7 O'Clock Capital: Why Halving Leads to Price Increases

7 O'Clock Capital has compiled eight major tokens that are set to halve or produce in 2023-2024 for the reference of miners and investors.

7 O'Clock Capital has compiled eight major tokens that are set to halve or produce in 2023-2024 for the reference of miners and investors.Author: 7 O'Clock Capital

Introduction

At the beginning of 2023, BTC embarked on a new journey, and the market began to awaken, with various sectors rising in turn. Among them, the Ethereum Shanghai upgrade remains the main narrative line of the year, continuing to generate heat. The application of AI technology, being in its nascent stage, has gradually receded after a short-term speculative frenzy. Now, after BTC has broken through $25,000, it has started to consolidate and adjust. Following the speculative activities across various sectors, attention is gradually shifting towards the upcoming halving events for DASH and LTC, as each halving tends to disrupt the supply-demand balance, coupled with market speculation, leading to significant price fluctuations.

Looking at the historical price movements surrounding halving events, Bitcoin garners the most attention. Although there are other PoW tokens, they generally follow BTC's trend and do not exhibit independent market movements. 7 O'Clock Capital has compiled eight major tokens that are set to halve between 2023 and 2024 for miners and investors to reference.

Table of Contents

Why Halving Leads to Price Increases

Halving Timeline and Market Changes Before and After

Conclusion

1. Why Halving Leads to Price Increases

Halving is a clever design in economic models, primarily aimed at avoiding inflation issues by controlling supply to favor price increases. From a supply perspective, halving disrupts the dynamic balance of output; when the supply is halved and demand increases, the market overall tends to be bullish, thus halving is seen as a positive catalyst for market sentiment. However, the price increase solely due to changes in supply is superficial, and there are two underlying reasons:

Halving brings at least a 1x expectation to the market, as pre-halving speculation inevitably drives market sentiment, attracting retail investors and pushing prices up.

Halving is crucial for miners, mining pools, and mining machine manufacturers, as it occurs in PoW tokens, meaning that mining rewards decrease and mining costs significantly increase, theoretically driving prices up. However, this also brings direct negative impacts; if profits decrease, some miners may exit or switch to mining other mainstream tokens.

In summary, it is widely believed that a price increase before halving is a relatively clear feast.

2. Halving Timeline and Market Changes Before and After

Halving inevitably brings market volatility, but what is more worth analyzing is the core groups behind halving tokens. This allows us to concentrate funds on more promising projects among various choices. The following will analyze historical market changes in this manner and extract referenceable patterns:

BTC ------ Miners, institutions/capital, OGs;

LTC ------ Miners, institutions/capital, OGs, but overall core group strength is less than BTC;

BCH, BSV ------ Miners, speculative funds;

ZEC, ZEN, DASH, ETC ------ Anonymous traders (lower market cap, gradually being phased out by the market).

For halving tokens, we need to analyze not only the core user groups but also their narratives. Price increases primarily rely on large capital inflows and high certainty trades. If a project lacks a good narrative, even if a price increase occurs, users will find it difficult to determine the expected timing for entry and exit. Through the following data analysis, we can preemptively position funds.

(1) Halving Countdown

(2) Impact of Halving on Prices

1. BTC Halving Market

Summary

(1) The Bitcoin halving cycle occurs approximately every four years, where Bitcoin's output is halved. The halving interval is based on every 210,000 blocks, at which point the block reward is halved.

(2) Historically, Bitcoin has experienced three block reward halvings (the K-line displayed by AIcoin is from after 2017, so the following will narrate market changes in text):

In November 2012, Bitcoin's block reward was halved for the first time, and a year later, Bitcoin's price broke through $1,000, setting a historical high;

In July 2016, Bitcoin's block reward was halved for the second time, and in the following year (2017), Bitcoin's price soared, eventually breaking nearly $20,000;

In May 2020, Bitcoin's third halving occurred, with price increases reaching historical highs during the bull market.

