Review the historical data of Binance Launchpad and analyze the long-term holding returns of BNB

Compare the historical assessment of the current Launchpad's yield level, and benchmark the ETH staking return to calculate the long-term holding return rate of BNB in new token offerings.

Compare the historical assessment of the current Launchpad's yield level, and benchmark the ETH staking return to calculate the long-term holding return rate of BNB in new token offerings.Original Title: "Reviewing Binance Launchpad Historical Data, Analyzing Long-Term Returns of BNB"

Original Source: CapitalismLab

Binance Launchpad has recently faced negative reviews, but the sentiment of "we can't afford to neglect education" still reflects the warmth and positivity that Launchpad brings to the crypto community.

We have analyzed the historical data of Launchpad from 2021 to the present, using data to compare historical performance with current Launchpad returns, exploring the reasons behind the "lackluster" reviews, and benchmarking the long-term returns of holding BNB against ETH staking returns, providing a comprehensive analysis of the issue of "BNB returns."

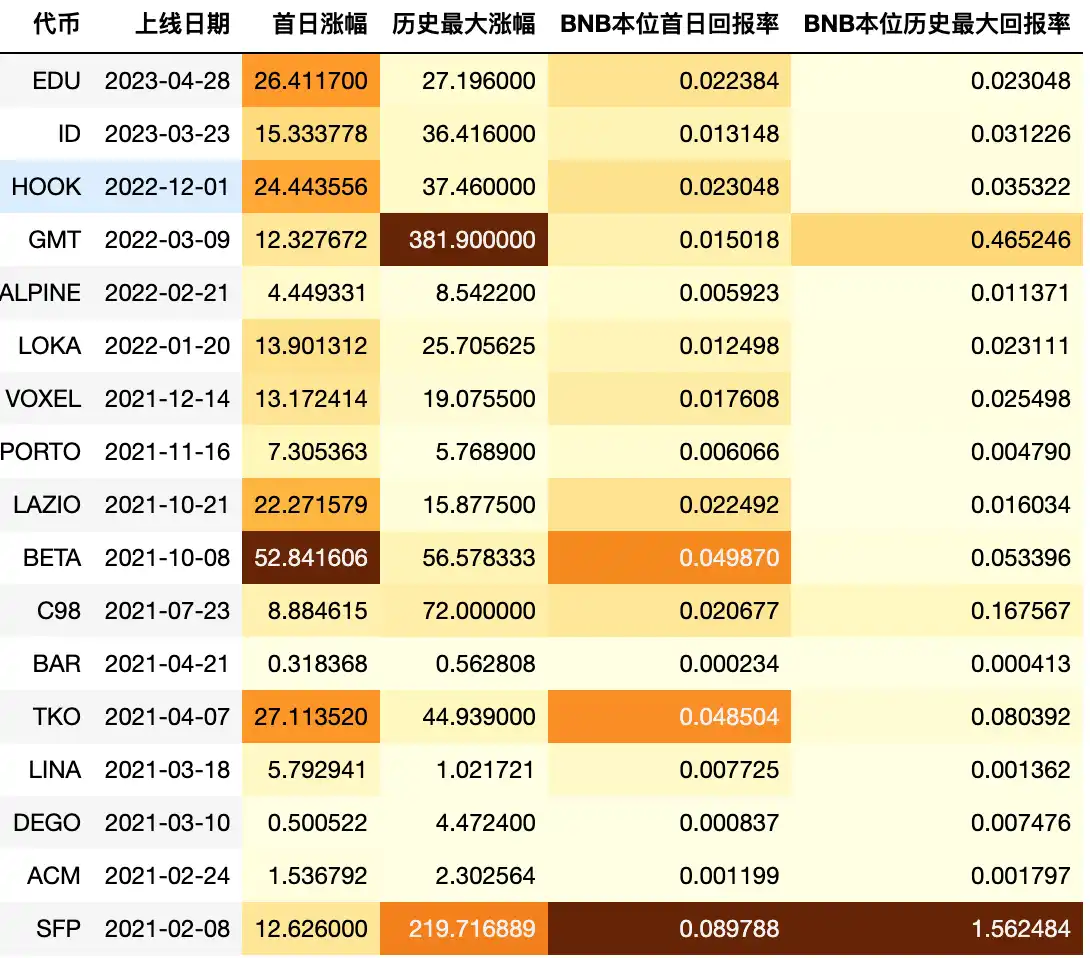

Metric Explanation

First-day increase: The price on the first UTC+0:00 after launch compared to the IDO increase.

Historical maximum increase: The highest historical price compared to the IDO increase.

BNB-based first-day return rate: The amount of BNB that can be obtained by selling tokens on the first day after investing 1 BNB in the IDO.

BNB-based historical maximum return rate: The amount of BNB that can be obtained by selling at the historical highest price after investing 1 BNB in the IDO.

Return Assessment

Taking the median of all projects, the first-day increase is 12.6 times, the historical maximum increase is 25.7 times, the BNB first-day return rate is 0.015, and the BNB-based historical maximum return rate is 0.031.

Since HOOK, the three tokens launched have all performed above average. The median first-day increase of 24.4 times is 1.9 times the historical median, the historical maximum increase is 1.4 times the historical median, the BNB-based first-day return rate is 1.5 times, and the BNB historical maximum return rate is 1.3 times. This means that these projects launched during the bear market are actually more profitable than most projects launched during the bull market.

Current policies are also relatively friendly to arbitrage users. Compared to the previously uneven returns, the BNB-based return rates of the last three projects are around 2%. If the terms of future Launchpad projects remain similar to these, then users who buy spot to short contracts for IDOs, as well as those who borrow BNB for IDOs through Venus, can expect a relatively stable return.

Why Does It Feel Lackluster?

