Mint Ventures: The Outlook for the "Native Bond Market" in the Crypto World

Why the on-chain bond market has not developed rapidly and what direction it may take in the future.

Why the on-chain bond market has not developed rapidly and what direction it may take in the future.Written by: Colin Li, Mint Ventures

Supply: The Cycle is Unfavorable for Long-Duration Low-Risk Investors

In traditional finance, bond investors generally have a lower risk appetite than stock investors. The goal of bond investors is to take on relatively low risk to achieve more stable returns.

The crypto market has grown to become a massive market with a total market capitalization exceeding $1 trillion. However, against the backdrop of BTC's "4-year halving" and the rapid rise and fall of bubbles caused by the industry's wild growth, the market has exhibited extreme volatility. For example, during a bull market, Bitcoin can yield returns of dozens or even hundreds of times at its peak, but after turning bearish, it can quickly experience declines of 80% or more. Other cryptocurrencies show even more exaggerated performance in bull and bear markets. This high volatility has led to approximately 90% of traders losing money and exiting the market. Perhaps for this reason, we see that perpetual contracts, which are settled daily, are more popular, while longer-duration leverage is almost nonexistent.

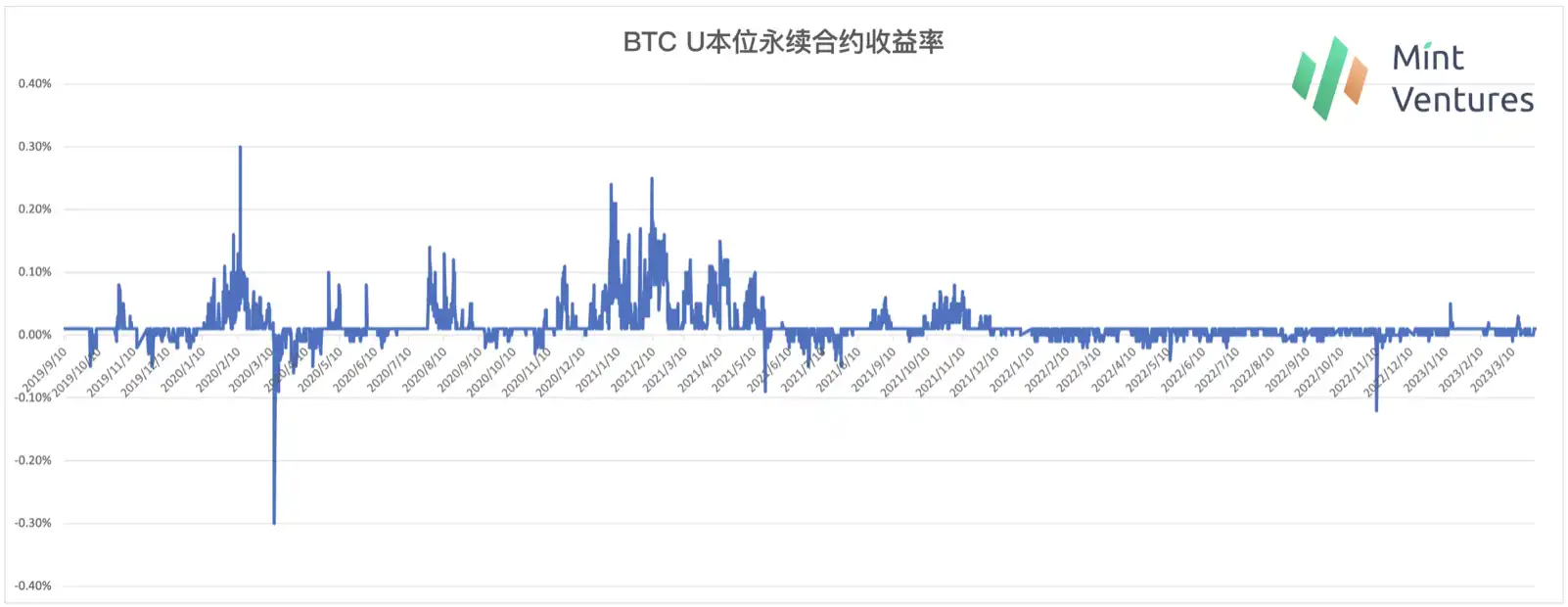

Other low-risk investment opportunities in the market also exhibit strong cyclicality. Taking the funding rate of the longest-existing BTC perpetual contracts as an example, the market's yield in a bull market is significantly higher than in a bear market. This instability in investment returns makes it difficult for long-duration liability investors seeking to invest in lower-risk "bond-like" opportunities to find high-risk investors who can sustain high financing costs over the long term.

Demand: Institutional Large-Scale Entry and DAO Treasury Narratives Have Yet to Materialize

In the recent bull market, the themes of "institutional" entry and DAO Treasury have been repeatedly mentioned, which is also the original intention behind some projects, such as DeFi projects targeting market makers. However, following the collapse of Luna in May 2022 and the subsequent impacts on Three Arrows and FTX, many institutional investors were hit hard. This not only affected the use of existing funds in the market by institutions but also led regulators to pay more attention to the regulation of the crypto space. Coupled with the recent bankruptcies or exits of a few crypto-friendly banks in the U.S., large-scale institutional entry may require more time and confidence to recover.

