Failed algorithmic stablecoin projects: What issues did AMPL, ESD, and Terra encounter?

The decentralized non-collateralized algorithmic stablecoin represented by Terra has reached a historical turning point.

The decentralized non-collateralized algorithmic stablecoin represented by Terra has reached a historical turning point.Author: DODO Research Institute

This article analyzes the issues faced by several algorithmic stablecoin projects in history and draws some lessons they can teach us. It also aims to provide a summary at this turning point, offering some references for potentially better algorithmic stablecoin solutions that may emerge in the future.

The decentralized, non-collateralized algorithmic stablecoin represented by Terra has reached a historical turning point. This article analyzes the issues faced by several algorithmic stablecoin projects in history and draws some lessons they can teach us. It also aims to provide a summary at this turning point, offering some references for potentially better algorithmic stablecoin solutions that may emerge in the future.

The collapse of the Terra ecosystem is destined to be recorded in the annals of blockchain history. The decentralized, non-collateralized algorithmic stablecoin it represents has also reached a historical turning point.

This article analyzes the issues faced by several algorithmic stablecoin projects in history and draws some lessons they can teach us. It also aims to provide a summary at this turning point, offering some references for potentially better algorithmic stablecoin solutions that may emerge in the future.

The Dark Age of Uncollateralized Stablecoins: The Game of Air and Human Nature

Uncollateralized algorithmic stablecoins have no safety net; everything is built on participants' consensus about their value. However, during the early stages of algorithmic stablecoins, the entire blockchain ecosystem lacked sufficient use cases, making it difficult to endow such tokens with intrinsic value. This was a carnival for speculators and the most intuitive manifestation of the "Greater Fool Theory."

Ampleforth: Amplified Volatility and Compatibility Issues with Rebase Tokens

Ampleforth is often mentioned as one of the pioneers of algorithmic stablecoins. Its original design aimed to stabilize the token price at a value of 1 USD in 2019.

Mechanism

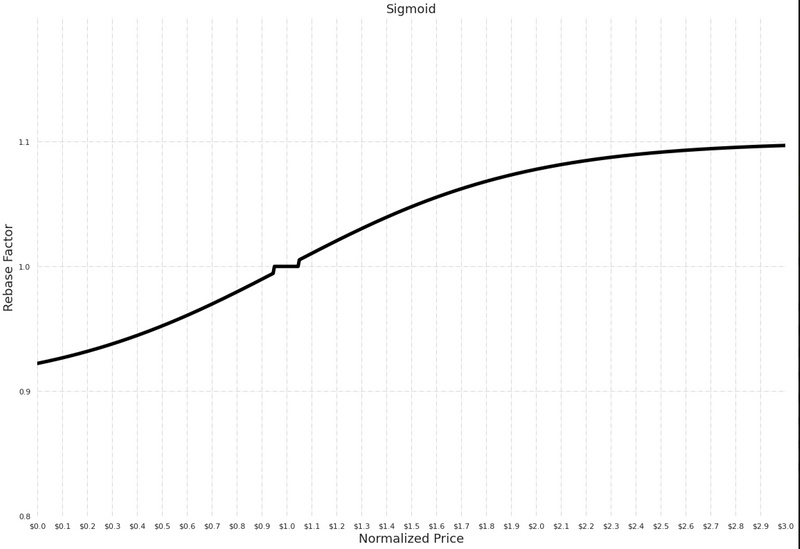

As a rebase token, its supply changes every 24 hours based on the target price:

When the price is within 5% of the target price (the current CPI-adjusted target price is 1.1 USD), the token supply remains unchanged.

When the price is more than 5% below the target price, the number of tokens held by all holders will continuously decrease until the target price is reached.

When the price is more than 5% above the target price, the number of tokens held by all holders will continuously increase until the target price is reached.

Currently, the entire increase process of AMPL is controlled by a proposal passed in February 2022, with a maximum daily change of either an increase of 10% or a decrease of 7.78%, occurring when the market price is above 3 USD or below 0 USD.

The volatility of AMPL mainly stems from the lag in market adjustments and the amplified fluctuations caused by rebase.

When the market changes drastically in a short period (such as a 50% drop in 24 hours), the Ampleforth protocol cannot directly absorb all the fluctuations at the next rebase time point. Instead, there will be an adjustment period Δt. During this period, the number of AMPL tokens will continuously decrease to reduce supply and thus increase price.

