Utility of Tokens

Original Title: 《Tokenomics 103: Utility》

Author: Nat Eliason

Compiled by: Lu, WhoKnows DAO

01 Introduction

In the first part of the tokenomics series, we introduced the high-level concepts you need to understand when evaluating a company's or project's token. In the second part of this series, I discussed how to analyze the token supply, including aspects such as emission rates, the relationship between market cap and FDV, total supply, and token distribution. In the third part, I will introduce the utility of tokens. Utility is a branch topic on the demand side of building a tokenomics model. Even if a token has a good supply model, it still needs a good reason for people to hold it. If a token is not useful, there will be no demand for it, and no one will want to buy or hold it. Let’s dive into the issue of token utility, and here are the scenarios in which tokens can be useful:

- Spending vs Holding;

- Cash Flow;

- Governance;

- Collateral;

02 Spending vs Holding

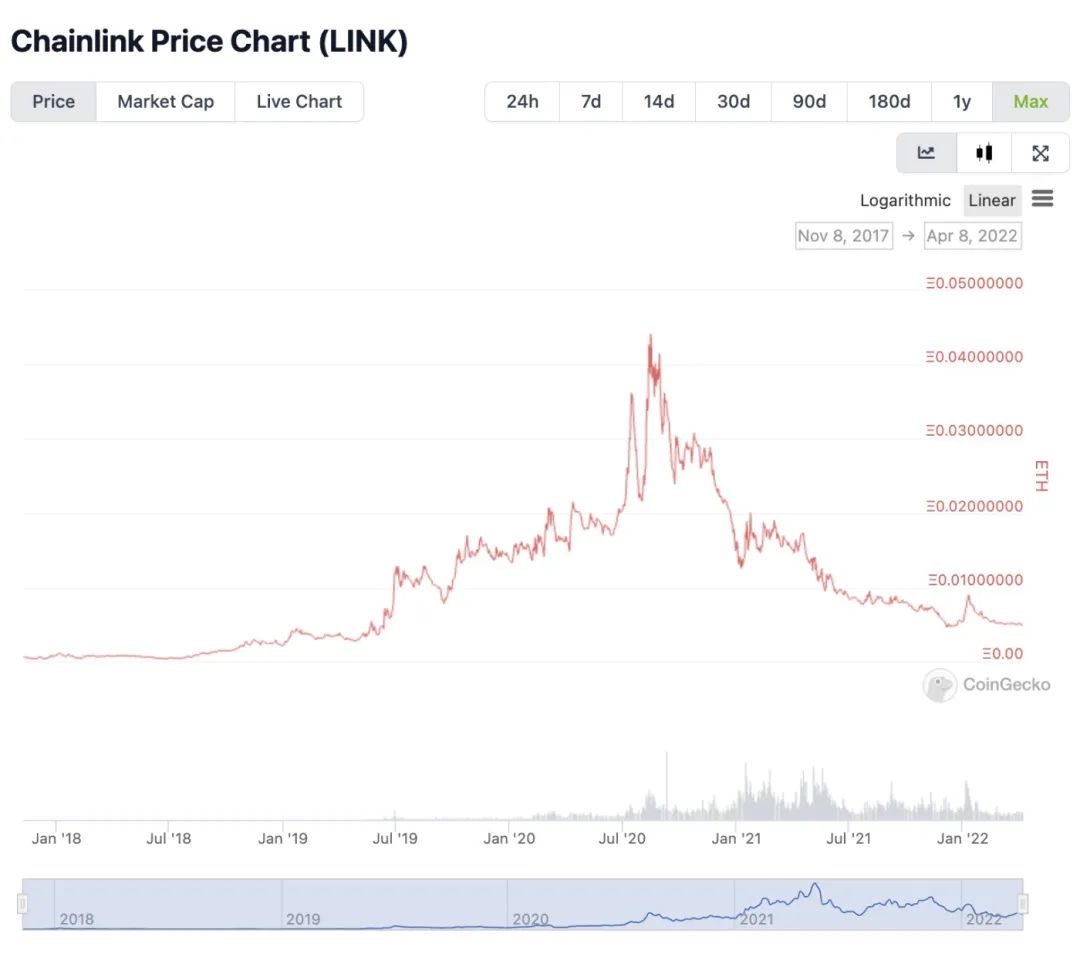

When we are trying to understand a token, the first question to clarify is: Are you holding this token to pay for the costs of using the protocol? Or is it for investment? If this is a token you should spend, then there is no point in holding it long-term. You can buy it in small amounts when needed. Therefore, clarifying what these tokens can be used for is one of the first things you should research. For example, let’s look at Chainlink. Chainlink is one of the most important services in the crypto world. It is absolutely core infrastructure for keeping DApps running smoothly. So, buying LINK should be a good investment, right? However, unless you bought in mid-2019, the situation is not as we might think. Take a look at the chart below:

If you bought LINK after July 2019 and held it, you have lost 50-90% of its value. Why is that?

At first glance, LINK seems like a good investment target. Limited supply, valuable infrastructure, everything looks great. However, the problem lies in the use case; the LINK token is primarily used to pay for Chainlink's services. It is a consumption token, not an investment token.

