The thunder of regulation descends, is it the "spring" for decentralized stablecoins?

Decentralized stablecoins, as the "disaster recovery value" of the Web3 settlement layer, have become more evident after the Tornado Cash incident.

Decentralized stablecoins, as the "disaster recovery value" of the Web3 settlement layer, have become more evident after the Tornado Cash incident.Original Title: "MintClips|The Regulatory Thunder Strikes, Is the Spring of Decentralized Stablecoins Here?"

Author: Mint Ventures

The Regulatory Thunder Strikes Tornado Cash

Aside from the upcoming Ethereum merge, the U.S. Treasury Department's Office of Foreign Assets Control (OFAC) sanctioning the privacy mixer Tornado Cash built on Ethereum has become the biggest industry hotspot recently.

As more and more web3 institutions or protocols actively or passively follow OFAC's regulatory policies, they have begun to block addresses that have interacted with Tornado Cash. Additionally, the community has responded to the harsh regulatory demands with "poisoning" protests (referring to certain users withdrawing small amounts of funds from Tornado Cash to well-known institutions or celebrity Ethereum addresses, causing these accounts to also be affected by regulatory policies). This regulatory incident surrounding Tornado Cash has intensified, sparking widespread discussion.

At the center of this storm of public opinion, besides Tornado Cash, is the U.S. institution Circle, which issues and operates the USD stablecoin. Following OFAC's announcement of sanctions, Circle quickly implemented its blacklist function, freezing USDC in the Tornado Cash protocol. In contrast, the ETH in Tornado Cash, due to its permissionless nature, could not be frozen and was used by the community as a medium for "poisoning" to express dissatisfaction with regulatory policies.

Although both are crypto assets operating on permissionless public chain networks, the contrast in decentralization between USDC and ETH in the face of regulation is stark.

Decentralized Stablecoins vs. Centralized Stablecoins

The Importance of Stablecoins

The core cooperative role played by USDC in this regulatory event has led to a renewed awareness of the importance of concepts that fundamentalists have always insisted on but have gradually been overlooked in recent years—censorship resistance, permissionlessness, and decentralization.

As the settlement layer of the Web3 economy, the importance of stablecoins almost surpasses that of all other DeFi foundational applications, reflected in their:

- Widest user base: Including users of centralized exchanges, the number of stablecoin holders is absolutely the largest.

- Largest trading volume: Stablecoins serve as intermediaries in transactions with extremely high turnover rates, and most of the trading volume in the crypto world is related to stablecoins.

- Huge asset scale: The total market capitalization of stablecoins is currently over $150 billion, second only to BTC and ETH.

Thus, it is not an exaggeration to say that stablecoins are the most important foundational setup above the public chain layer in the Web3 economy.

However, since the birth of stablecoins, the landscape dominated by centralized institutions such as Tether (USDT), Circle (USDC), and Binance&Paxo (BUSD) has remained solid. The market share of centralized stablecoins, whether in terms of market capitalization, trading volume, or user numbers, has been continuously expanding.