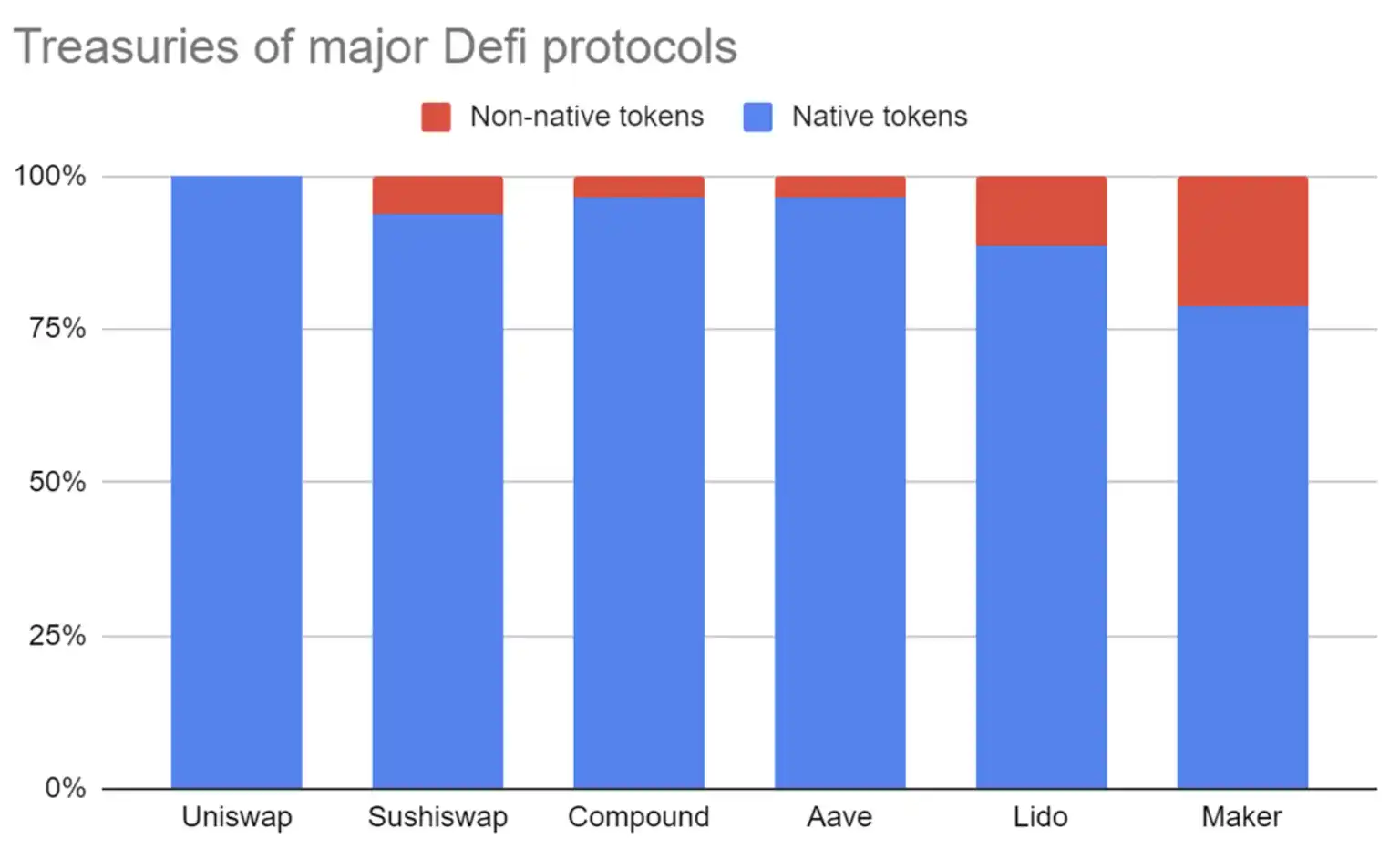

There has been much discussion in the market regarding the narrative of DAO Treasury financial management. However, Hasu analyzed the distribution of funds in Treasuries back in 2021. Most assets are the project's own tokens. Even looking at it now, quality projects like Lido and MakerDAO treasury still primarily hold their own tokens.

Even if we do not consider the current situation and look to the future of DAOs, it is likely that most projects will not have enough other assets stored in their Treasuries. This may relate to the inherent characteristics of the crypto industry. Since the crypto industry develops globally, there is no unified regulation among countries, leading to a strong Matthew effect in the crypto space. This phenomenon is particularly evident in the most mature decentralized exchanges (DEX) and lending sectors within DeFi at this stage. The reason for this situation is that the crypto market connects global liquidity and is still insufficiently regulated.

DeFi is a form of finance and will inherently possess some financial characteristics, such as investors expecting the lowest costs, highest returns, and best security. Since it does not involve customer management, differentiation can only be made at the product level, but as open-source projects, it is not difficult to copy code or product features. However, due to DeFi's inherent preference for liquidity and trading costs, user liquidity cannot be easily replicated. Therefore, the Matthew effect is quite strong, with early projects having a greater chance of becoming leaders.

