Multi-Ecological LSD Development Report: The Track is Grand, the Project is Early Stage

The development and gameplay of LSD in public chain ecosystems such as BNB Chain, Cosmos, and Polygon.

The development and gameplay of LSD in public chain ecosystems such as BNB Chain, Cosmos, and Polygon.Written by: waynezhang.eth

Last week, we released the LSDFi Ecosystem / LSDFi War Report and the report on the impact of the Shanghai upgrade on LSD, but both the selected projects and the thinking background are based on Ethereum. This is because the amount of funds brought by Ethereum's liquid staking alone exceeds $14 billion. Today's report will explore the development and gameplay of LSD in other public chain ecosystems, and observe the development status, trends, and the impact of data on the LSD industry, as well as discussions on LSD product design and legitimacy.

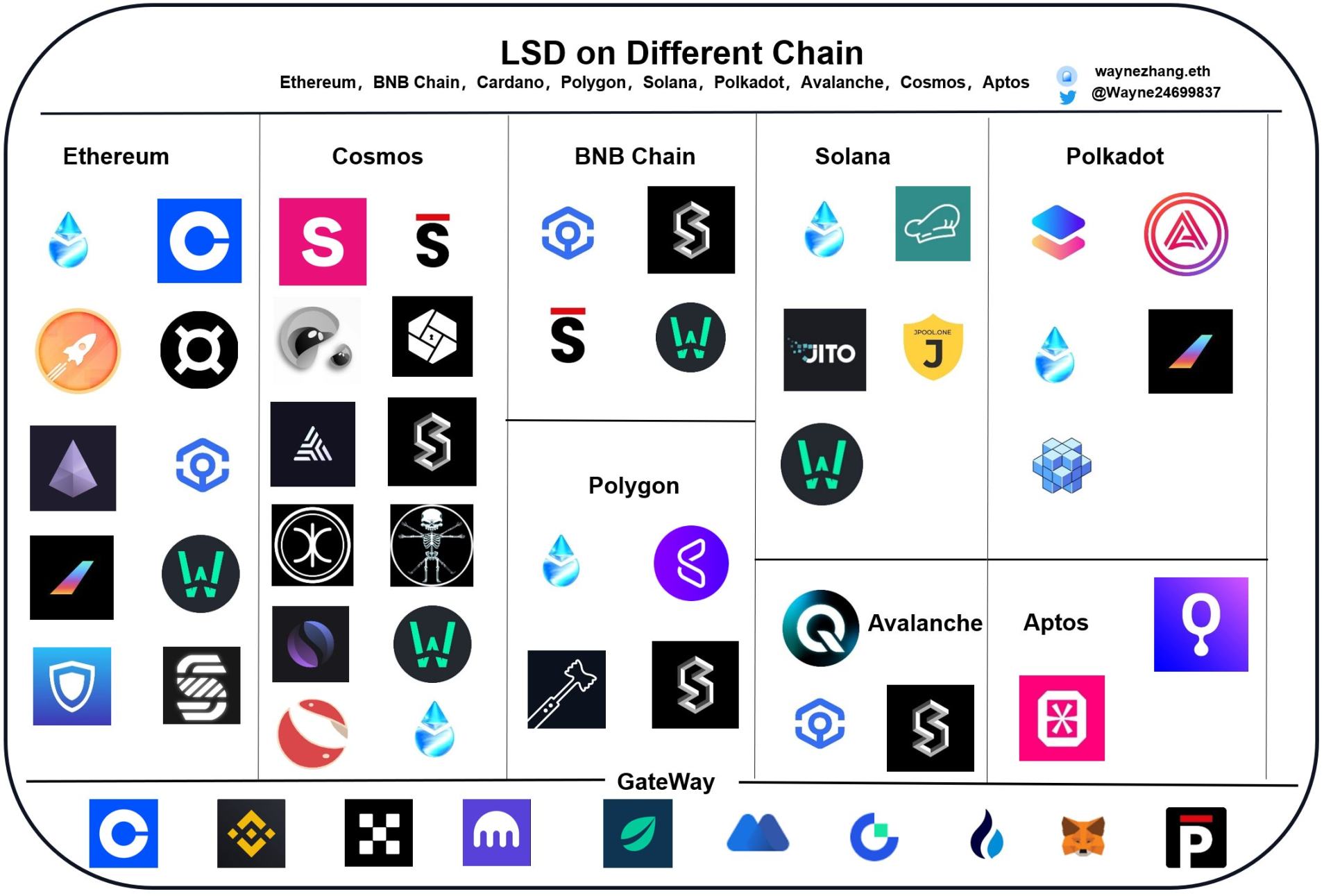

The public chains included in this research will be: BNB Chain, Cardano, Polygon, Solana, Polkadot, Avalanche, Cosmos, Aptos (some public chains ranked in the top 25 according to Coingecko MC).

