How did Solana perform in Q4 last year after the FTX collapse?

Although Solana's value is most affected, overall, its network health remains stable.

Although Solana's value is most affected, overall, its network health remains stable.Original Title: 《State of Solana Q4 2022》

Author: James Trautman, Messari

Compiled by: Babywhale, Foresight News

Key Points:

- After the collapse of FTX, Solana was the most affected, with its market cap dropping by 70%, but the network's health remained stable.

- Integrations unrelated to FTX are ongoing to strengthen the Solana DeFi ecosystem and position it to support and serve additional demands.

- The NFT landscape on Solana continues to develop actively, with GameFi nearing reality.

- Rumors about Solana development stumbling after FTX and a mass exodus of core developers are false.

- Following the FTX and Hetzner incidents, the network's staking and decentralization remained stable and improved its condition.

- Solana will continue to roll out multiple initiatives, including network upgrades, Neon EVM, Firedancer, Solana Mobile Stack (SMS), and community work, among others.

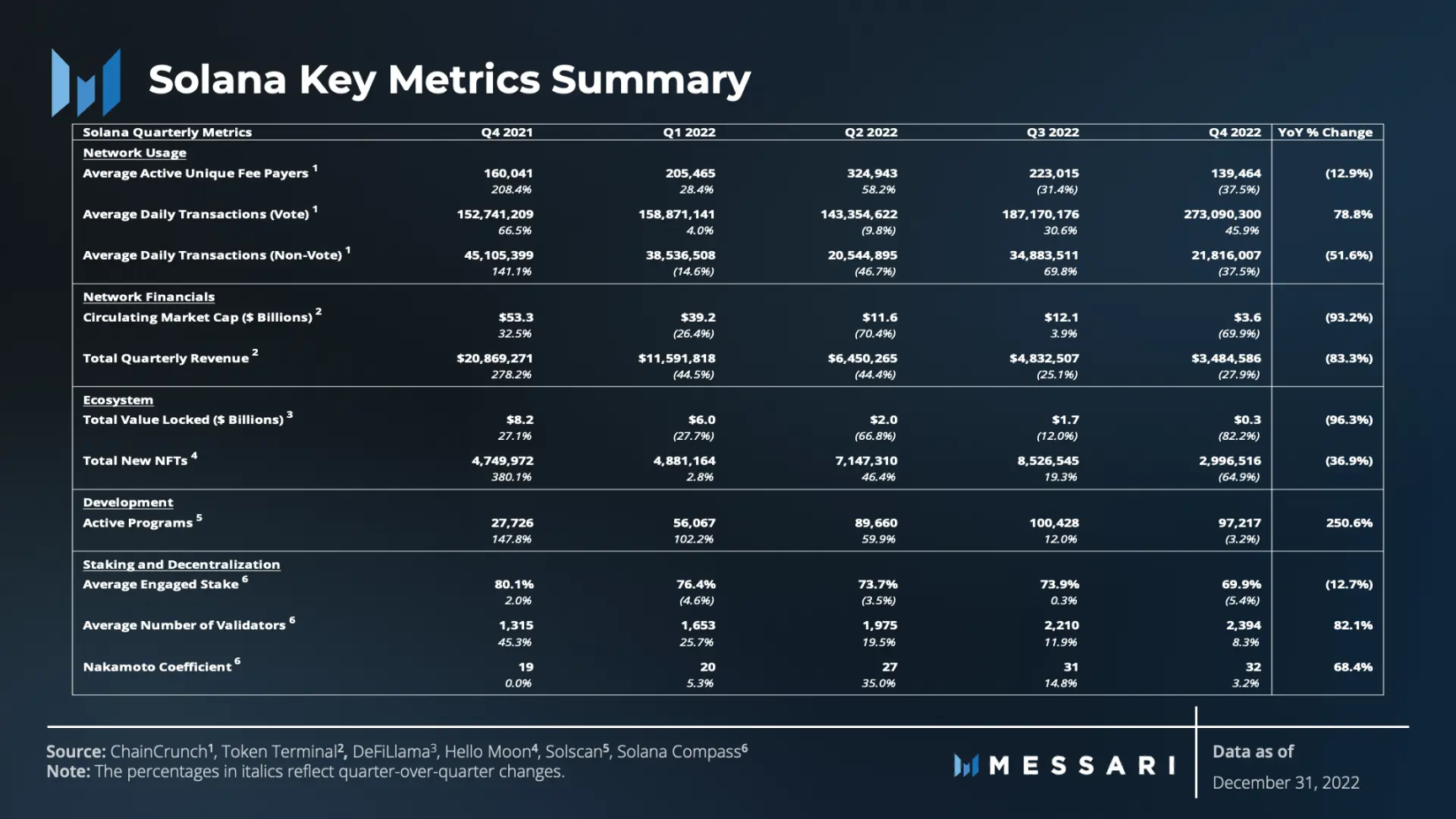

Key Metrics

Q4 Narrative

Despite showcasing advantages in Q3 2022 and successfully navigating challenges throughout the year, Q4 saw a rollercoaster-like decline. With the collapse of FTX and the ensuing spread of sentiment, Q4 experienced a significant turning point, but it did not lose everything.

Although overshadowed by the bankruptcy of FTX, Solana's network and ecosystem still demonstrated strong vitality in Q4. The mission to increase usage remains unchanged, with ongoing developments, further integrations with partners like Instagram and Facebook, and ecosystem expansions into GameFi and DePIN (Decentralized Physical Infrastructure Networks) proving this point. The development of network functionalities is also ongoing, along with countless other potential growth catalysts.

As a follow-up to the Q3 2022 Solana Report, this report will delve into the data performance of this quarter and provide qualitative evidence of how Solana continues to overcome challenges and make progress under adverse market conditions (qualitative content is not displayed in this article; interested users can read the original text).

Performance Analysis

Financial and Network Overview

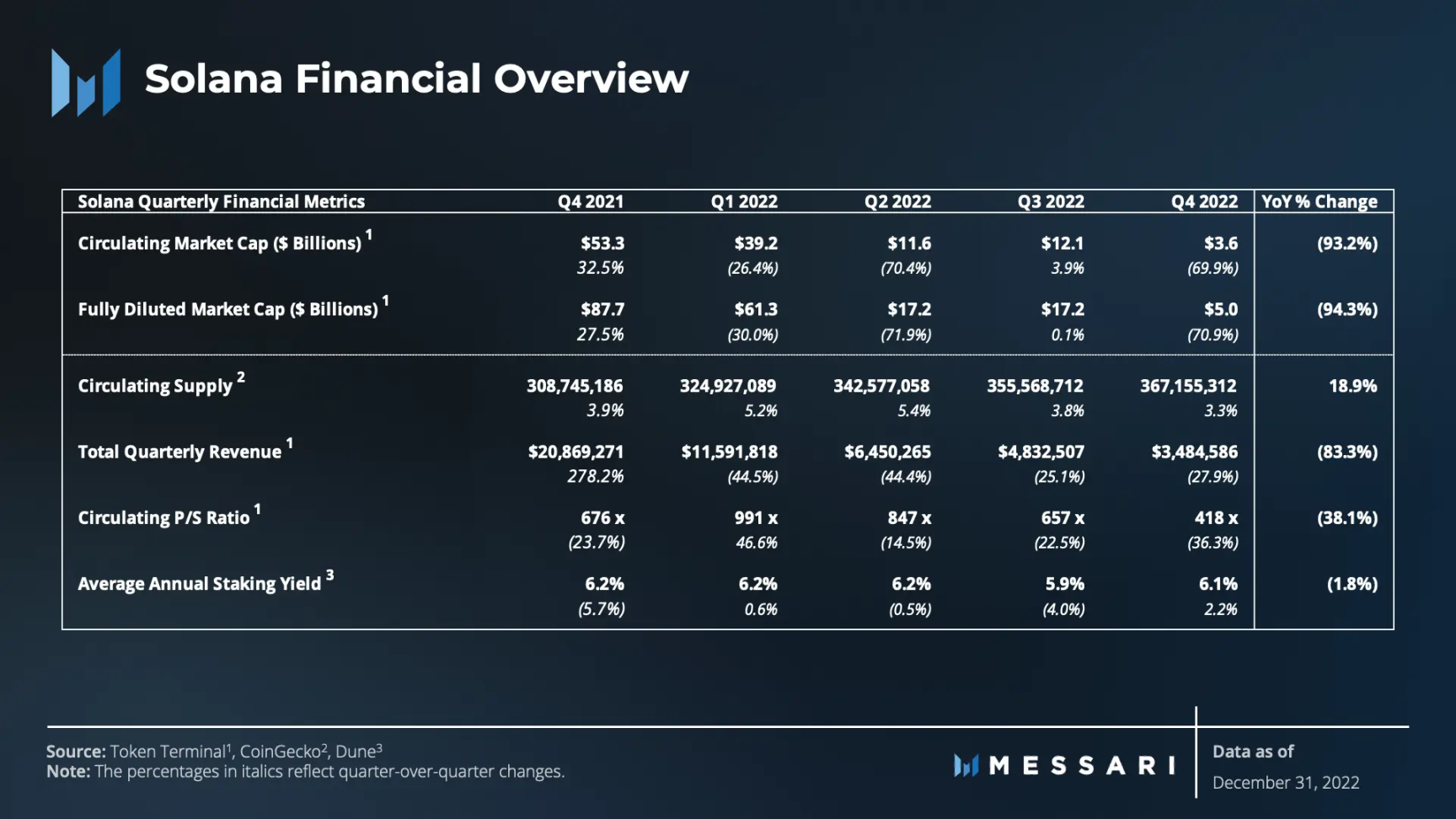

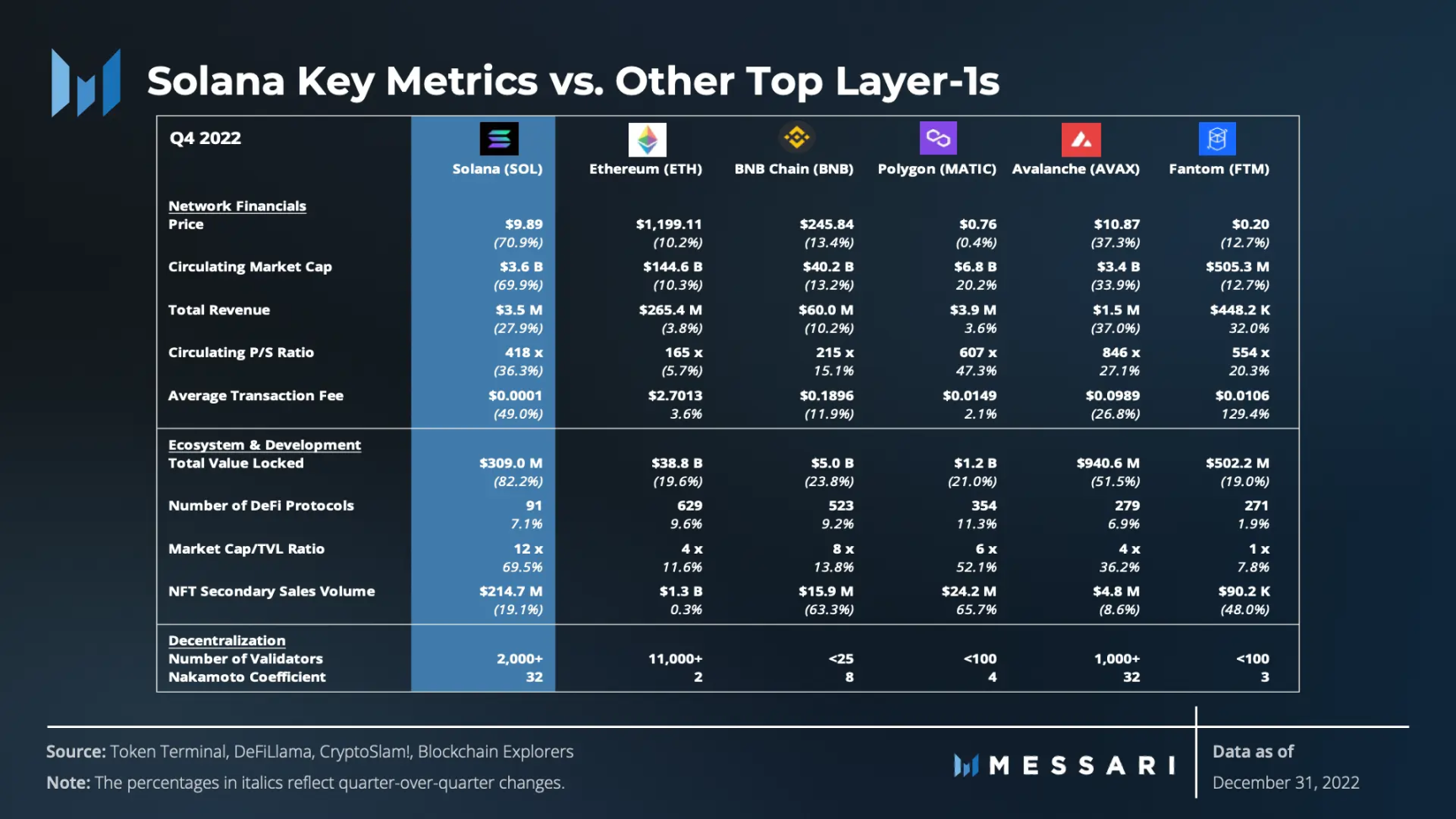

In Q4, the ongoing bear market combined with the bankruptcy of FTX had a significant negative impact. FTX was a major investor in Solana and an integral part of Solana DeFi, particularly in the development of DEX Serum. As a result, Solana became one of the most affected networks, with its market cap plummeting by 70%, from $12.1 billion to $3.6 billion.

