How should Web3 projects issue tokens?

From the perspective of the project party, analyze the issues to pay attention to when issuing tokens, common strategies, and best practices.

From the perspective of the project party, analyze the issues to pay attention to when issuing tokens, common strategies, and best practices.Original Title: 《Tokenomics 104: How to Launch a Token》

Author: Nat Eliason

Translation: Lu, WhoKnows DAO

When designing a project or researching a project's tokenomics, there is an important question—how will these tokens get into the hands of users?

You must pay attention to this aspect, as the method of token release can significantly impact whether the project achieves long-term success. If you are the founder of a project planning to issue tokens, you need to ensure you have a good token release plan that allows users to purchase it without jeopardizing the project's prospects.

Therefore, whether you are part of the project team or a researcher, here are my thoughts on how to deliver tokens to users.

I have divided this topic into three parts:

- Considerations during issuance: including how many tokens to initially issue, liquidity requirements, incentives, key milestones, token pairing, and when to issue.

- Issuance strategies: including ICOs, IDOs, liquidity bootstrapping, liquidity incentives, liquidity bonds, interactive rewards, and airdrops.

- Case studies: breaking down the initial release strategies of some projects and highlighting what I think they did well.

In the end, you will understand everything about issuing tokens or evaluating a new token issuance strategy.

### 1. Considerations for Token Issuance

Unless you have enough funds and connections to list immediately on Coinbase or another major CEX, you must start by using a DEX to issue your tokens on-chain.

Your primary goal is to make it easy for people to purchase this token, rather than complicating, making it expensive, or unstable.

This means you need:

- A recognized, easy-to-use exchange for people to buy the token;

- A popular trading pair for people to exchange your token;

- Sufficient liquidity for most people to buy your token;

You also need to figure out:

- How many tokens to release;

- The initial pricing scheme;

- Whether you need others to provide seed liquidity for your token;

- When to issue;

Appropriate Channels & Simple Processes

The first question to solve is: On which chain should I issue these tokens?

You may already have an idea, but if not, take some time to research the various public chains you can use based on the direction you want to optimize.

If you want maximum security and liquidity (beneficial for DeFi), you may need to issue your tokens on Ethereum or Arbitrum.

If you are a gaming project that requires faster transaction speeds and lower costs, consider Polygon, Solana, or Avalanche.

Or if you feel adventurous and want to bring people to Moonriver, Celo, Harmony, or other public chains, I wouldn't recommend it, but if they offer you a large sum of money or you have reason to believe you can attract people there, go for it.

Once you've chosen a chain, you need to select your exchange. Uniswap and Sushiswap are always safe choices. Additionally, you can choose the leading exchanges on the chain your project is on, such as QuickSwap on Polygon, Trader Joe on Avalanche, or Raydium on Solana.

A common best practice at project launch is to list on only one exchange initially, so you don't dilute liquidity too much. While it may seem tempting to list tokens on multiple exchanges, it can degrade the user experience for those making large trades. If not necessary, do not increase the entities.

Once you've chosen the exchange for your token launch, the next question is: What token will you pair with?

Choosing Your Trading Token

Any trade on a DEX requires two tokens: the token you want to buy and the token you use for trading.

When issuing a token, you must choose another token to pair with your token. When making this decision, you should consider the following points:

First: Make it easy for users to purchase your token. If you choose a common, highly liquid pairing token like ETH, users will find it easy to buy your token since they already have ETH. If you choose a less common token, it could hinder the user experience, as people may have to buy another token first.

Second: How it affects the price of your token. The price of tokens on a DEX is determined by the ratio between the two tokens in the trading pool. Therefore, regardless of which token you pair your token with, its value will be influenced by the value of the other token.

Imagine your trading pair is ETH. If there are 1,000 ETH and 10,000 of your issued tokens (YourToken) in the trading pool, then YourToken is worth 0.1 ETH. If ETH rises 10% against the dollar and no trades occur in the pool, then YourToken will also automatically rise 10% against the dollar, as it maintains the same ratio with ETH.