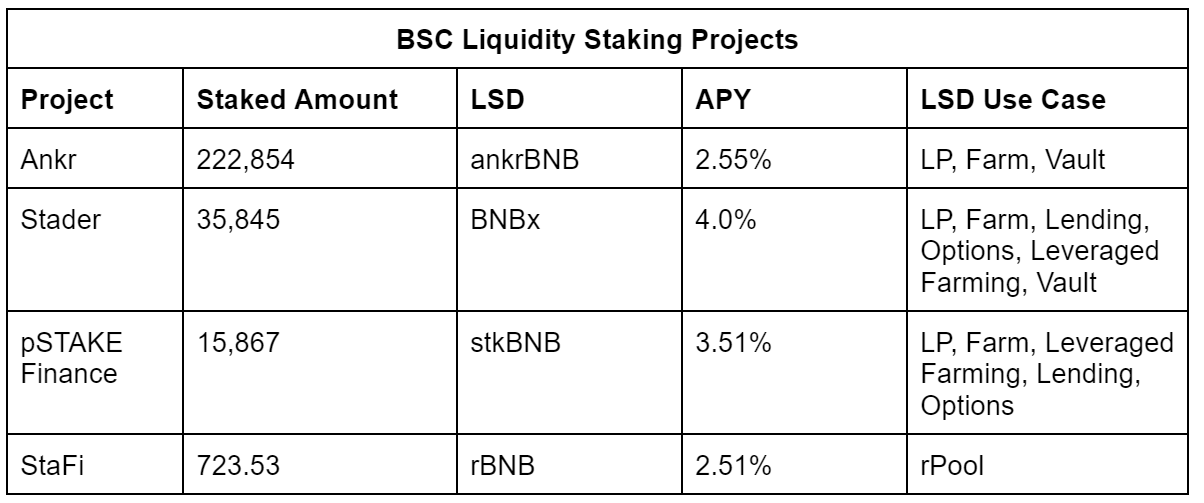

BNB Chain

The current staking status of BNB is similar to Ethereum, with a staking rate of 15.44% (Ethereum is about 15.43%), and the average annualized yield for staking is currently about 2.84%, which is relatively low. Among them, the largest decentralized staking platform on BNB Chain, Ankr, accounts for about 0.56% of the circulating supply.

I believe the reasons for the slow development of LSD on BNB Chain are as follows:

The profitability of native DeFi protocols on BNB. From DeFillama data, it can be seen that among the 337 trading pairs involving BNB, over 80% exceed the average annualized yield, not to mention the various DeFi protocols on the chain, most of which are likely to far exceed the staking yield.

BNB utility

① BNB is also the platform token of Binance exchange. Holding BNB in the exchange can earn fee discounts and other services.

② At the same time, Binance has its own dedicated services such as Launchpad, which attracts users to keep their BNB in wallets or exchanges. For example, in the recent Space ID launchpad, the total amount of BNB invested reached 8,677,923.94, with 103,598 participants. This number is nearly 39 times the total staking amount of Ankr.

For trading-type holders, whether it is kept in Binance for fee discounts or participating in various DeFi products on DEX, the yield and stability are higher. In BNB Chain, the potential for LSD is far less than that of ETH chain.