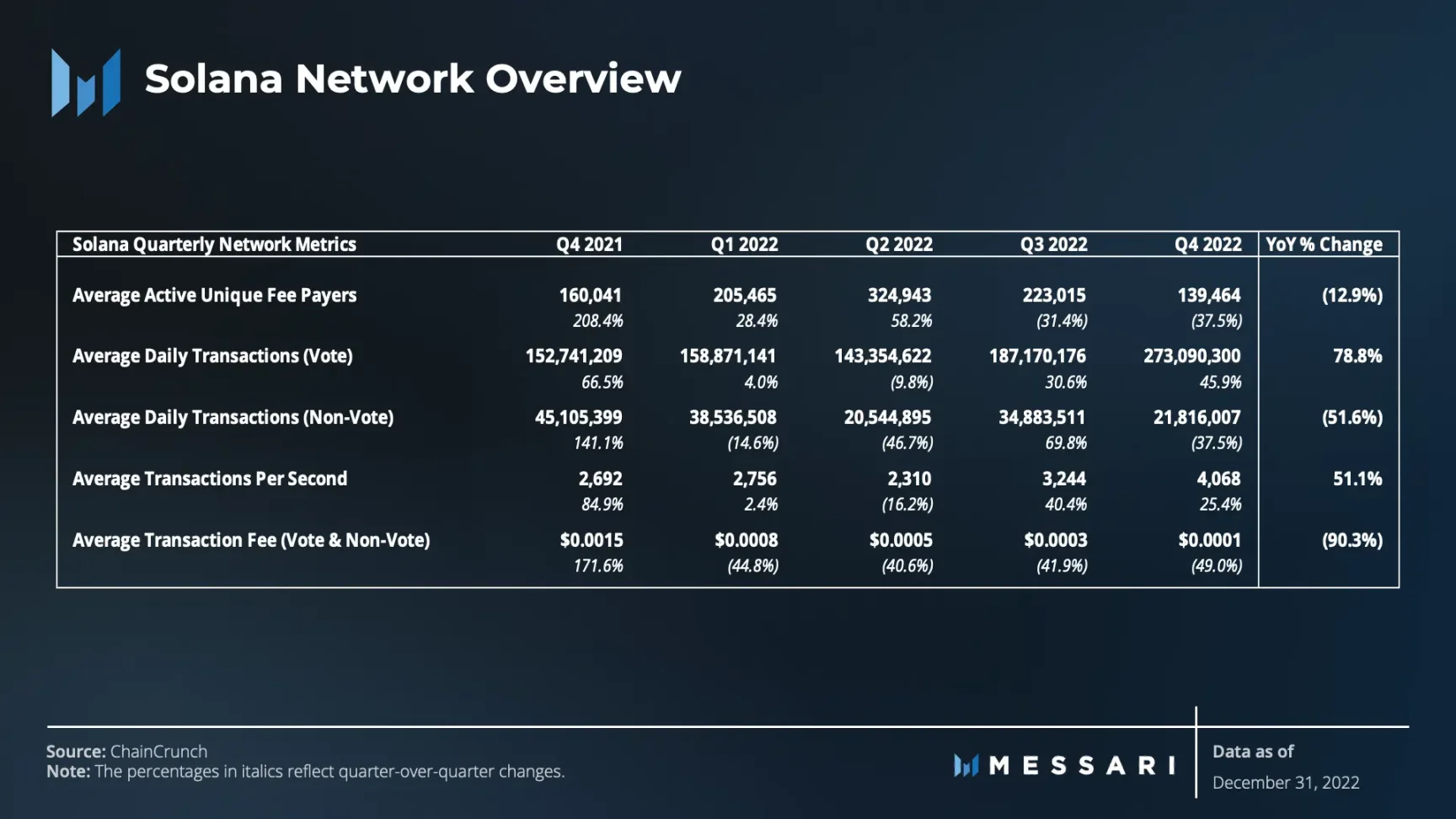

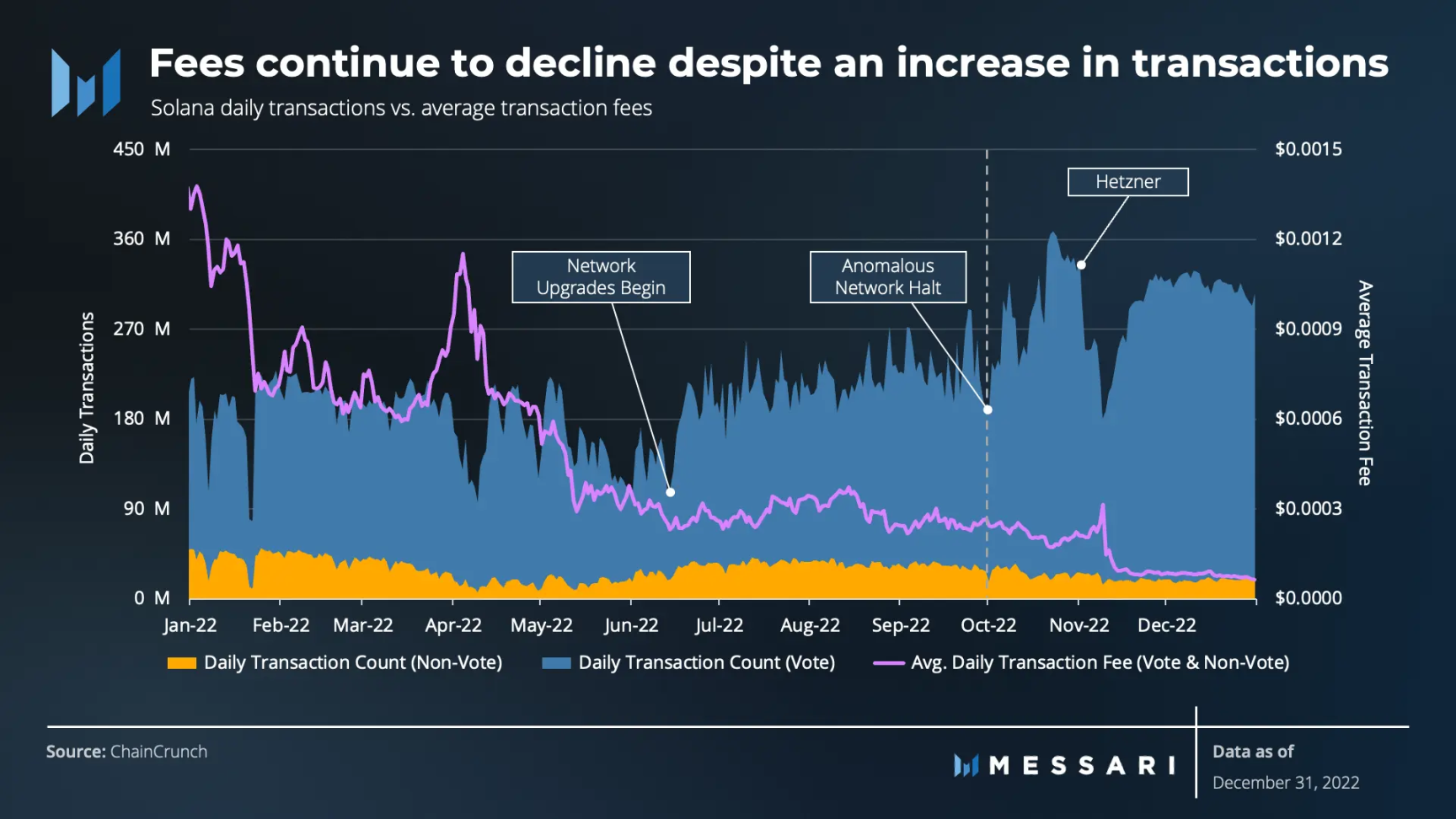

Despite market conditions exerting downward pressure on user activity, average daily transaction volume and transactions per second (TPS) continued to increase due to improved network performance.

Although total transaction volume increased, average transaction fees continued to decline (49%). After declining for the fourth consecutive quarter, average transaction fees fell by 90.3% year-on-year. Q4 revenue also continued to decline (27.9%). Similarly, total quarterly revenue decreased by 83.3% year-on-year. Nevertheless, the extent of the revenue decline was less than that of transaction fees, indicating that revenue was partially supported by the growth in transaction activity.

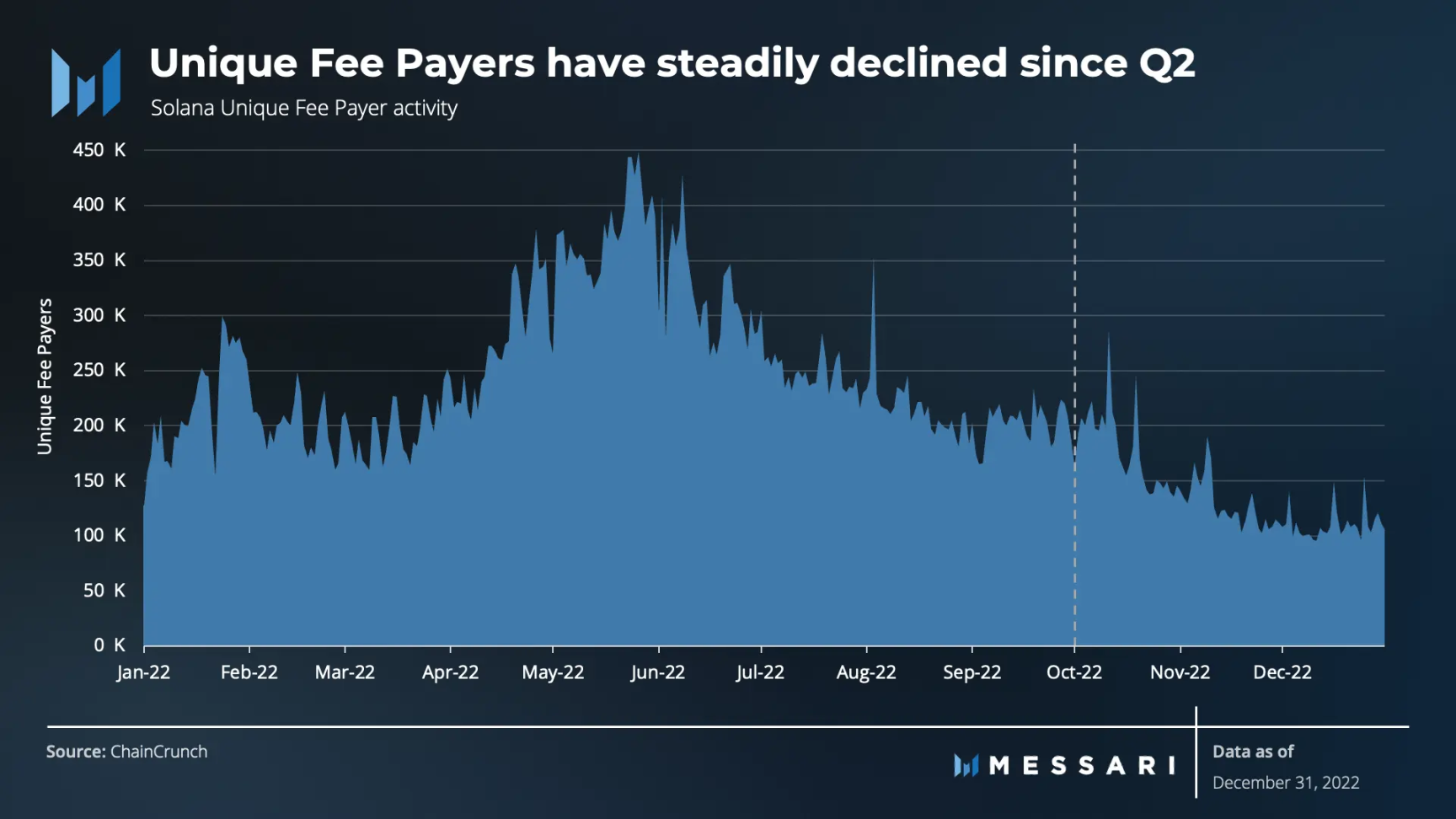

The Unique Fee Payers metric includes the number of unique accounts that pay fees for at least one transaction daily. Since the end of Q2, the daily average fees paid by unique fee payers have been steadily declining. This user group stabilized at a baseline level by the end of Q3, as it reached a long-term average. However, market sentiment post-FTX drove user activity down by 37.5% in Q4, ultimately resulting in a year-on-year decline of 12.9%.