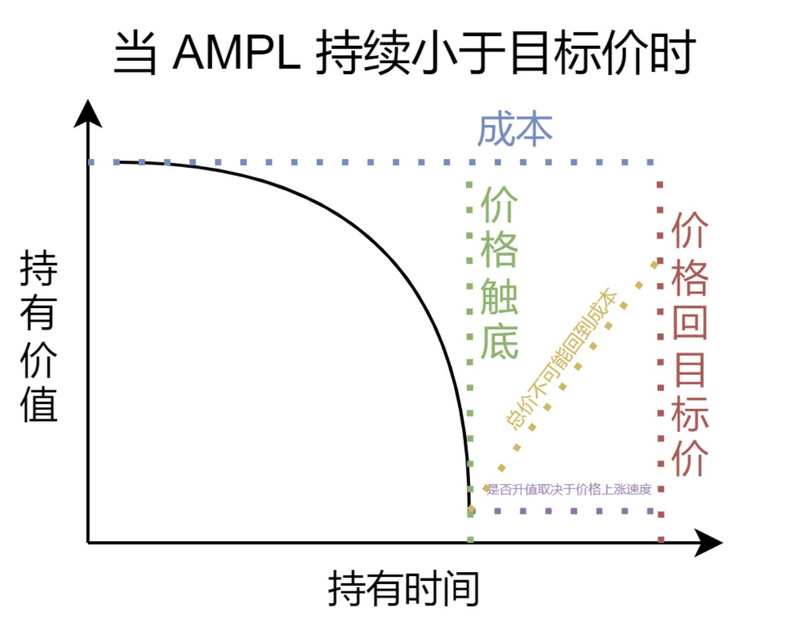

However, during its decline and rebase process, true holders actually bear a double loss pressure. On one hand, the token that was originally worth 1.1 USD is now worth less than 1.1 USD; on the other hand, the 1 token originally held will become less than 1 token after each rebase.

At this point, if no action is taken and the rebase token supply is allowed to decrease to pull the price back to the range of 1.1 USD, the price of the tokens held by the holders may return, but the number of tokens cannot. Therefore, during this period of volatility, holders actually suffer a net loss in terms of token quantity.

Game Theory

When the loss in token quantity due to the decline occurs, the most efficient remedial action, aside from selling tokens, is to continuously buy AMPL tokens when the price is below the target price, hoping to lower the average cost and profit after subsequent price increases. If this strategy is consistently executed, as long as the token price is below the target price, one must keep buying AMPL tokens until the average price is lower than the current price, thereby reducing losses through profits. However, buying also carries risks, because if the token price cannot rise back to the target price of 1.1 USD for an extended period, the tokens held will continue to shrink, resulting in ongoing losses. Therefore, in such situations, holders generally tend to sell early to cut losses. The selling pressure will also cause the price to continue to decline until enough people form a consensus that "buying can yield profits," allowing the token price to rebound.