Data analysis after halving indicates that the multiple increase from the early stages of the bull market to the peak has been decreasing, with the volume of funds increasing. The driving force of the bull market requires more capital inflow, transitioning from retail-driven markets to institutional-driven markets, making it increasingly difficult for retail investors to profit.

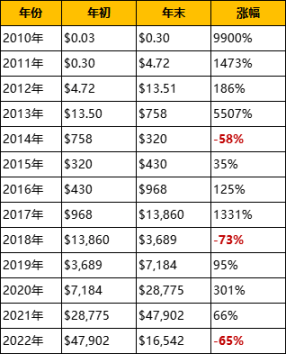

(3) Based on price analysis at the beginning of the bull market, the next bull market's initial price is more than double the previous bear market's low, thus it can be roughly predicted that the initial price of the next bull market will not be lower than $30,000, and the maximum will not be lower than $120,000. Therefore, the current price of $16,000 is relatively reasonable and low, and gradual accumulation can be considered.

(4) Historical data collection and analysis show that 2014, 2018, and 2022 were years that initiated bear markets with continuous declines; 2016, 2020, and 2024 are years of Bitcoin halving, marking the beginning of bull markets; 2017, 2021, and 2025 are all years during bull markets, where prices will reach new highs again.

(5) The following is a comparison of BTC's prices at the beginning and end of the year from 2010 to 2022. Based on the price performance of BTC over the past 12 years, with a four-year market cycle, the next upward trend may gradually begin.

2. LTC Halving Market

Summary

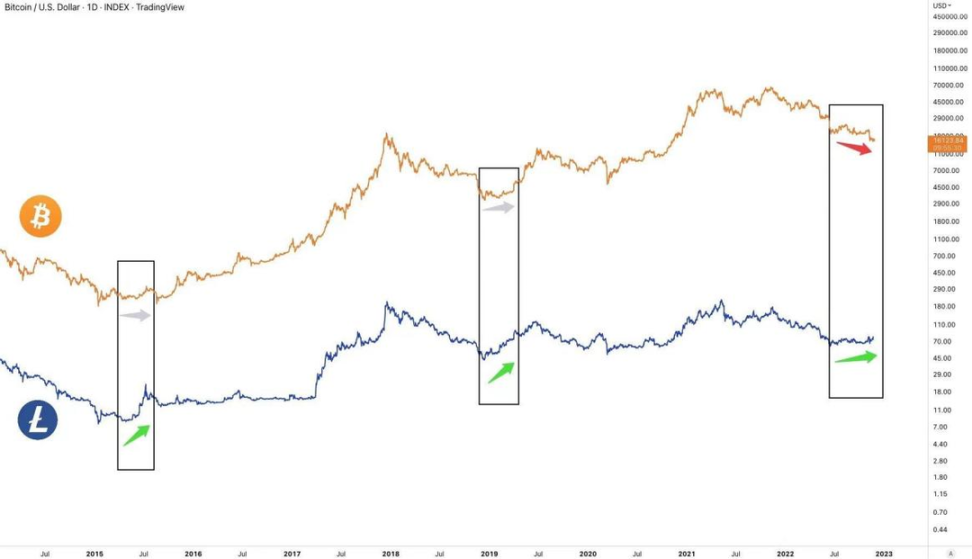

(1) Since its launch in October 2011, LTC has undergone two halvings. The above chart shows that LTC's market started three months in advance in 2015 and six months in advance in 2019, indicating that the speculation expectation for halving begins 3-6 months prior. The halving opportunities for LTC differ from those of BTC; after BTC's three halvings, a bull market is inevitable, while LTC's halving only has speculation expectations before it, with the market ending nearly two months before the halving.

(2) From the K-line chart, it can be seen that LTC has been hovering around the price of 55-60 for nearly half a year, with a solid bottom structure, making it the best buying point. Looking back now, with market speculation and the early 2023 market, it has nearly doubled. Compared to the last halving, LTC rose directly from $22 in December 2018 to $146 in June 2019, increasing by more than six times, and it is expected that there is still 2-3 times of space before the market ends in June 2023.