The Unique Fee Payers metric may not be the best way to measure user activity on Solana, as it does not account for transactions authorized by multiple users but paid for by a single account. The Unique Signers metric may more accurately measure absolute user activity.

Nonetheless, the trend of unique signers is closely related to the unique fee payers for both this quarter and the year.

Transactions on Solana can be categorized into consensus (voting) and non-consensus (non-voting). Non-voting transactions are similar to EVM transaction counts. They represent actual economic activity on the network.

Throughout 2022, the network's transaction activity and performance fluctuated for various reasons. In the first two quarters, network performance was affected by spam caused by Gulfstream, which is Solana's alternative mempool for pending transactions. At the end of Q3 and the beginning of Q4, the network halted due to abnormal consensus errors. Finally, changes in Hetzner services triggered a wave of transaction fluctuations in early November.

However, the narrative of "interruptions" is changing, as the aforementioned factors leading to poor performance have stabilized since the end of Q2. The network's uptime since April 2022 has been very long, with monthly uptime exceeding 99%. Due to several network upgrades, TPS reached a historical high as a quarterly average in Q4. Throughout the year and in Q4, Solana continued to roll out upgrades related to QUIC, staking-weighted Quality of Service (QoS), and local fee markets.

QUIC

Solana replaced its old data transmission protocol, the User Datagram Protocol (UDP), with QUIC. Although QUIC shares some similarities with UDP, it allows for better control of data flow. QUIC enables validators to exercise more discretion when sending and receiving transaction data to and from the slot leader. In other words, validators can more easily filter out spam transaction data that previously disrupted the chain.

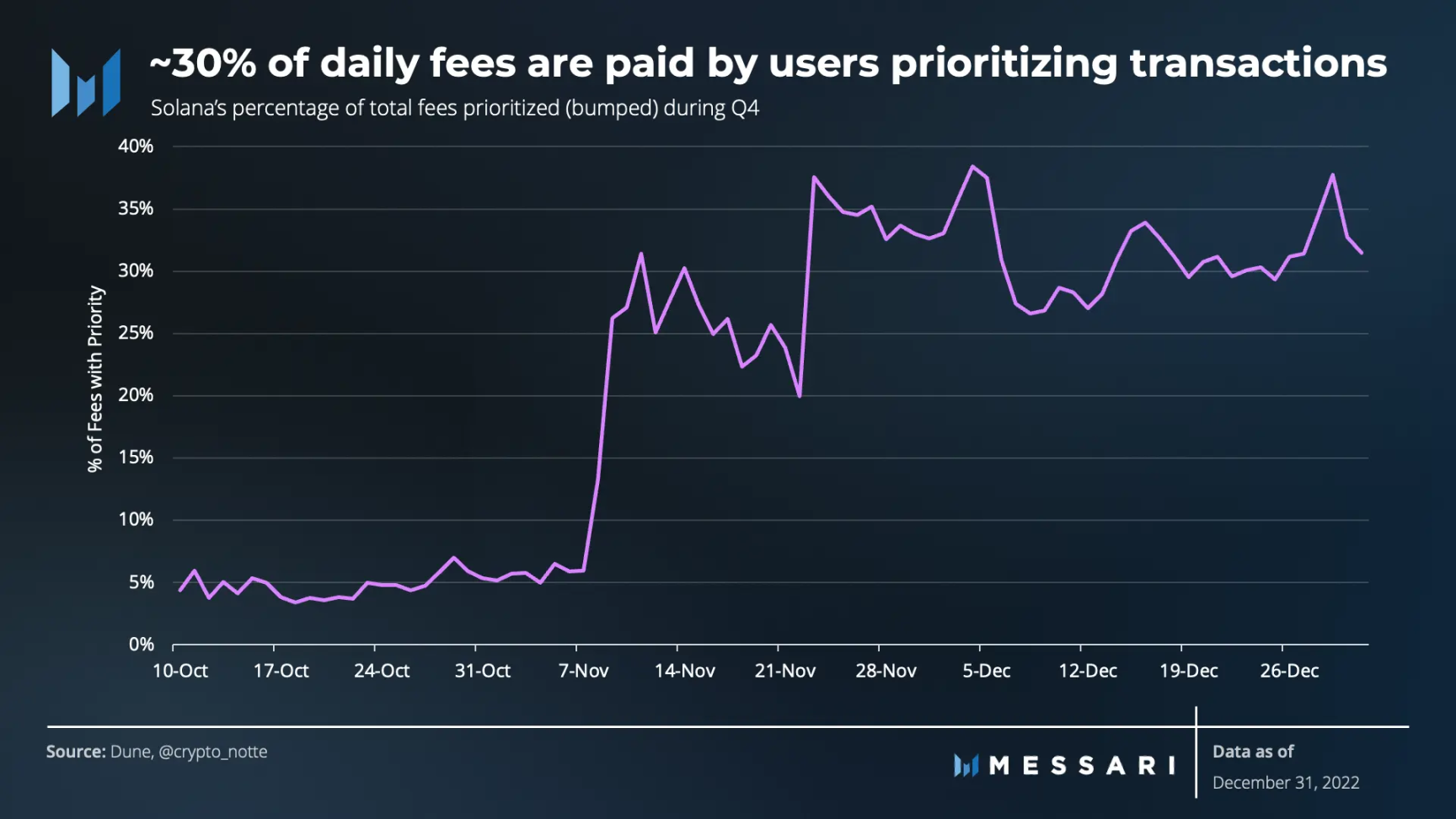

Local Fee Market

Solana accounts have hard computational limits. Once reached, subsequent transactions cannot modify the state of that account during the given block period. The local fee market allows users to send priority transaction fees to validators to modify the state of a specific account before it reaches the computational limit in the current block.

The result is less network spam (as it may bid higher), and a more efficient block space market.

On average, over 30% of daily fees are paid by users of priority transactions. As more wallets integrate local priority transaction fees, this average may increase.

Additionally, Solana's local fee market can play a role during periods of high network activity. Base fees remain stable, but priority transaction fees are soaring in more active areas of the network.

Staking-Weighted Quality of Service (QoS)

Staking-weighted guarantees that validators always have the right to transmit transaction data packets to the leader, rather than validators indiscriminately accepting and transmitting transactions. For example, a validator with 0.1% of the staking share can always transmit 0.1% of the transaction data packets to the leader. The previous indiscriminate approach made it easy for validators to transmit packets smaller than their staking weight. Therefore, the network will support smaller validators, increasing centralization.

Overall, these three upgrades bring performance stability to the network. Nevertheless, non-voting transactions (economic activity) decreased by 37.5% quarter-on-quarter and 33.3% year-on-year, likely due to market sentiment.

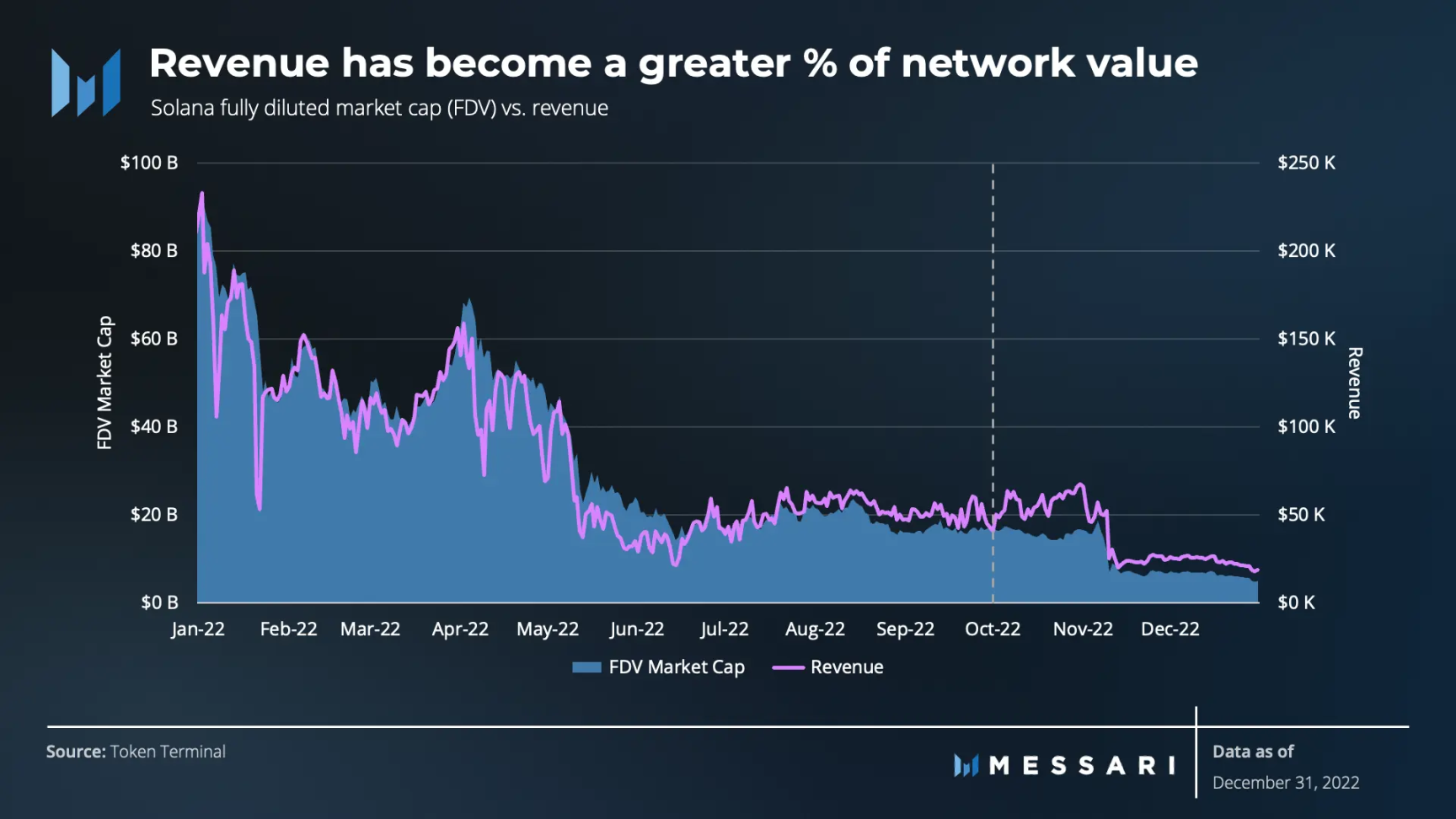

The presence of payers and the stability of daily transactions drive the network's revenue and value growth. Ideally, more users and transactions (despite lower fees) would increase revenue and represent fundamental value growth.

To this end, considering that daily revenue fluctuations and trends typically accompany changes in network value, there remains a correlation between revenue and network value.

As seen in 2021 and throughout Q1 and Q2 of 2022, declines in network performance led to reduced network transaction activity and diminished sustained revenue. This exerted downward pressure on network value during that period. However, network upgrades have brought more stability. The 49% decline in transaction fees coupled with a 28% drop in revenue indicates that fundamentals such as network stability, user activity, and transaction activity are becoming important components of Solana's network value.

From a valuation perspective, the relationship between network value and revenue also aligns with trends in the price-to-sales ratio. Since Q1, the price-to-sales ratio has dropped from 991x to 418x, indicating that the network is undervalued compared to historical levels.

However, it must be remembered that blockchain assets represent an unprecedented asset class that may require the application of unique valuation techniques. Therefore, traditional financial metrics such as revenue and P/S ratios may not be the most appropriate when evaluating these indicators.