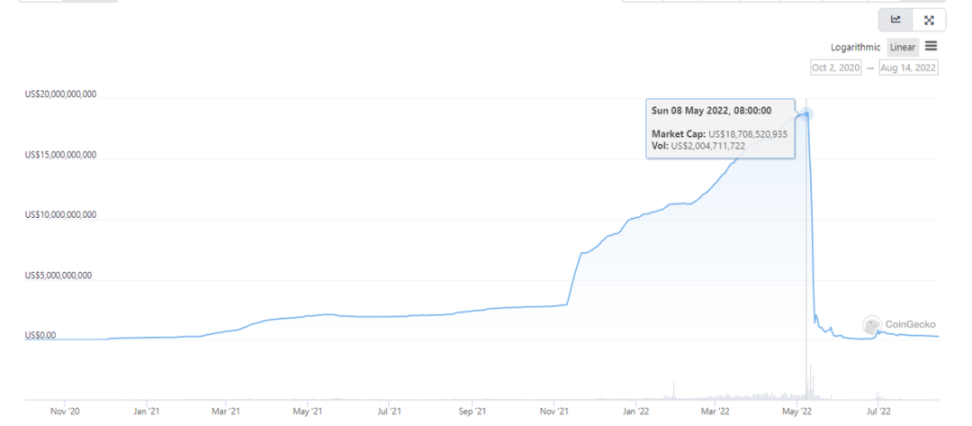

Although in 2021-22, the decentralized stablecoin UST, issued on the Terra network and based on Luna as its underlying asset, once grew against the trend, surpassing the third-largest stablecoin BUSD with a market cap of over $18 billion, it collapsed rapidly in May of this year, becoming a bright but short-lived meteor in the history of stablecoin development.

The reasons hindering the expansion of decentralized stablecoins are varied, but the most important and straightforward reason is: compared to centralized stablecoins, decentralized stablecoins do not have a clear product experience advantage.

The concept of "decentralization," which has allowed BTC, blockchain, and Web3 to rise from the ground up, seems less important in the field of stablecoins.

What matters more is price stability, ease of use, and accessibility.

Until people witnessed the first regulatory thunder strike on the DeFi protocol Tornado Cash in August 2022.

Decentralized asset ETH was able to escape unscathed from Tornado Cash, while centralized USDC may forever be left behind.

Growth Bottlenecks of Decentralized Stablecoins

The Tornado Cash regulatory incident serves as a giant advertisement for the importance of "decentralization" in stablecoins.

This advertisement targets not only ordinary users but also decentralized stablecoin projects that use centralized stablecoins as collateral, with MakerDAO and its issued DAI being the representative of the current largest decentralized stablecoin protocol, which has a current issuance scale of $6.8 billion.

So, will the centralization concerns triggered by regulation pave the way for the "decentralization" of the stablecoin market, becoming a direct driving factor for the increase in the share of decentralized stablecoins?

Before pondering this question, it is necessary to reassess the bottlenecks that have prevented decentralized stablecoin projects from breaking through their market share.

The market value and popularity of decentralized stablecoin projects are always influenced by two core factors: the actual demand for business or scenario construction and the narrative of the exciting track.

The former is an intrinsic factor for their long-term development, while the latter can drive short-term user and capital influx, attracting significant attention and discussion, raising public expectations and prices for the projects.

1. Business and Scenario Bottlenecks

In terms of business and scenarios, the growth path of UST's market value scale is a typical case of "demand-driven growth":

Data Source: Coingecko

Previously, the lending protocol Anchor in Terra provided a stablecoin interest rate of 19-20% for a long time, significantly higher than the risk-free rates in both the web3 and traditional worlds at that time. Since the Anchor protocol only accepted UST as a stablecoin deposit, this directly boosted the demand for UST, allowing it to grow into the third-largest stablecoin, peaking at a market cap of $18.7 billion within just a year.

Of course, the 20% interest rate also led to a series of adverse consequences:

- UST's scale expanded too quickly, leading to excessive debt in the Terra ecosystem.

- High debt costs.

- Extremely high yields squeezed the space for other DeFi projects in the Terra ecosystem.

Apart from Terra, other protocols issuing decentralized stablecoins have also attempted to create initial demand for their stablecoins.

For example, the leveraged mining protocol Alpaca on BNBchain has its stablecoin AUSD. Alpaca also launched an automated yield product called "Automated Vault" in the first half of this year. This product can be simply understood as a financial product based on leveraged mining strategies. Due to high predicted yields at the launch, the high-multiplication product quotas were extremely popular and often sold out instantly.

Thus, Alpaca later set multiple conditions for purchasing such products, such as providing liquidity for AUSD on Ellipsis.finance (a Curve-like trading platform on BNBchain focused on stablecoin trading) to obtain purchase quotas, attempting to create demand for AUSD through its popular business. However, as of now, AUSD's market cap is still only over $3 million.