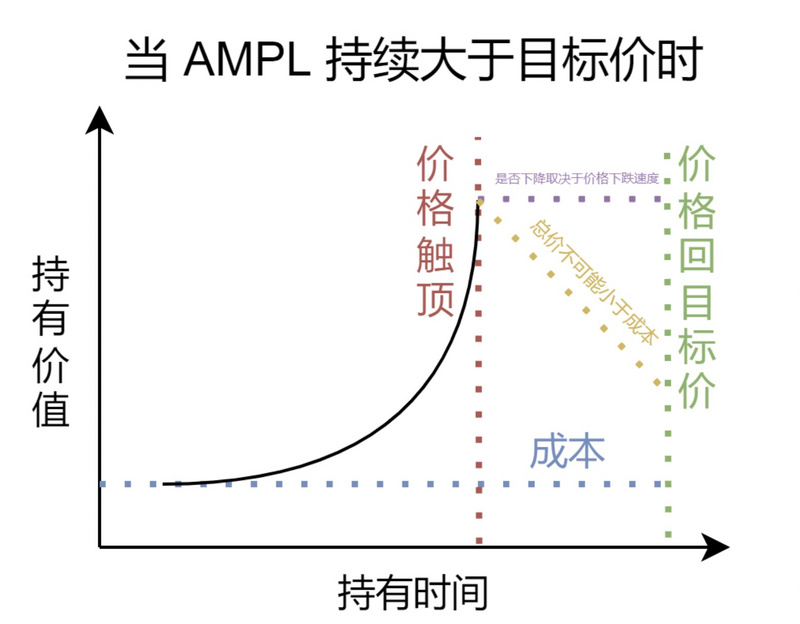

On the other hand, when AMPL is above the target price, the issuance of AMPL tokens allows token holders to continuously profit. At this time, the daily returns from holding AMPL can be quite substantial. In the blockchain market, the fear of missing out (FOMO) can drive a token to rise even higher during significant price increases or when high returns are available. If the AMPL price remains more than 50% above the target price, according to the curve, daily returns of around 5% can be achieved, which is enough to drive all speculators crazy. In this frenzy of returns, even though many people know that the continuous issuance will lead to selling pressure, as long as speculators keep promoting the high yield, more speculators will buy in at high prices, and together with the entire community, they will form a consensus of reinvestment (doing nothing), causing the token price to keep rising. Of course, the pressure from issuance will eventually reach a critical point; once there is any disturbance, the consensus will dissipate, bringing immense selling pressure to the entire token market. Moreover, since everyone has earned extra tokens when the price was above the target price, even if the current price is below the target price, selling can still yield a positive or break-even return. Thus, all historical surges of AMPL have ultimately led to trading prices significantly below the target price.

Incompatibility of Rebase with DeFi

In many DeFi lending or staking protocols, changes in the quantity of collateral assets make it difficult to calculate the collateralization ratio for loans. The high volatility of AMPL tokens leads to frequent rebases. Additionally, because the rebase mechanism directly changes the number of tokens held by addresses, various DeFi protocols need to implement special logic to provide real-time updates on token quantities for their AMPL users. Furthermore, as decentralized liquidity providers, they already bear the risk of impermanent loss from providing liquidity; the higher price volatility and changes in token quantity brought by AMPL's rebase make providers almost unwilling to take on this risk.

Summary

AMPL is one of the earliest attempts at algorithmic stablecoins in web3. Its simple and crude adjustments in supply relations, while directly addressing the essence of algorithmic stablecoins, ironically make it impossible to maintain long-term stability at the target price due to its rebase mechanism. Because the actual stabilization effect is poor, AMPL no longer promotes itself as an algorithmic stablecoin today. However, its stable mechanism has provided a foundation for the improvement of various algorithmic stablecoins that followed.

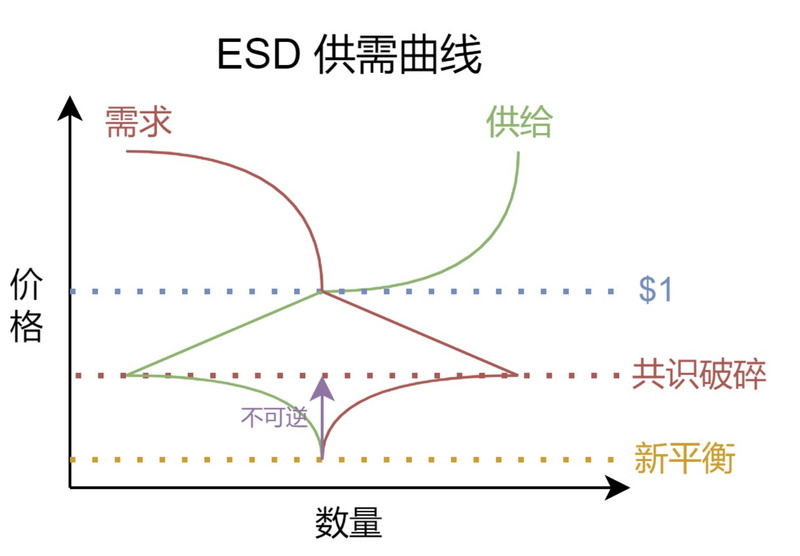

ESD: Losing Consensus Means Losing Everything

ESD is an algorithmic stablecoin modified from the original Basis white paper, and its mechanism is similar to Basis, which will be briefly skipped in this article. The introduction of the bond concept to stabilize currency value in ESD seems to have inherent problems, yet it also attracts speculators continuously. However, if all players are here for speculation, it becomes difficult for the project to establish a firm value consensus. Coupled with issues in its redemption mechanism, the entire uncollateralized ecosystem of ESD collapsed just four months after its launch.

Mechanism

ESD has an oracle that uses Uniswap v2 as its price source.

When the price is below 1 USD, ESD holders can burn their ESD to receive an equivalent bond. The bond has a validity period of 90 days (as stated in the original white paper).

