In-depth exploration of the long-term viability of the AMM model and how Uniswap adapts to future financial developments

AMM is a foundational layer protocol that aggregators, brokers, gaming applications, and others will use to obtain liquidity.

AMM is a foundational layer protocol that aggregators, brokers, gaming applications, and others will use to obtain liquidity.Title: DeFi Thesis: Uniswap & AMMs

Author: Michael Nadeau

Compiled by: Dong Xun, The Way of DeFi

Uniswap has just completed a $165 million Series B funding round. In this week's report, we explore the long-term viability of the Automated Market Maker (AMM) model and how DeFi protocols like Uniswap are adapting to the future of finance.

Topics Covered:

- High-level overview of AMMs and Uniswap

- Should Uniswap create its own blockchain?

- MEV and order flow payments

- The future of centralized exchanges

- Regulation

We are still in the very early stages of fully adopting these new technologies. Predicting how things will evolve is quite challenging. But as we consider building, we think it might look like this:

- Hardware (ASIC miners, GPUs, computers/servers)

- Software: Layer 1 blockchains (Bitcoin, Ethereum, Solana, etc.)

- Layer 2 scaling solutions (Lightning, Arbitrum, Optimism, etc.)

- Bridges or connections between Layer 1/Layer 2 blockchains and TradFi systems

- Data/computation layers across the entire tech stack

- Consumer-facing applications

We are currently between steps 2-4. This report aims to give you a comprehensive understanding of the infrastructure being used today and our direction of development. As adoption rates increase, clarifying our current trajectory may prove very valuable in the coming years. We are now seeing many high-quality projects being built. It would not be surprising to see this space grow tenfold in the next cycle. This research helps us think about where value can be generated and how we should position ourselves.

High-Level Overview of Automated Market Makers (AMMs) and Uniswap

Automated Market Makers (also known as decentralized exchanges) function by organically forming bilateral markets using blockchain technology and smart contracts.

How it Works: Anyone with an internet connection can become a liquidity provider. Liquidity providers (LPs) deposit crypto assets into liquidity pools. In return, they receive a derivative token or "liquidity token"—used to provide liquidity to the protocol.

The "liquidity token" represents a specific liquidity provider's contribution to the pool, as a percentage of the total liquidity in the pool. Traders enter and trade within the liquidity pool. They pay fees directly to liquidity providers (most pools charge 30 basis points). This is all calculated using liquidity tokens (which are just data). Liquidity providers = supply, traders = demand. Traders pay liquidity providers directly. Smart contracts (if/then statements written in computer code) act as intermediaries.

Simple Example: You deposit 1 ETH (and USDC worth 1 ETH) into Uniswap's ETH/USDC trading pool. For simplicity, assume you own 10% of the pool. A trader comes in and swaps ETH for USDC, paying 30 basis points to the pool. Assume 30 basis points equals $1. By providing liquidity to the protocol, you would earn $0.10. You can continue to do this as long as you wish to earn passive income. When you want to remove liquidity, you can send the liquidity token back to the smart contract. The smart contract then returns your original ETH and USDC contribution + your % of fees directly to your wallet.

Compared to TradFi: In TradFi, traders do not need to pay fees. But that’s not entirely true. We do pay fees, but we don’t know how to quantify them. Suppose you submit a trade to Robinhood, TD Ameritrade, or your favorite brokerage account. Robinhood sends your order to market makers like Citadel. Citadel executes the trade for you (providing liquidity). They may also front-run your trade or use information to engage in rapid arbitrage.

Thus, when we compare Uniswap and the AMM model, you will find that people around the world are playing the role of Citadel, acting as market makers. Just in this case, the market makers are not front-running you (keep this thought in mind). Uniswap essentially breaks the monopoly of market makers by redistributing the business model to anyone who wants to participate. Currently, 100% of the fees generated by the protocol are directly allocated to liquidity providers or market makers.

AMMs are not order books. Users swap tokens on Uniswap and other AMMs. For example, UNI for ETH, or UNI for ETH. Uniswap's fees are lower than centralized order books like Coinbase (which charges 100 basis points or 1%). The additional demand for Uniswap comes from traders—who gauge their profitability based on the amount of ETH or UNI in each pool (and other pools) relative to the prices of these assets on other exchanges. When opportunities arise, arbitrageurs will swap various assets in the liquidity pool to align the prices between currency pairs and the listed prices on other centralized and decentralized exchanges.

