Messari: Frequent heavy-handed actions, SEC regulatory measures will continue to impact the volatility of digital assets

As cryptocurrency companies and regulators battle it out in court, these actions may lead to long-term volatility in digital assets.

As cryptocurrency companies and regulators battle it out in court, these actions may lead to long-term volatility in digital assets.Original Title: Regulation by Enforcement Continues to be the SEC Strategy for Crypto

Original Authors: Tom Dunleavy, Chris Collar, messari

Compiled by: BlockTurbo

Key Points

- Without digital asset legislation, the U.S. Securities and Exchange Commission continues to regulate through enforcement;

- Economic data continues to indicate more persistent inflationary pressures than the Federal Reserve would like. It is now almost certain that there will be two more rate hikes in the first half of 2022;

- Silvergate has attracted interest from many notable buyers, despite being the most shorted stock in the U.S. stock market.

SEC Continues to Regulate Through Enforcement in the Absence of Digital Asset Legislation

Last week, the U.S. Securities and Exchange Commission (SEC) took two significant actions related to digital assets. These actions followed last month’s allegations against Genesis and Gemini for offering and selling crypto asset securities through the unregistered Gemini Earn lending program.

The first action occurred on February 9, when the SEC continued to regulate through enforcement in the absence of digital asset legislation, charging Payward Ventures, Inc. and Payward Trading Ltd. (both commonly known as Kraken) for "failing to register their crypto asset staking-as-a-service offerings and sales." The Kraken entities settled with the SEC for $30 million and immediately ceased offering or selling securities through their crypto asset staking services or staking programs in the U.S. Additionally, without admitting or denying the allegations in the SEC complaint, Kraken agreed to permanently cease staking operations in the U.S.

The announcement prompted several responses from industry leaders and the SEC. The first came from SEC Commissioner Hester Peirce, who opposed her organization’s decision. Peirce claimed that registration is impossible and that "products related to cryptocurrencies are difficult to navigate through the SEC’s registration channels." Furthermore, she suggested that there is currently insufficient guidance for companies like Kraken to make informed decisions regarding registration.

Industry leaders subsequently responded. Coinbase CEO Brian Armstrong and its Chief Legal Officer Paul Grewal, along with Kraken Chairman Jesse Powell, expressed agreement with Peirce’s dissent on Twitter. They responded that there is currently no way to register such programs.

The next day, on February 10, Coinbase supported its executives' statements. Coinbase issued an official statement written by Paul Grewal, stating that staking is not a security under the Securities Act of 1933 and the Howey test. The exchange added that securities laws would prevent U.S. consumers from accessing basic crypto services and force them to use offshore platforms. On Twitter, Brian Armstrong added that the company would be happy to defend Coinbase staking in court.

On the same day, SEC Chairman Gary Gensler gave interviews to Bloomberg and CNBC to clarify the regulator's decisions. In Kraken's case, Gensler explained that Kraken had not disclosed information that would allow the public investors to understand how the company handled token deposits. More broadly, he stated that exchanges and platforms are generally non-compliant and need to differentiate business functions and register separately. He added that there is sufficient guidance, forms, and staff support to help companies register and draft disclosure information.

When Bloomberg's David Westin asked if there would be further actions, Gensler responded, "It doesn’t matter what you call it—earn, lend, staking-as-a-service, yield—labels don’t matter, economics do. The investing public is putting their hard-earned money into a platform and getting these yields; the law requires them to disclose, and the company needs to register."