Alpaca's automated yield product, Data Source: Alpaca

The above attempts to drive stablecoin business growth through self-created demand have ultimately not been very successful.

UST's failure primarily stemmed from a loss of control over monetary policy, while AUSD's business segment aimed at driving demand was simply too small and lacked sufficient demand, leading to an inability to provide adequate demand for the stablecoin.

The reason Terra and Alpaca had to create demand for their stablecoins themselves is that it is very difficult for new stablecoins to gain external adoption and achieve good liquidity. In the competitive open market, players are already very abundant, and both users and protocols tend to choose mature stablecoins; the cost of liquidity for stablecoins has already been fully priced through protocols like Curve. New stablecoins need to provide subsidies, purchase governance votes, or engage in mutual benefit exchanges with other DeFi protocols to gain liquidity, which is not cheap.

2. Narrative Bottlenecks

In recent years, there have been two significant narrative trends in the decentralized stablecoin space.

The first was the algorithmic stablecoin wave driven by Empty Set Dollar and Basis Cash from late 2020 to early 2021, and the second was the public chain + stablecoin dual-drive model brought about by the success of Terra.

Regarding the former, Empty Set Dollar and Basis Cash attempted to achieve rapid market value and network expansion through completely uncollateralized methods, using a Ponzi-like inflation design to balance stablecoin prices purely based on inflation/deflation demand. At the time, this was quite an imaginative monetary experiment, and representative decentralized stablecoin projects were referred to by many investors as the "underground Federal Reserve." "Believe it or not, I can outperform your BTC with a stablecoin" became a famous saying during the wealth creation wave of algorithmic stablecoins. However, ultimately, such explorations were proven to be failures; in the early stages of stablecoin projects, relying solely on expectations to achieve currency stability is difficult to establish.

The success of Terra directly led to numerous public chains issuing their own stablecoins in imitation. Before the collapse of UST, projects announcing the launch of their own public chain stablecoins included Near, Secret, Tron, etc., which referenced Terra's minting model to varying degrees and had good short-term performance in market capitalization after announcing their plans.

However, Terra's failure shifted the market's perception of the public chain self-operated stablecoin model from astonishment to skepticism, and on the narrative level, the second wave of stablecoin trends has temporarily quieted.

Like other Web3 commercial projects, the development and expansion of decentralized stablecoins rely on long-term business and short-term narratives. The previous bottleneck for decentralized stablecoins lay in insufficient internal and external demand for business on one hand, and on the other hand, the market had not found new narrative highlights in the short term.

However, the current market situation, with the variables brought by regulation, may provide a new wave of development opportunities for decentralized stablecoins.

A New Spring for Decentralized Stablecoins?

The Sower of Spring: Regulation

From a narrative perspective, the public's concerns about regulation have become a reality, and centralized stablecoins are the direct targets of regulation.

A significant part of the charm of the Web3 commercial world comes from the efficient innovation and combinations created in a permissionless environment, as well as the convenient cross-border capital flow. If the settlement layer is entirely dominated by centralized stablecoins in a world that advocates decentralization and permissionlessness, it is unacceptable to most people. The asset freezing incident involving USDC due to the regulation of Tornado Cash has made it clear to the public: decentralized stablecoins are no longer merely a "regulatory disaster backup" for centralized stablecoins, but may become a necessity for assets.

The push for decentralized stablecoins by regulation is not only at the narrative level; it may also directly lead to an increase in business demand in the future.

If similar events occur again in the future, or if stablecoins like USDT and BUSD are also forced to join the sanctions, user dissatisfaction with harsh regulation and the demand for permissionless currency will be further activated.

