A brief overview of China's regulatory attitude towards virtual currencies

The strict regulatory logic of our country regarding virtual currencies lies in cutting off all circulation of virtual currencies with fiat currencies (mainly the RMB) from the perspective of national financial stability, clearly defining the "non-monetary" nature of virtual currencies.

The strict regulatory logic of our country regarding virtual currencies lies in cutting off all circulation of virtual currencies with fiat currencies (mainly the RMB) from the perspective of national financial stability, clearly defining the "non-monetary" nature of virtual currencies.Author: Web3 Xiaolu

Source: DeFi Dao

To clarify the global regulatory compliance of Web3, one cannot avoid China. Firstly, regardless of our country's "one-size-fits-all" prohibition on virtual currencies, considering that most Web3 project teams are based in @PRC and the majority of users of Web3 projects are also from @PRC, it is essential to understand China's regulatory stance on virtual currencies, which helps in grasping the overall legal compliance risks of Web3 projects.

As of now, due to the domestic "one-size-fits-all" prohibition on virtual currencies, it is even more difficult to discuss a legal regulatory framework for virtual currencies. In contrast, Hong Kong has recently been continuously releasing favorable policies for Web3, indicating that the mainland is primarily developing the digital economy derived from the internet economy from the perspectives of blockchain (separation of currency and chain) and the metaverse, while Hong Kong is developing the digital economy derived from the traditional financial system from the crypto-native and virtual currency perspectives.

1. The "Notice on Preventing Bitcoin Risks" (the "289 Notice") in the Bitcoin Era

On December 3, 2013, due to the widespread international attention on a so-called "Bitcoin" calculated through specific computer programs, some domestic institutions and individuals took the opportunity to speculate on Bitcoin and related products. Therefore, the People's Bank of China, the Ministry of Industry and Information Technology, the China Securities Regulatory Commission, the China Banking Regulatory Commission, and the China Insurance Regulatory Commission jointly issued the "Notice on Preventing Bitcoin Risks" (Yin Fa [2013] No. 289) to protect the property rights of the public, safeguard the legal status of the Renminbi, prevent money laundering risks, and maintain financial stability.

Take Aways:

++(1) Correctly understand the attributes of Bitcoin: Bitcoin has four main characteristics: no centralized issuer, limited total supply, unrestricted use across regions, and anonymity. Although Bitcoin is referred to as "currency," it is not issued by a monetary authority, does not possess legal tender and coercive attributes, and is not truly a currency in the strict sense. Bitcoin should be regarded as a specific virtual commodity, lacking the same legal status as currency, and should not be circulated or used as currency in the market.++

++(2) Financial institutions and payment institutions are prohibited from engaging in any business related to Bitcoin, including: providing registration, trading, clearing, and settlement services for Bitcoin; accepting Bitcoin or using Bitcoin as a payment settlement tool; providing exchange services between Bitcoin and Renminbi or foreign currencies; offering storage, custody, and mortgage services for Bitcoin; issuing financial products related to Bitcoin; and using Bitcoin as an investment target for trusts, funds, etc.++

Since Bitcoin came under regulatory scrutiny, China has adopted a relatively cautious regulatory attitude, first directly denying the monetary attributes of Bitcoin, stating that "it is not issued by a monetary authority, does not possess legal tender and coercive attributes, and is not truly a currency," which can be regarded as the basic principle of domestic regulation of virtual currencies and has continued to this day. In judicial practice, courts have often recognized the validity of virtual currency trading contracts and classified Bitcoin and other virtual currencies as virtual commodities.

2. The "Announcement on Preventing Risks of Token Issuance and Financing" (the "September 4 Announcement") in the ICO Era

On September 4, 2017, due to the emergence of numerous financing activities through token issuance, including Initial Coin Offerings (ICOs), rampant speculation, and suspected illegal financial activities that severely disrupted the economic and financial order, the People's Bank of China, the Cyberspace Administration of China, the Ministry of Industry and Information Technology, the State Administration for Industry and Commerce, the China Securities Regulatory Commission, the China Banking Regulatory Commission, and the China Insurance Regulatory Commission jointly issued the "Announcement on Preventing Risks of Token Issuance and Financing" to implement the spirit of the National Financial Work Conference, protect the legitimate rights and interests of investors, and prevent and mitigate financial risks.