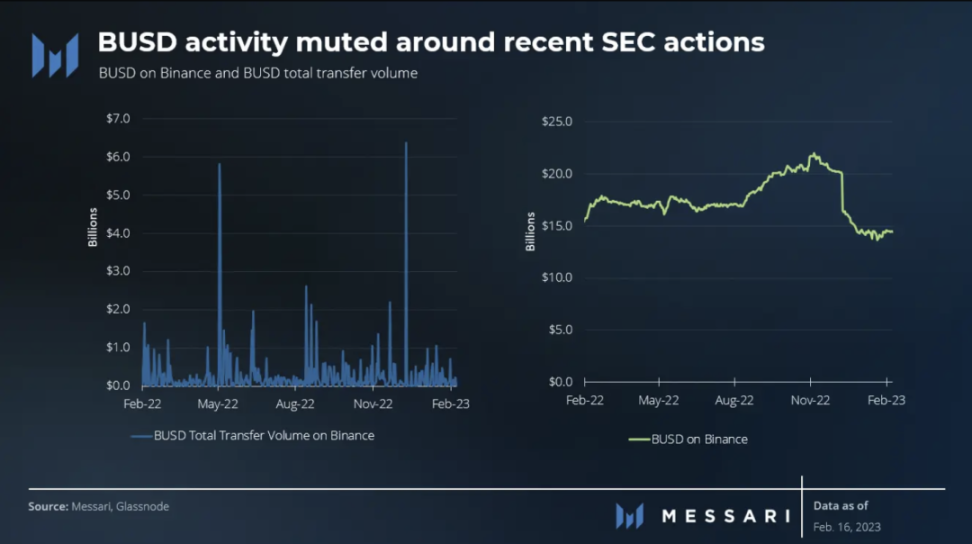

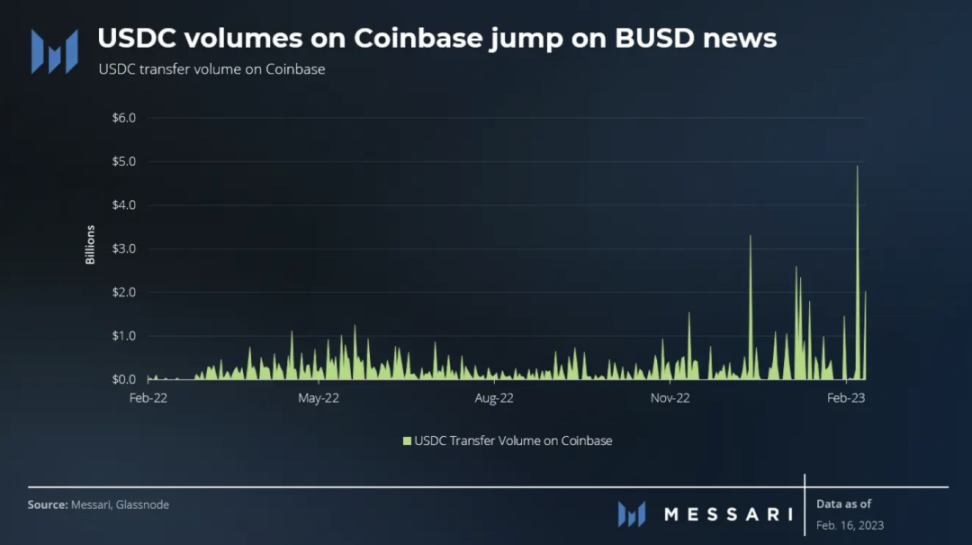

The second action occurred on February 12, when The Wall Street Journal reported that SEC enforcement officials had sent a notice to Wells Trust Co, indicating that the regulator planned to sue the company for violating investor protection laws. The letter stated that the stablecoin Binance USD (BUSD), owned and issued by Paxos, is an unregistered security. Notably, the Wells notice is not a definitive sign that the SEC will take enforcement action.

After the SEC threatened legal action, Paxos immediately announced the termination of its relationship with Binance and would stop issuing new BUSD tokens per the instructions of the New York Department of Financial Services (NYDFS), effective February 21. Additionally, the company assured BUSD holders that they could redeem their funds for U.S. dollars or the regulated dollar-backed stablecoin Pax Dollar (USDP) at least until February 2024.

The next day, on February 13, Binance CEO Changpeng Zhao responded that the exchange would continue to support BUSD for the foreseeable future and would begin to adjust its products accordingly, phasing out the use of BUSD. Later that day, Paxos sent a statement to The Block via email, confirming it had received the SEC's notice and stated it "strongly disagrees" with the SEC's assertion, indicating it would "vigorously defend itself in court if necessary" and that "there are no other allegations against Paxos."