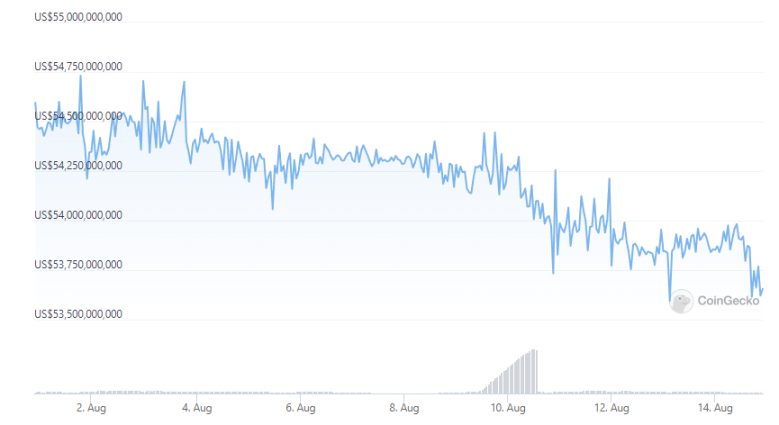

From a data perspective, the direct freezing of DeFi protocols and users' assets by USDC has undoubtedly reduced its credibility in Web3 business, with its market cap dropping by about $700 million in the past week.

USDC Market Cap, Data Source: Coingecko

However, the market share lost by USDC has not yet been captured by decentralized stablecoins. On one hand, as a whole, decentralized stablecoins have historically demonstrated far less stability and security than centralized stablecoins; on the other hand, the scenarios for decentralized stablecoins are sparse, with a narrow acceptance range, and actual use often requires multiple exchanges. Furthermore, the largest decentralized stablecoin DAI has USDC as its largest collateral asset, which may also be affected by USDC in the future. These shortcomings have prevented decentralized stablecoins from directly seizing the territory lost by USDC.

The Sower of Spring: Leading DeFi Protocols Join the Battle

Of course, in addition to the external force of regulation, decentralized stablecoins have many noteworthy internal development drivers.

After the wave of self-created stablecoins in public chains from March to May this year, leading DeFi projects developing stablecoins are becoming a new trend worth paying attention to.

The most representative projects are the lending protocol Aave's planned issuance of GHO and Curve's stablecoin (tentatively referred to as crvUSD).

Self-operated stablecoins by DeFi protocols are not new; lending protocols like Abracadabra, Venus, and Dforce have issued stablecoins MIM, VAI, and USX.

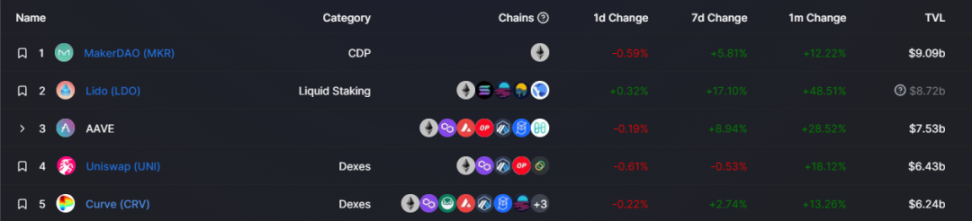

The reason why Aave and Curve's announcements to create decentralized stablecoins are noteworthy is that these two DeFi protocols are absolute leaders in DeFi, ranking third and fifth in terms of Total Value Locked (TVL).

DeFi TVL Rankings, Data Source: DeFillama

In addition to TVL, Aave and Curve also have advantages including:

- Strong dominance in their respective tracks.

- Good multi-chain and L2 product deployment.

- Integration by numerous external protocols.

- A long development history without serious security losses, resulting in excellent brand credibility and ecological appeal.

These are lacking in other DeFi projects.

More importantly, the self-operated stablecoins of the two projects also have clear business motivations, rather than being mere narrative hype.

For instance, the stablecoin issued by Curve is likely to be minted by users using LP from Curve's core pools as collateral, which creates higher capital efficiency for Curve's liquidity providers, enhances the attractiveness of market-making for Curve, and provides Curve with an opportunity to leverage and increase its TVL.

In fact, a significant portion of MakerDAO and Uniswap's high TVL comes from the following leveraged cycle:

- Users mint DAI at MakerDAO.