Impermanent Loss. This refers to situations where liquidity providers would have been better off holding their assets rather than depositing/lending them into the liquidity pool to earn fees. Without delving too deeply, you can think of it as the opportunity cost incurred when the price of your deposited assets changes significantly. In other words, passively providing liquidity in an AMM is not entirely without risk.

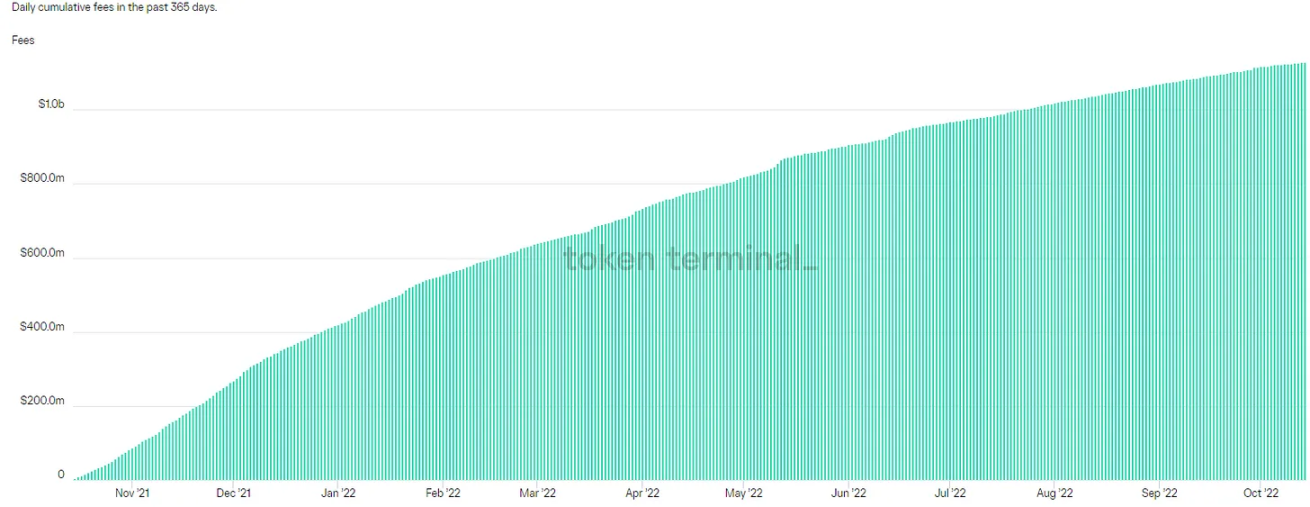

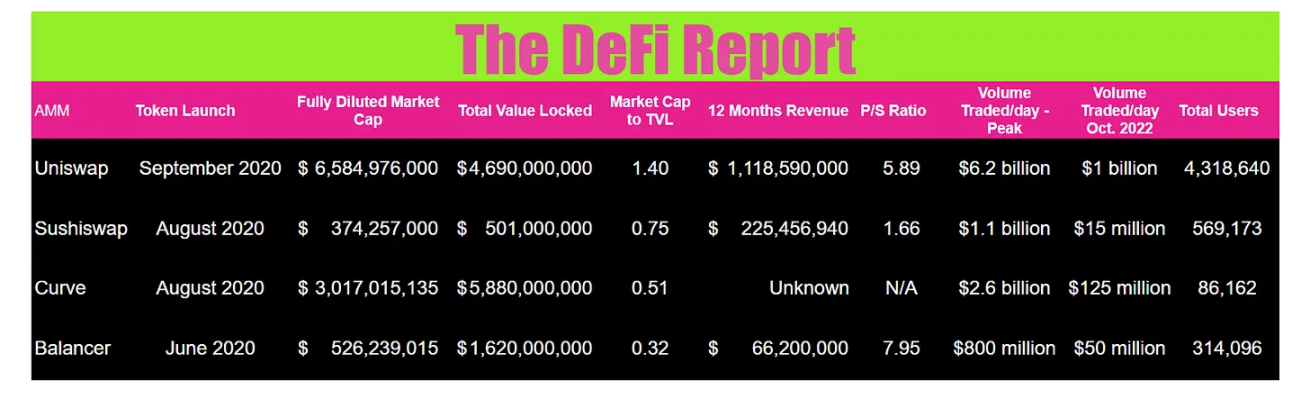

Uniswap's 365-day revenue = $1.1 billion.

