2023 Q1 Market Review: Looking for the True Competitor to the Dollar System

In the second half of 2023, Bitcoin is expected to rise above $32,000.

In the second half of 2023, Bitcoin is expected to rise above $32,000.Author: Bing Ventures

The anticipated rebound will be pushed back to the first quarter of next year. Of course, do not base expectations on a policy shift; expectations should be based on technological innovation. The only point we can expect is that the global spillover effects of interest rate hikes are backfiring on those fragile fiat currency units.

--- --- "Using the Catfish Effect to View the Rebound of Cryptocurrency," Bing Ventures, November 19, 2022

The first quarter of 2023 ended perfectly, and the volatility in the cryptocurrency market is evident. We share a retrospective analysis of the cryptocurrency and macro markets for the first quarter of 2023, along with predictions for the next phase.

Bitcoin: Strong Rebound Followed by Consolidation

The cryptocurrency market performed strongly in the first quarter of 2023, with a total market capitalization growth of 49% to $1.19 trillion. Bitcoin rose by 72%, closing at $28,440; Ethereum increased by 53%, closing at $1,827. This wave of market movement was driven by multiple factors, such as tightening monetary policy and banking crises. However, there are some signs indicating that this upward trend may not last, such as increased outflows of stablecoins and funds leaving exchanges.