Some Insights

The SEC's two actions leave much room for speculation among the public. However, some first-order effects can be reasonably inferred from the statements of all parties involved.

First, any centralized or decentralized exchanges and other digital asset businesses engaged in crypto asset interest-bearing accounts, products, or services should anticipate future actions from the SEC. Although the SEC's guidance is broad, vague, and potentially incomplete, its actions have been consistent.

Second, due to litigation and settlements between businesses and regulators, the public investors should expect long-term volatility in digital assets. There is a clear divergence of opinion on whether there are sufficient rules and forms to cooperate with regulators. Additionally, at least verbally, leading industry firms are determined to deal with regulators in court rather than settle outside of court.

Third, any business engaged in the issuance and trading of unregistered stablecoins should anticipate future actions from the SEC. Gensler has made it clear that the SEC views stablecoins as securities, partly because they share similarities with money market accounts and money market mutual funds. However, due to past efforts, such as Circle's attempt to go public last December, some issuers and stablecoins may be further along in compliance than others.

Inflation, Retail, and PPI All Higher Than Expected, Indicating Persistent Inflationary Pressures

It has been a busy week for key macroeconomic data. The highly anticipated inflation data was released on Tuesday. The CPI and core CPI were 6.4% and 5.6%, respectively, exceeding expectations by 0.2% and 0.1%. Both doves and hawks can point to some areas to support their positions. Hawks noted significant increases in household food prices (up 11.3% year-over-year) and double-digit growth in electricity prices. The report also included updated category weights and methodological changes, making it more challenging to draw conclusions from the data.

Later this week, the market saw both retail and producer price index (PPI) figures come in well above expectations. Initial jobless claims were lower than the downward level, indicating that the labor market remains strong despite tightening financial conditions. The stock market fell sharply on the PPI news, while cryptocurrencies continued to hold their gains. By the end of the week, the rationale for the Federal Reserve to raise rates twice more in March and May appeared quite compelling. The market is pricing in an 82% chance of a March rate hike and a 67% chance of a May hike.

Silvergate Capital Stock Continues to Attract Attention from Financial Institutions

It has been a month since we last reported on Silvergate Capital (SI) and its Q4 2022 earnings, as well as the significant ownership acquisitions by Block.one and Brendan Blumer in November 2022. Following the report, SI's stock price surged over 50% amid a series of lawsuits from FTX clients, an alleged fraud investigation by the U.S. Department of Justice, and the departure of Silvergate board member Rebecca Rettig. Despite these headlines and legal hurdles, SI's clients may continue to rely on the world's largest digital asset trading network.

Two weeks ago, MicroStrategy Chairman Michael Saylor told CNBC that the company would remain a client of SI. He stated, "We will continue to do business with Silvergate. The mismanaged institutions collapsed—FTX, Alameda, Voyager, BlockFi. Silvergate is a responsible institution." He added, "I believe they are operating in a responsible manner, and they are good citizens of the ecosystem."

During the same period, investors and financial institutions also seemed to agree with Saylor's viewpoint. Overall, funds and investors are net long on SI stock, despite it recently becoming the most shorted stock with 73% short interest. Since the end of January, market interest in SI has only increased:

- January 31—BlackRock increased its stake from 5.9% to 7.20%;

- February 2—State Street increased its stake from 5.3% to 9.32%;

- February 9—Vanguard increased its stake from 8.59% to 9.47%;

- February 10—Block.one increased its stake from 7.46% to 8.09%;

- February 10—Brendan Blumer increased his stake from 9.27% to 9.90%;

- February 13—Group One Trading holds a 7.27% long position, with 93.64% of that being call options. The company also holds a short position equivalent to 90.73% of its long position;

- February 14—Citadel Securities holds a 5.50% long position, with 92.63% of that being call options. The company also holds a short position that is 77.56% of its long position;

- February 14—Susquehanna Intl holds a 7.5% long position, with 81.81% of that being call options. The company also holds a short position equivalent to 92.93% of its long position;

- February 14—Jane Street Group holds 5.5%. 91.62% of that position is in call options. The company also holds a short position that is 37.65% of its long position;

- February 14—Soros Fund Management holds a short position of 100,000 shares at $17.40 per share.