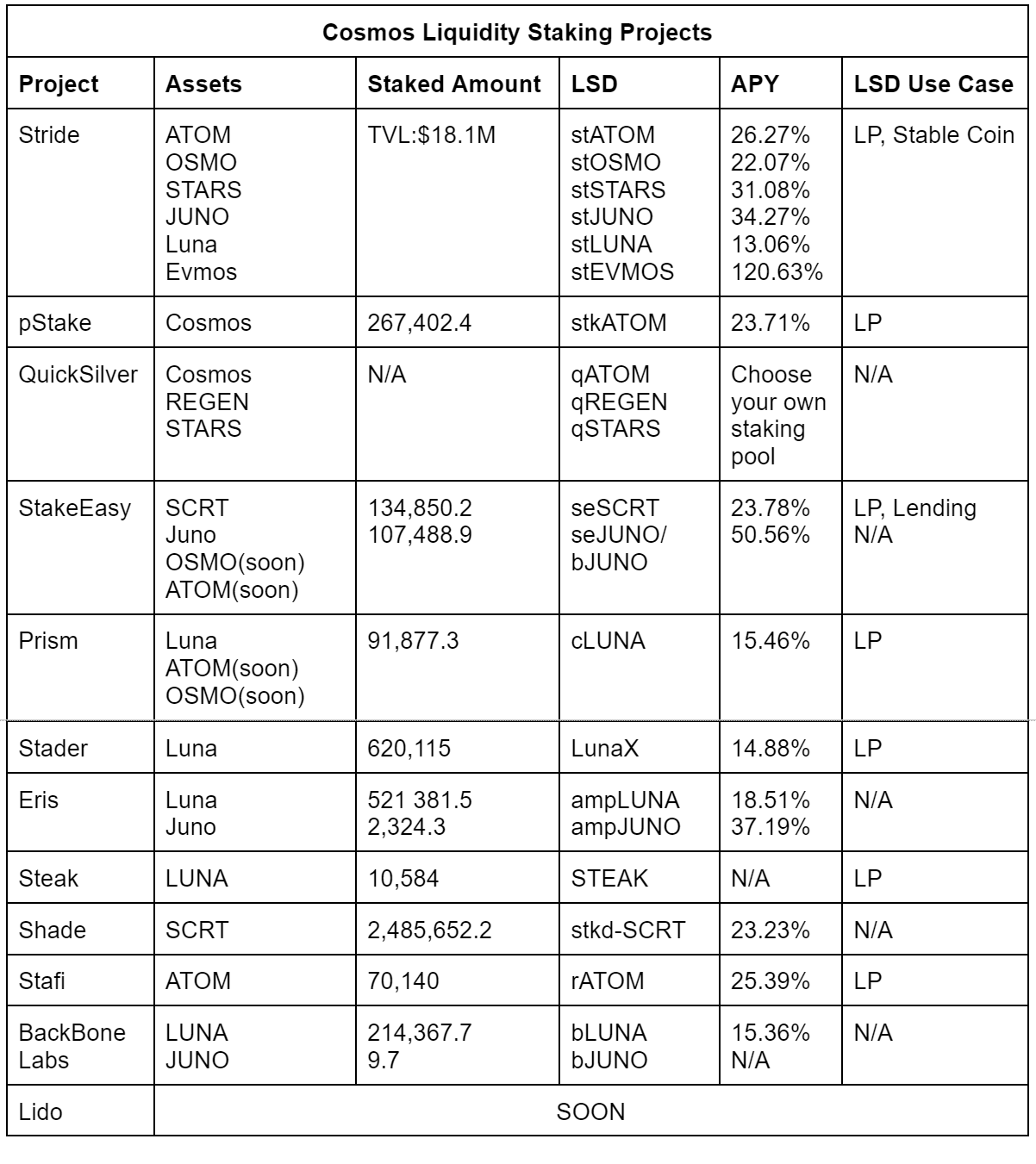

Cosmos

The staking rate of Cosmos Hub is about 61.96%, with an average staking yield of about 25.92%, and it requires a waiting period of 21 days after applying for unstaking. The staking status of Cosmos is technically distinctive compared to ETH and BNB chains. Since ATOM is only the token of Cosmos Hub, any application chain launched within the Cosmos ecosystem can operate without using ATOM tokens. This is because the fee logic is native to each application chain (developers choose which token to pay gas), and each application chain has its own validator network. Therefore, when compiling statistics, we cannot only consider the protocols on the ATOM chain. Stride, QuickSilver, etc., have their own chains for protocol construction, so we will compile the LSD protocols on Cosmos and its IBC chains (mainly focusing on ATOM, OSMO, STARS, JUNO, Luna, Evmos).

From the table above, you can see two interesting points:

The LSD scale in the Cosmos ecosystem is currently very small, and there are not many LSD application cases. Stride, as the current leader in Cosmos LSD, has a total TVL of only $15M.

Luna appears in many LSD projects and has many types of LSD.

1. Why is the LSD scale small?

① The Cosmos ecosystem actually has many similar L1 chains, but these ecosystems are temporarily unable to break out of Cosmos. Cosmos is not a unified public chain but consists of special function chains and Appchain chains through the IBC protocol, such as Kava and Osmosis. General chains like Canto, Juno, and Evmos are still in their infancy.

Luna once had over $30 billion worth of LUNA staked across various protocols on March 2, 2022, surpassing the staked value of $28 billion ETH, becoming the second-largest staked asset among mainstream cryptocurrencies. At that time, Lido also participated in designing bLUNA as an LSD, but the subsequent Luna-UST incident occurred. Terra then had rich infrastructure, and LSD could be used as collateral for UST, lending, etc.

② Opportunity cost: Overall, high yields bring opportunity costs. Taking ATOM as an example, if holders do not stake ATOM, their opportunity cost is about 26%. You can check the liquidity list of Osmosis, where only three ATOM LPs exceed 26%. Of course, there are other high-yield methods, but none are as stable and secure as direct staking. This also creates a vicious cycle: low DeFi utilization → yields lower than staking → reduced user participation in DeFi → low DeFi utilization.