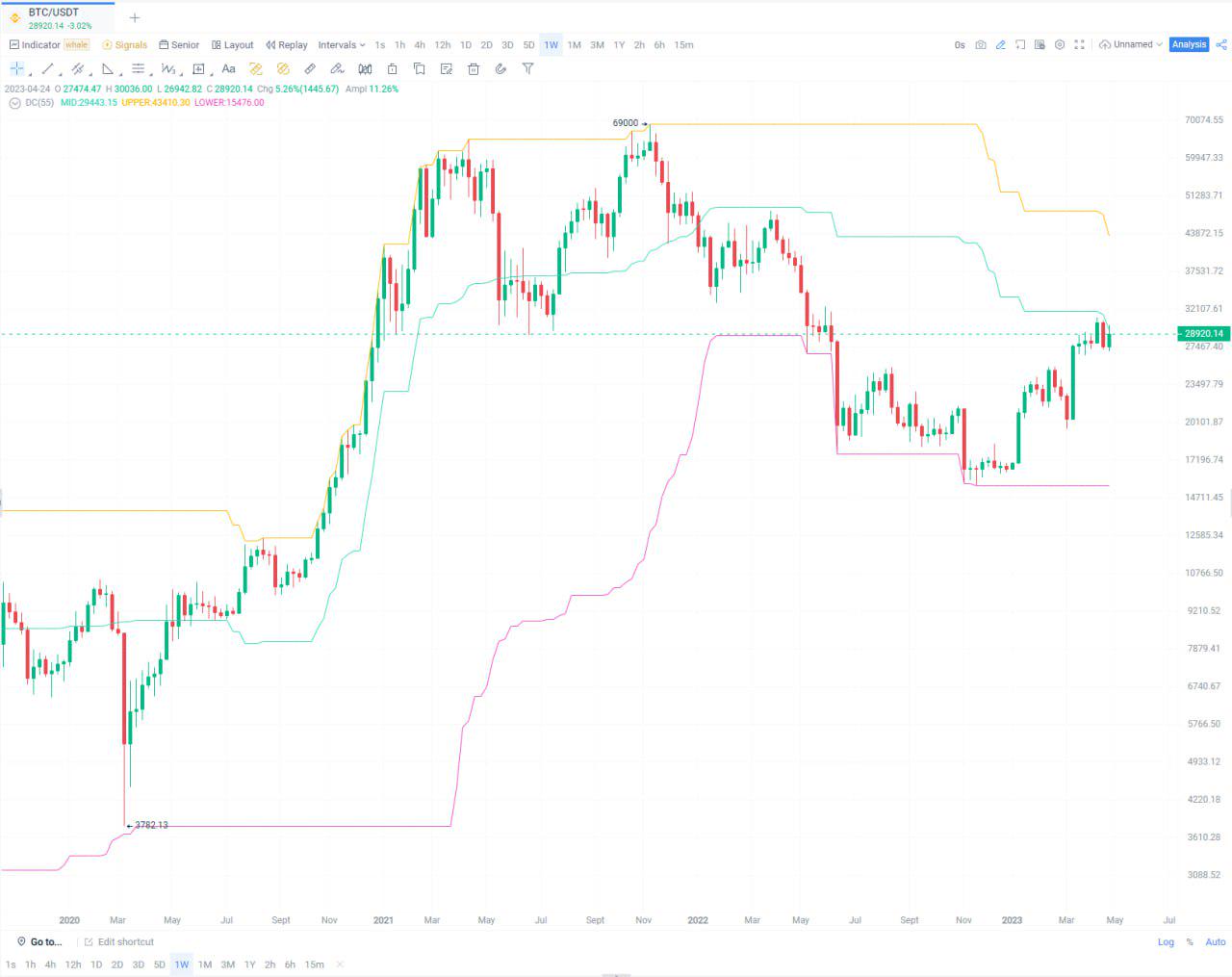

Bitcoin tested the support level of $15,000 in the first quarter and began a rebound. Entering a new quarter, BTC also started a new journey at the weekly and monthly levels. We attempt to introduce the Donchian Channel to show market price volatility. (Note: It consists of three differently colored lines, typically calculated using the highest and lowest prices over a 20-day period. When the channel narrows, market volatility is low, while when it widens, market volatility is high. The Donchian Channel can be used to determine buy and sell timing; when the price breaks above the upper channel, it may signal a buy; when the price breaks below the lower channel, it may signal a sell.)

- Weekly: From the perspective of the Donchian Channel DC indicator, BTC is still operating below the DC centerline of $32,000, having slightly oscillated for more than two weeks after a strong rebound, indicating that it is still in a post-rebound consolidation phase at the weekly level. Combined with the ATR indicator (Average True Range), the ATR has emerged from a long-term downtrend but is currently still at a low point in the cycle, indicating that the market is in a consolidation phase. We can use the DC centerline along with the ATR indicator as a reference signal; once the weekly chart breaks above the DC centerline of $32,000 and stabilizes, and the ATR also reverses and breaks through, it indicates that a strong upward phase is coming, allowing for timely entry.

- Monthly: The BTC monthly chart has just completed three consecutive bullish months, but it has not fully offset the decline from the opening price of $35,000 in June last year. Considering the price of the weekly DC centerline, $32,000 is the next major resistance level for upward movement. From the monthly DC indicator perspective, BTC is still operating below the centerline, with a significant distance from the lower channel. The ATR indicator is still in a long-term downtrend, indicating that there will not be an instantaneous reversal in market trends.

In summary, BTC has just completed a strong rebound in the first quarter, with nearly 80% growth throughout the quarter, which is undoubtedly a good signal for long-term investors, indicating that the quarterly trend has also ended its decline and will now undergo new oscillation and consolidation.

U.S. Stocks: Macroeconomic Uncertainty Remains, Future Uncertain

The performance of the U.S. stock market in the first quarter of 2023 generally met expectations, with both fundamentals and technicals playing a positive role. First, the PCE year-on-year increase of 5% fell short of expectations, indicating a slowdown in inflationary pressures, which is favorable for the stock market. Second, the U.S. economy remains strong, with continued corporate earnings growth supporting the stock market's rebound. Third, employment data looks good, providing more growth opportunities for U.S. corporate performance. On the policy front, a future shift in the Fed's stance could help alleviate downward pressure on the stock market.