Thus, if you want your token to keep pace with the broader cryptocurrency market, you should choose a trading token like ETH. If you want it to be more stable or reflect your business situation, then pair it with USDC.

Once this is handled, you need to consider how to provide sufficient liquidity for trading.

Providing Sufficient Liquidity for Trading

After you list your token on a DEX, you will have to provide initial liquidity for trading that token.

The more popular your product is, the more liquidity you will need to allow users to trade internally. For example, if a user wants to purchase $10,000 worth of tokens, you need enough tokens and ETH in the pool to ensure the user's trade is not affected by significant slippage.

Therefore, regardless of how much you can envision someone's maximum trading amount to be, you may need at least 10-20 times that in liquidity. The smaller your project, the less you need. However, if you are still on a CEX, you may need a deep liquidity pool.

If you plan to increase liquidity through incentives (which we will discuss later), you may not need to start with so much. However, if you want to provide liquidity yourself without paying for the liquidity provided by others, you will need a considerable amount of funds initially.

Assuming you want your token to have at least $2 million to $5 million in liquidity. If the initial CEX is very aggressive, you will need even more. This means you will need at least $1 million in ETH (or whatever your trading token is) as initial liquidity to pair with your token.

Thus, you need to have strong financial backing, raise funds from investors, or only provide a portion of liquidity (perhaps only $100,000 to $250,000) and incentivize others to fill the remaining liquidity gap.

The next topic will focus on this issue—you need to figure out how many tokens to issue.

Token Issuance Amount

This is a seemingly tricky question because it requires you to find an optimal solution that meets all requirements regarding the initial target price of the token, your liquidity constraints, your inflation rate, and your community ownership.

For example, suppose there are only $250,000 worth of ETH paired with your token. If you initially release 10% of the tokens through LP, then your FDV will be set at $2.5 million, which is quite a low expectation for a crypto project.

Someone could spend $50,000 to buy your tokens, and they would now hold 2% of the total supply. What strong control!

So maybe you want a higher initial FDV so that whales won't easily control the market and dump later. You initially release only 2.5% of the total supply of tokens, so now the FDV is $10,000,000. You've solved the whale problem, but now you need to figure out how to issue the remaining 97.5% of the tokens.

With only 2.5% of the tokens in circulation, you can almost guarantee that the initial buyers will face significant inflation pressure later on. A large number of new tokens will need to be released into the market later, making it difficult for the token to maintain its price and ensuring the interests of early investors.

Well, you want to release 10%, and you want a $10,000,000 FDV. Now you need $1 million in liquidity to pair! Do you see the problem?

Your options are basically:

- To reduce inflation and limit liquidity requirements, there is a risk of losing project control too early;

- Invest a large amount of initial liquidity so you can control inflation;

- Maintain control while using limited liquidity, which will lead to significant inflation, unfavorable for early investors;

Unfortunately, these are all trade-offs that need to be weighed, and there really is no way around them; your choices will always come with pain.

Around this topic, you need to determine what kind of target price you want.

Target Price of the Token

This can be said to be the hardest question to answer here because you will certainly go wrong in one direction or another.

You might set the price too low, missing out on millions you could have earned with better pricing.

Or you might price it too high, causing anyone to dump immediately after acquiring the token, leading to a loss of initial liquidity.

For this, I have some mental models to help you make decisions.

First, I think it's best to set the price a bit lower. Users will be more satisfied, and you can still benefit from the remaining tokens in your possession, while also scratching the itch of users wanting to "get in early and make money."

Second, assuming you don't want to do an ICO-type token issuance, I think you should decide based on the available liquidity reserves and the percentage of the initial release of tokens, then observe the price fluctuations. If you have $500,000 available for liquidity and only want to initially release 10% of the tokens, then logically, your FDV is $5,000,000.

Third, it's worth considering how you want the initial batch of tokens to reach users. Are you planning to establish a liquidity bootstrapping pool? A presale? These can help you plan a target for initial pricing. Alternatively, if you are conducting an airdrop, you must consider what price is low enough to prevent people from dumping immediately after receiving the tokens.