Ecosystem and Development Overview

DeFi

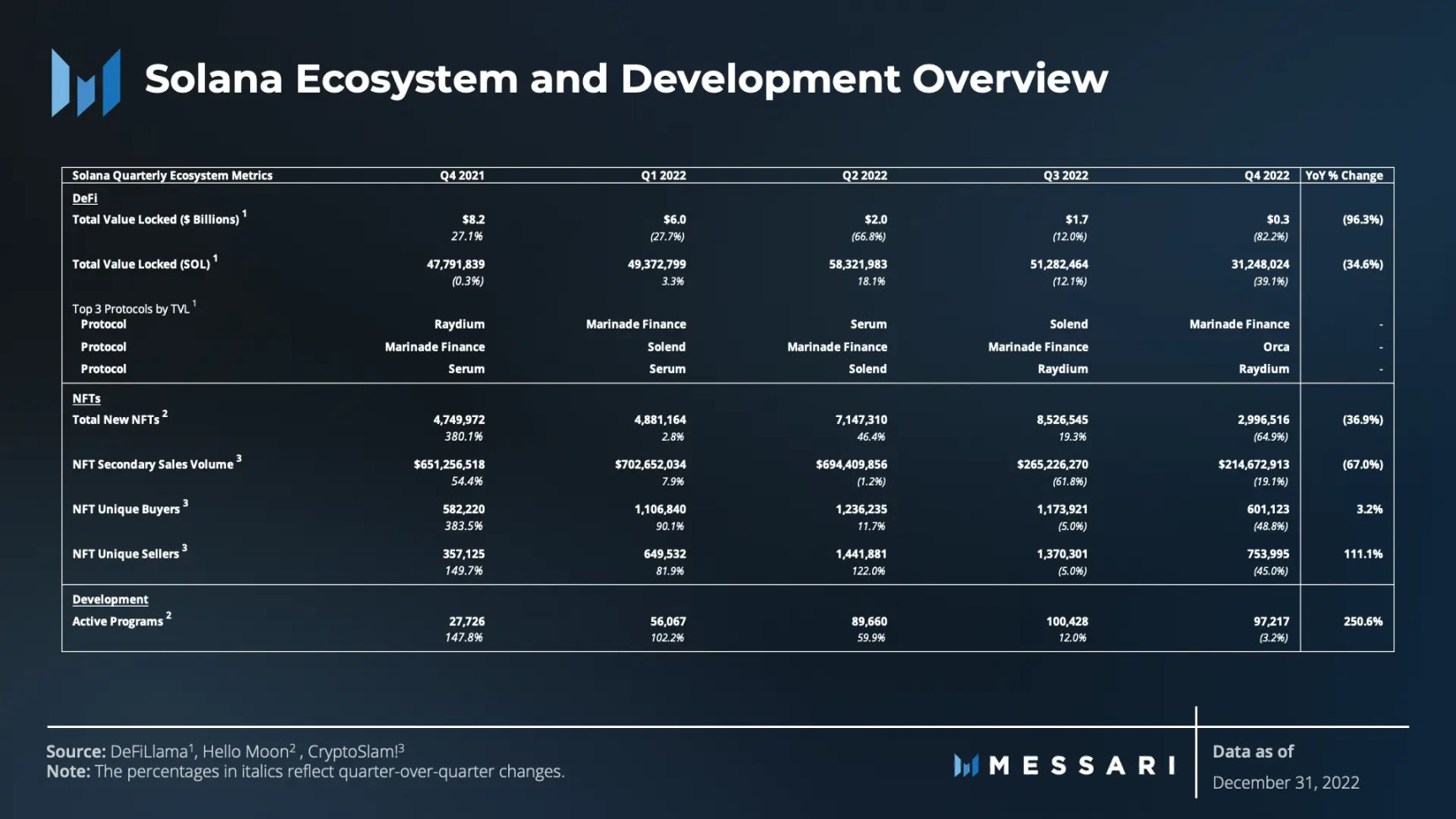

Solana DeFi was significantly impacted by the October Mango Markets exploit and the November FTX collapse impacts. With Alameda no longer conducting on-chain operations, Total Value Locked (TVL) saw a substantial decline.

Mango Markets

On October 11, 2022, cryptocurrency trader Avraham Eisenberg executed a series of trades that artificially inflated the price of the MNGO token. The trader profited from the rise, borrowing $116 million against unrealized profits and withdrawing those funds from Mango Markets. This exploit is a classic example of cross-market manipulation, and the attacker was ultimately arrested.

FTX Bankruptcy

- By the end of Q4, following the FTX/Alameda collapse, Solana's TVL fell by 26% in SOL terms, while the dollar value of SOL itself dropped by 67%.

- The community deployed a forked version of Serum, as FTX/Alameda held the upgrade keys to the original Serum contract. This fork quickly gained over $50 million in order book depth on the SOL/USDC pair.

- The price of Sollet wrapped tokens "supported" by FTX plummeted and began trading at significant discounts below their expected collateral-backed value.

- The "Solend whale" was liquidated, leaving the protocol with approximately $6.5 million in bad debt. The DAO passed a vote to use the Solend treasury to compensate users.

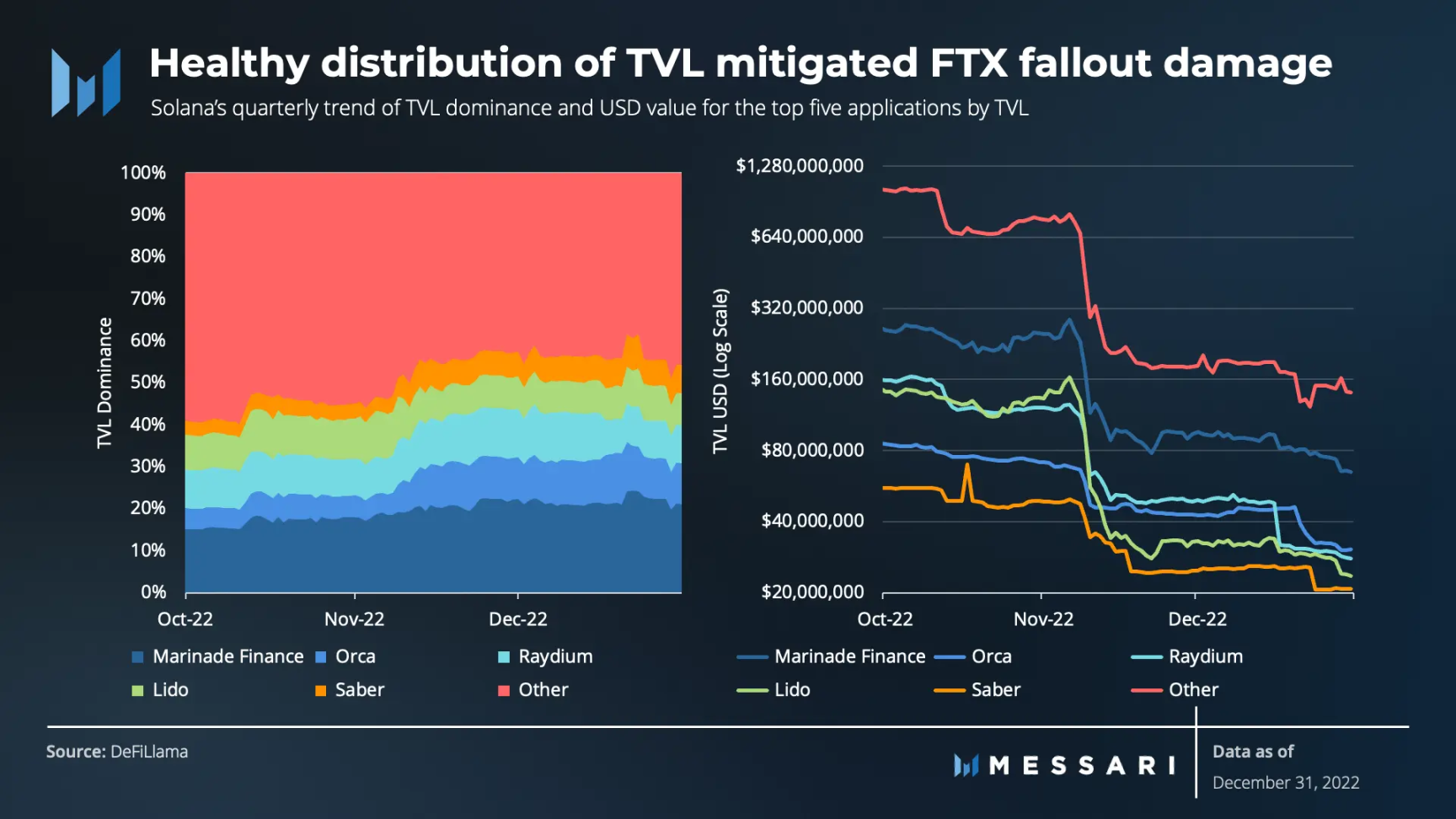

Despite this, there has always been a healthy cross-application TVL distribution on Solana, which may have mitigated further damage to the overall DeFi ecosystem. Currently, about 50% of the TVL is locked in most long-tail DeFi protocols on the network.

Despite the challenging conditions, DeFi unrelated to FTX continues to develop within the Solana ecosystem, positioning itself to support and serve additional demands.

Spot DEX

OpenBook and Ellipsis Labs are two newly emerging DEXs that have gained attention.

OpenBook is the community version of Serum V3, created to address potential security issues with the Serum upgrade keys.

Ellipsis Labs' Phoenix order book is built on the centralized limit order book (CLOB) concept of Serum. It features design decisions that enhance efficiency, such as removing the time-consuming process of inputting DEX order books and setting optimal bids and asks from DEX design.

Derivatives and Structured Products

Many teams are building in the derivatives, options, and structured products space, including Drift, Zeta Markets, Mango Markets, Friktion, 01, and Cega. These teams are addressing key issues such as liquidity, new asset backing, cross-margining, and user experience.

The core protocol of Hxro Network also launched in Q4. Hxro is an on-chain derivatives infrastructure that supports and facilitates any derivatives applications built on Solana.

Liquid Staking Derivatives (LSD)

In Q4, liquid staking became more prevalent across the cryptocurrency space. On Solana, Jito Labs' JitoSOL is gaining attention. Currently, Marinade and Lido still lead in market share, but this may change if JitoSOL maintains higher yields.

NFT

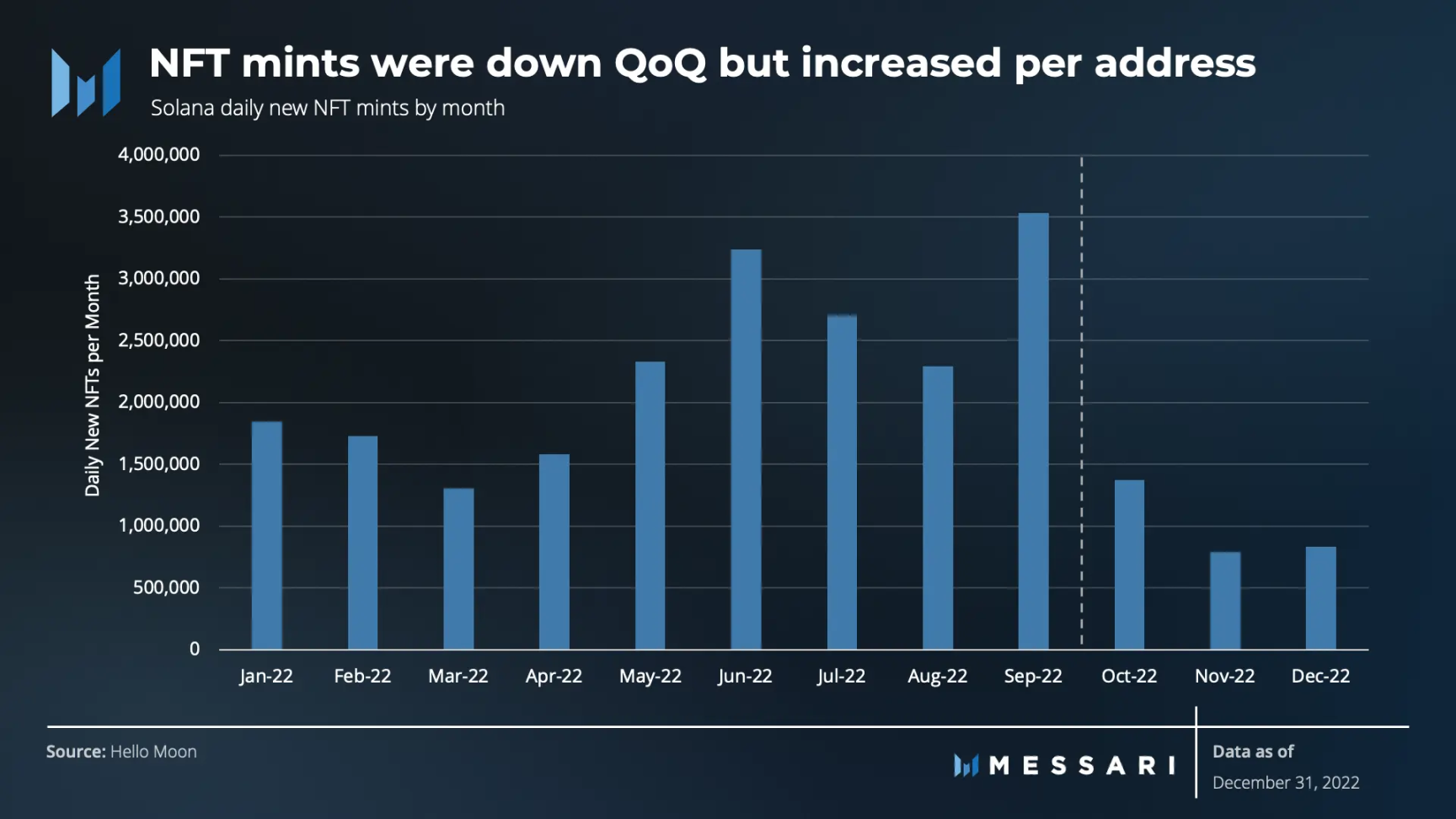

Solana's NFT ecosystem also experienced a downturn, but not as severe as DeFi, similar to most other networks. The total number of new NFTs minted daily saw its first quarter-on-quarter decline, with a drop of 65%. However, this decline occurred after a significant surge in Q3. Despite the decrease in minting volume, the average number of NFTs minted per address increased, indicating that loyal users are emerging.