Source: Token Terminal

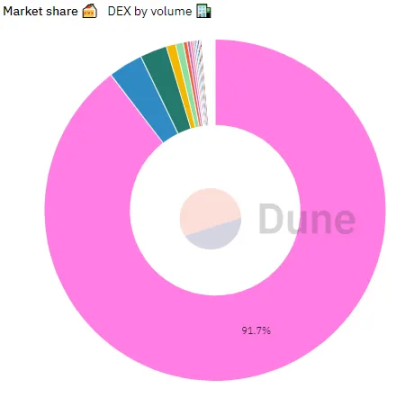

Uniswap's Market Share

Data Source: Dune Analytics

Although Uniswap's code is open-source and can be forked and replicated freely, it still dominates trading volume among automated market makers. Notably, their share has been increasing during the bear market.

Currently, Uniswap's average trading volume is about $1 billion per day. Its volume once soared to $6.5 billion in a single day and exceeded $1 trillion in total trading volume in May of this year. Below is a quick comparison with several other Ethereum AMMs. Note that alternative AMMs on L1 chains are also growing.

Data: Coinmarketcap, Dappradar, Token Terminal, Dune Analytics

* Users = total number over a period of time. Market Cap to TVL uses fully diluted market cap.

At this point, Uniswap seems poised to win the battle of automated market makers. We see signs of a power law emerging in DeFi. Projects that are genuinely being used are starting to stand out.

But what unforeseen challenges does Uniswap face?

MEV: Maximum Extractable Value

Some analysts suggest that Uniswap should launch its own blockchain or "application chain." This is feasible on Cosmos or Polkadot.

But why would Uniswap want to do this?

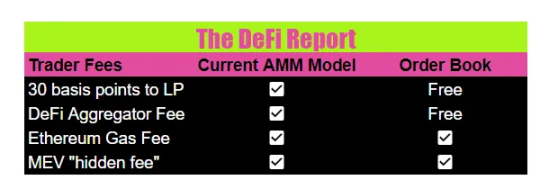

To understand this, we need to delve into how trading operates on Uniswap. Currently, when traders process a trade, they are effectively paying 3 or 4 fees:

- Note that DeFi aggregator fees only apply to trades made through MetaMask, Zapper, Matcha, etc. (which account for about 80% of all Uniswap trades)

- Ethereum gas fees paid to transaction validators

- MEV "hidden fees" paid to block builders and validators

MEV or Maximum Extractable Value = the value extracted by block builders and validators when they order transactions in their memory pool (where transactions are processed before being added to a block)—in a way that favors certain arbitrageurs. Notably, MEV is an emerging phenomenon in any market—massive trades across asset types and markets create significant value only for those who can understand the nature of the trades and profit from the information. This is not unique to Ethereum or cryptocurrency.

Here are a few examples of how MEV works:

Sandwich Attack: This is a form of pre-running where bots detect trades in the memory pool. They then front-run the trade, pushing up the price of the subsequent trade, and sell at the inflated price. This is essentially what Citadel does in traditional finance, and it is entirely legal.

Arbitrage Across Different AMMs: The price of tokens may vary slightly across different AMMs. When price discrepancies arise, MEV bots will buy assets on one AMM and sell them on another. Of course, being able to order transactions within a block to extract maximum value becomes very profitable. It should be noted that arbitrageurs do provide a service, as they help balance prices across exchanges when market price dislocations occur.

Impact on Uniswap

As we have seen, the Uniswap protocol creates significant value due to its deep liquidity. However, today Uniswap users (a distributed collection of liquidity providers) only charge 30 basis points in fees. The remaining value flows to the underlying layer's aggregators and Ethereum validators (including MEV or those bribing validators). For this reason, some believe Uniswap should launch its own blockchain. This would allow them to control the entire value chain.

But what is the cost of doing so?

DeFi protocols are life and death for liquidity. Uniswap has extensive liquidity because it is built on Ethereum. If Uniswap's liquidity decreases, the fees it generates will decrease, and the slippage in trades will increase. This would threaten their entire business model.

Uniswap must build the data and smart contract infrastructure they currently obtain from Ethereum. This means they need their own validators and must launch from scratch. This is not an easy task.