Through this part of the thinking, you may realize that you urgently need support from others in providing liquidity. Next, let's talk about this.

Do You Need Others to Provide Liquidity?

Perhaps you calculated in the previous questions and realized that you do not have enough funds to build a liquidity pool for user trading; you need external funds to do this.

You have several options. You can conduct a presale or ICO early on (though we don't call it that now) to raise some funds and then use that money as initial liquidity.

You can also use liquidity incentive pools (which I will introduce below) to raise funds, which helps improve liquidity and assists in calculating a reasonable initial price for the token.

Alternatively, you can conduct liquidity incentives immediately after issuance. When you only have $100,000 to $250,000 in funds, this is a good option, but you know that some members in the community fund will farm your tokens. You have to accept one thing: in the first few days after launching the token, your price curve will exhibit a spike pattern. Frankly, I prefer this strategy; it is most suitable for teams using LBP, and I will explain why later.

Now, the last question—when to issue the tokens?

When to Issue Tokens?

There is no optimal answer to this question; I believe you should meet your functional and funding needs as late as possible.

If you are a resource-constrained guiding team, you may need to issue tokens earlier to fund development. Many teams have successfully navigated this process and made good progress, while many others have collapsed or run away after doing so.

Another issue is the utility of the token. If certain features within the application require its consumption, then it clearly needs to be issued before or at the same time as that feature goes live. If it is a governance token or represents the scale and economy of the project, it can be issued a bit later.

But I would never try to issue tokens immediately. If you don't need the tokens and can afford to build the project for a while without using them, then the early stages of the project are not a good time to issue tokens. The more patient you are in waiting, the more control you will have over the project, the more stable the project will be, and you can invest more time in building without the interference of token prices. Once a token price starts to affect community sentiment, the feeling of building becomes different.

So, wait as long as possible; if you don't urgently need money and there are no use cases for the tokens, please continue to wait.

Now you have understood all the considerations for issuing tokens:

- Which exchange to list on;

- What trading token to pair with;

- How much liquidity to invest;

- What the issuance amount of the token is;

- What the target price of the token is;

- Whether you need external help;

- When to issue;

Next, we can talk about the tools and strategies you can use when issuing tokens.

### 2. Token Issuance Strategies

These strategies can be picked individually as needed. There are many ways to address issues like how to issue to the market, how to raise funds, how to incentivize the community, and support your project in development.

We will cover the following content:

- ICO;

- IDO;

- Liquidity bootstrapping;

- Liquidity incentives;

- Liquidity bonds;

- Interactive rewards;

- Airdrops;

ICO

This is the earliest method of releasing tokens to the market, and we rarely see it now. You set up a website, set a price in ETH, and then people can trade your tokens with their ETH.

It is now generally considered a securities transaction, with legal risks, so you won't see it anymore. It also feels a bit bland because there won't be any market price appreciation after the sale, nor will there be liquidity after the transaction is completed.

Private placements are a method that still exists today. Some projects will raise a certain amount of funds from investors before launching and promise to provide them with tokens after the launch. This is a common way to address initial liquidity issues, as you can use the funds you raise to provide liquidity for your public token issuance.

Another method is through a creative approach we call donations, where you can donate some ETH to a contract and then receive some tokens in return. It's basically an ICO with an extra step. You can adopt this idea, and I will explain it in other cases.

IDO

In the previous section, we discussed increasing liquidity by going to exchanges like SUSHI or Uniswap, injecting your tokens and paired tokens into the pool, allowing people to start trading with it.

This is how you launch token trading, and the reason we call it an IDO is that it occurs on a DEX rather than being sold on the project website initially.

Recently, almost all projects consider IDOs as the starting point for issuing tokens, even if you airdropped some tokens beforehand (which is usually a bad idea, as explained below), those tokens have no value until there is liquidity to trade.

Therefore, in almost all cases, your IDO should coincide with the token issuance. That is when people can trade it, and it is also when you are troubled by the aforementioned issues.

This is an important moment! Celebrate briefly, then brace for months of anxiety as you watch your company's value fluctuate dramatically every hour.