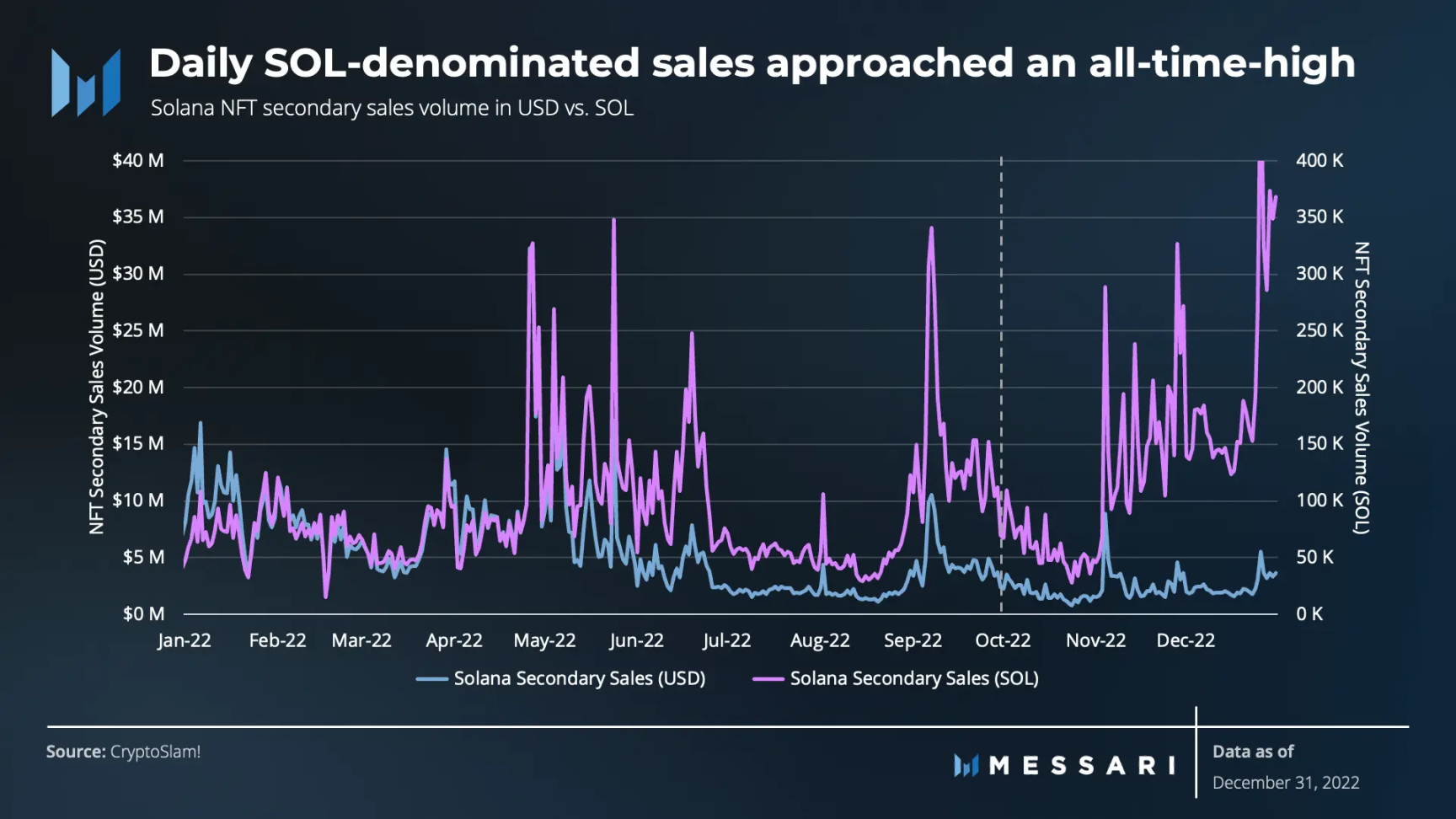

Although the number of new NFTs declined under the impact of the FTX bankruptcy, NFT sales activity remained relatively resilient. Daily sales priced in SOL reached an all-time high in December, as holders and traders rushed to adjust strategies in response to the plummeting SOL price.

Nevertheless, Solana's NFT landscape continues to develop actively.

In addition to continuously optimizing the Metaplex digital asset standard, Metaplex also advanced several key initiatives in Q4, including:

- Developing solutions to reduce the cost of minting NFTs;

- Launching no-code solutions for technically challenged creators;

- Enhancing its popular open-source minting solution, such as Candy Machine (V3);

- Enabling creators to collect royalties.

In addition to Metaplex, NFT platforms Magic Eden and Cardinal also announced a form of protocol-level creator royalty protection. Some designs allow creators to prohibit markets that do not enforce royalty collection. Over time, it will be seen which design prevails.

In addition to leading NFT platforms, Instagram and Facebook have also integrated Solana NFTs and went live in Q4.

Solana's strategy and position in the NFT space remain strong, making it the second-largest network in terms of secondary market trading volume, only behind Ethereum.

GameFi

The crypto space positions itself to support GameFi ecosystems, with Solana Ventures leading the way. Its $150 million fund to promote the development of the Solana gaming ecosystem has attracted additional investment (especially Magic Eden's Magic Ventures and increased the appeal of gaming. Such developments place GameFi at the forefront of catalyzing growth in the crypto space, and Solana is fully committed to developing its GameFi ecosystem.

Over 1,100 gamers participated in the Solana Foundation Games Day in Lisbon. They tried dozens of completed (or nearly completed) Solana ecosystem games. Currently (as of January 20), there are 15 games launched, with expectations to increase to 37 by March 2023.

Some highly anticipated games include Star Atlas, ev.io, BR1: Infinite, Aurory, and the open alpha version of Legends of Elumia and the public beta of Elumia launched in Q4 2022.

Cutting-Edge Use Cases

- Orbis: Enables Solana developers to integrate social experiences into their applications using their SDK;

- Aleph.im Network: Launched the first fully open-source decentralized indexer for Solana;

- Hivemapper: A decentralized mapping network that gained attention after its launch;

- Homebase: Onboarding real estate onto the blockchain via Solana;

- Helium: Officially migrating to Solana in Q1 2023.

- Bonk: The first meme token on Solana.

The payment sector is also continuously emerging. In early November, sportswear company ASICS collaborated with STEPN to launch and sell a running shoe called UI Collection. The running shoes were sold during the Breakpoint event and could only be purchased using USDC via Solana Pay. The UI Collection sold out within five days, generating over $600,000 in sales, with revenue settled instantly and no credit card fees.

Despite the challenges facing the Solana ecosystem, there is still hope for the future. As new applications revive usage and Solana's technology continues to evolve, the downward trend in value growth may be reversed.

