available liquidity within the current quoted range until it reaches the next price Tick, at which point the contract will immediately switch to the new Tick, activating any dormant liquidity within the newly activated Tick interval. The interval of the Tick is also correlated with the trading fee levels; the higher the fee, the closer the Tick points are.

By utilizing centralized liquidity, LPs can earn more trading fees and achieve higher capital efficiency.

Permissionless Pool Creation

Before SUI, one of the representatives of high-speed public chains was Solana. However, one major factor for the lack of momentum in the development of the Solana ecosystem was the prolonged absence of permissionless pool DEXs. Community-native or MEME projects struggled to emerge, leading to insufficient attention to the ecosystem and a lack of new hot money, reducing it to a "big player chain." With the launch of SUI, the rapid prosperity of the ecosystem will heavily depend on the status of community-native projects. At Cetus, users can create liquidity pools without permission, and projects can launch new tokens on Cetus without permission. This will attract more early-stage projects and quickly establish pricing power for long-tail assets.

Flexible Trading Fees

Cetus allows teams and users to choose custom trading fee levels, with multiple pools for the same token at different trading fee levels. Currently, four trading fee levels are allowed: 0.01%, 0.05%, 0.25%, and 1%. This design encourages the market to find the most suitable liquidity allocation scheme on its own, providing greater flexibility for LPs and trading users. Stablecoin trading pairs, which are low-volatility assets, may concentrate in the pools with the lowest fees, while high-volatility or low-trading-volume assets may be more concentrated in high-fee pools to hedge risks.

Automatic Position Management

Users can implement take-profit and limit orders based on range orders. After a position is liquidated, general users need to exit their positions promptly to avoid the spot price re-entering the price range. Users can also use third-party position managers integrated with Cetus to manage their positions, thereby reducing the difficulty of liquidity management and facilitating long-tail asset LPs.

Composability

CETUS supports high composability, allowing other project teams to easily establish a swap interface on their front end by integrating the Cetus SDK, enabling quick access to Cetus's liquidity. For example, the options project Typus in the ecosystem achieved one-click hedging for long-tail assets by integrating CETUS, while also enhancing the liquidity and coverage of its own options. Secure Cross-Chain Bridge The cross-chain bridge created by Cetus based on Wormhole went live in November last year, allowing users to safely and conveniently transfer assets across nearly 20 public chains. Strongly Correlated Token Economic Model Cetus has adopted the xToken economic model. By holding CETUS tokens and xCETUS, users can receive protocol revenue sharing, ensuring the alignment of community and protocol interests.

03 Cetus Team: Experienced in Developing Centralized Liquidity Market-Making Algorithms

Uniswap v3 represents an innovation in the DeFi architecture, with its core being the centralized liquidity market-making algorithm (CLMM), which maximizes the capital utilization of LPs. However, Uniswap established a commercial source code license in March 2021 to prevent others from forking its source code, which expired in April. On EVM chains, competitors like Pancake and Quickswap have already launched V3 alternatives. However, there are fewer competitors in the CLMM track on non-EVM high-speed chains. In the future, competition among CLMM-type DEXs will trend towards the operational side, with the lightly operated Uniswap gradually becoming disadvantaged. Cetus is backed by a mature Dex team with development and operational experience, and its APTOS version has been deployed and is running stably. With a guaranteed product, strong BD capabilities within the ecosystem, and continuous narrative capabilities in operations, the Cetus team is expected to achieve a leading position in CLMM infrastructure on SUI.

++04++ The Innovative Soil Brought by Centralized Liquidity Protocols in DeFi

Automated Liquidity Management Protocol for LPs

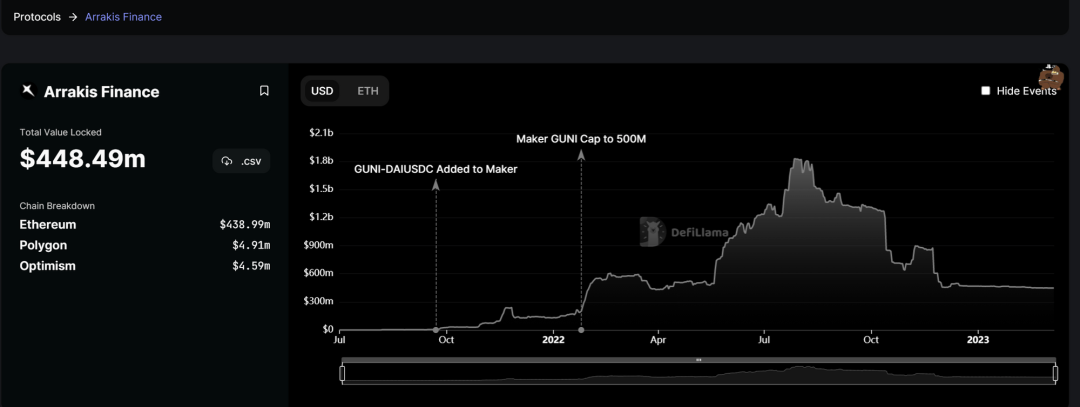

Under centralized liquidity protocols, LPs generally choose to provide liquidity near the market price, but when the market price exceeds the strategy range, LPs face not only impermanent loss but also the inability to earn LP fees, requiring them to actively redeploy their market-making strategies. Automated liquidity management protocols have emerged to help LPs automatically execute market-making strategies. Leading projects like Arrakis Finance have already reached a TVL of $440 million.

These protocols can also achieve:

- Single-sided asset LP mining, where LPs can preferentially deploy initial liquidity, such as only deploying project tokens. The protocol can help absorb base assets like USDT or ETH to balance the liquidity composition, and as trading occurs, the project's native assets will gradually be converted into base assets. In this case, LPs can achieve liquidity without selling their own tokens or needing to incentivize external capital.

- Issuing ERC20 LP tokens to LP providers, which can not only be liquid but also be re-collateralized, further enhancing the capital efficiency of LP assets.

New Types of Liquidity Mining and Leveraged Mining

Previous passive liquidity mining also had leveraged mining, but since liquidity is evenly distributed, the overall yield of leveraged mining is not ideal. Under the CLMM algorithm, the advantages of capital are amplified, allowing professional quantitative institutions and market-making teams to granularly implement more customized strategies. Liquidity mining pools can obtain funds from protocol users or lending protocols, adopting proactive and stable strategies to generate returns, which holds immense value for large users with investment needs.

New Derivative Systems

Under the CLMM system, while LP yields increase, they also face higher impermanent risks. In extreme market conditions, the liquidity set by LPs can be drained by arbitrageurs. How to construct derivatives that can hedge LP market-making risks to buffer against project malicious sell-offs that harm LP interests is also a track worth paying attention to.

Based on the composability advantages of the CLMM algorithm, there are many potential DeFi protocols that can be explored, especially after events like the FTX collapse and BUSD regulation, the importance of DeFi has become increasingly evident. The above three DeFi products are just the tip of the iceberg.

05 Conclusion

We believe that the Cetus team possesses mature product delivery capabilities, strong BD capabilities across ecosystems, and operational capabilities. They have a profound and unique understanding of the DEX product and track. We believe that Cetus has a high potential to become a leader in the unique ecological track of SUI.