Security. Uniswap currently leverages Ethereum for base layer security. This cannot be underestimated. Transitioning to their own chain and starting security from zero is a daunting task.

For these reasons, we believe it makes little sense for Uniswap to launch its own blockchain. This brings us back to MEV and the emergence of order flow payments in DeFi…

Order Flow Payments (PFOF)

It is said that large traditional financial players are already building solutions to introduce PFOF into DeFi in the new trading model.

In this section, we will discuss what it might look like and its impact on AMMs like Uniswap. Specifically, does PFOF undermine the current model of distributed liquidity providers?

As we mentioned above, MEV is essentially a cost incurred by traders today due to hasty trade execution and bribery in the block-building layer of the tech stack. Traders are paying for this and paying fees to Uniswap's "LPs." If the order flow payment model enters the competition, what happens to MEV?

With order flow payments, you might bid in an auction to fill trades before receiving the transaction (order block). The exchange would sell the order flow—similar to how Robinhood and other brokers currently sell their order flow to large market makers. This means traders would sell order flow through DeFi protocols without paying any fees. This model would revert to what we see in traditional finance. Companies paying for order flow would order trades favorable to them (they become MEV) and pay small fees directly to aggregators or order book protocols (or wallets like MetaMask) to provide traffic. Here’s how the fee structure changes:

The difference here is that PFOF companies charge fees and separate them from the aggregators/wallets providing them traffic. They cut out the distributed liquidity providers. If the market seeks the most efficient and cost-effective route, it may trend in this direction. This assumes that Uniswap's model does not undergo other types of restructuring. As adoption rates and trading volumes increase, LP fees may also decrease.

We believe the PFOF model makes sense in a multi-chain future. For example, games could build their own application chains, while PFOF companies could direct liquidity to various unrelated applications/ecosystems as liquidity demand arises.

Ultimately, we believe the market will choose to create services with the best cost and most user-friendly execution. Fees, slippage, front-running, etc., will all impact this.

Note that blockchains like Bitcoin do not have MEV. Bitcoin is merely a payment network and value storage. Therefore, there are no arbitrage opportunities for traders to exploit across different markets.

Uniswap + Genie

Uniswap recently acquired the NFT aggregator Genie. This implies a few things:

They want to expand into the NFT exchange space.

They are considering new revenue models. Owning an aggregator allows Uniswap to control traffic.

This leads us to believe that Uniswap may seek to acquire large aggregator companies like Zapper. This would enable them to control the market to some extent, protect their liquidity providers, and maintain the ability to drive value back to their native token, UNI. For example, Uniswap could maintain its LP fee model and return any additional fees earned through the aggregator to the treasury or distribute them to token holders.

If Uniswap cannot maintain its decentralized liquidity provider model, its token could become worthless. Why? The ability to extract a portion of the fees paid to LPs (or aggregators) is what gives the token value today. Token holders can vote on future fee structures. In fact, the Uniswap DAO recently voted to experiment with protocol fees, returning 10% of LPs to the treasury of several selected pools. If we imagine Uniswap returning 10% of its LP fees to the protocol or token holders, this would equate to over $100 million or $0.13 per token annually—based on current revenue in the bear market. At the time of writing, Uniswap tokens are trading at $6.30, which corresponds to about a 2.1% yield.

If you believe Uniswap will increase its liquidity, volume, and revenue tenfold in the next cycle, then we would get about $1.3 per token, or a 21% yield based on the current token price. Note that this is purely speculative. We provide this data merely to offer a perspective on how investors might assess potential risks/rewards when analyzing Uniswap.

We believe acquiring an aggregator like Zapper would also allow Uniswap to make breakthroughs in the emerging PFOF model, protecting its LPs and controlling another layer of the value stack. The recent acquisition of Genie suggests this may already be a strategy the team is considering.

Centralized Exchanges

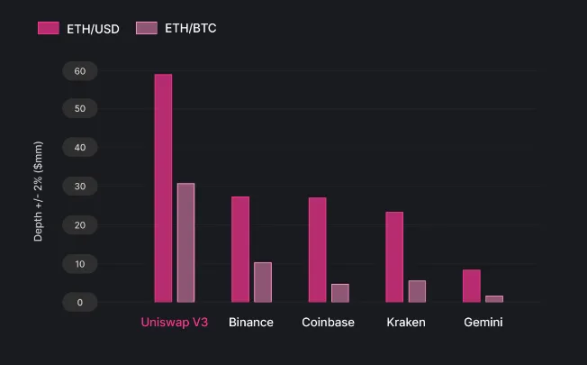

Large centralized exchanges like Coinbase, Binance, Kraken, and Gemini may face challenges. Because Uniswap has lower fees than they do. Below we can see a comparison of trading volumes for ETH/USD pairs and ETH/BTC pairs during the data sampling period from June 2021 to March 2022.