LBP

When you do not have enough liquidity funds for an IDO to reach your target price, liquidity bootstrapping pools are an elegant solution.

Instead of conducting a private placement or creating a small liquidity pool that leads to huge fluctuations, or risking significant pricing, you can host a liquidity launch event to raise funds for your initial liquidity and let the market determine the initial token price.

Copper Launch is a popular LBP tool. You inject some initial liquidity at a very high token price, and as more people join the liquidity, the price will decrease over time until people no longer find it worthwhile to join the liquidity fund for some token dividends.

At this point, the market price of your token has roughly been determined, and you can close the pool to claim the share of funds and distribute tokens. Then you can use these newly claimed funds to create liquidity for everyone's trades.

The benefit of this strategy is that you will find a good token issuance price, which is favorable for early investors. The downside is that you will end up releasing some tokens early, so you must set up some redemption mechanisms for your real tokens to prevent front-running.

You may also have a large number of tokens flowing without authorization, so you need to figure out how to set the parameters for the launch pool so that early investors do not dump immediately. This complicates the strategy, but it is a simple way to solve the fundraising and pricing issues.

Liquidity Incentives

This is a very common mechanism used to distribute tokens and address liquidity shortages. You do not have to create all the trading liquidity yourself; instead, you can first inject some initial liquidity and then pay people to add more liquidity.

Here's how it works:

- I issue a NAT token;

- I pair it with ETH and inject liquidity worth $250K;

- I distribute 10% of the total NAT supply as liquidity incentive funds, through 4 years of staking;

- So, after you purchase NAT tokens, they will be paired with ETH and injected into the liquidity pool, then establish a liquidity position on my website, earning NAT token rewards passively;

In this model, you rent liquidity from your users by paying them tokens to help fund your liquidity pool for a period. This is very useful for rapidly increasing your liquidity position (Crypto Raider increased from $200,000 in liquidity to over $10 million this way), but over time it can become expensive. It depends on how many tokens you give out; you may lose a significant amount of money to maintain your current liquidity.

That said, this is a good way to establish liquidity in the early stages. You just need a transition period, and a common method is liquidity bonds.

Liquidity Bonds

Bonds are a solution to the liquidity leasing problem, popularized by Olympus.

The way liquidity bonds work is that you offer tokens to users at a slightly lower price in exchange for some of their liquidity positions.

Therefore, instead of continuously paying tokens to users to maintain the same amount of liquidity, you can have them trade their liquidity positions to you in exchange for more tokens.

This allows your community members to still earn a good return on investment by providing liquidity to your tokens, enabling you to gradually build ownership of liquidity over time without risking the community taking ownership of your tokens.

In the long run, this approach is more sustainable, but it can be more challenging in the early stages. There needs to be enough liquidity for people to trade internally before they can start selling liquidity back to you, so generally, project teams will start with normal liquidity incentives and then transition to liquidity bond strategies over time.

While there are many different ways to incentivize liquidity, the simplest way to issue liquidity bonds is to partner with Olympus Pro. They will charge a small fee, but relying on their team to handle the entire process is worth it, as all aspects will be taken care of.

The above are ways users can obtain your tokens through paid means, but there are also ways for people to acquire them for free.

The first is through interactive rewards.

Interactive Rewards

Granting token rewards to users of the application is an essential part of the Crypto spirit. If there is any way to embed this mechanism into your application, you should do so. It's just part of the Web3 spirit, you know?

The question is how to obtain them and how much to receive. There are infinite combinations to form a scheme, but I will give you some entry points as a starting point.

First, I like to view this method as the largest source of token release for a project. In my STEPN article, I mentioned how wonderful it is for teams to give away 30% of the tokens to users of the application. Convex and Curve also do well in this regard, rewarding those who provide liquidity to their platform.

There may be an obvious way for projects to reward the top users of the platform with tokens, so be sure to think about how to incentivize user engagement through interactive rewards, rather than just letting your users farm and dump. If you want to learn more about this aspect, please check Tokenomics 103.