Take Aways:

++(1) ICOs are defined as unauthorized illegal public financing activities, clarifying the non-monetary attributes of tokens and prohibiting various token exchanges from providing exchange, trading, pricing, and information intermediary services.++

++(2) Accurately recognize the essential attributes of token issuance and financing activities. Token issuance and financing refer to the act of financing entities raising Bitcoin, Ethereum, and other so-called "virtual currencies" through the illegal sale and circulation of tokens, which is essentially an unauthorized illegal public financing activity and is suspected of illegal issuance of token vouchers, illegal issuance of securities, illegal fundraising, financial fraud, pyramid schemes, and other illegal activities. The tokens or "virtual currencies" used in token issuance and financing are not issued by monetary authorities, do not possess legal tender and coercive attributes, do not have the same legal status as currency, and cannot and should not be circulated or used as currency in the market.++

++(3) No organization or individual may illegally engage in token issuance and financing activities, including conducting exchange services between legal currencies and tokens, "virtual currencies," buying or selling tokens or "virtual currencies" as a central counterparty, or providing pricing, information intermediary, and other services for tokens or "virtual currencies."++

++(4) Financial institutions and non-bank payment institutions are prohibited from engaging in any business related to token issuance and financing transactions.++

On September 13, 2017, the China Internet Finance Association issued a "Notice on Preventing Risks of So-called 'Virtual Currencies' such as Bitcoin," clarifying that Bitcoin and other so-called "virtual currencies" lack a clear value foundation; various so-called "coin" trading platforms have no legal basis for establishment in China. Subsequently, various regulatory departments further alerted the potential risks of virtual currencies within their respective regulatory scopes. This also drove most virtual currency exchanges and related projects overseas.

During this period, both at the policy level and in judicial practice, it was believed that while virtual currencies do not possess monetary attributes, this does not prevent them from being recognized as commodities and receiving legal protection as general property. At the same time, in judicial practice, courts strictly followed the principle of "risk self-bear" in their rulings: although citizens' trading of virtual currencies is a personal freedom, such activities are not protected by law in China, and the consequences and risks arising from the transactions should be borne by the investors themselves. Parties engaging in illegal civil activities and claiming rights based on such activities should not receive support from the people's courts. Although the September 4 Announcement did not prohibit individuals from buying and investing in virtual currencies, since it defined ICOs as unauthorized illegal public financing activities, from the perspective of national policy, the number of court rulings denying the validity of virtual currency trading contracts began to increase.

3. The "Notice on Further Preventing and Handling Risks of Virtual Currency Trading Speculation" (the "924 Notice") in the Crypto Era

On September 15, 2021, due to the rise of virtual currency trading speculation activities, which disrupted the economic and financial order and gave rise to illegal activities such as gambling, illegal fundraising, fraud, pyramid schemes, and money laundering, seriously endangering the property safety of the people, the People's Bank of China, the Central Cyberspace Administration, the Supreme People's Court, the Supreme People's Procuratorate, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, and the State Administration of Foreign Exchange jointly issued the "Notice on Further Preventing and Handling Risks of Virtual Currency Trading Speculation" (Yin Fa [2021] No. 237) to further prevent and handle risks of virtual currency trading speculation and effectively maintain national security and social stability.

Take Aways:

++(1) Virtual currencies do not possess the same legal status as legal tender. Bitcoin, Ethereum, Tether, and other virtual currencies have the main characteristics of not being issued by monetary authorities, using encryption technology and distributed accounts or similar technologies, and existing in digital form, do not possess legal tender, and should not and cannot be circulated or used as currency in the market.++

++(2) Activities related to virtual currencies are considered illegal financial activities. Engaging in exchange services between legal currencies and virtual currencies, exchanges between virtual currencies, buying and selling virtual currencies as a central counterparty, providing information intermediary and pricing services for virtual currency trading, token issuance and financing, and virtual currency derivatives trading are all suspected of illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of futures business, illegal fundraising, and other illegal financial activities, which are strictly prohibited and resolutely banned by law. Criminal liability will be pursued for those engaging in related illegal financial activities.++

This regulation marks the first time at the national level that activities related to virtual currencies are recognized as illegal financial activities. All activities derived from virtual currencies (essentially all businesses that price and provide circulation for virtual currencies, most of which fall within the scope of exchange operations) are strictly prohibited within China and may even involve criminal offenses.