If you hold LINK, the only thing this token can do is pay for Chainlink's services. This service is very important, and you can buy it on-demand without needing to purchase tokens in advance.

This year, Chainlink is launching staking tokens to share revenue, but we do not know the specific details or the launch time. So, the only current use for LINK is to consume their services.

Another issue with spending tokens as investment targets is that the parent platform does not want to see the token price rise parabolically. If LINK appreciates significantly, all of Chainlink's services will become more expensive, and users may seek alternatives. It might make more sense for Chainlink to have two tokens: one for paying for platform services and one for staking investment, but that’s another topic.

Currently, LINK has the following issues as an investment target:

- This token is for consumption;

- Chainlink does not want its service prices to become too expensive;

- For LINK holders, there is no cash flow or other use cases;

Again, I want to emphasize that Chainlink is one of the most important projects in this field, but that does not mean their token has the same investment value!

Another good example is the game tokens used in P2E games, such as SLP from Axie Infinity or AURUM from Crypto Raiders.

When you earn AURUM in Crypto Raiders, it is primarily used for recruiting or exchanging for dungeon keys. It should not be held long-term because its supply is not fixed, and its inflation rate keeps changing. It also does not generate cash flow, cannot be used for governance, and has no utility beyond spending. The same goes for SLP; it has a price range for appreciation, but that does not mean it is an investment. For Axie Infinity, the investment token is AXS, while for Crypto Raiders, it is RAIDER.

Therefore, when researching a token, the primary question should be whether this token is used for consumption in the app or provides some compelling long-term investment opportunity, rather than just consumption.