(3) Based on the comparison of LTC and BTC trends, it can be predicted that LTC will reach a peak around June 15, 2023, about 40 days before the halving:

In 2013, LTC peaked at $53.15 on November 28, while BTC peaked at $1,156.12 on December 4; in 2015, both LTC and BTC reached their lowest points on January 14, 2014, with LTC at $1.11 and BTC at $171.51. The interval between LTC's peak and low was 408 days, and on July 10, 2015, LTC reached a short-term peak, with an interval of 177 days from the previous low on January 14, with 47 days remaining until the halving on August 26. At this time, BTC's market was still oscillating at the bottom without a price increase.

On December 19, 2017, LTC peaked at $375.29, while BTC peaked at $20,089 on December 17; on December 7, 2018, LTC reached its lowest point at $23, while BTC reached its lowest point at $3,191 on December 15. The interval between LTC's peak and bottom was 353 days, and by June 22, 2019, LTC reached a short-term peak, with an interval of 197 days from the previous low on December 7, with 44 days remaining until the second halving.

On May 10, 2021, LTC peaked at $413, while BTC peaked at $67,549 on November 9; on June 14, 2022, LTC reached its lowest point at $40, while BTC reached its lowest point at $15,476 on November 21. The interval between LTC's peak and bottom was 400 days.

Thus, it can be concluded:

In 2015, the interval between the peak and low was 408 days, and the interval to the short-term peak was 177 days, with 47 days remaining until the halving.

In 2019, the interval between the peak and low was 353 days, the interval to the short-term peak was 197 days, with 44 days remaining until the halving.

In 2023, the interval between the peak and low is about 400 days, and it is expected to reach a short-term peak around June 15, 2023, with 40 days remaining until the halving.

(4) The following chart shows that in every bear market, LTC's performance has outperformed BTC, and after an explosive start, it will show good performance, mainly driven by FOMO sentiment. LTC is a highly controlled project, and at a certain stage, the whales controlling it will need to take profits. Additionally, LTC is relatively dependent on the overall market recovery for FOMO sentiment to be effectively stimulated, so it is advisable to take profits and set stop-losses.

3. BCH and BSV Halving Market

Summary

(1) On April 8 and April 10, 2020, BCH and BSV completed their first halving, reducing the block reward from 12.5 BCH to 6.25 BCH.

(2) BSV and BCH are quite similar, both ending their halving markets two months in advance.

(3) BCH and BSV have only one halving history, and there are currently no good patterns to refer to. However, as forked tokens, they lack a complete ecosystem and demand, so their future upside potential is limited. Moreover, in the past few years, BCH and BSV have been eliminated from the top 10 market cap rankings.

4. ZEC Halving Market

Summary

(1) From the beginning of 2020 to the halving period, ZEC's maximum increase reached 501.17%. Among privacy tokens, its overall increase was relatively good. However, in the three months leading up to the halving, ZEC fell by 39.47%. In the past week and the last 24 hours, ZEC has only followed the overall market and has not shown its independent market trend. In summary, after the halving, ZEC's price did not show a significant upward trend until six months later, during the bull market in May 2021, when it reached a peak of $371.

(2) From the chart below, it can be seen that most of ZEC's increase was concentrated in January, when the halving concept was hot. Although there was also a significant increase in April, it was mainly due to the rebound from the March 12 crash. Additionally, ZEC reached a new high before the halving in August of the same year, also influenced by the positive market conditions.

(3) Whether ZEC can achieve new breakthroughs in the future depends on its ability to successfully integrate into the DeFi ecosystem and develop corresponding applications. This way, in the next bull market, ZEC's value and position in the privacy sector can be enhanced. Currently, the main trends in the market are DeFi, Web3, and the Metaverse. The total market cap ranking of anonymous tokens has started to decline in the past two years, with only Monero remaining among the top three anonymous tokens, while the other two have fallen outside the top 50. Although privacy is a necessity in the future, it may serve as a function to empower public chains. Based on current analysis, it is difficult for the privacy sector to see another explosion in the next 2-3 years.