③ Airdrops: Projects like Stride and Quicksilver in the Cosmos ecosystem usually airdrop a certain proportion of tokens directly to Cosmos token stakers upon launch, and according to my investigation, it seems that staking in LSD does not qualify for airdrops. So the opportunity cost further increases.

④ Liquidity risk: ATOM staking as LSD requires a 21-day waiting period to unlock (Stride shows as 21-24 days), which affects not only LSD but also staking nodes.

But Cosmos LSD still has extremely great prospects.

Cosmos 2.0: Inter-chain security will promote ATOM to serve as a security token for other IBC chains, enhancing the composability of ATOM through inter-chain accounts. The Cosmos team will soon support liquid staking functionality, thereby improving the liquidity of ATOM. The value of ATOM will further increase, directly impacting the prosperity of DeFi within the ecosystem.

Osmosis and Kava's DeFi are already working hard to develop, and they will build more lending and yield infrastructure for LSD. For example, SiennaLend accepts seSCRT as collateral. New LSD protocols like Quicksilver will attract more holders' attention through airdrops.

Stride and Quicksilver can provide governance functions such as proxy voting. Previously, voting was done by delegated nodes, but now it can be done directly through delegating to LSD, allowing LSD to tally the choices of stakers for proxy voting.

Liquidity benefits: The 21-day unlocking time for staking can achieve capital efficiency through LSD.

External factors: The LSD War brought about by Ethereum's Shanghai upgrade will directly promote the influence of LSD and indirectly drive the development of Cosmos LSD.

Cosmos is preparing to launch a liquid staking model (LSM).

However, there is a problem that LSD may not be able to solve. Taking QuickSilver as an example, QuickSilver's staking mechanism allows users to choose their own staking nodes for staking, and after staking, they receive qAssets. In this process, QuickSilver acts as an "intermediary" representing the user's delegation. Although theoretically, the "intermediary" represents the validators to whom users stake, it directly stakes to the nodes, which meets the conditions for project airdrops in the ecosystem. However, many airdrops have staking limits. For example, during the Stride airdrop claim, the maximum effective staking limit is 4200 ATOM, which means that even if QuickSilver can proxy claim airdrops, it can only claim a share of 4200 ATOM. Perhaps it can be designed with multiple accounts, but this is just speculation; the data risks and technical costs of managing separate accounts are currently unknown. Alternatively, LSD could proactively contact project parties for quotas, but this is also just speculation; projects are unlikely to give you quotas for no reason unless you can bring them benefits.

If you want to learn more about the technical differences among various staking protocols in the Cosmos ecosystem, please visit here.

If you want to learn about the history of Cosmos LSD development, please visit here.

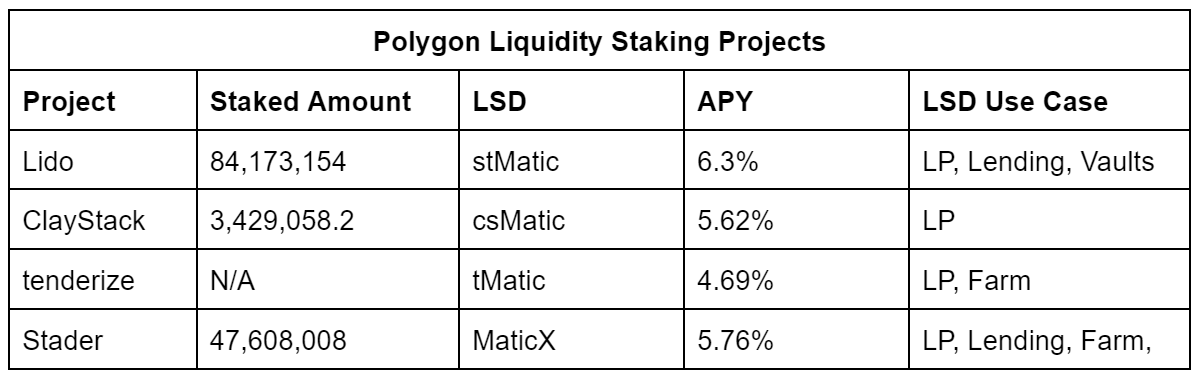

Polygon

The staking rate of Polygon is 39.92%, with an average annualized yield of 8.82%. Polygon POS is an EVM-compatible sidechain, where Matic acts as gas and is staked to nodes to complete POS consensus. 12% of Matic will be used as staking rewards.

An interesting point is that Lido on Polygon actually has the highest APY, and when I searched for MATIC trading pairs on DeFillama, among the trading pairs with TVL over $10M, stMatic is involved in four of them. The direct consequence of this influence may be that Lido is currently and will continue to dominate the Polygon LSD space.