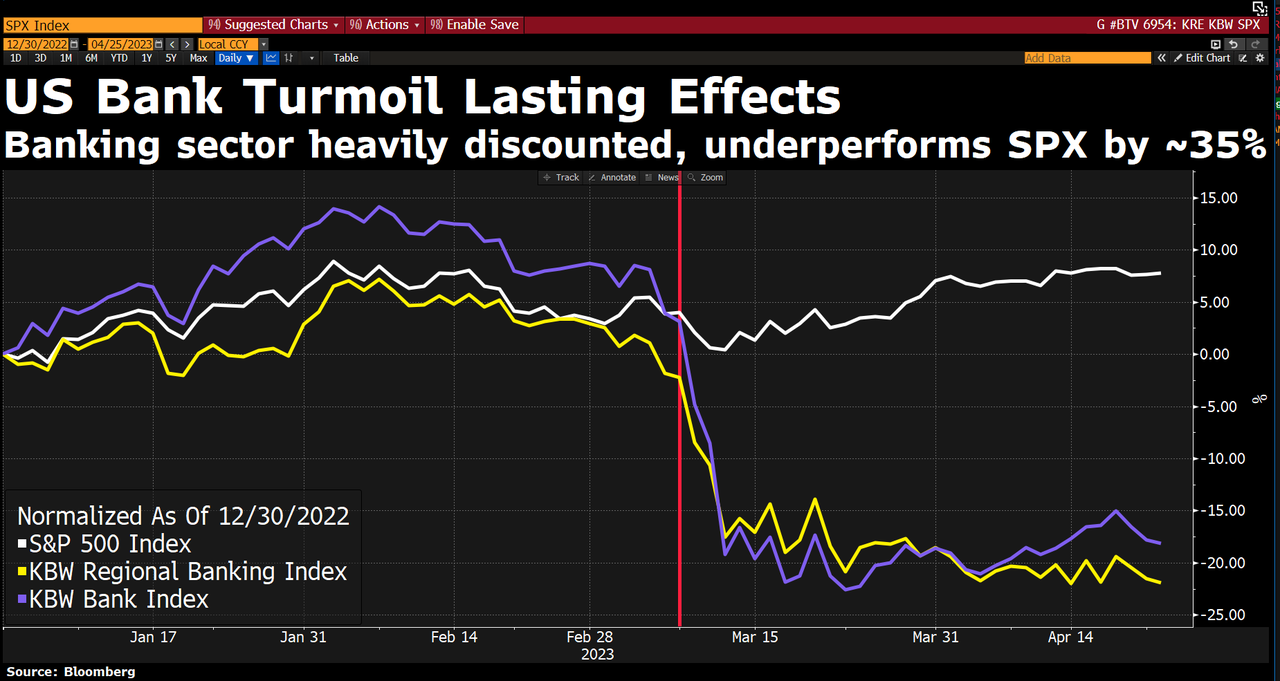

Looking back at Q1, the S&P, Dow, and Nasdaq all performed strongly, with the Nasdaq leading the way, mainly due to the strong performance of tech stocks. Both Meta and Tesla saw their stock prices rise by over 60%. However, bank stocks performed poorly, with the KBW Bank Index and KBW Regional Bank Index both declining. The U.S. economy is facing a binary choice between recession or continued stock market growth. We believe one of the biggest risks the market faces in the coming months is stagnation in the U.S. economy.

The Q1 earnings season and economic data releases will significantly impact the stock market's performance in the next quarter, especially data related to corporate earnings and economic growth. In this context, a shift in the Fed's stance may help warm up the stock market. We must acknowledge that the rise of the S&P 500 in the first quarter masked the overall market's downturn, with large tech stocks becoming a safe haven for investors.

However, the trajectory of U.S. stocks in the second quarter is becoming increasingly difficult to predict, primarily due to the ongoing uncertainties since last year, especially the impact of the Fed's interest rate hikes on the U.S. economy. Although the S&P 500 index has shown range-bound oscillation, daily volatility has increased, making it harder to determine the market's health. The earnings season for U.S. stocks in Q1 is underway, and the overall EPS for S&P 500 constituent companies is expected to decline, with the overall profit contraction trend likely continuing until the end of this year, before recovering growth trends in 2024.

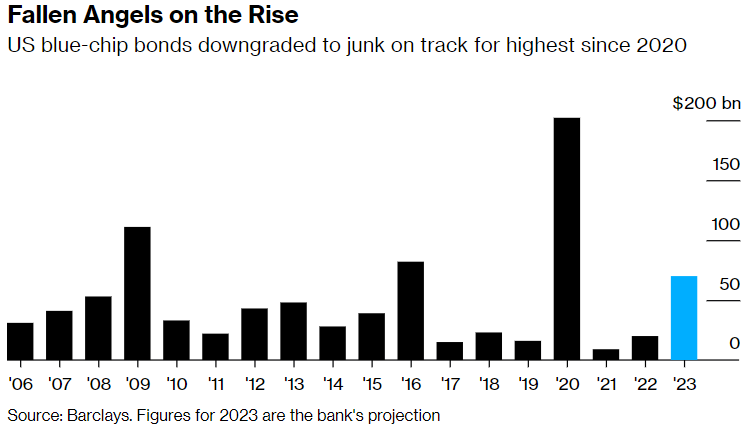

U.S. Treasuries: The Process of De-dollarization Accelerates, Foreign Purchases May "Increase on Paper but Decrease in Reality"

The yield on the U.S. ten-year bond has long been in a downtrend, but each time it rises to the upper edge of the downtrend channel, a financial crisis occurs globally. This time, the degree and speed of the rise in U.S. bond yields have reached a 40-year high. Currently, the U.S. bond yield curve is rapidly trending positive, appearing to be an early sign of a U.S. economic recession. The UK and Eurozone are the main buyers of U.S. Treasuries, while Japan and South Korea are "forced" to reduce their holdings, and China continues to decrease its holdings. In the second quarter of 2023, the momentum of foreign capital returning to the U.S. may further slow down, and there may even be a situation where U.S. Treasuries "increase on paper but decrease in reality."