Second, if the difficulty of obtaining tokens increases over time, this is usually a good thing. A higher early release volume will lead to significant user growth and incentivize them early on. Then you can gradually reduce the incentive levels so that later users will still be rewarded for joining, just not as much as your earliest users.

Finally, you need to find a way to slightly lock the incentives, which will help prevent arbitrage and dumping. For example, one option is a one-week lock-up period, where arbitrageurs must apply first to receive rewards. Tokemak does this well, where rewards will be distributed after a few days, with a seven-day lock-up period for users.

In addition to interactive rewards, another way to distribute tokens for free is through airdrops.

Airdrops

Everyone wants to get something for nothing, so if you can provide funds to early users without affecting the health of the project, you should do it.

This can be based on historical application usage, such as holding NFTs, being another project participant, or even being an early member of the DC.

One important thing to note is that early recipients of airdropped tokens will not sell them immediately. You need to establish some initial lock-up mechanism or staking mechanism to help avoid this issue. Alternatively, you can incentivize those users to re-stake their tokens at the moment the airdrop is realized, which can mitigate the soaring inflation rate during that period.

Another thing you must be cautious about is creating a situation where multiple wallets can witch-hunt your airdrop. Announcing an airdrop in advance will invite people to try to exploit it; usually, an airdrop is announced only after a snapshot of the recipients has been taken. You need to design a participation balance mechanism to prevent users from creating 10 addresses to do this, making the airdrop fairer.

You now understand the various issues to face when issuing tokens and the various strategies for token issuance.

### 3. Token Issuance Case Studies

Now let's look at some examples and ideas from projects regarding token issuance:

Saddle Exchange: Vesting Airdrops

Saddle is a fork of Curve on Ethereum, Fantom, Optimism, and Arbitrum, used for swapping two equally valued tokens.

Saddle operated and captured liquidity for six months without mentioning token issuance. Then, when they released their tokenomics plan, a significant portion of the tokens was allocated to early liquidity providers.

15% of their total token supply was allocated to early liquidity providers. However, users cannot immediately receive all tokens and dump them; the tokens will be granted over two years, and their trading permissions will be determined through community proposals.

I like this method of airdrop. It has a slower release rate, avoiding the one-time distribution of a large number of tokens, and requires users to continuously use the platform to at least check the tokens they unlock.

In contrast, the ordinary airdrop method allows people to receive all tokens at once, but this often yields poor results.

Therefore, if you plan to conduct an airdrop, consider adopting a strategy similar to Saddle's.

JPEG'd: Donations

When JPEG launched their token, they sold the initial 30% of tokens through a "donation" event.

You send ETH to a contract and receive 30% of the token share, and once all donations are collected, you will receive JPEG tokens, with the number of tokens depending on your contribution relative to the total.

For them, adopting such a strategy was crucial because they needed a massive liquidity pool to hold NFTs as collateral. If people borrow against their NFTs, JPEG needs to be able to quickly liquidate those NFTs, so raising a large amount of funds through the donation event makes sense.

In this way, everyone injects funds into the contract, and then based on the user's contribution relative to others, they receive a portion of the tokens, allowing for a more natural price discovery.