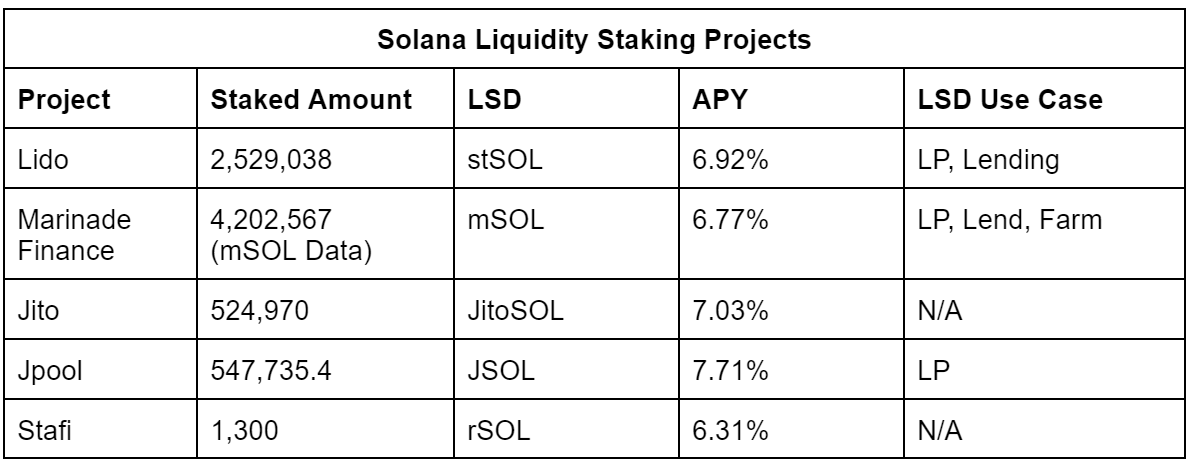

Solana

The network staking rate of Solana is 70.75%, with an average staking annualized yield of 70.75%. Solana has 3165 validators, and the validator with the most delegations only accounts for 2.86% of the total staking amount.

During the statistics process, LSD projects like aSOL, Eversol, Socean, etc., have seen their TVL decline since May 2022, and now their Twitter accounts have been deactivated and cannot be found, the outcome is lamentable. New entrants like Stader may bring new developments to Solana LSD.

Cardano

Cardano currently has a staking rate of 68.73%, with an average annualized yield of 3.26%. This is a decrease of 7.1% from when I published my last Cardano ecosystem report (December 18: 74.05%). However, the TVL in ADA terms is about to break the previous high.

The special technical architecture of Cardano makes it difficult for LSD to develop in its ecosystem. ADA is not locked for a certain period during staking or needs to be transferred to a mining pool, etc. After users stake to SPO, the SPO cannot access your assets; their fees are deducted from the total rewards generated by the staking pool, which means that Cardano's staking is not only non-custodial but also flexible. Moreover, users can use their assets for payments or in DeFi services while staking, such as using them as collateral for iUSD.

Another point is that Cardano does not have penalties; user assets will not be lost due to improper actions by the SPO. When an SPO makes a mistake, the network will cancel the rewards for that epoch, and repeated mistakes leading to a decrease in rewards will guide users away from such unqualified mining pools. However, the average annualized yield for Cardano operators is 4.99%, about 35% higher than ordinary staking users, which attracts many users to become SPOs directly, and the threshold is relatively low, with currently 3206 staking pools.

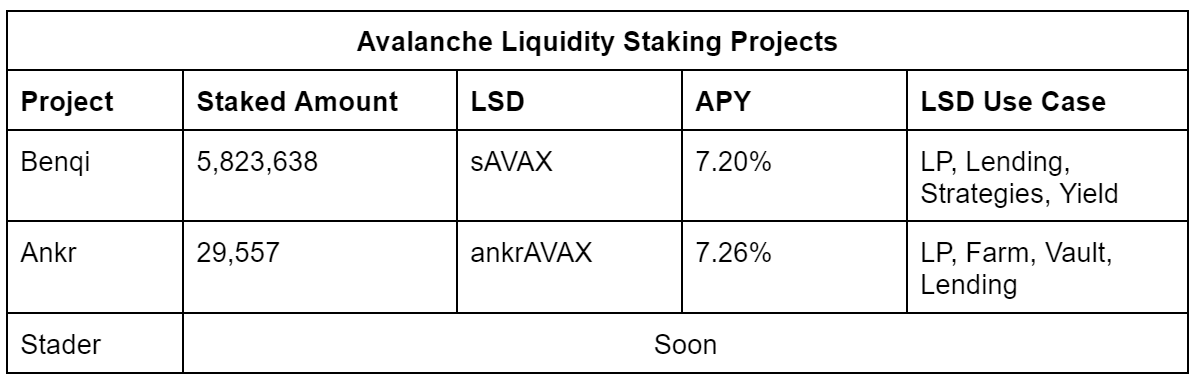

Avalanche

Avalanche's network staking rate is 62.05%, with an average annualized yield of 8.48%. The technical architecture of Avalanche is divided into:

C-Chain (Contract Chain): A smart contract platform for applications.