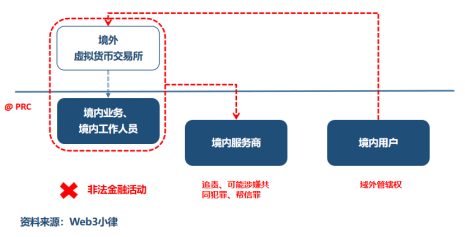

++(3) Overseas virtual currency exchanges providing services to residents in China via the internet are also considered illegal financial activities. For domestic staff of relevant overseas virtual currency exchanges, as well as legal entities, non-legal entities, and individuals who knowingly or should know that they are engaging in virtual currency-related businesses and still provide marketing, payment settlement, technical support, and other services for them, legal responsibility will be pursued.++

This regulation marks the first time that the domestic operations of overseas exchanges are classified as illegal financial activities. It can be understood based on the principles of China's criminal jurisdiction in three parts. First, for domestic staff of overseas exchanges @PRC, engaging in illegal financial activities may involve financial crimes such as illegal business operations, illegal public deposit absorption, fundraising fraud, and organizing and leading pyramid schemes.

Secondly, for service providers (such as third-party technical outsourcing, media public relations, and bank settlement) @PRC for overseas exchanges, since the business of the service object falls under illegal financial activities, the service providers may be held legally responsible, and in severe cases, may be suspected of joint crimes or separate aiding crimes.

Finally, if overseas exchanges provide virtual currency services to Chinese citizens @PRC via the internet from outside China's jurisdiction and engage in corresponding actions that violate Chinese law, they will still be subject to Chinese law. Furthermore, if the illegal financial activities of overseas exchanges constitute a crime, as long as the location of the information network system used by the victim, the location of the victim at the time of infringement, and the location of the victim's property loss are all in China @PRC, Chinese judicial authorities will have extraterritorial jurisdiction.

++(4) Participating in virtual currency investment and trading activities carries legal risks. Any legal entity, non-legal entity, or individual investing in virtual currencies and related derivatives that violate public order and good customs will have their related civil legal actions deemed invalid, and any resulting losses will be borne by themselves; those suspected of disrupting financial order and endangering financial security will be investigated and dealt with by relevant departments in accordance with the law.++

The emergence of this regulation has had a significant impact on subsequent civil judicial adjudications related to virtual currencies, with many cases arising from disputes over entrusted purchases and investments. Courts, based on recognizing the activities involved as illegal financial activities, will deem related civil legal actions invalid if they violate public order and good customs, and any resulting losses will be borne by the parties themselves. In conjunction with Article 157 of China's Civil Code, if civil legal actions are invalid, revoked, or determined to have no effect, the property obtained by the actor from such actions should be returned; if it cannot be returned or does not need to be returned, compensation should be made at a discounted price. The party at fault should compensate the other party for the losses incurred; if both parties are at fault, they should each bear corresponding responsibilities.

4. Conclusion

Through the above analysis, China's strict regulatory logic regarding virtual currencies lies in cutting off all circulation of virtual currencies with legal currencies (mainly the Renminbi) from the perspective of national financial stability and clarifying the "non-monetary" attributes of virtual currencies, which includes the issuance (ICO) and trading (legal currency exchange, currency-to-currency exchange) of virtual currencies—two important businesses of virtual currency exchanges. On this basis, criminally combating fraud, illegal public deposit absorption, pyramid schemes, money laundering, and other crimes arising from the attributes of virtual currencies, while clarifying the legal relationships for the parties involved at the civil level.

This can be simply summarized as follows:

(1) Virtual currencies do not possess monetary attributes and should not and cannot be circulated or used as currency in the market. Activities related to virtual currencies are considered illegal financial activities, and overseas virtual currency exchanges providing services to residents in China via the internet are also considered illegal financial activities.

(2) Any organization or individual is prohibited from illegally engaging in virtual currency issuance and financing activities, and all financial institutions and non-bank payment institutions are prohibited from conducting businesses related to virtual currencies.

(3) There has been no definition regarding the act of holding virtual currencies itself, meaning that holding virtual currencies remains a behavior not explicitly prohibited by law.