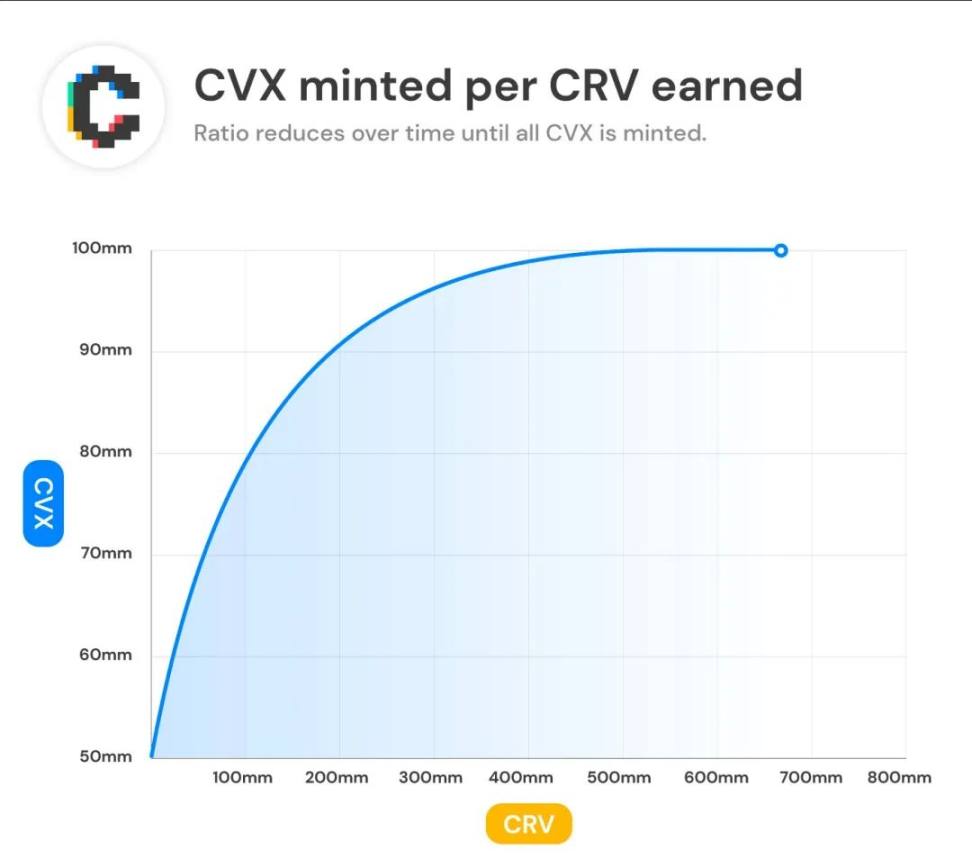

Convex: Airdrop & Interactive Rewards

Every article I write about tokenomics mentions Convex. Their rewards primarily focus on new and existing Curve liquidity providers, bringing a significant amount of liquidity to Convex's new platform.

First, they airdropped 1% of CVX tokens to veCRV holders. Then, they allocated 50% of the CVX release amount as rewards for platform interactions, incentivizing users who stake Curve liquidity tokens, with the release rate steadily decreasing:

Thus, depositing liquidity into Convex early is beneficial for users, but as the CVX release amount gradually decreases, the value begins to rise. Even though you receive fewer tokens, you can still achieve a good annual yield by maintaining your Curve LP curve.

Since their goal is to attract as much Curve liquidity as possible, this is a good way to release Convex tokens to target users.

Redacted: Strategic Asset Bonds

Redacted Cartel has adopted an interesting strategy based on Olympus's bond project. They released their BTFLY tokens to the market, tokenizing users' other assets to execute Curve War strategies:

Thus, they no longer issue ordinary liquidity bonds for their tokens, nor do they use ETH as a trading token, but instead allow people to trade BTRFLY tokens at a discount using other tokens like CVX and CRV.

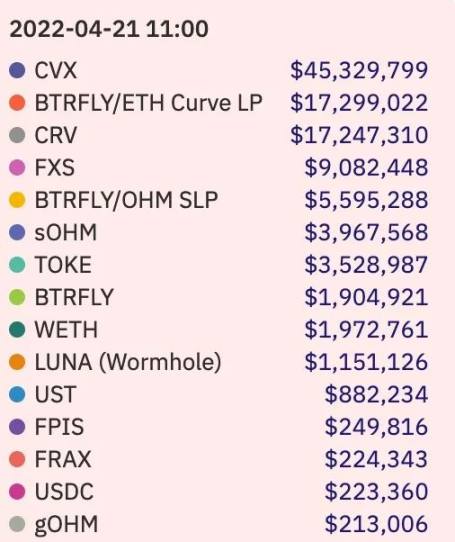

This makes them one of the largest holders of these tokens:

These are some of the more interesting token issuance ideas I have seen recently, and more imaginative strategies are emerging every week.

Now you have understood the basic issues of token issuance and the strategies that can be used during token issuance, allowing you to find good entry points in a token issuance plan or evaluate a project to see how other teams have launched their tokens.