P-Chain (Platform Chain): Used for staking and delegating AVAX, utilizing UTXO technology.

X-Chain (Transaction Chain): A chain for transferring funds, with fixed transfer fees.

The default way for non-technical users to participate in chain security is through the staking center on Avalanche Wallet, where staking only involves using the P-Chain and locking AVAX. After locking, it takes 21 days to resolve staking. After delegating AVAX, the rewards from validation will accumulate to the P-Chain address you provided. Therefore, LSD projects need to issue synthetic alternative assets using alternative assets on the C-Chain to create staking positions. This presents certain technical difficulties, requiring LSD to design contracts that connect AVAX on the P-Chain with LSD on the C-Chain. Currently, I have only found two LSD projects, with Benqi's sAVAX occupying a leading position.

The leading LSD project Benqi holds 1.7% of the circulating AVAX, and sAVAX has strong liquidity, with many options for lending (circular lending to increase yields), LP, and other DeFi products.

However, Avalanche's DeFi development is relatively good. Excluding $635.75m from Wonderland, the TVL is close to $830.91m, and various DeFi products can be found on Avalanche. The competitive landscape of DeFi on Avalanche has a unique feature: among the top 15 DeFi projects, AAVE, Curve, and Beefy are all entrants, with AAVE directly taking 36.95% of the market share. The native lending project Benqi has developed multiple business scales but is still less than 80% of AAVE, while self-ecosystem projects like GMX and Stargate choose to develop multi-chain, thriving on other chains. For example, GMX is directly a leader on Arbitrum, holding a 32.96% market share, with a significant gap in TVL between GMX and Stargate, where the difference is more than half.

But why is there so little LSD? In addition to technical reasons, this DeFi landscape may also be a contributing factor. Established DeFi projects are busy with multi-chain development, while new multi-chain DeFi projects often focus on single business lines. For them, if they want to expand into new LSD businesses, they mostly start from their native development chains. This may pose difficulties in terms of competitiveness and resource collaboration for new projects that purely focus on LSD.

If you want to learn about Avalanche's specific staking mechanism, please visit here.

Polkadot

Polkadot has a staking rate of 47.05%, with an annualized yield of 15.29%, and a staking lock-in period of 28 days. Polkadot's consensus mechanism is NPOS (Nominated Proof of Stake), which has two roles: validators and nominators. Validators need to run validation nodes, while nominators earn rewards by selecting excellent validators and staking DOT to support their work while protecting the network. If the nominated validator follows network rules and maintains network security, nominators can share the staking rewards they generate. Conversely, if validators behave improperly, they will be penalized, and users will also lose DOT rewards.

Another feature of Polkadot is its slot auction mechanism: it allows multiple specialized blockchains to communicate with each other in a secure, trustless environment, thus achieving blockchain scalability. Parachains are connected to the relay chain, which requires parachain slots. Simply put, the relay chain is the socket, and parachains are the appliances. The number of socket holes is limited and needs to be competed for through auctions, so projects invent crowdloans (Crowdloan, PLO), where project parties raise funds from the market to participate in the auction and receive project token rewards upon success. However, projects that do not participate in the auction can also use the Parathread mechanism, which differs from parachains in that it requires payment based on usage, while parachains are free to use indefinitely. The following are some examples of PLO; due to the existence of crowdloans, the attractiveness of LSD in terms of yield is somewhat insufficient, and many DeFi projects are built around PLO.