- They exchange DAI for some USDC and use the liquidity management platform Arrakis for DAI-USDC stablecoin market-making, obtaining G-UNI LP.

- They use G-UNI LP as collateral to borrow DAI again at MakerDAO.

- Repeat the above cycle.

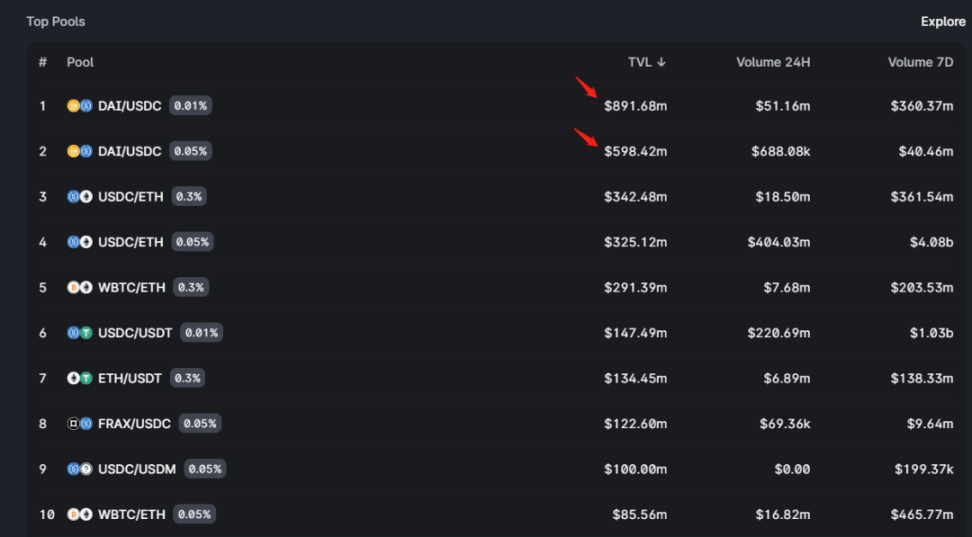

This cycle is one of the secrets behind Uniswap and MakerDAO's consistent top-five TVL rankings. By examining Uni V3 data, we can see that the TVL of just the DAI-USDC trading pair accounts for 32.6% of Uni V3's TVL.

Uni V3 Pool TVL Rankings, Data Source: Uniswap V3

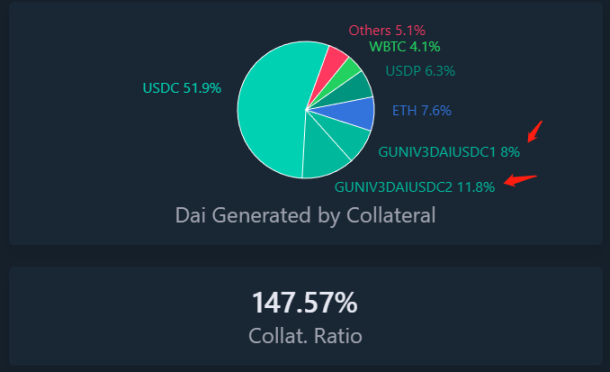

In MakerDAO's DAI minting, 19.8% of DAI comes from G-UNI's collateral.

Proportion of Collateral Sources for Minted DAI, Data Source: https://daistats.com/

If Curve launches its own decentralized stablecoin, it is expected to replicate the above cycle, achieving capital efficiency and increasing TVL.

The Sower of Spring: DeFi Ecosystem

In addition to the narrative and business driving forces of regulation and the self-operation of leading DeFi projects, another opportunity for the development of decentralized stablecoins may come from the overall push of projects capable of building DeFi ecosystems.

If the interaction of leveraged cycles in MakerDAO and Uniswap is merely a form of business cooperation based on composability, then the design and construction of DeFi ecosystems will place synergy among various businesses within the ecosystem at the core from the outset.