Recently, under the influence of banking risk events, investors have lowered their overall judgment on the 10-year U.S. Treasury yield range for the next three months, with the mainstream view still oscillating in the range of 3.4% to 3.6%.

The latest international capital flow report shows that in January of this year, at least 16 countries sold U.S. Treasuries, including China, Belgium, Luxembourg, Ireland, Brazil, France, Saudi Arabia, Germany, Mexico, Israel, Kuwait, Colombia, Sweden, the Bahamas, Vietnam, and Peru. This trend reflects an increasing awareness of the backlash effects of the U.S. debt economic model, and monetary authorities are well aware of the unreliability of U.S. debt—as a core dollar asset. At the same time, this trend aligns with our prediction in the article "++The Fed's Overconfidence with Hands in Pockets++" published on October 18, 2022: "The Fed's aggressive rate hikes and rapid appreciation of the dollar will further accelerate the de-dollarization and de-Treasurization processes in some countries."

Dollar: Reduced to a Weapon in International Financial Markets

The U.S. non-farm payroll report for March, released on April 7, shows that the labor market is resilient and exceeds expectations. Meanwhile, the Consumer Price Index (CPI) released on April 12 showed a decline. Despite growing concerns about the dollar index's weakness, U.S. economic activity remains reasonable, and inflationary pressures have eased. We believe the overall environment may push the Fed's monetary policy tightening cycle close to an end.

Source: Bureau of Labor Statistics

Previously, the Fed's aggressive tightening and massive capital inflow into the U.S. created a "dollar shortage." The global "dollar shortage" has intensified but has not triggered a market liquidity crisis. In the first quarter of 2023, the influx of foreign capital into dollar assets has slowed due to the dollar's oversupply. Therefore, we believe the dollar index may test its low point for the year in the coming weeks and then maintain oscillation.

Most importantly, the Russia-Ukraine war has made users of the dollar system acutely aware that dollar reserves can be frozen by the U.S. The gradual decoupling and multipolar division of the global financial market is currently the trend. If the value of the dollar system declines, the value of its counterpart will rise, and at least one strong currency will emerge.

Conclusion: Returning Above $32,000

We believe that when certain countries' fiat currencies, based on national credit, further collapse due to debt crises, Bitcoin will fully reveal its role in countering the entire debt financial system. As long as the scale of debt continues to expand, the source of gold within Bitcoin's credit regeneration pool will continue to grow. In the second half of 2023, we expect Bitcoin to rise above $32,000. We are optimistic about the following catalysts for Bitcoin:

- Lower inflation

- Easing energy issues

- Ceasefire in the Russia-Ukraine war

- Reversal of M2 supply

These factors will drive the beginning of a new bull market. We believe consumers will gradually view Bitcoin as a store of value and a hedge against M2 inflation, rather than a direct hedge against CPI inflation. Especially in emerging markets caught in the middle of multipolar friction, Bitcoin will become one of the best neutral alternatives to dollar hegemony. Meanwhile, if the economic recession we anticipate occurs, the Fed is likely to pause interest rate hikes, while monetary overexpansion and government budget deficits will continue.

We still maintain the view expressed in last year's article "++The Fed's Overconfidence with Hands in Pockets++": "The author expects that by mid-next year, the CPI year-on-year will likely fall below 5%, while the unemployment rate will continue to rise, providing the Fed with the best reason to end interest rate hikes." This round of global "dollar shortage" has exposed the inherent flaws of the current international monetary system, and combined with geopolitical factors, it helps promote the multipolarization of the international monetary system.

The counterpart of the dollar system will inevitably have less power and discretion than the current dollar system managers, fundamentally eliminating the risk of fiat currencies being weaponized by a small number of authoritarian countries. In this context, the complete denationalization narrative of Bitcoin is a wiser choice. The large-scale liberalization of Bitcoin can significantly reduce the probability of conflicts among interest groups in political management.

In summary, we believe we are at a very important turning point in the economic cycle. The Fed's biggest problem lies in merely managing economic growth and inflation issues. When an unpredictable crisis occurs in the economy, the challenges faced by the Fed will be greater. In this case, if no specific bad news related to cryptocurrencies emerges, Bitcoin's price can rebound and climb back to the height of $32,000.