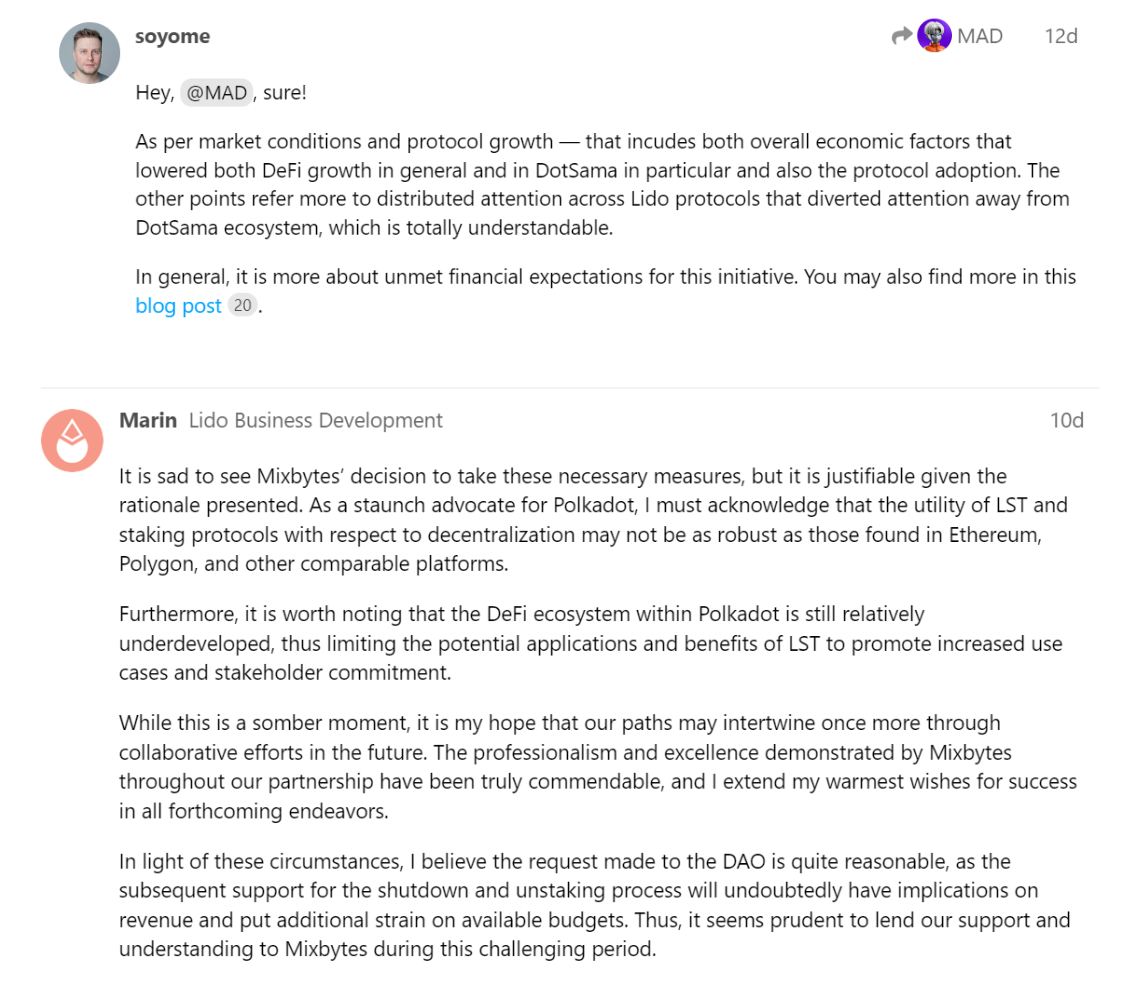

On March 15, Lido officially suspended staking deposits for Polkadot and KSM. I reviewed the proposal at that time, and the comments from the proposal initiators soyome (head of Lido partner MixBytes) and Marin (Lido's BD) are as follows:

The general idea is that the DeFi ecosystem within Polkadot is still relatively underdeveloped, limiting the potential applications and benefits of LSD, along with some market and operational issues. Because the Polkadot ecosystem is quite complex, I only conducted a brief study on it without delving deeply into the reasons for its ecological development. However, during my research, many articles about Polkadot and crowdloans were published in 2021 and 2022, and there are indeed very few recent articles. The report published by Messari, “State of Polkadot Q4 2022”, may provide us with some answers.

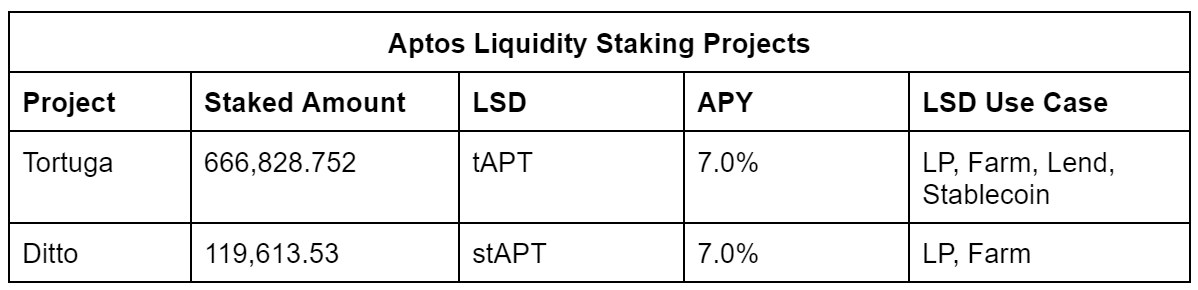

Aptos

According to data from Aptos Explorer, the staking amount of Aptos nodes accounts for 82.5% of the $APT supply, with miners' average annualized yield around 7%. During the investigation, we actually found many Aptos-related LSD projects, but most of them stopped updating their Twitter accounts after October 2022, and their project websites are currently inaccessible. Moreover, the current TVL of Aptos DeFi is only $37M, and the corresponding foundational LSD protocols are even fewer. From the LP pools of Pancake and Liquid Swap, the highest APY for one pool can reach 10%+ (whUSDC-tAPT LP), while the rest are below 2.78%. However, the number of holders for tAPT and stAPT has reached 45.2K and 29.9K respectively, which is far higher than other ecosystems of similar scale LSD.

Theoretically, Aptos and Sui both belong to the Move ecosystem, and if the LSD protocol can manage APT, it can also manage SUI. The Sui mainnet will launch in Q2; will this promote the development of DeFi in the Move ecosystem, thereby creating more infrastructure and use cases for LSD? This is worth looking forward to.

Conclusion

From the multi-chain planning of LSD projects like Lido, Stader, Bifrost, it can be seen that the multi-chain nature of LSD business is an inevitable trend. As long as there is a POS mechanism, LSD can theoretically be created from a staking perspective. However, from the cases of these projects above, the vast majority of LSD projects should start from a certain chain or ecosystem before expanding to other public chains.

Operational issues: During the data organization process, many LSD projects have very poor UI experiences. Additionally, many projects have numerous use cases for their LSD but do not inform users how to use them, resulting in an overall poor UX experience.

CEX is a factor that cannot be ignored. As the largest traffic entry point for Web3 and a gathering place for various tokens, taking Coinbase as an example, the trading volume brought by just CBETH-ETH reaches as high as $8.4M. Besides liquidity, this will also affect token speculators' attention to the LSD track.

The suspension of some LSD protocols after the launch of the Aptos mainnet has also reminded us to pay attention to the upcoming LSD protocols in new L1s/L2s ecosystems, choosing projects that can sustain operations to invest our assets.

Recently, with the launch of FVM, LSD solutions such as SFT, MFIL, STFIL, HashMix are already prepared to go live. LSD has become an essential DeFi protocol for public chains.

Earning rewards through LSD or accessing LSD Pools and LSD DeFi products can provide real yields. For comprehensive DeFi, the LSD business may become a new growth point for the income of old DeFi.

MetaMask announced the opening of Ethereum staking functionality in January, which is currently in beta testing. In Cosmos, the Keplr wallet serves as an entry point for many people to stake assets, and there are similar wallet entries for staking SPO on Cardano. The BD of LSDFi projects may consider partnering with wallet providers.

Discussion (Subjective Opinion Area)

Regardless of the various analyses I have done before, they are based on one point: will holders pursue stability and high returns? But one point has been overlooked: the correctness of staking, participation in governance, and maintaining network security. The main purpose of POS or modified POS mechanisms is to maintain network security. However, in reality, the decentralization of nodes and the basic distribution of tokens have already been determined during the initial fundraising phase and the testnet stage of most public chains. Next is governance; the proxy voting solutions of Cosmos's Stride and Quicksilver are good examples of earning rewards while participating in governance.

Is it necessary for LSD to combine to earn rewards? I cannot answer directly, but I thought of two cases:

① In some small countries in Africa with underdeveloped financial facilities, you should worry about currency inflation issues, but if you are on Wall Street, you would think more about creating higher financial tools and products.

② There are many tokens in the market with negligible utility, which can be calculated to exceed a scale of around hundreds of billions. However, LSD is backed by ETH, the second most valuable currency in the crypto world, which can support the development of more products in terms of both actual value and stability. What reason is there to give up this vast market for LSD? Currently, even in a bear market, ETH's FDV exceeds $200 billion; how large is the imagination space for LSD?

③ Is LSD necessary for other chains? Yes, LSD can promote network staking in an ecosystem, enhance network security, and provide liquidity for DeFi, thereby promoting the development of DeFi within the ecosystem.

The biggest influencers in the LSD war may be node operators and CEX. Lido, as the largest LSD leader, holds only 4.87% of the ETH ecosystem, while in some ecosystems, such as Cosmos's $ATOM, large operators may delegate over 4.4% (stake.fish) of ATOM, and the holdings of nodes like Binance and Kraken far exceed those of LSD projects. The VC-owned nodes marked in the circles in the image below may also become influencing factors in the LSD War.

Can non-POS network native assets do LSD? I haven't found suitable cases, but one idea is that without the need to maintain network security, governance rights could be designed. After token locking, it could become xToken, representing the right to redeem assets after a certain period, and could also be tied to governance. If this protocol decides on profit distribution through governance, then products could be developed based on xToken to determine yields, etc.

References: Staking situation: Staking Rewards, various blockchain explorers Project situation: Defilillam, public chain official websites, Twitter, Google Project data: Data from various project official websites, Coingecko Other reference materials: KOLs Thread, various blogs and articles DM channel: Twitter @Wayne24698337