5. ZEN Halving Market

Summary

(1) The above data shows that ZEN's performance in the month of halving is poor. The price increase in the five months leading up to the halving did not fluctuate much. After the halving, ZEN began to rise along with BTC's upward trend, reaching a new high of $169 on May 8, 2021, nearly six months after the halving was completed, and has not broken a new high since then.

(2) ZEN's market trend follows BTC's trend and has not shown its independent market trend. Currently, it is the lowest-ranked project by market cap among halving tokens. Although ZEN has backing from Grayscale and has many traditional partners in its ecosystem, based on halving market analysis, the opportunities appear limited. With the development of Web3, there may be continued growth, which remains to be seen.

6. DASH Halving Market

Summary

(1) DASH undergoes a halving every year, with a reduction of 7.14%. The first halving saw a peak within five months before the halving, with an increase of 232.06%, and its trend was consistent with BTC's market fluctuations, not showing an independent market trend. After reaching the peak, it began to fluctuate and decline.

(2) The second halving occurred on March 23, 2022, with a drop from a high of $138 to a low of $45 (on May 12), nearly a threefold decrease, and it has fallen more than ten times from the high of $478 in 2021. Two weeks before the halving, DASH's price reached the lows of 2018 and 2019, and began to decline after the halving. On November 9, 2022, DASH fell to a low of $30, and by December 13, it surged to $50, nearly doubling in a month. At the beginning of 2023, with BTC's rise, DASH broke through $77.9, currently retracing around $71. If BTC does not experience a significant drop, it is likely to continue rising.

(3) During the sideways period in 2022, DASH's accumulation cost was around $38-$50, and it has already risen about 35%. Users who are optimistic can gradually accumulate, expecting around 2x returns.

7. ETC Halving Market

Summary

(1) Currently, ETC has completed three halvings, with each halving reducing the reward by 20%. The first halving began its upward trend from the bottom on November 3, 2017, reaching a peak on December 20; before the second halving, the crypto asset market experienced the "March 12" crash, with ETC dropping from a high of $13.2 to a low of $3.1 within 40 days before the halving, a decline of -329.97%; the third halving occurred on April 25, 2022, during which ETC rose from $25.6 to a peak of $52.66 between March 16 and 29, achieving a 105.7% increase, becoming one of the few standout projects at that time. The upcoming halving is clearly a catalyst for this rise. Overall, ETC has had a wave of market activity 30-40 days before each halving.

(2) Whether it is the migration of consensus mechanisms, the carrying of computing power, or halving, these are just steps in ETC's development process and do not fully promote its better development, especially as new public chain ecosystems and practical applications emerge. ETC's development still needs to be improved.

3. Conclusion

Halving events that occur every four years seem to have a stronger explosive potential than annual reductions. Based on the halving timeline, next year will officially kick off the halving drama, with LTC and DASH being the first coins to position. However, the maximum profit potential should be with LTC. Although DASH will begin its reduction first, the proportion of reduction is relatively low, and its impact is not particularly significant. Moreover, the current environment is a bear market nearing the bottom. LTC is a halving event, while DASH is a reduction; comparatively, LTC has a higher speculative consensus heat. The last LTC halving saw an increase of about six times. If one missed the speculation in November last year, the next two months will be a suitable time for positioning.

Based on the pattern of BTC's halving leading to the start of a bull market, it can be predicted that 2024 will be the real bull market, specifically on May 2, 2024. Additionally, there will be positive news from BCH and BSV's halving in April 2024. However, the halving times for these three tokens are too close, making it difficult for funds to concentrate on speculation. ZEC and ZEN face similar situations, while ETC's halving time has no competitors, leaving some room for imagination.

Halving/reduction cannot actually save prices; it requires favorable news, along with the overall market conditions and sufficient narratives.