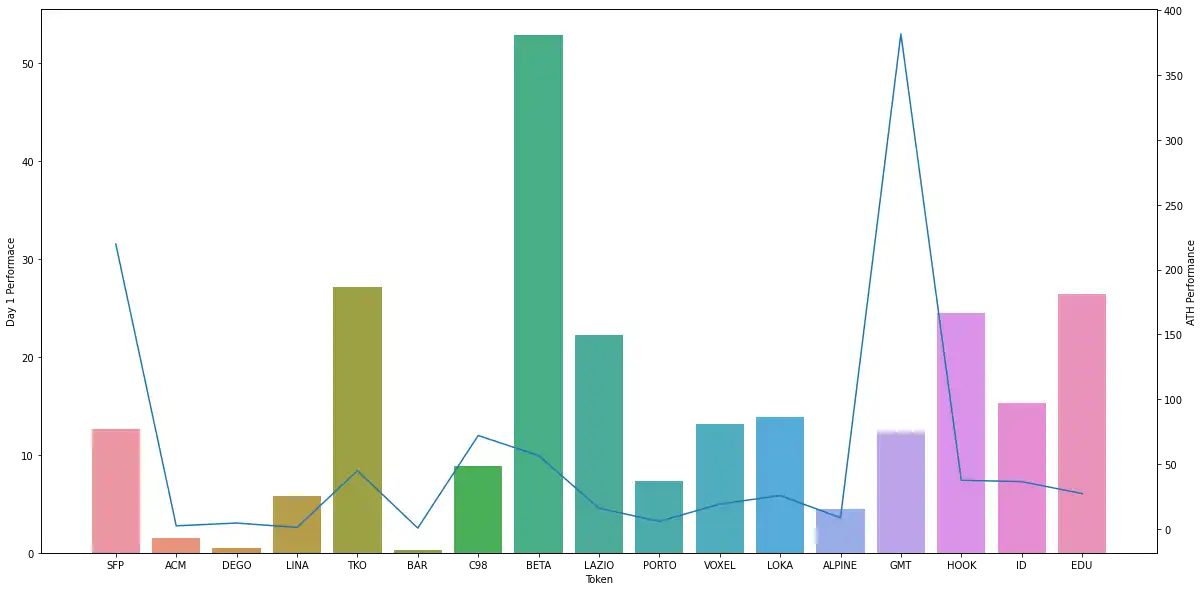

The question arises: why does it always feel less impactful than before? The reason is mostly due to the lack of major breakout projects. In 2021/2022, there were products like SFP/GMT that offered returns of hundreds of times; holding onto them was like having ten. The gap between SFP and GMT was about a year, and now, a year after GMT, there hasn't been a project that has achieved similar levels of increase.

It's normal for a phenomenal project to leave a stronger impression than three above-average projects. When you look at the chart below, your first reaction is likely to search for GMT. What does the so-called BNB-based historical maximum return rate of 0.46 for GMT mean? It means that if you invest 1 BNB in GMT, you can sell at the peak for 0.46 BNB, while SFP could even allow you to turn 1 BNB into 1.56 BNB! No wonder people have a strong impression. In contrast, the current maximum returns of 0.0X feel somewhat lackluster.

Interestingly, both SFP and GMT had relatively average first-day increases, only 12 times, which is half of what Hook/EDU achieved. The three new projects have not been online for long, and in the current bear market, Ponzi-like models are unlikely to thrive, so there shouldn't be too high expectations for now.

Long-Term Returns of Holding BNB

The annualized returns of BNB LaunchPad can actually be compared to ETH staking returns. Over approximately two and a half years since 2021, if tokens were sold on the first day, the total BNB-based return rate would be 36%, with an annualized return of 14%, which appears slightly higher than the ETH staking returns during the same period.

However, BNB also has Launchpool returns. If we add the returns from Launchpool mining and selling, the total BNB-based return rate would amount to 52%, with an annualized return of 21%, which is more than twice the ETH staking returns during the same period.

Since the bear market, the total return of projects over the past year has been about 9.5%, while the ETH staking APR benefiting from MEV income after the Merge is around 6%. This indicates that BNB's IDO return rate has still maintained over 50% compared to ETH staking returns during the bear market.

If a bull market arrives, as per this tweet, ETH staking returns are expected to benefit from MEV income, while BNB Launchpad is likely to experience a double boost in both quantity and price increase. However, ETH's current staking rate is relatively low, and compared to other L1s, there is still 2-3 times potential for growth, which may dilute returns due to more staking. The amount of IDOs on Launchpad currently appears stable around 10M in both bull and bear markets, coupled with the allure of "historical maximum returns," making BNB relatively more elastic.

Of course, both BNB and ETH are currently undergoing deflationary burns, with BNB's burn rate being significantly faster. However, the returns from burns will directly reflect in the coin price. Historically, the long-term trend of BNB/ETH has been upward, and since 2021, BNB/ETH has basically been in a sideways fluctuation state. Therefore, directly comparing staking returns with staking yields is also quite reasonable.

Conclusion

Since the bear market, the comprehensive return rates of the three Launchpad projects have been in the historical upper-middle range, with various metrics approximately 1.3-1.9 times the historical median, and the current BNB-based first-day return rate stabilizing around 2%, making it suitable for arbitrage.

It has been a year since projects like SFP/GMT, which could achieve a maximum return of 1.5 BNB from 1 BNB investment, have appeared, and the negative market feedback may stem from this.

Compared to ETH staking, the current long-term holding of BNB yields an annualized return of about 9.5% from IDOs, which is 1.5 times that of ETH. In the previous bull market, BNB returns were about twice that of ETH, and it is expected to have even more upward elasticity in the next bull market.

However, we shouldn't rely solely on calculators; in the next bull market, the use case of ETH/BNB may be the key factor determining returns. Currently, ETH L2 is developing well, and whether BNB Chain can continue to gain momentum is also a particularly important point to watch.