The construction of a DeFi ecosystem is essentially a vertical integration of the ecological chain, integrating segments with business synergy effects in the ecosystem.

Currently, there are two exploratory directions for this vertical integration.

The first method is through mergers and acquisitions or deeply controlling the governance rights of collaborative projects to integrate multiple projects into a DeFi ecosystem or matrix. A well-known DeFi developer, AC (Andre Cronje), the founder of the Yearn protocol, is an active practitioner of this approach. Since the onset of the DeFi summer in 2020, AC has either created, supported, sponsored, or deeply participated in governance, almost integrating a DeFi ecosystem that includes multiple tracks such as public chains (Fantom), DEX (Solidly, Sushiswap), lending (Abracadabra, Cream), aggregators (Yearn), and cross-chain bridges (Multichain).

However, coordinating multiple projects with inconsistent interests, users, and core teams is not easy, and this attempt has not yet succeeded; AC has expressed disillusionment and announced his withdrawal from the space.

Similarly, the acquisition of the lending project Rari Capital by the stablecoin protocol Fei Protocol has not been considered successful so far.

The second method is to build an ecosystem from scratch. Binance is the best practitioner of building an ecosystem in the CeFi field. In the DeFi space, the representative project for self-built ecosystems is Frax. Frax has already launched or is about to launch business segments including: decentralized stablecoin (FRAX), Swap (Fraxswap), lending (Fraxlend), and staking business (fraxETH).

Based on these business segments, combined with Frax's governance influence on Convex (Frax has become the largest single holder of CVX) and Curve, as well as its flexible monetary tool module AMO, whether Frax can turn its various business segments into mutually accelerating flywheels to promote the long-term development of its decentralized stablecoin is one of the experiments we are currently paying close attention to.

Concerns for Decentralized Stablecoins

Of course, despite the various development incentives for decentralized stablecoins that we have identified in the current market, there are still some issues that deserve our attention, such as:

- Many decentralized stablecoin projects have underlying assets that are centralized assets like USDC. For example, among the issued DAI, 51.9% of DAI comes from USDC (not including USDC in G-UNI LP). The initial collateral for Frax is also USDC, but the actual collateral for the FRAX stablecoin is not solely USDC; most of it is LP from Curve stablecoin pools. This means that unless Circle blacklists the Curve protocol, it cannot freeze Frax's collateral assets. However, will DeFi protocols like Curve become the next targets of sanctions?

- Expansion of balance sheets. If decentralized stablecoin protocols continue to adopt over-collateralization mechanisms, the scale of collateral such as ETH will become the ceiling for the expansion of the protocol's balance sheet. Of course, since the introduction of MakerDAO's D3M module and Frax's AMO V2, they can output DAI and FRAX directly through protocols like Aave without needing collateral. When users borrow DAI and FRAX from Aave, the collateral is provided by the users, which improves the efficiency of capital expansion for the protocols. However, even this method is unlikely to meet the overall monetary demand scale of Web3 business.

- Multi-chain security risks. Whether it is Curve, Aave, or FRAX, they have deployed products across multiple chains. While multi-chain operations benefit these projects by allowing their stablecoins to be natively issued across various chains, they also amplify risks, meaning that security issues and bad debts on one chain may affect the entire system.

Final Thoughts

As the "disaster recovery value" of the Web3 settlement layer, decentralized stablecoins have further revealed their significance after the Tornado Cash incident. Of course, we believe that Circle will exercise restraint while assisting regulators in enforcement actions. If USDC blacklisting Tornado Cash is somewhat justifiable, when it targets the next DeFi protocol like Curve, it may lose the trust of Web3 users even faster than the protocol it sanctioned, being forced to exit this market.

But the question is, by that time, will decentralized stablecoins be ready to receive those users and funds fleeing from centralized stablecoins?

Currently, it is clear that they are not.

But it is precisely because they are "not ready" that the vast blank space in this market excites and inspires our expectations.