03 Cash Flow

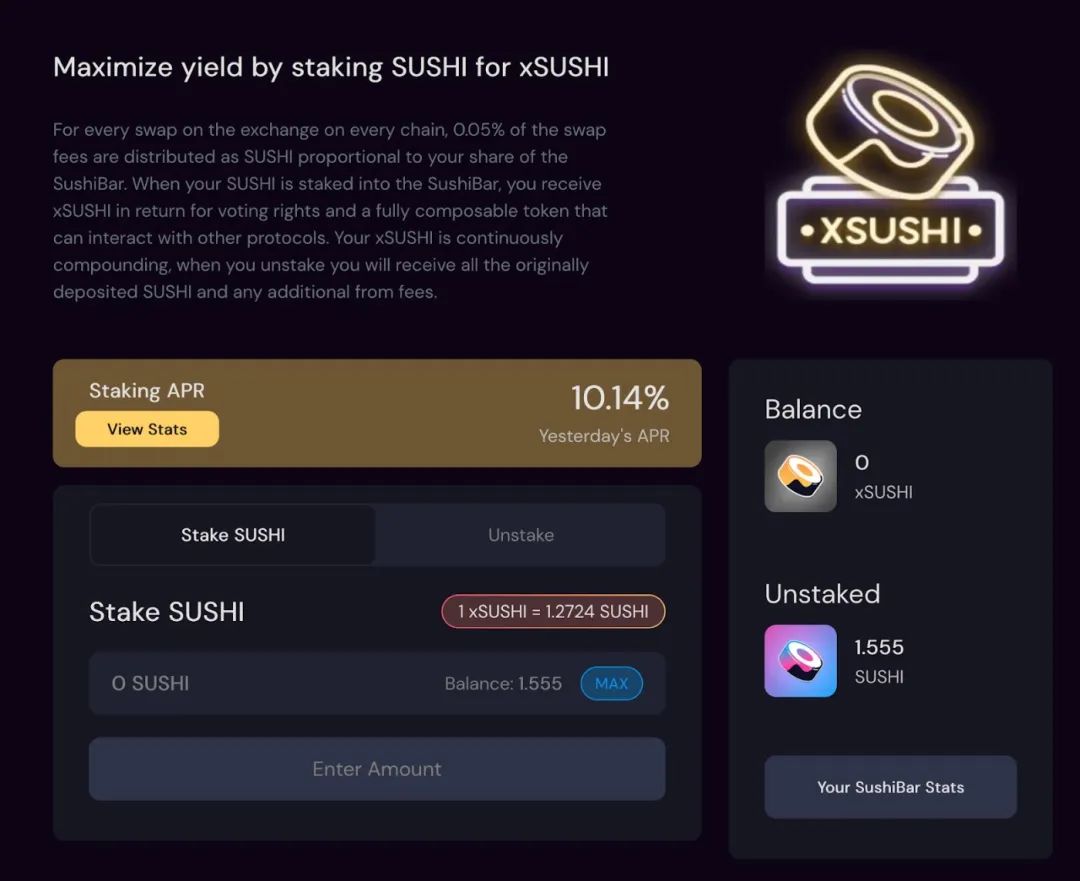

If you are going to hold a token rather than consume it, the next question will be: Why hold it? The most common compelling use case is cash flow generated from holding the token. If there are mechanisms that allow you to earn returns while holding and consuming the token, they are worth buying. Although they may not maintain price stability as BTC and ETH do over the long term. Fee sharing is one way to achieve this mechanism. If you buy SUSHI, you can hold it and invest in the long-term value of SushiSwap. Alternatively, you can stake SUSHI to earn xSUSHI, a way to earn a share of all the fees generated by the platform.