Data Source: Paradigm Capital

Keep in mind that centralized exchanges are building multiple lines of business. Coinbase is aggressively entering the staking business and has a strong institutional custody line. They have also been pushing their wallet and building an NFT marketplace. As a publicly traded company, Coinbase has become a trusted source for institutions in custody and trading. Deals with Blackrock and Google are representative of this. We expect Coinbase's share of trading revenue to decline in the coming years, while its ancillary business lines may grow significantly.

Today, companies like Coinbase control the on/off ramps. But this may not be guaranteed in the future. MetaMask recently partnered with fintech company Sardine to allow banks to transfer directly to MetaMask users' wallets/DeFi brokers. This cuts out Coinbase and creates a direct bridge from banks to DeFi without first going through a centralized exchange. It also allows MetaMask to capture more direct traffic.

Remember, this space is very early. Coinbase and other centralized companies may lose a percentage of trading fees due to AMMs like Uniswap, but in the foreseeable future, the rising tide may benefit all companies.

Regulation

A quick note on regulation. Uniswap and other AMMs are currently unregulated. The same goes for Coinbase. It is important to note that Coinbase is on the on/off ramp to traditional banking. To create a Coinbase account, you must go through KYC (Know Your Customer). This means law enforcement can track anyone entering or leaving cryptocurrency through their exchange. Uniswap does not have this. This means two things: 1) Tracking illegal activity on Uniswap is more difficult, and 2) Tracking tax activity is more difficult.

Keep in mind that today, the vast majority of users entering Uniswap must start from Coinbase or another centralized exchange—buying cryptocurrencies that can be used in DeFi. Uniswap does not have a direct on/off ramp with KYC providers.

According to legislation proposed in Congress, the CFTC seems poised to regulate most cryptocurrencies. Centralized exchanges will fall under their oversight. Predicting what might happen with DeFi protocols becomes trickier. Uniswap could certainly be forced to implement KYC through its website interface for direct access to the protocol. The same goes for any aggregator built on top of Uniswap. Law enforcement may also devise new methods to track illegal activities and tax evasion. We could also see some pools on Uniswap being "permissioned," while others remain permissionless.

Of course, we cannot rule out Uniswap obtaining broker/dealer licenses, registering with the SEC, and becoming the trading infrastructure for a new financial system where all assets are tokenized.

This is all speculation. But do not forget that Uniswap just raised $165 million from some very powerful venture capital firms (VCs). For more on this topic, the insights of Jake Chervinsky, policy director at the Blockchain Association, are quite helpful.

Conclusion

We believe DeFi protocols are infrastructure, and Uniswap is infrastructure. Similar to our paper on lending protocols, we view AMMs as layer 1 protocols. We believe aggregators, brokers, gaming applications, etc., will leverage AMMs to obtain liquidity. Even traditional order books like Robinhood may one day leverage Uniswap for liquidity.

Based on what we have outlined in this report, acquiring a middleware aggregator may be in Uniswap's best interest. This would allow them to control a key layer of the trading stack. Most importantly, it would enable them to maintain a fully decentralized liquidity provider/market maker structure. In this scenario, aggregators would charge a small fee (which could be paid to the treasury or token holders), providing a smooth interface for Uniswap (and other AMMs), while LPs would still collect their fees for providing services at the base layer.

Meanwhile, Flashbots is seeking to address the issue of hasty execution in the block-building layer of the trading tech stack while keeping the network as decentralized as possible.

Due to impermanent loss, earning profits as a simple, passive liquidity provider on Uniswap is becoming increasingly difficult. Over time, we expect to see larger participants enter and capture larger shares. Liquidity provision may become institutionalized.

We may also see an order book model built on top of Uniswap. Over time, the path will become clearer for the Uniswap team.

But one thing is certain: the most important metric for any DeFi protocol is liquidity. And Uniswap is the king today.