Developer Activity

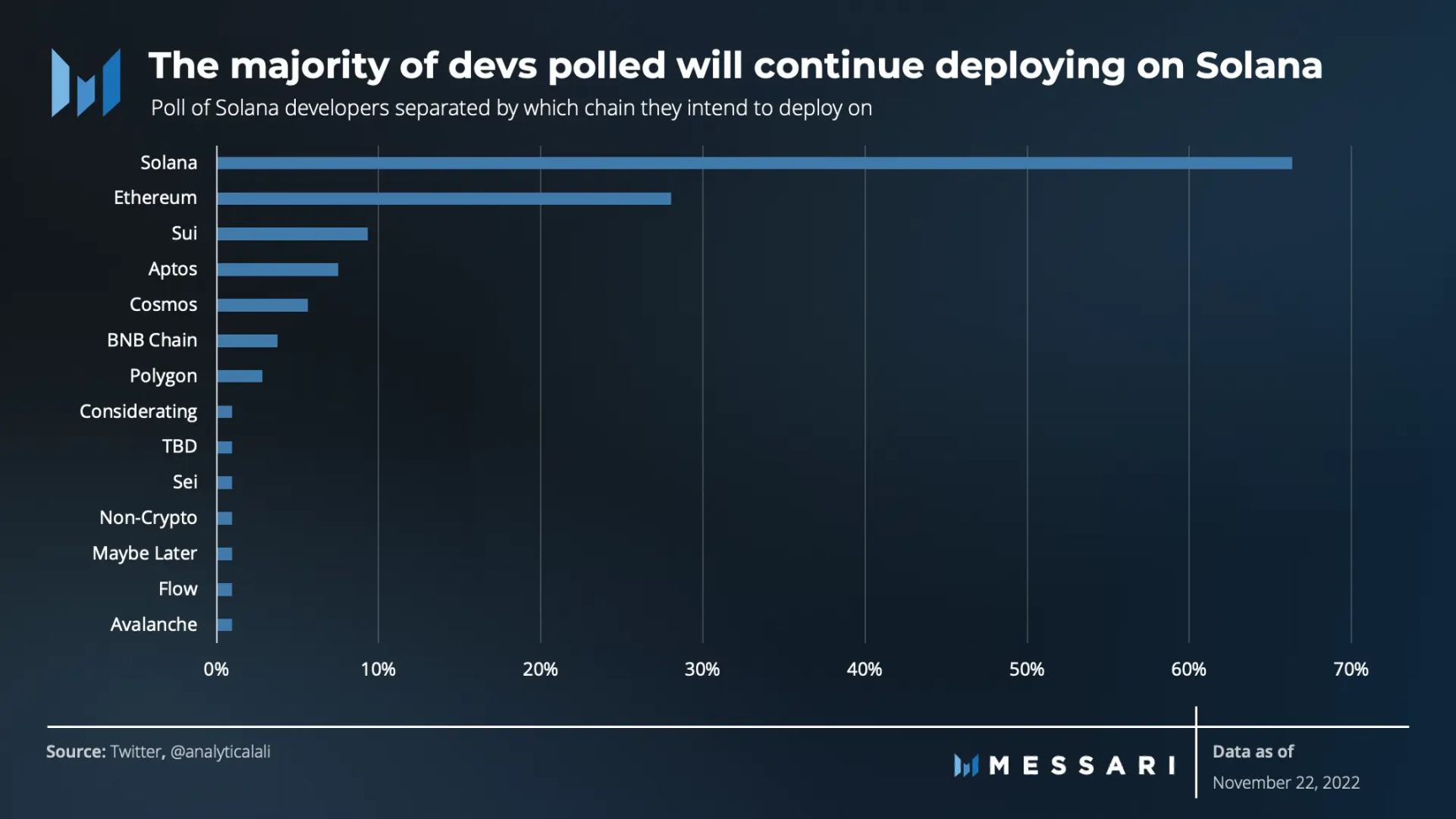

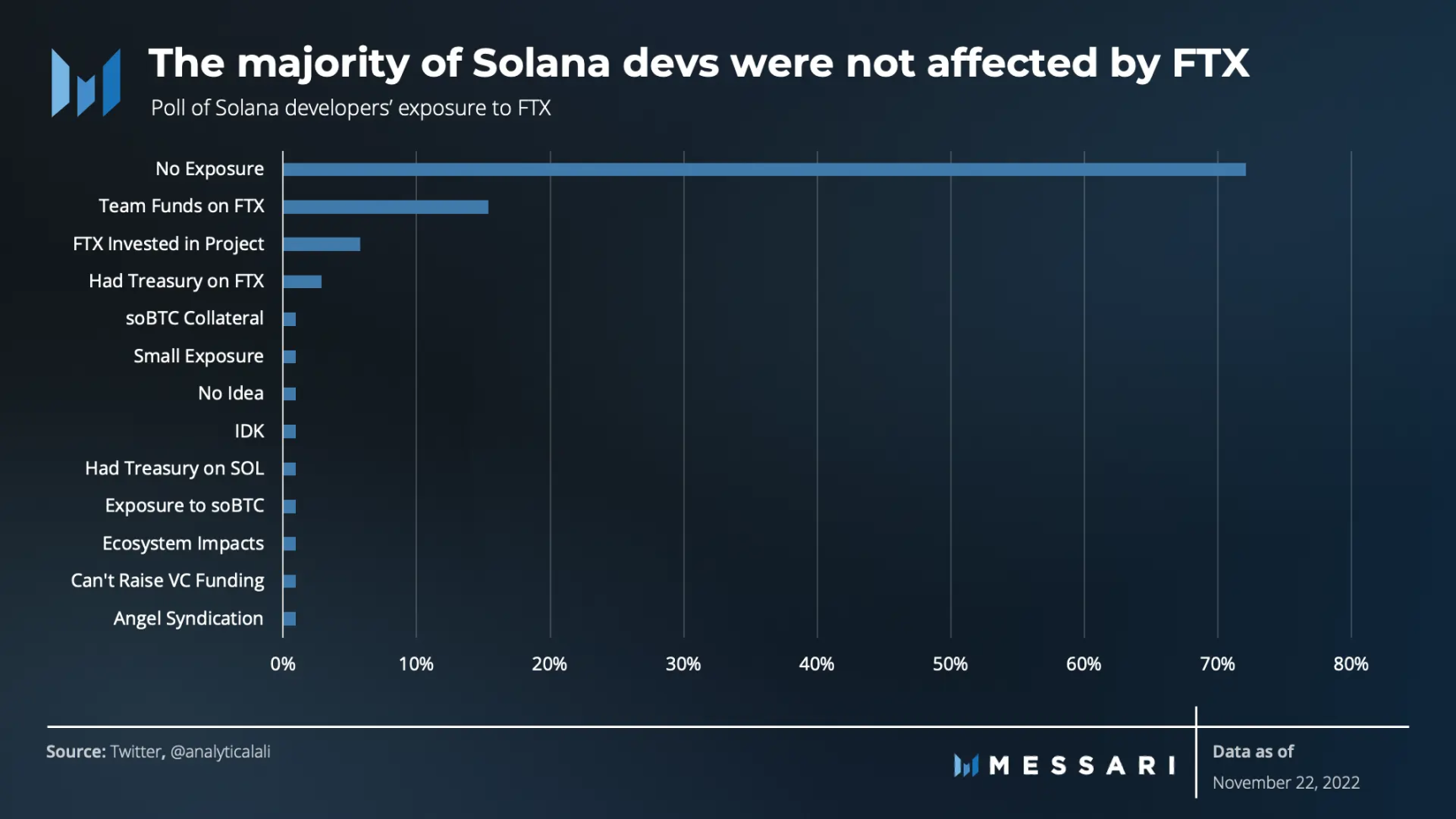

After the FTX bankruptcy in Q4, rumors circulated on Twitter about Solana's development stumbling rumors and a mass exodus of core developers. These rumors are false and primarily stem from data issues from Token Terminal.

Additionally, a survey was conducted in Q4 to dispel the rumors. While surveys like this may not be rigorous enough for academic research, they do provide directional data for a better understanding of reality. Two main takeaways:

- A significant number of developers chose to deploy applications on other chains, especially Ethereum, but the majority of respondents (66%) still stick to using Solana.

- 72% of developers indicated that their teams were not affected by FTX.

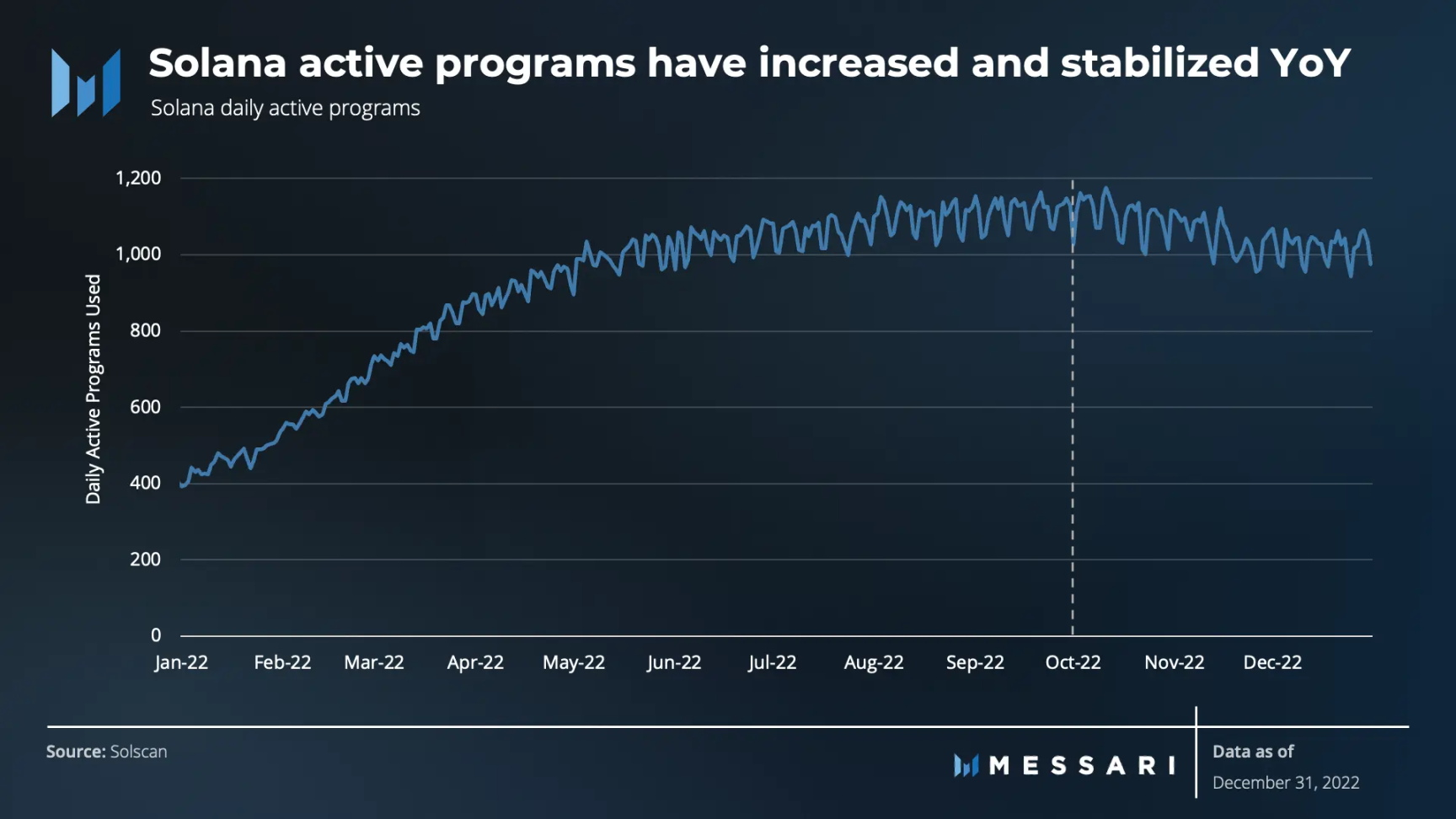

The number of active projects during specific periods is another indicator of ecosystem development. As more applications are launched and the user base grows, the number of active applications has also increased and stabilized.

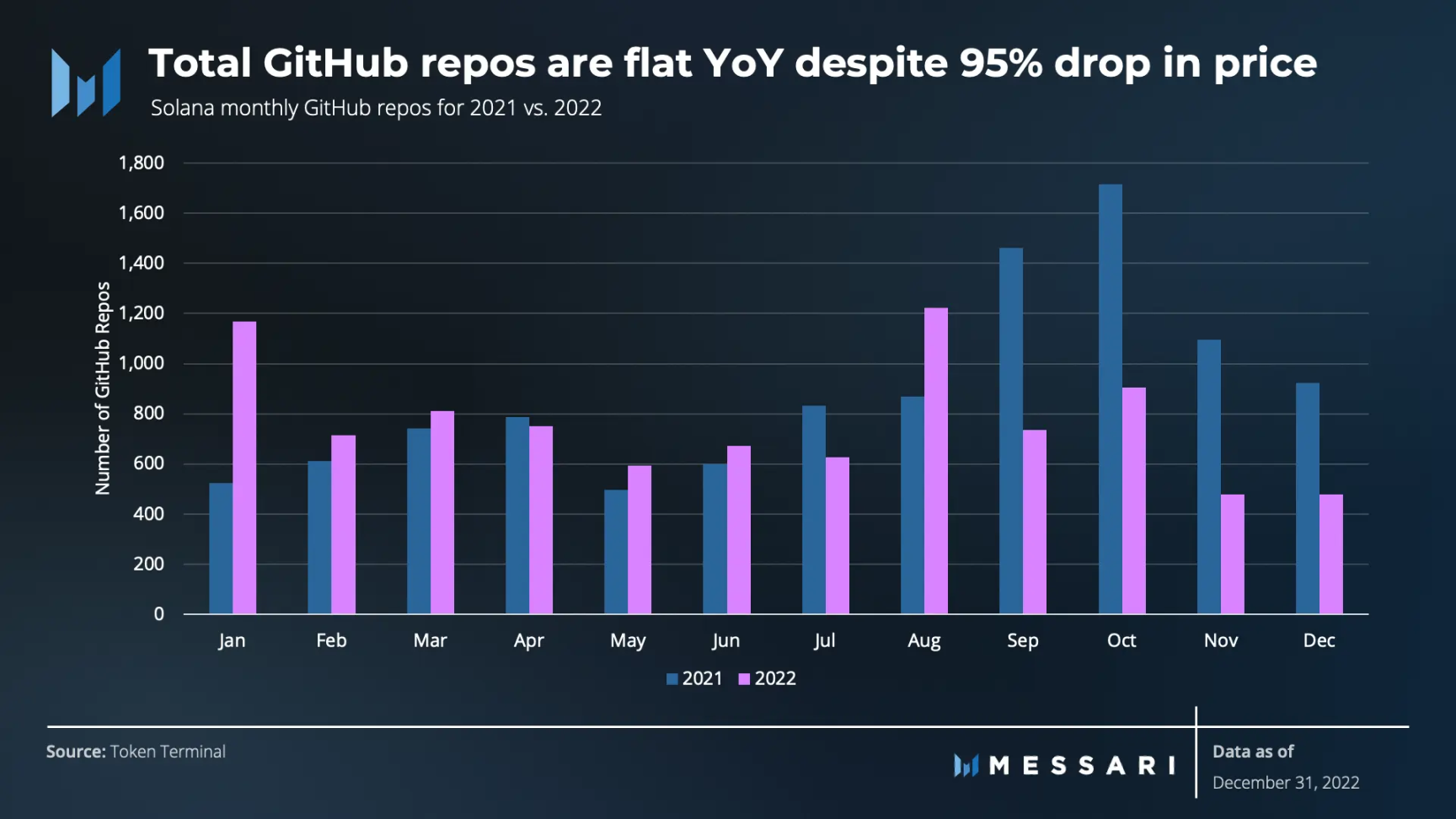

In previous reports, the participation of core developers was also measured by tracking event data from the Solana Lab GitHub repository.

However, the current data sources regarding developer activity are not comprehensive. Not all submitted code or documentation can be treated equally, which may lead to incomplete statistics on core developer activity.

Despite the incomplete data, evidence still suggests that the number of GitHub developers remained stable year-on-year, even as the price of SOL declined by 95% during the same period.