In traditional markets, some regulatory policies aim to prevent monopolies, hoping to have enough market participants and reviewing mergers and acquisitions, which in a sense suppresses the Matthew effect. Looking back at DeFi, there is no regulation, no customer service, and no artificial suppression of monopoly issues from regulators, so the Matthew effect is stronger than in traditional fields.

So, will many current DeFi projects still exist in the future? It may be difficult, or even if many DeFi projects exist, the vast majority may be small in scale, with the top three projects possibly holding a market share of 95% or even higher. The assets in the DAO Treasuries of leading projects will be more substantial, so the narrative that many DAOs have large Treasuries may not hold true; only a few leading DAOs in each sector may have enough funds for Treasury management.

In the long term, most sub-sectors of DeFi may experience an oligopoly with leading projects capturing around 90% of the market share due to their advantages in liquidity and trading costs. Therefore, there may not be many funding scenarios that DAOs need to manage.

Tokens Have Dual Characteristics of Equity and Debt

Returning to the tokens themselves, tokens possess dual attributes of equity and debt:

From an equity perspective, holding tokens allows participation in community voting and deep involvement in project governance, and may also entitle holders to a share of the fees and commissions earned by the project due to value capture attributes. From a debt perspective, tokens have their unique characteristics. In the traditional business world, when a company expands and engages in equity financing, it can obtain cash. To gain a larger market share, it will use the funds obtained for marketing, such as advertising, physical rewards, and discount incentives. At this point, the company offers equity in exchange for cash.

In the crypto market, once a project is established, a portion of its tokens is used as "incentives." When users engage in behaviors that meet the project's requirements, they become eligible for incentive distribution. Generally, when tokens are distributed as incentives, they are settled at a specific time point, such as every block, daily, or weekly. Since user behaviors occur before the distribution of token incentives, each time before the token incentives are distributed, it is akin to the project owing "debts" to users, similar to "estimated liabilities" in traditional accounting for sales rebates. If the founding team wants to expand its debt, it can reserve more tokens as "incentives" for post-launch project operations. The existence of this type of "incentive" as a new form of debt is preferable to directly applying for loans or issuing bonds, as traditional loans and bonds are rigid debts denominated in fiat currency, which can be a significant burden for any founding team. If they cannot repay, they face legal and other issues. In contrast, the issuance rights of tokens lie with the project itself, with no expected price requirements, only a planned quantity of tokens. This new form of debt is more favorable for project parties. The emergence of tokens as a new medium of value and financing method has significantly reduced the need for traditional debt financing by project parties.

Future Development Predictions

From the three points mentioned above, it can be seen that, whether from the strong cyclicality of the market itself or from the supply and demand sides of fixed-income products, there is currently no visible soil for the development of a market similar to traditional bond markets. What kind of bond market might be more suitable for the development of the crypto industry?

From the Perspective of Interest Rate Benchmarks

The yield of POS based on public chains may be the best choice. This yield level is based on a larger ecosystem, and its business development volatility is generally smaller compared to individual Dapp projects. Furthermore, this yield anchors the growth of the ecosystem, making it more easily accepted by participants of that chain. Additionally, a Dapp has control over user incentives, meaning not every user needs to buy the Dapp's token; for public chains, as long as users need to engage in substantive activities on the chain, they must purchase the public chain token to pay fees, which may lead to a greater dispersion of public chain tokens. Moreover, influenced by the theory of fat protocols, many investors tend to buy public chain tokens to earn beta returns. Therefore, PoS yields are not significantly affected by individual Dapp project parties over the long term and are more stable.

From the Audience Perspective

It is more suitable for the participants in the bond market to be positioned as high-risk speculators and low-risk arbitrageurs. Currently, the crypto market lacks long-duration investors, making it difficult to find a large number of stable investors. Additionally, the volatility of interest rates still requires another counterparty to bear the risk; risk can only be transferred, not disappear out of thin air, so a high-risk participant willing to speculate on interest rate fluctuations is needed. Although there is a lack of funding sources from institutions and DAOs, there are many arbitrage traders in the market, and this group of investors can serve as a source of funds for "low-risk investments." Meanwhile, the market is filled with high-risk speculative traders, who can absorb volatility on the other end. For example, projects like Pendle, which are based on LSD-derived yield tokenization, split the yield of LSD into two parts:

Principle Token, a fixed-rate product that can be seen as a zero-coupon bond;

Yield Token, with floating interest rates, allowing users to buy yield tokens to speculate on future increases in yield. This satisfies the yield requirements of arbitrageurs and low-risk investors while allowing high-risk investors to participate in speculative predictions regarding LSD yields.

From the Perspective of Duration

The overall cycle of the crypto market is relatively fast, so the duration of bonds should also be shorter, such as bonds with a maturity of less than one year. The benefit of this design is not only favorable for low-risk arbitrage traders but also for high-risk traders: short-term interest rate fluctuations will be more intense and frequent, providing more potential trading opportunities for short-term traders.

Risk warning

Risk warning Risk warning

Risk warning