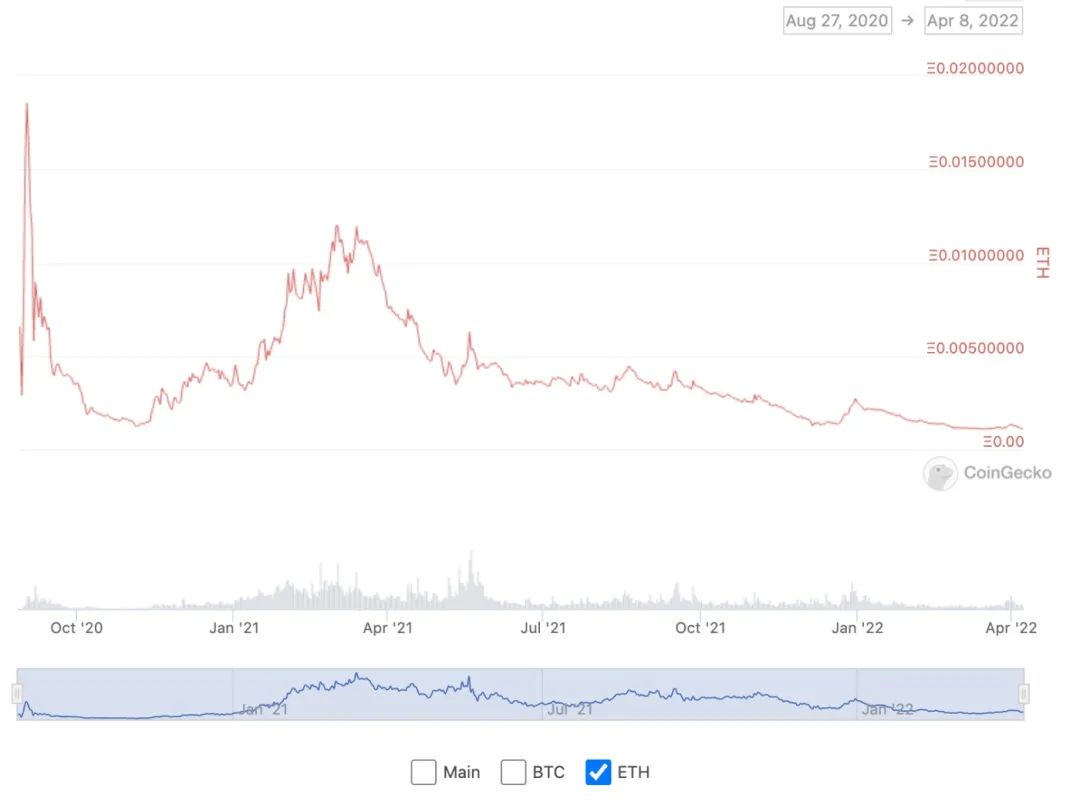

xSUSHI is a "liquid staking token." To earn trading fee shares, you must stake your SUSHI. Additionally, the redemption price of xSUSHI will increase over time. This makes you want to hold this token wherever you are to avoid using them as collateral for secondary loans on platforms like AAVE. Earning a 10% annual interest rate is much better than holding regular SUSHI tokens with 0% yield, but we must consider the value fluctuations of yield-bearing tokens. In the case of xSUSHI, because the value of SUSHI itself has been decreasing compared to ETH and other mainstream tokens, the 10% APR returns are not enough to offset the losses from token depreciation unless you bought SUSHI in November 2020; otherwise, this trade would be poor.

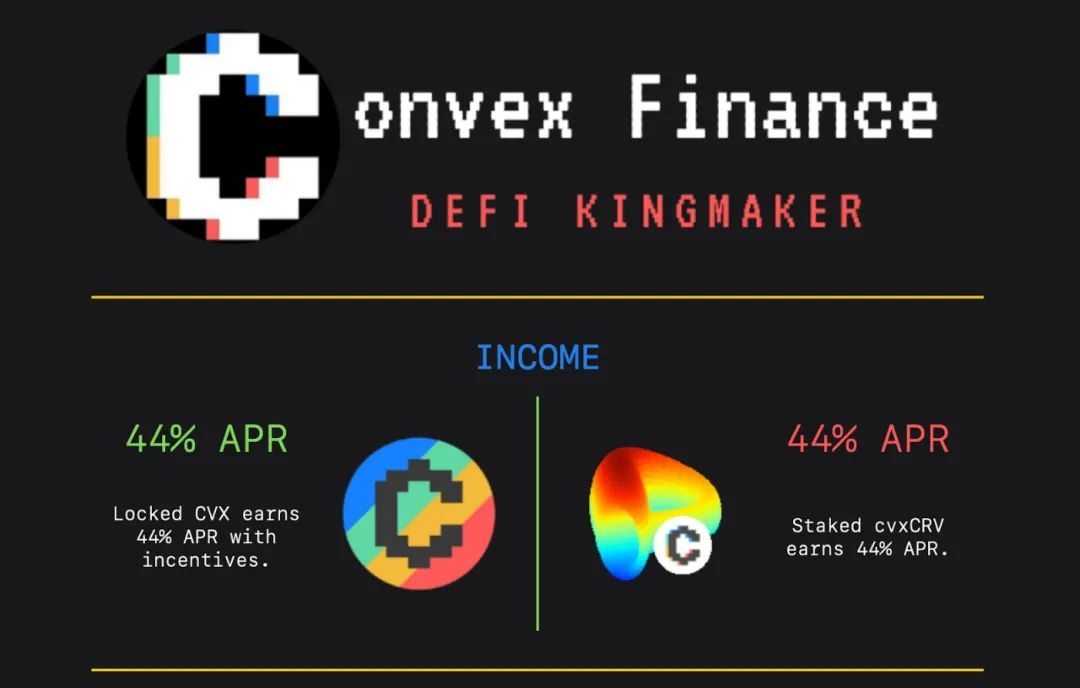

Convex, which I often talk about, is another token that can generate cash flow. According to Llama Airforce Union (all information has been discussed in the article on The Curve Wars), the current annual yield for locked Convex is 44%.

Moreover, if you look at Convex's performance against ETH, you will find it performs much better.

So, this token currently has a good appreciation situation against ETH and pays a 44% dividend. This is a win-win situation. Although buying CVX in January would have been at its price peak, the approximately 10% ROI from the last three months has compensated for a significant portion of the decline since then. For a token's cash flow, you ultimately need to ensure how it is generated. If staking these tokens merely earns you more of the same tokens and they are released into the market, you are not really earning anything; you are just avoiding the dilution of your token value. You want to find a cash flow project based on actual income, ideally without paying you in the tokens you are staking.

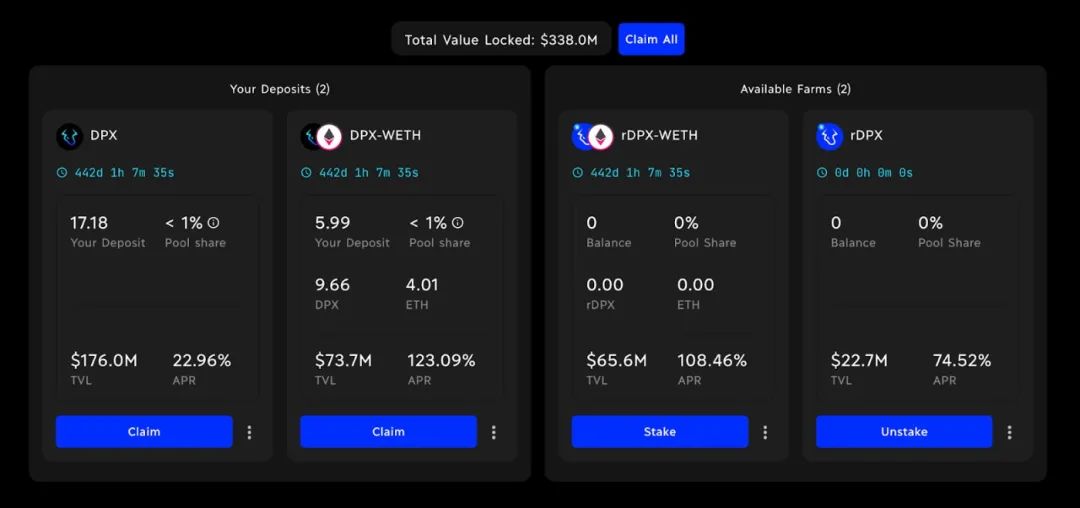

Convex pays various tokens based on your staking. In Crypto Raiders, when your RAIDER is staked, you earn rebates based on the AURUM consumed in the game. However, for the current Dopex, staking income is paid in DPX and rDPX, which is a way of token release until their revenue sharing plan begins. Therefore, its cash flow system is not as good as Convex, but it at least reduces the pressure of your token share being diluted in the protocol. In the near future, this system will transition into a real income-sharing system.

For me, cash flow is the most interesting way to earn returns using tokens. If it is a token you want to hold, then holding it should be more worthwhile than just holding ETH. In addition to investing in the future value appreciation of the token, cash flow is also a good method. However, there are other factors to consider, and the next one is governance.

04 Governance

If you are very fond of a protocol and want to participate in their decision-making, governance is a way you can invest in the utility of a token, even if it may not meet some of the standards we mentioned above. For example, here is a chart of AAVE against ETH:

But the AAVE community is very active, and most governance proposals attract 250,000 to 400,000 votes:

Therefore, if you belong to another DeFi protocol, a venture capital firm, or a whale, or simply want to make an impact on AAVE's future decisions, holding some AAVE tokens to propose and vote is worthwhile.

Personally, I do not find this right to be attractive enough. I would rather believe that AAVE's development will be achieved through centralized decision-making on the platform. But in some cases, there is arbitrage potential in this scenario. Technically, Convex's cash flow is earned by bribing governance votes, so if the protocol has governance votes that can have a significant impact, securing a seat at the decision-making table can be profitable.

If you are holding DAO tokens, governance rights are also a significant benefit. The more Cabin DAO tokens you hold, the more influence you have in major decisions at Cabin, such as how funds are used and who can become partners. The same goes for other well-known DAO organizations, such as FWB.

Therefore, if your goal is to participate in the governance of a community, the governance rights brought by the token will be substantial. If you are pursuing maximum ROI, merely considering governance rights is somewhat insufficient.

So, the last thing to consider before holding a token is whether this token can serve as collateral.