During the bond's validity period, if the price is above 1 USD, bondholders will redeem their bonds in the order of submission. The system will generate new ESD to meet the bond redemption demand. If the bonds are fully redeemed and the price remains above 1 USD, new ESD will be distributed equally among all ESD stakers in the DAO.

ESD transfers the selling pressure onto the water; this practice ensures that its token price will be below 1 USD for most of the time.

When the market price is below 1 USD, speculators can buy low-priced ESD and gain the right to redeem it at the market price of 1 USD when the price rises above 1 USD. These bonds will enter a countdown to expiration upon purchase. Expiration will cause the face value to drop to zero, achieving deflation. All bonds will be "unlocked" through the inflation mechanism when the market price is above 1 USD. At the time of unlocking, due to the pressure of the countdown to expiration, the vast majority of bondholders will attempt to redeem their bonds. At this point, the ESD that was originally "locked" due to bond purchases will be unlocked due to the inflation mechanism, increasing liquidity and creating new potential selling pressure on the entire market.

Game Theory

When the price is above 1 USD:

On the supply side, ESD begins to inflate; the higher the price, the faster the supply increases.

On the demand side, due to the potential effects of ESD inflation, when the price remains above 1 USD, it means that staking rewards will be distributed to ESD stakers, leading to significant staking demand in the early stages. However, as the price continues to rise, speculators will gradually stop staking new tokens. At this point, the relative relationship between supply and demand remains unchanged, maintaining a balance point at 1 USD.

When the price is below 1 USD:

If it is slightly below 1 USD, the market will have strong confidence in its return to 1 USD and above, leading holders and new speculators to prefer purchasing bonds to gain priority in profiting above 1 USD.

However, as the price gradually deviates from 1 USD, market confidence in its return will decrease, increasing the risk of purchasing bonds. At the same time, the potential benefits of the bonds will also increase, attracting more high-risk preference capital into the market.

The game between risk capital and holders has no lower limit. When the price is low enough, and the market sees no possibility of recovery, panic selling will ensue. At this point, the consensus on ESD's standard price of 1 USD begins to fade. Risk capital will also become unwilling to buy bonds that lack consensus and cannot be redeemed. Thus, the supply-demand relationship will reverse until a new equilibrium point is reached, significantly below 1 USD.

At this point, the market has completely lost its consensus on ESD's standard price of 1 USD, and the mechanism to pull the price back to 1 USD when it is below that has completely failed, as no one will buy a bond that cannot be redeemed. Although there is no inflation at this time, there will also be no deflation. The market will fall silent and then move towards death.

Summary

At first glance, ESD's mechanism seems unproblematic; the bond's implicit destruction mechanism can effectively raise prices when below 1 USD. However, once its consensus is shattered, unlike AMPL, which can infinitely deflate, ESD has no remedial measures. Because at this point, no one is willing to buy bonds that cannot be redeemed but have a redemption deadline. Therefore, for ESD, losing the consensus of 1 USD means losing everything.

The Era of Collateralization: Playing with Human Nature and Greed

After countless failures in the uncollateralized era, everyone finally realized the importance of full collateralization. However, the stabilization mechanisms of algorithmic stablecoins also have their merits. Thus, starting with Frax, algorithmic stablecoins gradually entered the era of collateralization. Frax, as a project that can approach 0% collateralization or retreat to 100% collateralization, can be said to be one of the most stable algorithmic stablecoins currently. Meanwhile, the Terra ecosystem's stablecoin system, using its mainnet token as collateral, is also rapidly developing.

UST (Terra Money): A High-Risk, High-Reward Stablecoin Empowered by Mainnet (L1) and Mainnet Tokens

The emergence of UST answered a question for various L1 (mainnet) projects: how to better capture the expected future value of mainnet tokens? Terra chose to establish a stablecoin system.

Mechanism

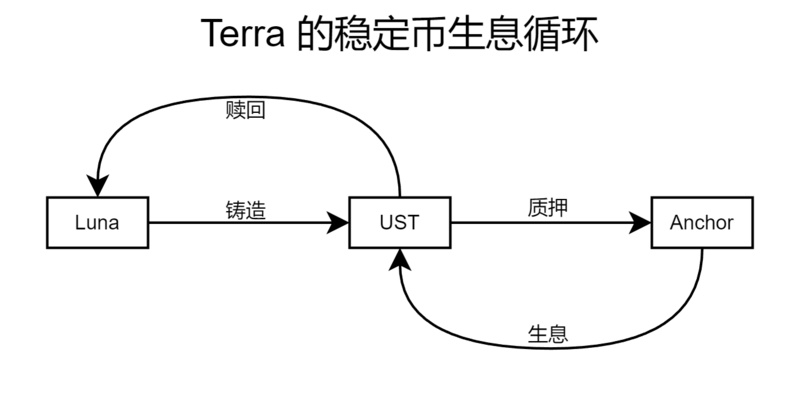

UST uses the Terra mainnet token Luna as collateral, and the entire ecosystem initially had no cash reserves.

