Taking GNS as an example, understanding the DEX PERP track: mechanism, development history, competitive advantages

Rise from the ruins of Luna and soar again.

Rise from the ruins of Luna and soar again.Written by: CapitalismLab

The new versions of GMX and SNX Perp have both drawn inspiration from a project called GNS. Since the Luna crisis last year, GNS has increased more than tenfold, with trading volume and fee income hitting new highs, thanks to its continuous innovation in mechanisms. This article will provide you with a detailed introduction to GNS's mechanisms, development history, and competitive advantages. Understanding GNS can give you insights into many DEX PERP platforms.

This article is relatively complex, so it is recommended to focus on the key points I have extracted while reading.

GNS Mechanism

If you lack a basic understanding of GNS, simply put, it is a decentralized perpetual contract platform:

Oracle pricing, LP and Trader betting against each other.

LP is purely stablecoin, supporting Forex/Stock/Cryptocurrency trading.

Bidirectional funding rates, similar to CEX Perp, where one side pays the other.

On the other hand, you can read my previously written GNS Chinese encyclopedia, as the content outside of LP (DAI Vault) is still meaningful.

The core of the betting model is risk control. We previously discussed that GMX operates on a full collateralization model, meaning that for every 1 ETH long position, there is 1 ETH in spot support for the underlying GLP, allowing GMX to weather the storm during a raging bull market. So how does GNS, which only has stablecoins as its underlying assets, manage risk?

GNS has established a triple mechanism for risk control on both the trading and LP sides, with the core being:

Asset spot liquidity determines on-site trading slippage, preventing price manipulation.

Asset price volatility and long-short ratio determine the cost of holding positions, addressing one-sided market conditions.

Net value model combined with liquidity adjustment and cash flow circulation creates a robust LP.

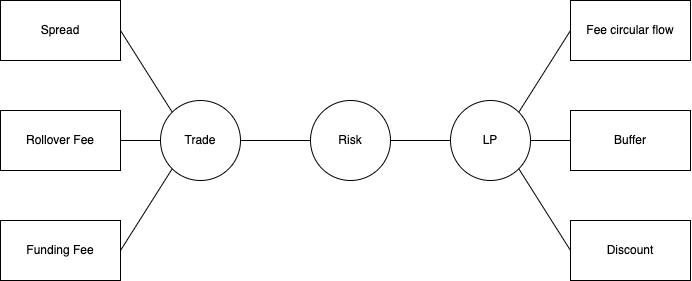

GNS uses a triple mechanism of Spread, Rollover Fee, and Funding Fee for risk control on the trading side.

Spread: Additional opening costs; the larger the position, the worse the asset liquidity, and the higher the fees. This is used to prevent price attacks and facilitate the listing of small tokens.

Rollover Fee: Priced based on spot volatility, used to control traders' leverage and risk.

Funding Fee: Priced based on the difference between long and short positions and spot volatility; when long/short > 1, longs pay shorts, and vice versa, to balance the long-short ratio and avoid excessive one-sided exposure.

For details, see: gTrade v6.1: In-depth

![]()