05 Collateral

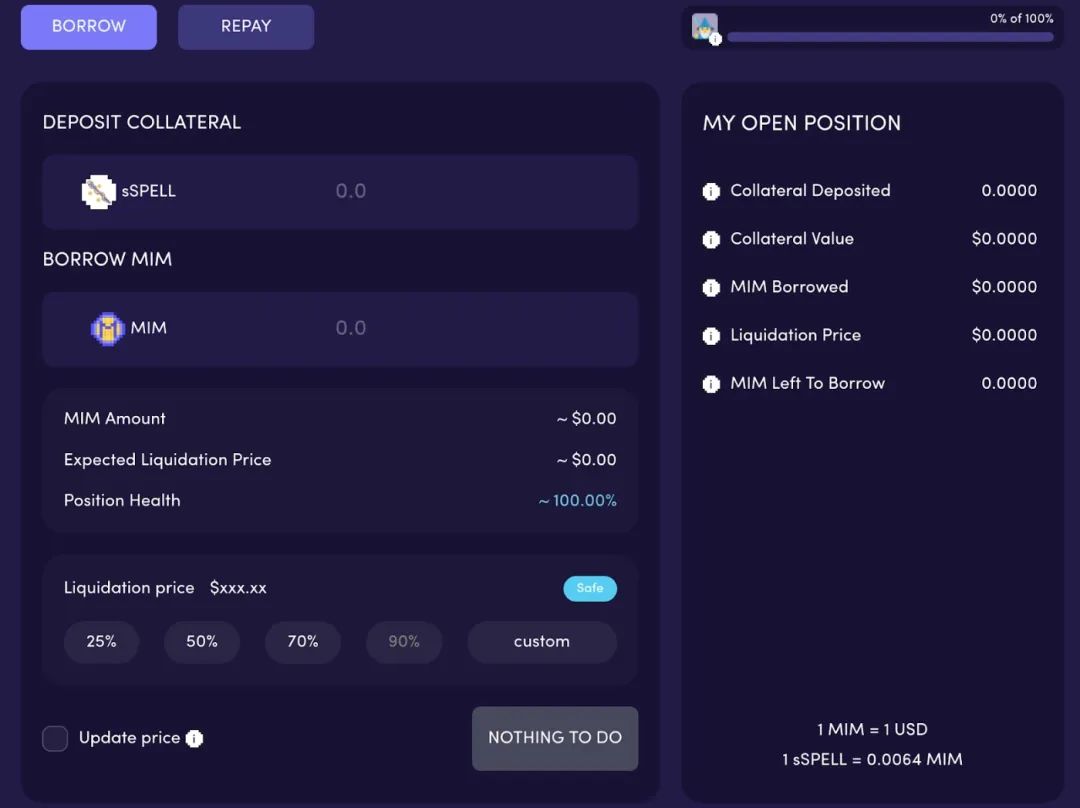

If you are buying a protocol's token and want to hold it long-term, the last thing you want to encounter is having to sell these tokens for short-term liquidity. Maybe your tax bill is much higher than you expected, or perhaps you want to pay a down payment on a car; whatever the case, being able to obtain some liquidity from your investment assets will greatly help long-term holding. Therefore, the last question you might ask is whether this token can serve as collateral for borrowing on mainstream lending platforms. xSUSHI is a great example because you can deposit xSUSHI in AAVE for borrowing. This does not require paying too much interest, and when you deposit it, you can still earn 10% returns. In AAVE, you can borrow other assets worth 50% of your collateralized asset, such as ETH and USDC. You can do the same when collateralizing SPELL tokens on Abracadabra.

This may be the least significant factor in the utility of a token, but it is still worth considering. Being able to use an investment target as collateral for loans makes holding assets much easier.

This may be the least significant factor in the utility of a token, but it is still worth considering. Being able to use an investment target as collateral for loans makes holding assets much easier.

06 Start Combining Supply and Demand

Now that we have discussed two deeper topics, token supply and token utility. I arranged it this way because I primarily observe the token supply; if it passes the testing questions listed in the article, I will then consider the token's utility. If it passes these considerations, I will increasingly feel that it is a good investment. However, there are more factors we have yet to discuss, such as game theory, growth, and adoption. In the subsequent articles of this series, we will continue to discuss.