When the price is above 1 USD, arbitrageurs can burn Luna purchased for 1 USD to mint UST and sell it at the current price above 1 USD for profit.

When the price is below 1 USD, arbitrageurs can buy UST at a price below 1 USD and exchange it for Luna at the market price of 1 USD to profit from selling Luna. This method of arbitrage has a maximum limit of 300 million USD per day, with the limit resetting every 36 blocks (later increased to 1.2 billion USD per day through proposals during the UST collapse).

The extreme interest-bearing liability structure that UST failed to adjust in time dealt it a fatal blow.

In 2020, Do Kwon proposed a solution to the problem of low staking rates for assets on the Terra chain. In mid-2020, one of the most efficient interest-bearing protocols in blockchain history, Anchor, was launched. Subsequently, under the attraction of a 20% interest rate, Anchor's total locked value (TVL) continued to rise. By January 2022, it reached nearly 5 billion USD. In just four months, it surged to a terrifying TVL of over 14 billion USD. On the eve of Luna's collapse (May 8), UST's total market cap was only about 18 billion USD, while the locked value of UST in Anchor was 14 billion USD.

At the same time, facing high yields, the seemingly harmless and stable UST attracted many people to pursue high leverage. Thus, although the extremely high interest-bearing locked value posed significant risks, the concentrated liquidation of leverage was also a key factor in the collapse.

At this point, it is no wonder that an 85 million USD sell-off could trigger a series of subsequent events.

Game Theory

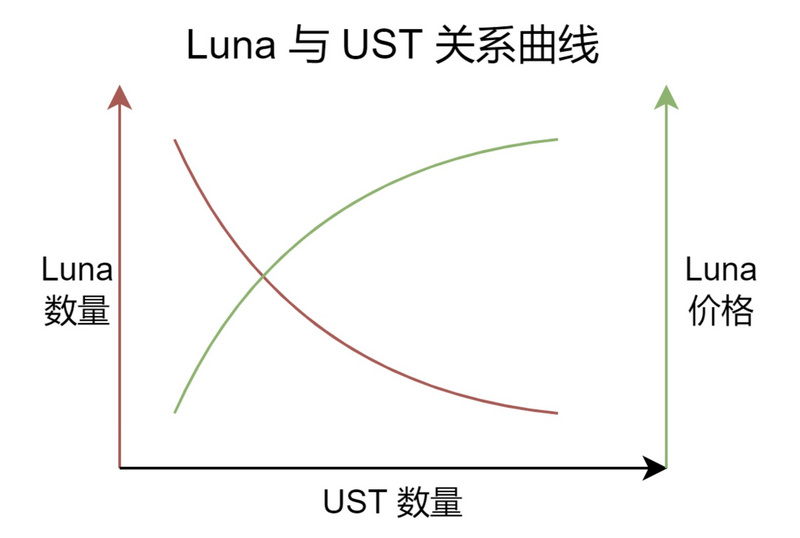

UST is a game between the mainnet token Luna in the Terra ecosystem. The value of Luna comes from its role as the mainnet token for gas fees and the POS mining mechanism for the entire ecosystem. UST transfers the value generated by Luna and exists in the Terra ecosystem in the form of a stablecoin, providing a better and more stable use case platform for Terra (compared to other mainnet tokens like ETH, which are more volatile). In this process, the value purchased by holders of Luna and UST is the same, namely the ecological value of the Terra mainnet.

So, if someone says that the primary value of the Terra ecosystem is the yield staking of Anchor's UST, doesn't that sound very much like a pure Ponzi scheme of money making money?