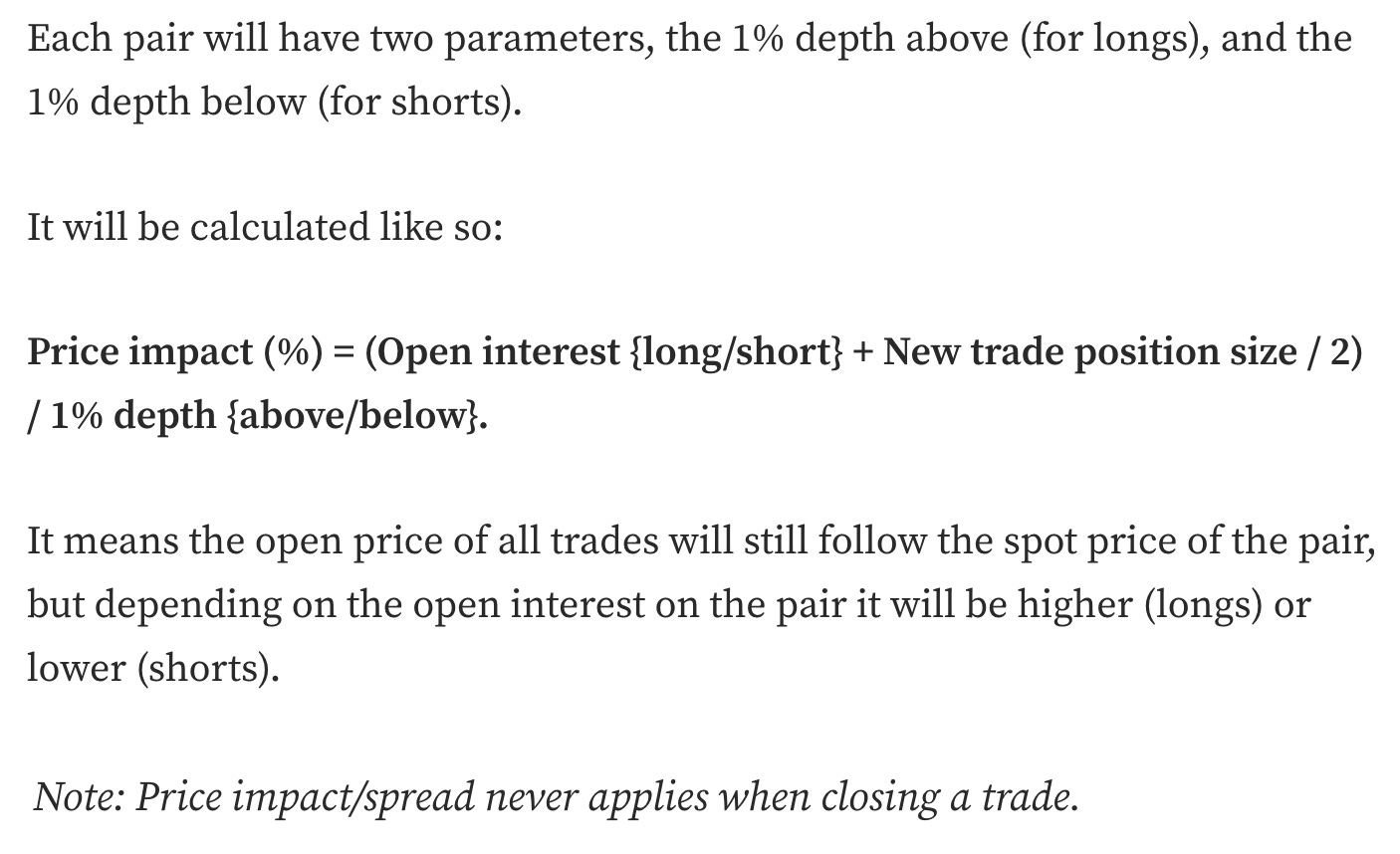

The Spread is the additional slippage incurred when opening a position. For oracle pricing, its slippage should be dynamically adjusted based on the depth of the trading pairs from the oracle source (CEX), ensuring that the cost of manipulating prices off-chain is always higher than the profit made on-chain. Therefore, Spread is positively correlated with the opening size and on-chain open interest, while negatively correlated with off-chain spot depth. The formula is shown in the image below.

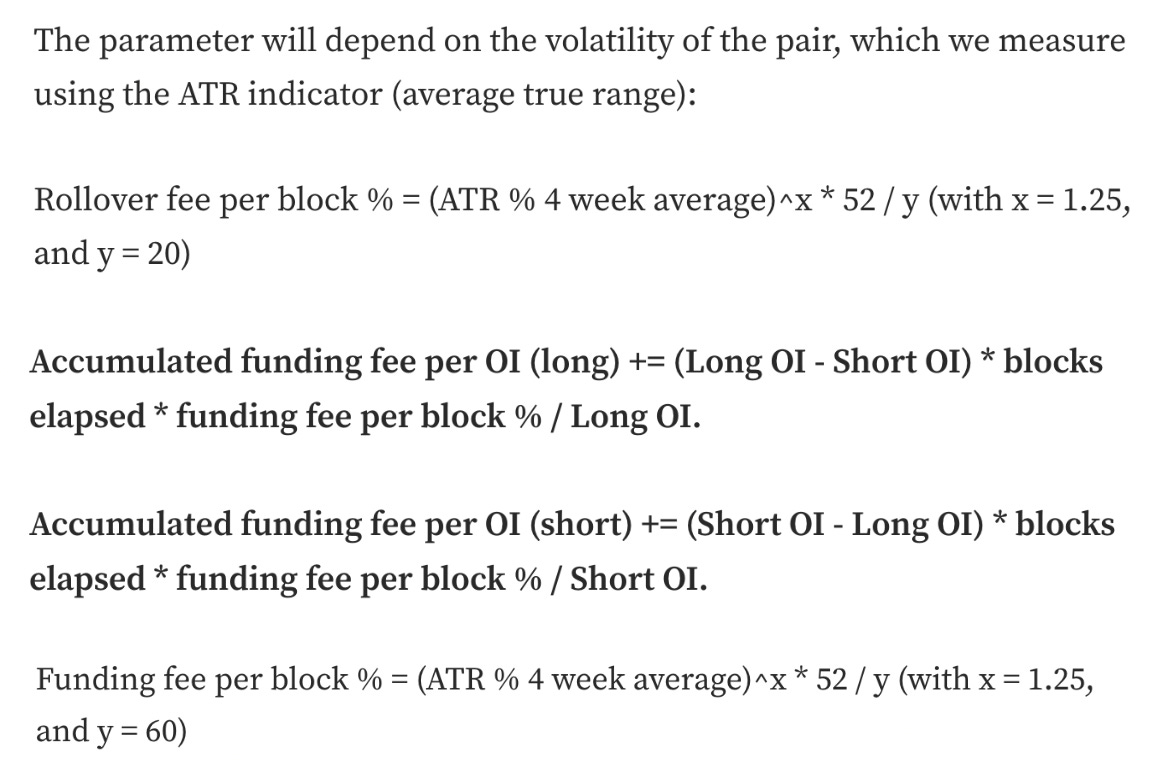

Rollover Fee / Funding Fee are calculated based on recent volatility. Both longs and shorts must pay Rollover Fee, while Funding Fee is determined by the long-short ratio, with one side paying the other. The specific formula is shown in the image below. In a raging bull market, the increase in volatility and long-short ratio will cause the fees paid by longs to rise rapidly, compensating for the losses of the counterparty and controlling the long-short ratio. Of course, this also results in significant trading costs, so in the category of cryptocurrencies that can be used as Index Asset LP, the scale will be less than GMX. However, for stocks/forex, which lack on-chain assets, it has a significant advantage.

The so-called Rollover Fee only applies to the collateral, meaning if you open a $10k position with $1k, you only pay interest on your $1k, while the Funding Fee applies to the position, charging 41% on $10k. For example, in the image below, if you open a short position of $10k BTC with $1k, Funding Fee (s) = -0.0005%, Rollover Fee = 0.0043%. Therefore, the final fee to be paid = ($1k * 0.0043% - $10k * 0.0005%) / $10k = -0.00007%, meaning you can still earn interest when shorting at this point.

On the LP side, gDAI also has a triple mechanism to ensure its robust operation:

A net value product similar to GLP, not principal-protected.

Fee income / Trader profit and loss creates a buffer for gDAI, preventing price drops.

Incentives for long-term locked funds, dynamically adjusting entry and exit times to avoid extreme liquidity issues.

The advantage of a net value product lies in treating all stakers fairly, sharing the burden in extreme situations. The old LP model was supposedly principal-protected, but in a deficit situation, the last one to run away gets nothing, which is similar to what happened with FTX, making panic more likely in a crisis.

The most difficult concept to understand here is the Buffer mechanism. A portion of GNS's fee income will mint new GNS to pay users, while the DAI that was originally income enters gDAI to form an excess collateral Buffer. Trader profits and losses also contribute to the Buffer under excess collateral conditions, which means that although gDAI is nominally not principal-protected, its price will not drop most of the time, showing a deep understanding of the public's "loss aversion" psychology.

GNS also extracts a portion of the profits from Trader losses to repurchase GNS, maintaining the excess collateral ratio within a safe range. This way, in the long run, GNS will not be in a state of continuous issuance.

Long-term locked LP will receive a certain discount, and the source of the discount funds also comes from this Buffer. The so-called dynamic adjustment means that the lower the excess collateral ratio, the slower the withdrawals, increasing risk resistance. Although this approach may seem strange, the rules are publicly transparent in advance.

Yes, you may not have understood the above paragraphs, which is normal; otherwise, how could I call it the most intricately complex system in history? If you really want to understand, you can first read the original gDAI introduction Introducing gToken Vaults. and then come back to the above paragraphs, which I believe will resolve many of your doubts.

Development History

During the collapse caused by Luna, GNS's LP once fell into a deficit stalemate, being forced to sell GNS for DAI to fill the gap. Later, GNS made multiple improvements and performed well during the panic caused by FTX.

In June, shortly after falling into difficulties, the triple risk control mechanisms on the trading side described earlier were fully implemented, allowing it to resume normal operations. In September, it began to capture the trend of the significant depreciation of foreign currencies against the dollar, bringing it back into the public eye. By early December, gDAI reached its limit, and by the end of the month, it was deployed on Arbitrum, leading to explosive growth in both token price and business data at the beginning of this year. The efficient team has allowed GNS to continuously evolve, resulting in such a phoenix-like rebirth.

Competitive Advantages

The core advantage lies in its complex risk control mechanisms, providing a qualified trading venue for Forex/Stock derivatives, where the trading experience on these assets is unparalleled, allowing its products to stand firm. On the other hand, bidirectional funding rates and other factors enable it to achieve differentiated competition with GMX, successfully acquiring some customers in the cryptocurrency space. Achieving this is inseparable from the excellence of the GNS team, which is the most valuable asset of this growing project.

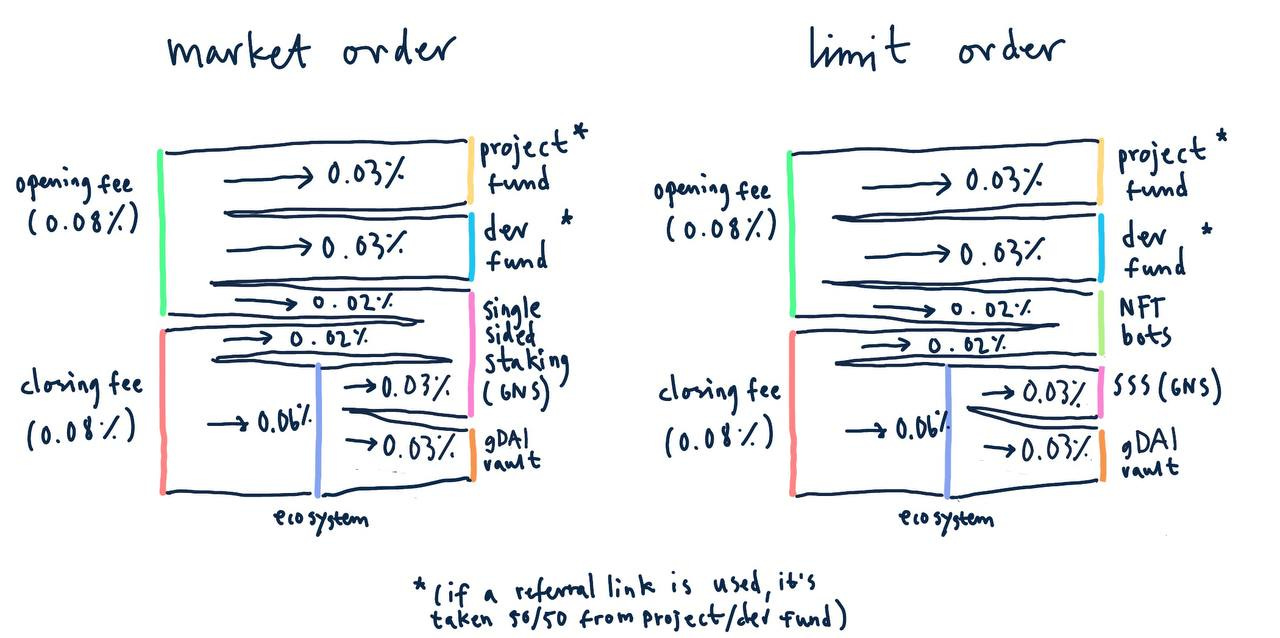

The details of GNS's fee distribution are shown in the image below. Considering that market orders account for about 70%, GNS Staking distribution is approximately 0.07/0.16x70% + 0.03/0.16x70% = 36.25%, while gDAI distribution is approximately 0.03/0.16 = 18.75%. The portion paid to NFT Bots (execution bots) in limit orders is the part that enters the gDAI Buffer mentioned in the previous tweet.

Yes, the proportion of income paid to LP by GNS is remarkably low. So how can it achieve this?

To avoid forks, GNS has audits but has not yet fully open-sourced.

As mentioned in previous tweets, its mechanism is extremely complex and difficult to replicate; if not done well, it can easily fail.

The non-full collateralization model of LP allows it to operate with high capital efficiency.

Although GNS appears to allocate a large portion of income to the team, in reality, most projects today, such as UNI, Maker, Lido, etc., cannot or can barely cover team expenses with their treasury income, so they still need to continuously sell tokens. In contrast, GNS can sustain itself through income sharing, which is quite commendable, as you cannot expect every team to operate like GMX, a charitable organization.

Summary

By the time you reach this point, you might feel a sense of reflection. In fact, the so-called DEX Perp is far from being as simple as traders and LP being counterparts. It was only when GMX adopted a low-risk Index Asset full collateralization model, combined with its team's excellent attention to detail, that a usable product finally emerged. However, to trade off-chain assets like Forex/Stocks and further expand the market, it is essential to use a synthetic asset model like GNS, and it is only through this iteration that we have finally seen the light of day. Salute to the Builders.