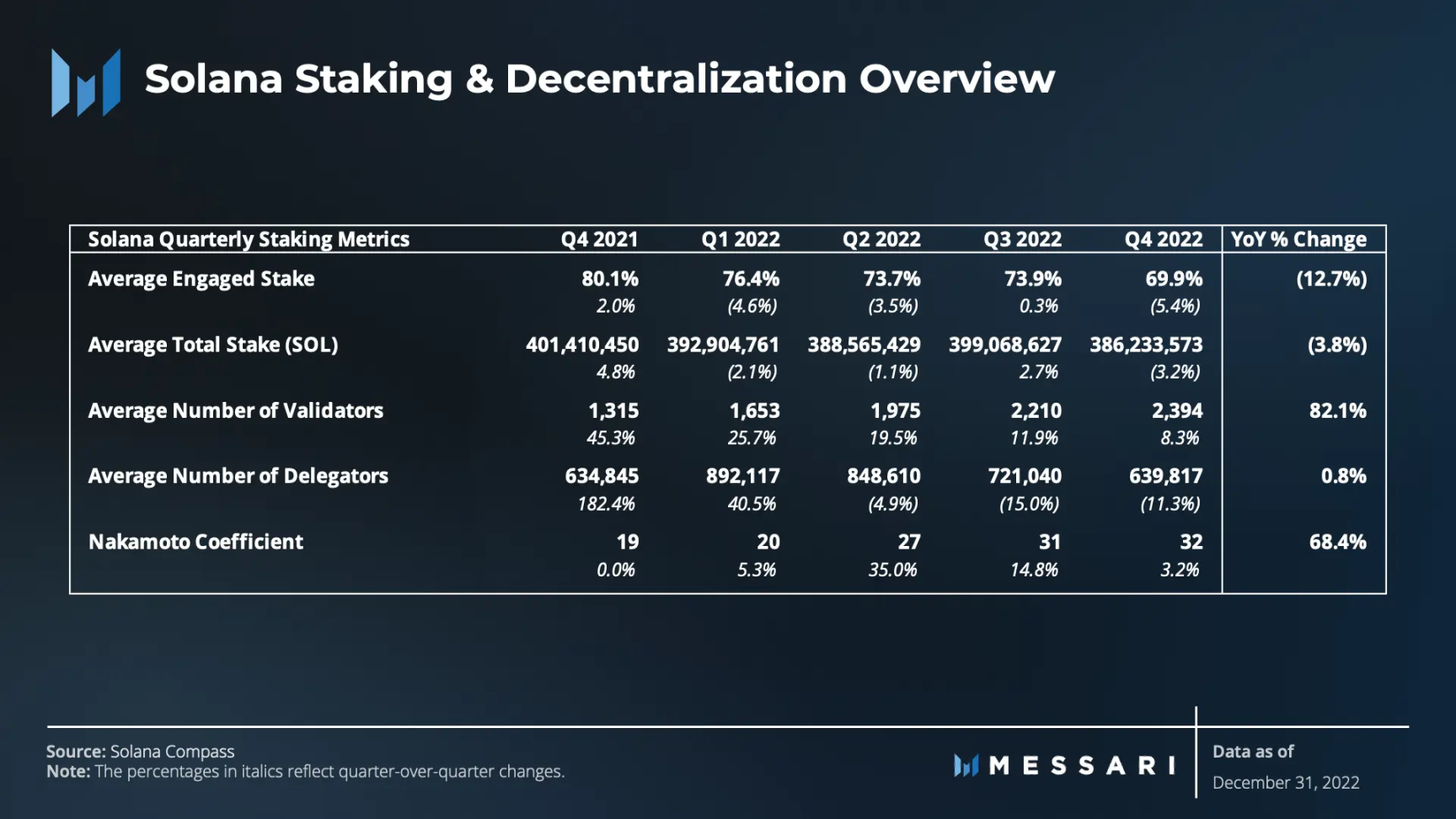

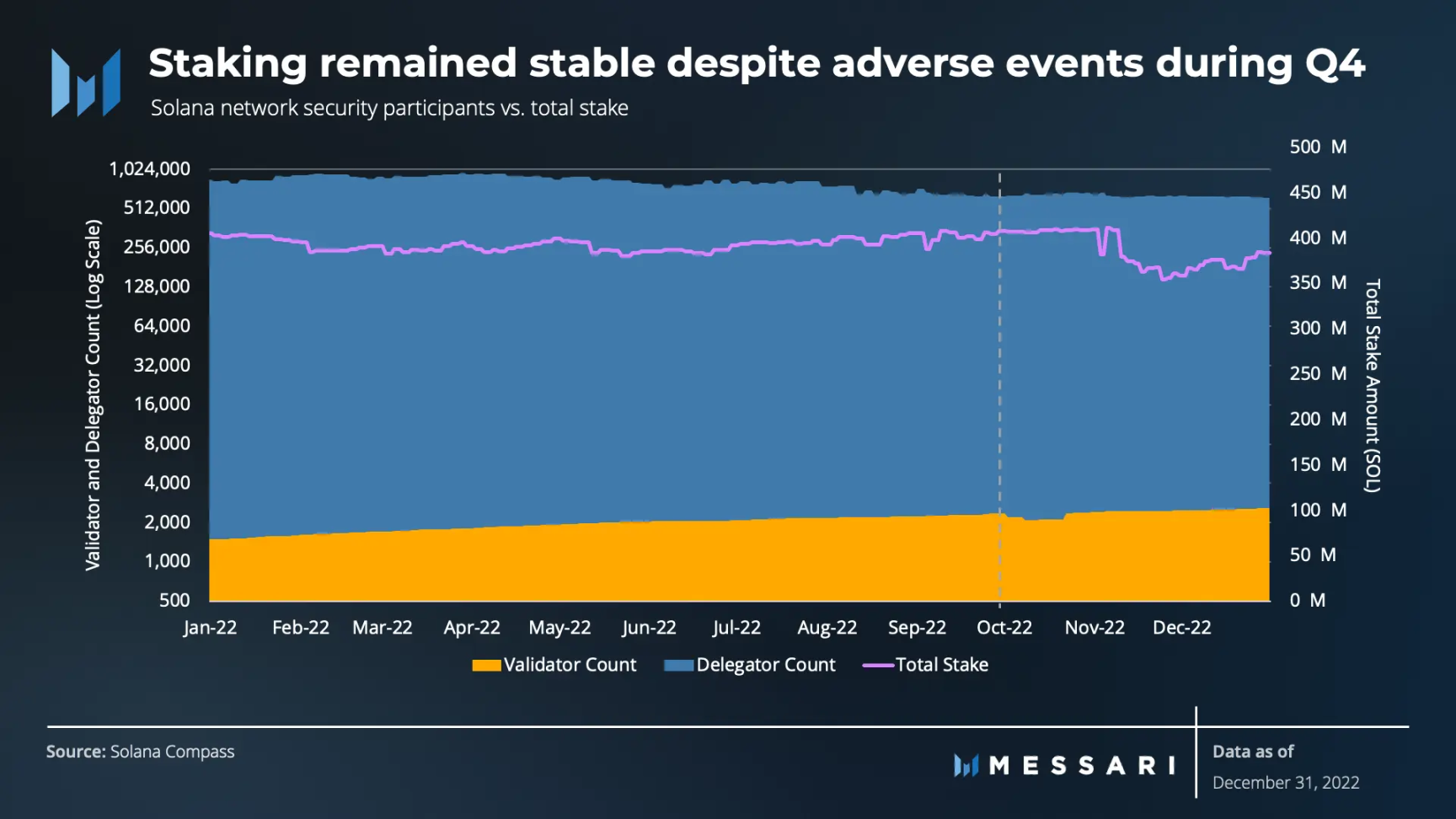

Staking and Decentralization Overview

The narrative regarding the health of Solana's network infrastructure has also changed. Concerns arose that the guardians of network security would flee for some reason.

In Q4, the Twitter community speculated that Alameda Research, which controlled 13% of the total supply of SOL, would lead to significant selling pressure. However, the tokens are locked and protected under bankruptcy law. In other words, these SOL can only be unlocked after the liquidation process is completed, which may take a considerable amount of time.

Despite adverse events for Solana, the network's staking and decentralization remained relatively stable. Solana's average staking participation rate has remained around 75% over the past year.

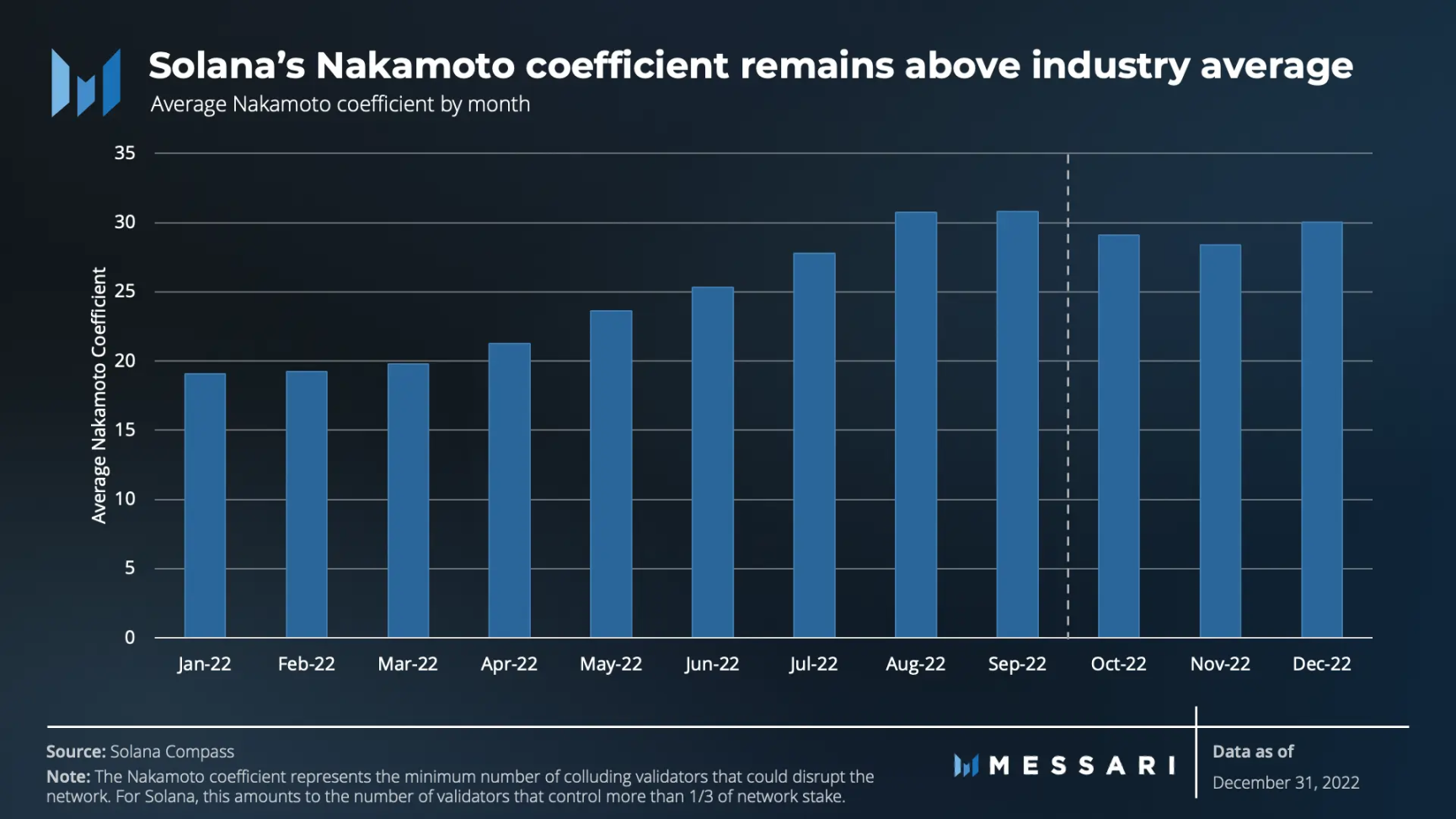

Solana's 32 Nakamoto coefficient remains above the industry average compared to other Layer 1 networks.

While a high Nakamoto coefficient and a growing validator set are beneficial, they do not guarantee immunity from centralization risks. Indicators such as geographical diversity, data center ownership, and entities' control over validators also need to be referenced to ensure a more comprehensive assessment of network health.

