Arthur Hayes: My Expectations for U.S. Monetary Policy

Even if the Federal Reserve does not issue a formal signal of a shift, the New York Fed and the Treasury are likely to release dollar liquidity before the election.

Even if the Federal Reserve does not issue a formal signal of a shift, the New York Fed and the Treasury are likely to release dollar liquidity before the election.Original Author: Arthur Hayes, Co-founder of 100x

Original Compilation: Wu Zhuocheng, Wu Says

Recently, the Federal Reserve has slowed its tightening policy over the past few weeks, coupled with the Treasury injecting a large amount of liquidity into the credit system, which has driven a rebound in risk assets. We do not know what factors have driven the Federal Reserve's recent actions, but if this continues, it will somewhat weaken our expectations for U.S. monetary tightening. Currently, we have not changed our view, but we will continue to closely monitor the situation.

Dollar liquidity consists of three parts:

The size of the Federal Reserve's balance sheet. The Federal Reserve deposits funds into banks, and in return, banks sell U.S. Treasury bonds and/or U.S. mortgage-backed securities. This is how the Federal Reserve "prints" money to inject vitality into the financial system.

The size of the reverse repurchase (RRP) balance held by the New York Fed. The Federal Reserve allows eligible counterparties to deposit dollars and earn a certain return. Once the deposited funds enter the Federal Reserve's account, they become "dead money" because the Federal Reserve does not use the deposited funds for commercial loans. In fact, the monetary multiplier for the New York Fed's RRP balance is 0, while the multiplier for deposits in any other financial intermediary is non-zero. (Before the pandemic, reserve requirement ratios hovered between 3% and 10%—leading to a monetary multiplier for U.S. commercial banks of 33 to 10 times—but the Federal Reserve has since lowered it to 0%, meaning commercial banks can lend out 100% of the deposits they receive). Money market funds (MMFs) are funds where retail and institutional investors place cash to earn short-term returns; all my idle cash is deposited in MMFs, and I can withdraw my cash within one business day. MMFs can deposit funds into RRP, as well as various other low-risk short-term credit instruments (such as U.S. Treasury bonds, AAA-rated U.S. corporate commercial paper). Keeping money at the Federal Reserve is the least risky option, with fees paid being roughly the same as the other two options, but there is indeed some risk. Therefore, if possible, money market funds prefer to keep funds at the Federal Reserve rather than in leveraged financial economies and various other low-risk short-term credit instruments (such as U.S. Treasury bonds, AAA-rated U.S. corporate commercial paper).

The balance of the U.S. Treasury General Account (TGA) with the Federal Reserve, which is the Treasury's checking account. When it decreases, it means the Treasury is injecting funds directly into the economy and creating liquidity. When it increases, it means the Treasury is saving funds rather than stimulating economic activity. The TGA also increases when the Treasury sells bonds. This action eliminates liquidity from the market because buyers must pay for their bonds in dollars.

In summary, dollar liquidity increases/decreases under the following circumstances:

Dollar liquidity rises:

Federal Reserve balance sheet ------ increases

RRP balance ------ decreases

TGA ------ decreases

Dollar liquidity falls:

Federal Reserve balance sheet ------ decreases

RRP balance ------ increases

TGA ------ increases

However, all three potential factors do not always point in the same direction. For example, sometimes the Federal Reserve's balance sheet is growing while the TGA is also increasing. Therefore, whether dollar liquidity is increasing or decreasing depends on the interaction of these three factors, their directions, and the extent or speed at which they occur.

Although the Federal Reserve began implementing quantitative tightening (QT) in June of this year, meaning they decided to shrink the balance sheet to combat inflation, the recent decrease in the size of its balance sheet has been offset by decreases in RRP and TGA. This typically leads to an increase in dollar liquidity rather than a decrease.

The maximum size of the RRP tool, the return rates offered, and the companies allowed to use it are entirely at the discretion of the Federal Reserve. Therefore, the Federal Reserve can influence how this liquidity faucet affects the entire market. For example, the Federal Reserve can completely shut down this tool, forcing money market funds and other institutions to move cash elsewhere, thereby releasing $2 trillion of base money into the system in the process. This base money, depending on who it is provided to, can be further leveraged to actively drive financial economic activity. Recently, RRP has declined, and I do not have (nor have I read) a compelling theory about the reasons for the balance decline—but what we need to understand for this article is that it has been declining.

With only a few months until the election, it is widely believed that many people vote with their wallets. From now until November, to help improve wallet voters' perceptions of the U.S. economy, Yellen and the Treasury could choose to directly create looser monetary conditions—injecting a large portion of the remaining $500 billion in TGA into the economy, thereby stimulating it. Throughout the summer, the TGA balance has shrunk. Similar to the recent decline in RRP, I do not have a reliable theory to explain why—but again, what we need to know is that it has gotten smaller.

Therefore, both the RRP balance and the TGA have recently declined. This raises the question: Is the Treasury actively using RRP and TGA leverage to counter the Federal Reserve's current established policy of combating inflation by reducing the money supply? If so, do they intend to continue doing so? I do not have answers to these questions, but the ruling party always has a strong political will to create favorable short-term economic conditions before elections so that party members can keep their jobs.

When all of this finally crystallized in my mind, I created a custom chart depicting what I call the Dollar Liquidity Condition Index.