Earlier this week, as the 13G filings expired, hedge funds like Citadel Securities and Susquehanna Intl made headlines for disclosing ownership of SI stock. However, a closer examination of the 13F filings of the aforementioned hedge funds reveals that the market's reaction was largely exaggerated. While these funds are net long, they also hold significant short positions relative to their long positions. This indicates that these funds are market-making rather than behaving as the headlines would lead the public to believe. Overall, this may suggest that investors can expect a higher degree of volatility in the coming months.

Conclusion

The SEC continues to regulate digital assets through enforcement actions, such as the recent charges against Kraken and potential charges against Paxos. Industry leaders have responded, disagreeing with the SEC's stance, with some willing to challenge it in court. As businesses and regulators battle it out in court, these actions may lead to long-term volatility in digital assets. Regulation remains the biggest risk facing cryptocurrencies.

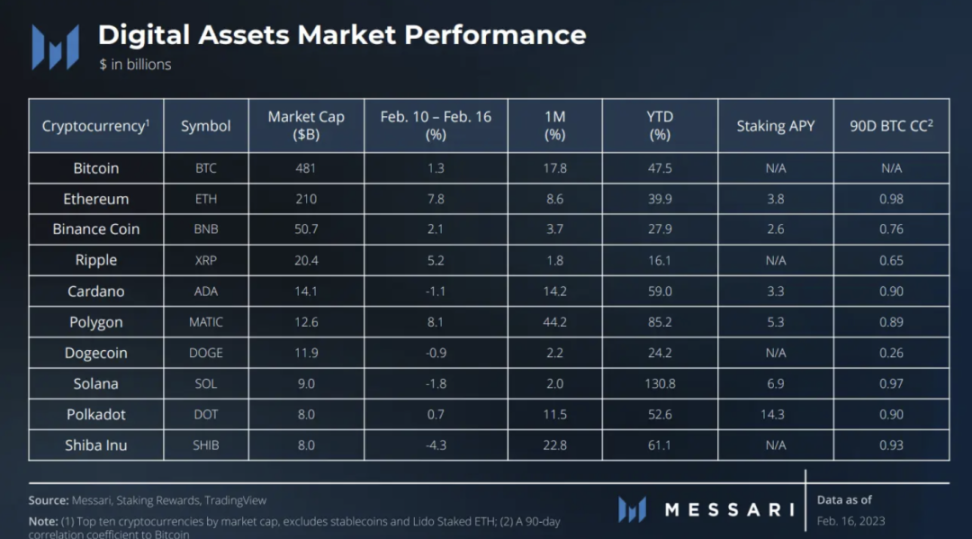

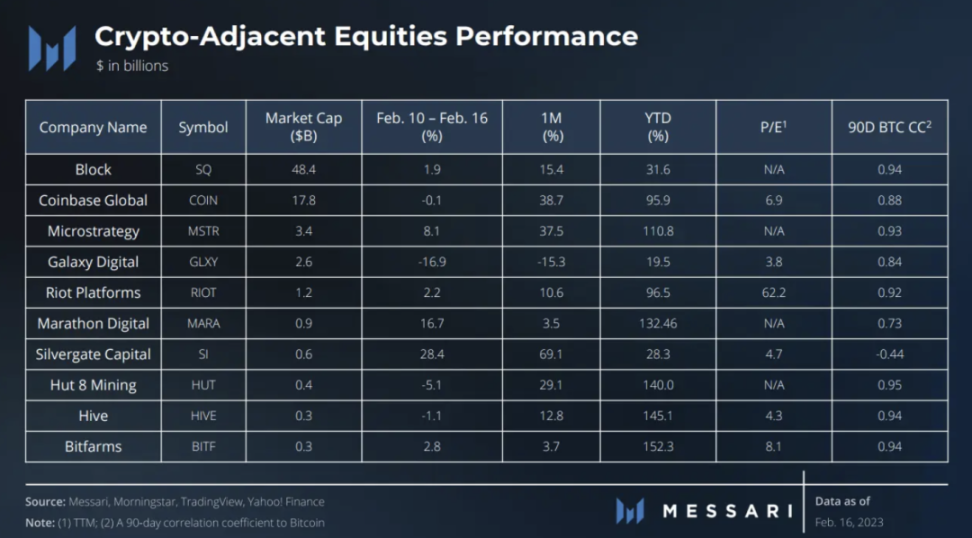

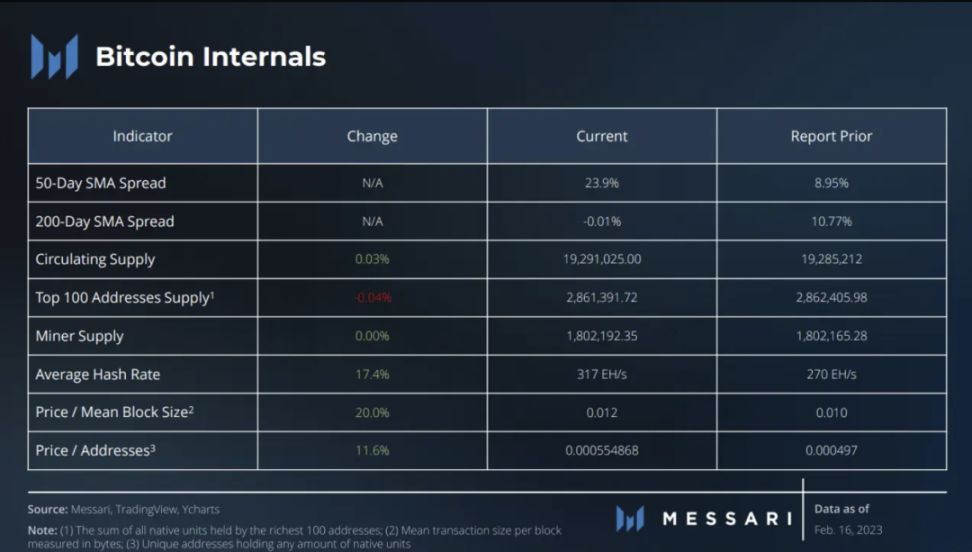

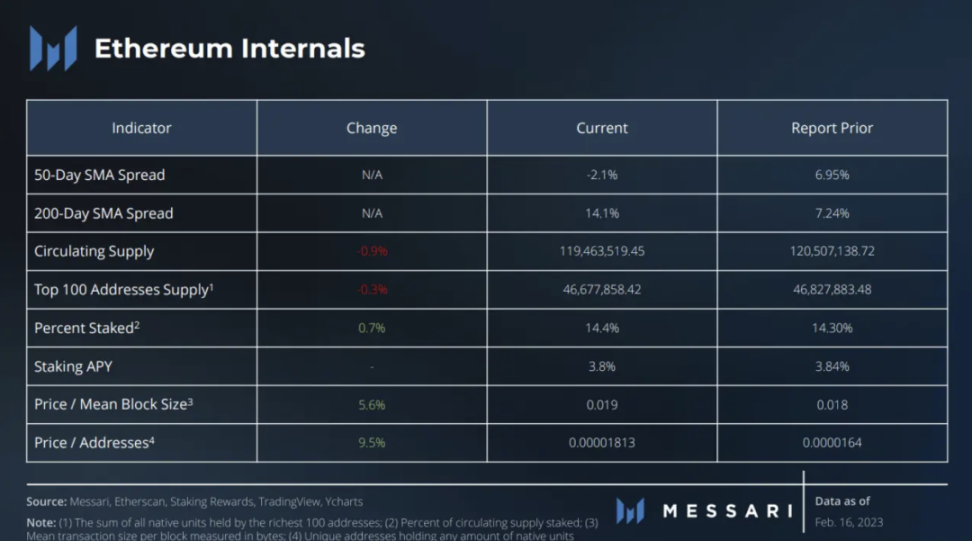

Market Overview