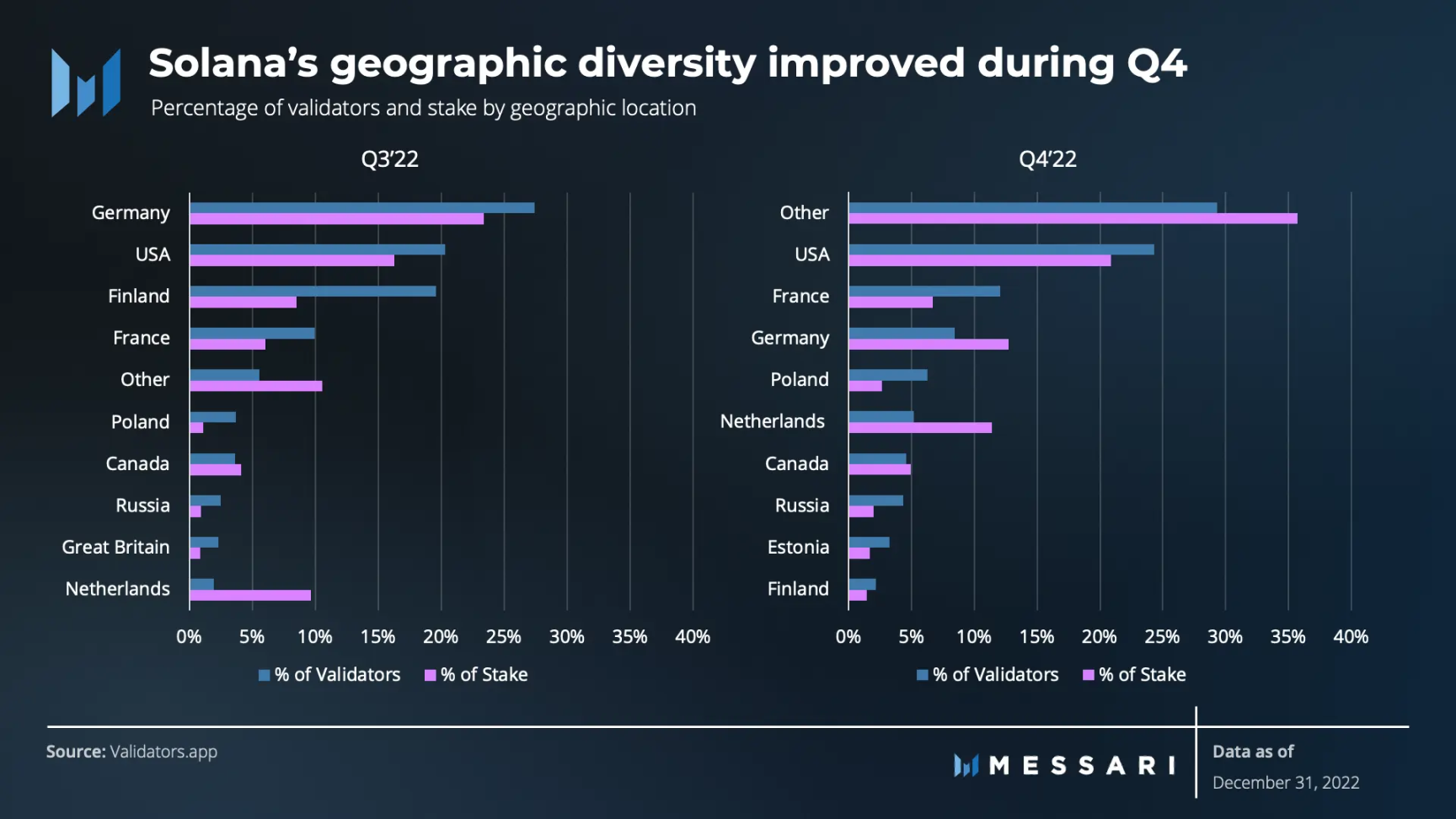

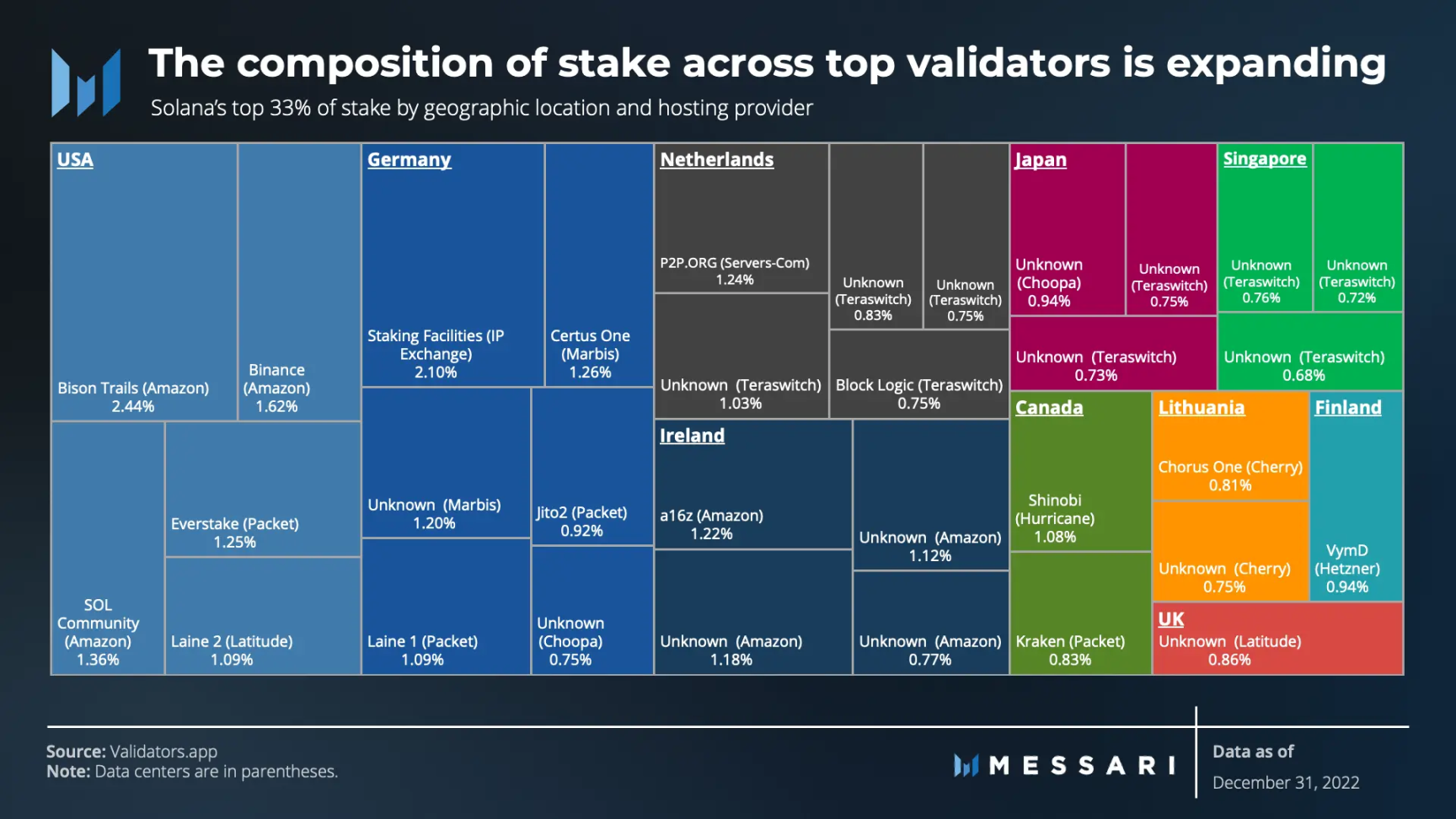

Solana aims to address the typical geographical centralization issues of Layer 1 networks. Too many validators in the same geographical location may jeopardize the network's health due to geopolitical risks, regulations, and natural disasters.

As of December 31, 2022, validators and staking are distributed across more than 35 geographical locations and over 130 independent data centers worldwide.

While distributed globally, about 25% of Solana validators and about 20% of staking volume are located in the United States. The "Other" category accounts for approximately 30% of total validators and staking, including over 25 different countries.

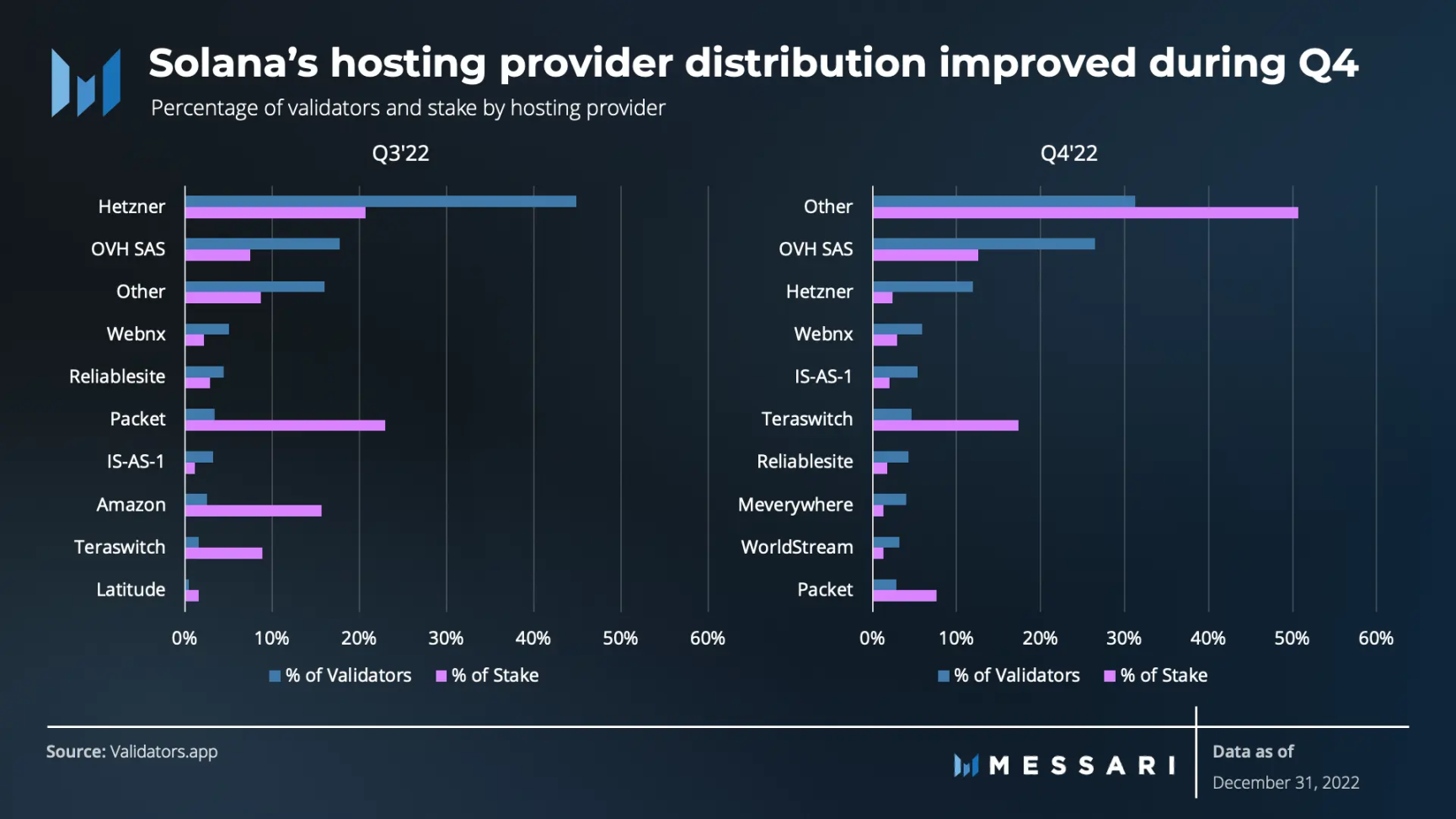

Data center centralization is another issue. Private data centers like AWS that run validators may grant their owners disproportionate power over the network. As of December 31, 2022, no single data center hosted more than 33.3% of the staking volume. The "Other" category, which accounts for over 30% of total shares, includes more than 125 independent data centers.

At the end of September 2022, a German web hosting company, Hetzner, hosted over 40% of the network's validators and over 20% of the staking volume. This relationship led to a high concentration of the network in Germany, particularly in one data center.

In early November 2022, Hetzner withdrew support for Solana-related activities, stating that its policy prohibits the use of its servers for cryptocurrency-related activities. Fortunately, this action was not enough to disrupt the network. Nevertheless, the incident highlighted the potential risks of the network being overly concentrated in a single geographical location and data center.

When evaluating the top 32 validators that constitute the Nakamoto coefficient, the situation is slightly different.

More than half of the validators control over 33% of the network's staking volume, primarily hosted by Amazon and Teraswitch. Additionally, one-third of these staking volumes are located in the United States. Assessing the composition of these stakes among top validators is essential, even if there is not enough staking volume to collude maliciously. In this case, if these stakes were to shift to more centralized geographical areas like the U.S. or to a few data centers like Amazon or Teraswitch, the network could be at risk.

Ultimately, after validators and staking migrated from Hetzner to dozens of other geographical locations and data centers, the decentralization and health of the Solana network remained intact and in better condition.

Competitive Analysis

Since its inception, Solana experienced rapid growth until Q3 2022, but its position as one of the top ten most valuable Layer 1 networks has since declined. Here, we compare Solana with the five chains with the highest TVL.

Following the FTX bankruptcy, Solana's valuation plummeted. Other chains were also affected, but to a lesser extent, particularly Polygon.

Similarly, Solana's daily revenue is on a downward trend, despite an increase in total daily transaction volume. Therefore, the decline in revenue is attributed to the decrease in transaction fees. Other chains (except for Polygon and Fantom) experienced only slight declines throughout the quarter.

In this quarter, Solana's price-to-sales ratio decreased. Changes in P/S measure the protocol's revenue and provide insight into the number and cost of transactions processed by the protocol. As Solana's value changes more significantly than its revenue, the cost per unit of revenue for SOL becomes lower.

In Q4, DeFi faced a setback, with Solana experiencing the largest decline in TVL. The decline in TVL is typically assessed in dollars, so the drop in the value of native assets represents a change in the actual utilization of TVL relative to native assets in DeFi. While the dollar-denominated TVL dropped an astonishing 82%, the locked amount in SOL terms decreased by a smaller margin (39%).

Some developments in Solana's NFT space have allowed it to maintain a strong position in total secondary market NFT trading volume relative to the top five L1s (including Solana).

Although Ethereum continues to dominate the secondary NFT market, Solana remains strong in second place after Ethereum, far ahead of other peers.