Moreover, the ecological issues of Luna and UST are not limited to Anchor. In the process of generating UST, the total market cap of Luna + UST should remain unchanged. This is because UST represents the market value burned by Luna and exists within the entire ecosystem. Minting UST should not be seen as a demand for Luna tokens but merely a form of conversion. Those who want to purchase Luna can also obtain it by buying UST and then exchanging it for Luna. However, in reality, the market views the minting of UST as a demand and consumption of Luna, leading to an extreme overestimation of Luna's value. The overestimation results in more UST being minted for fewer Luna, creating a vicious cycle and exacerbating the false prosperity.

In fact, as a mainnet ecosystem, the construction of UST is quite ingenious. However, for the Terra ecosystem, on one hand, Anchor's high yields rapidly built a financial empire worth billions, while on the other hand, Anchor's high yields immersed the public in a false sense of high value and ultimately led to collapse. The market's valuation of this model of value exchange between mainnet tokens and stablecoins also lacked sufficient understanding, ultimately exacerbating the entire collapse.

Throughout the process, the bottom line is that Anchor played with the public's greed, while UST manipulated the public's perception of value. Together, they packaged a financial empire's dream of wealth, leading countless people to become addicted and ultimately collapse together.

How to View Algorithmic Stablecoins in the Post-Terra Era

Do We Really Need Algorithmic Stablecoins?

The collapse of Terra has made many people very averse to non-overcollateralized or fully collateralized stablecoins, viewing them as Ponzi schemes that produce air. However, some believe that the collapse of Terra is not closely related to algorithmic stablecoins but rather due to the overall imperfection of the Terra Money ecosystem.

On May 25, 2022, Vitalik clearly favored the latter view and praised the stabilization mechanism of RAI in his article. On that day, he published two standards he uses to evaluate stablecoins.

Can stablecoins safely withdraw all users?

What happens when the stablecoin mechanism is pegged to an index that rises 20% annually?

For a detailed analysis, refer to the original text.

The essence of algorithmic stablecoins is a decentralized movement of minting rights, achieving what only states could do through user consensus and a series of algorithms on the internet. Of course, the current path of algorithmic stablecoins has not been smooth, especially with Terra's failure causing many to lose confidence, leading to the question: "Since there are already centralized compliant stablecoins like USDC and overcollateralized stablecoins like DAI, why do we still need algorithmic stablecoins?"

For these two types of stablecoins, the answer given by algorithmic stablecoins is also quite simple: centralized stablecoins face the risk of regulatory bans, while overcollateralized stablecoins face issues of capital efficiency. Since fully decentralized blockchain networks have emerged, why should everyone comply with centralized control? Since better capital utilization can achieve higher returns with lower collateral risks, why should more collateral assets be pledged? We should not fall into a storm of criticism simply because of the failures of current algorithmic stablecoin projects. As a practice of the future form of stablecoins, algorithmic stablecoins still have their value and necessity.

Does Every Public Chain Need Its Own Algorithmic Stablecoin?

After the success of algorithmic stablecoins in the Terra ecosystem, public chains like Waves, NEAR, and TRON have launched their own algorithmic stablecoins. Now that Luna has fallen from grace, a question arises: do other public chains need to launch their own algorithmic stablecoins?

Algorithmic stablecoins that coexist with the native tokens of public chains can provide better and more stable economic models for the public chains themselves. However, caution is needed regarding macroeconomic aspects to avoid repeating the mistakes of Terra. So far, there has not been a time-tested algorithmic stablecoin solution that can enhance the ecosystem of a public chain token. Therefore, in the short term, smaller public chains will maintain a cautious attitude towards any algorithmic stablecoins that intersect with their native tokens.

It is undeniable that stablecoins supplement an important asset for public chains, enriching their ecosystems. Currently, the cross-chain bridge assets of various other stablecoins are sufficient to support the stablecoin demand of an early-stage public chain. However, in the later stages, when a new public chain develops into a complete ecosystem and forms a system similar to a "nation," native algorithmic stablecoins will undoubtedly become an indispensable part of forming a complete financial system.

In Conclusion

The early uncollateralized algorithmic stablecoins proved that the path of being uncollateralized is not viable. Meanwhile, overcollateralized or fully collateralized traditional stablecoins have gradually become the mainstream in the market. The rise of Terra and UST was not accidental; using mainnet tokens as collateral to provide a stable settlement system for the ecosystem is a feasible path, but the financial regulation and balance involved are far from simple. The story of Terra constantly reminds us to view the value of mainnets rationally. Do not abandon the value that algorithmic stablecoins can bring to an ecosystem for the sake of so-called TVL, false prosperity, or greed for money.

Risk warning

Risk warning Risk warning

Risk warning