Dollar Liquidity Condition Index = [Federal Reserve's Balance Sheet] - [Total Amount of Reverse Repo Bids Accepted by the New York Fed] - [Balance of the U.S. Treasury General Account Held by the New York Fed]

Bitcoin and the Dollar Liquidity Condition Index

At the current stage of the cryptocurrency capital market, Bitcoin represents a strong synchronization (sometimes a leading indicator) of global dollar liquidity conditions.

Bitcoin (yellow) vs. Dollar Liquidity Conditions (white)

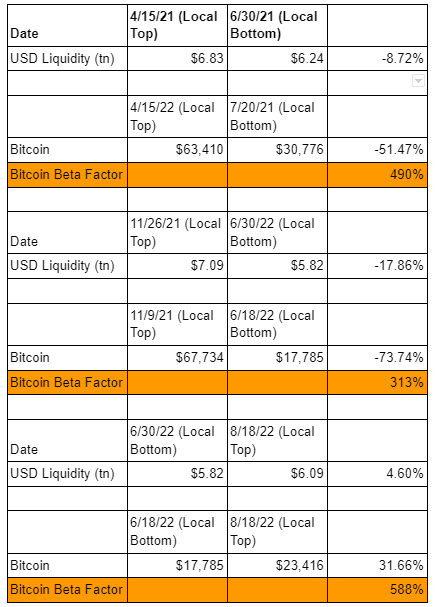

To determine the validity of this relationship, let’s look at the local liquidity tops and bottoms from 2021 to the present.

Each date corresponds to a local top or bottom—and the timing is incredible. Bitcoin has risen when liquidity is rising and fallen when liquidity is declining. It is somewhat unfortunate that currently, Bitcoin is merely a high-energy indicator of dollar liquidity, but fundamentally, this is not surprising.

Bitcoin is a digital currency that represents different systems and ideologies about how society should best organize its monetary affairs. The dollar is the global reserve currency, installed alongside the Western financial system led by the U.S. If the dollar system generates excess, Bitcoin absorbs it. Bitcoin acts as a real-time smoke detector related to the profligacy of the dollar-based financial system.

Price vs. Quantity

Which is more important for risk assets—the price of the dollar (federal funds rate) or the quantity of dollars (dollar liquidity conditions)?

Federal Funds Upper Limit (yellow) vs. Dollar Liquidity Conditions (white)

The Federal Reserve began "actively" raising policy rates in March of this year. However, following the recent local bottom rebound, dollar liquidity conditions have begun to improve. Despite rising monetary prices, risk assets like Bitcoin and U.S. stocks have responded positively to the increase in dollar liquidity.

Thus, it currently appears that the performance of financial assets is more dependent on the quantity of money rather than its price.

Bitcoin Control Factors

In the case of Bitcoin being institutionalized, most cryptocurrencies cannot outperform the market's dollar performance on an absolute basis. However, I am confident about Ethereum's recent positive price performance, entirely due to the anticipated impact of the upcoming merge. I elaborated on this in my previous articles "ETH -flexive" and "Max Bidding."

In the latter article, I argued why we might see the Federal Reserve shift from combating inflation to loosening financial conditions in the short term. However, if we look back at the dollar liquidity condition index chart, the liquidity condition index has recently declined from a local high (indicating tightening liquidity conditions), and cryptocurrencies have thus been halved. I can form all the theories I want about the Federal Reserve's pivot, but if the dollar liquidity condition index continues to decline, I am fundamentally wrong. However, now that I have a more comprehensive fundamental understanding of how the different aspects of this index promote increases or decreases in dollar liquidity, I can form a more nuanced view of how the Federal Reserve sways.

Let’s treat this situation as if we are politicians more concerned with accounting and public perception than economic reality. I need the Federal Reserve to appear to be fighting inflation, but I also need the stock market to rise so that my wealthy donors will be happy. What to do?

If the quantity of money has a greater impact on financial markets than its price, then the Federal Reserve can raise rates at will without harming the market—as long as the dollar liquidity condition index also rises. The act of raising policy rates will make the Federal Reserve appear to be fighting inflation, and the Federal Reserve can even allow its balance sheet to decline to help maintain this image. But behind the scenes, it still has the ability to influence RRP balances, and it can also call on the Treasury to spend more money to generate economic activity—resulting in a net increase in funds and boosting stock performance. Clearly, the capabilities of these two potential levers are limited—RRP balances and TGA cannot go below zero—but they can still be used to effectively offset QT in the short term.

In summary, I remain concerned about the macro-financial conditions before and after the merge, which is scheduled to take place two months before the U.S. midterm elections in November. I still believe that even if the Federal Reserve does not send a formal pivot signal, the New York Fed and the Treasury are likely to release dollar liquidity (through RRP balances and TGA) before the elections, which will act as a booster for risk assets in the market.

Unless the Federal Reserve or the Treasury explicitly tells us that the pace of RRP tool or TGA depletion will change, we can only monitor the weekly changes in these three liquidity index variables and make imperfect assumptions about their recent trajectories.

Some may argue that I am moving the goalposts to justify my market positioning, which is entirely fair. However, as I mentioned earlier, regardless of the dollar liquidity condition, I believe the merge will drive up the price of ETH. I still believe that the significant reduction in ETH output will have a positive impact on price, and the positive reflexivity between price/network activity/network usage will overcome any tightening of dollar liquidity conditions—only the price trend may be weaker than I predict or hope.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles