Let's talk about algorithmic stablecoins after UST fell into a death spiral

Due to the collapse of UST, the development of stablecoins has gained significant attention from the market and has also faced many doubts. What is a stablecoin, and what is an algorithmic stablecoin? Why did LUNA and UST collapse?

Due to the collapse of UST, the development of stablecoins has gained significant attention from the market and has also faced many doubts. What is a stablecoin, and what is an algorithmic stablecoin? Why did LUNA and UST collapse?Author: IOBC Capital

Once ranked as the third largest stablecoin globally, TerraUSD (UST) has recently collapsed rapidly, stirring the cryptocurrency community and attracting the attention of U.S. Treasury Secretary Janet Yellen.

During a hearing on May 10, Yellen emphasized the necessity of a regulatory framework for stablecoins. She stated that the current regulatory framework "does not provide consistent and comprehensive standards for the risks of stablecoins." Furthermore, Yellen specifically mentioned the significant de-pegging of UST.

Due to the collapse of UST, the development of stablecoins has gained significant market attention but also faced many doubts. What is a stablecoin, and what is an algorithmic stablecoin? Why did LUNA and UST collapse?

With these questions in mind, let's start with the development history of stablecoins. There are mainly three types of stablecoins in the blockchain industry:

1. Fiat-Collateralized Stablecoins

Due to regulatory policies in certain regions, exchanges cannot provide "fiat-to-crypto" services to users in those areas, which has facilitated the development of the first generation of stablecoins—fiat-collateralized stablecoins.

The main characteristic of fiat-collateralized stablecoins is that they use fiat currency as the underlying asset, with centralized institutions acting as the issuers, which have a rigid obligation to redeem. USDT, USDC, and BUSD are the main representatives.

USDT

USDT is a stablecoin pegged to the U.S. dollar launched by Tether. Like other cryptocurrencies, USDT is built on the blockchain and can currently be minted and traded on multiple public chains, including Ethereum, Tron, Solana, Algorand, EOS, Omni, and Avalanche.

The issuance, circulation, and destruction mechanism of USDT is as follows:

Illustration: IOBC Capital

Tether claims to strictly adhere to a 1:1 reserve guarantee, meaning that for every USDT issued, there is 1 dollar in its bank account as collateral. The reserve value of USDT is published daily and updated at least once a day, with reserves reviewed quarterly.

Source: Tether Official Website

According to the reserve report disclosed on December 31, 2021, Tether's reserves are not all cash; they include cash and bank deposits, treasury bills, commercial paper, certificates of deposit, money market funds, reverse repurchase agreements, corporate bonds, funds, precious metals, secured loans, and other investments.

USDC

USDC is a fully collateralized stablecoin pegged to the U.S. dollar issued by Circle, heavily supported by Coinbase. Grant Thornton publishes a public report every month disclosing the financial status of USDC issued by Circle.

Circle is backed by institutions such as Goldman Sachs, IDG, CICC, Everbright, Baidu, Bitmain, and Yixin Industry Fund, and holds payment licenses in all U.S. states except Hawaii, the UK, and the EU, making it the company with the most licenses in the crypto asset industry, providing compliant channels for USD, GBP, and EUR to enter crypto assets.

BUSD

BUSD is a stablecoin pegged to the U.S. dollar approved by the New York State Department of Financial Services (NYDFS) and issued in partnership between Binance and Paxos. BUSD is currently the third largest stablecoin, following USDT and USDC.

Fiat-collateralized stablecoins can generally meet the needs of ordinary trading users and have the advantages of ensuring peg and high capital efficiency. However, due to their centralized nature and the lack of transparency regarding underlying asset reserves, they often face scrutiny. Moreover, they require licensing and are subject to regulation.

2. Over-Collateralized Stablecoins

The main characteristic of over-collateralized stablecoins is that they use mainstream cryptocurrencies (such as ETH, BTC) as over-collateralized underlying assets. The primary representative of over-collateralized stablecoins is MakerDAO's DAI.

As the name suggests, in over-collateralized stablecoins, the value of the collateralized assets exceeds the value of the minted stablecoins. For example, if you stake $100 worth of ETH, you can only mint 70 DAI. If the collateralization ratio falls below the minimum requirement, you will be required to add more collateral; if you fail to do so and fall below the liquidation threshold, your position will be liquidated, incurring liquidation penalties.

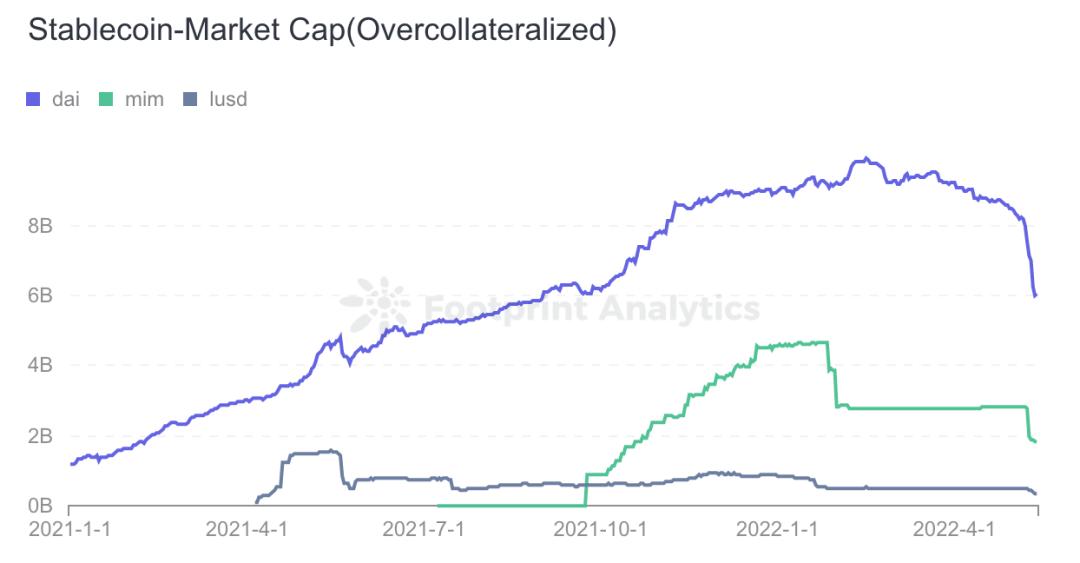

According to Footprint Analytics, the current market size of over-collateralized stablecoins is approximately $8 billion.

Data Source: Footprint Analytics

The biggest feature of over-collateralized stablecoins is their stability, as there is no concern about the opacity of centralized institutions; however, their downside is low capital efficiency and high security requirements for smart contracts, as well as certain performance requirements for the blockchain network, especially during significant price fluctuations of collateralized assets.

3. Algorithmic Stablecoins

Both fiat-collateralized and over-collateralized stablecoins have their drawbacks. Therefore, there has been exploration into algorithmic stablecoins within the industry.

People's attitudes toward algorithmic stablecoins are generally polarized: supporters view them as a monetary reform, while opponents see them as a Ponzi scheme.

Chart Source: Footprint Analytics

The development history of algorithmic stablecoins has been quite tumultuous. From AMPL, ESD to BAC, and then to Frax, Fei, OHM, these algorithmic stablecoins have garnered some attention in the community but have also faced abrupt endings. The only one that truly achieved a leap in market capitalization is UST, which once exceeded $18 billion, briefly surpassing BUSD to become the third largest stablecoin globally.

UST (TerraUSD)

UST is an algorithmic stablecoin launched by Terra. Terra launched its public chain and its native token LUNA in 2018, and later designed a dual-token system—using a two-way minting and burning mechanism between LUNA and UST to maintain UST's peg to $1.

The minting and burning logic of UST:

When 1 LUNA = 100 U, burning 1 LUNA can mint 100 UST; burning 1 UST can mint 0.01 LUNA.

The mechanism for UST to maintain stability:

UST achieves stability through an arbitrage mechanism. When UST > $1, users can burn $1 worth of LUNA to mint 1 UST, then sell UST in the secondary market for profit; when UST < $1, users can burn 1 UST to mint $1 worth of LUNA, then sell LUNA in the secondary market for profit.

For example:

When 1 UST = $1.5, users can burn $1 worth of LUNA to mint 1 UST, then sell it in the secondary market for $1.5, making a profit of $0.5. As more selling occurs, the price of UST will approach $1;

When 1 UST = $0.5, users can buy UST in the secondary market for $0.5, then burn 1 UST to mint $1 worth of LUNA, and sell LUNA in the secondary market for a profit of $0.5, pulling the price of UST back to $1 through arbitrage.

Why did UST grow to a market size of $18 billion?

At its peak, UST reached a market size of $18 billion, while the native token LUNA of the Terra public chain surged to a circulating market value of over $40 billion. In addition to the premium from the bull market cycle, it also relied on the development of its public chain ecosystem's DeFi.

First, Terra launched the algorithmic stablecoin UST based on its public chain's native token LUNA. Moreover, backed by investment from South Korea's second-largest payment group, it designed use cases for UST—consumption, payment, e-commerce, etc. For instance, Terra partnered with the mobile payment app Chai, allowing businesses to easily implement settlement transactions, with a total user base of 2.3 million.

Second, Terra also launched the synthetic asset protocol Mirror, increasing the financial applications of UST. In the Mirror protocol, UST can be over-collateralized to generate synthetic assets (such as stocks of leading tech companies like Google, Apple, Amazon, Tesla) to meet the investment needs of users who cannot directly invest in these assets (U.S. stocks).

Finally, Terra's most ambitious move was launching a savings protocol, Anchor, with an annual yield of up to 20%. Users only need to store UST in the Anchor protocol to earn nearly 20% annual interest and receive ANC token incentives.

Based on these various use cases for payments, investments, and savings, Terra established a highly leveraged ecosystem. In just two years, LUNA grew to a market value of over $40 billion, minting and issuing $18 billion worth of UST.

This development seemed very promising, but in reality, the minting logic of UST and its stabilization mechanism had already predetermined today's collapse.

Charlie Munger has a famous saying: "Tell me your motives, and I can tell you your outcome."

Many in the community have begun to suspect that the collapse of Terra may be the result of the project team cashing out at high prices. Why is there this feeling? The community has raised four main questions:

1. The flow of funds. Who minted LUNA and UST, and who took over?

It was mainly the project team that minted, while many holders of LUNA and UST during the collapse took over.

2. How can a stablecoin offer an annual yield of up to 20%?

To attract more people and more funds to take over. Investors must hold UST and stake it to earn the 20% annual yield. What can the borrowers of the Anchor protocol do with these funds to guarantee an annual yield of over 20%?

3. Where did over 80,000 Bitcoins go?

This question is currently the most concerning for people, including Binance's CZ, who publicly questioned on Twitter: Where did Terra's Bitcoin reserves go when it faced difficulties?

When UST began to decline on May 9, LFG announced it would start disposing of these over 80,000 Bitcoin reserves to stabilize the peg of UST to the dollar. The next day, LFG's Bitcoin reserves were completely depleted.

According to on-chain tracking by crypto data analysis company Elliptic, 52,189 BTC were transferred to Gemini, and another 28,205.5 BTC were transferred to Binance.

Source: Elliptic

On the morning of May 9, LFG announced it would "collateralize BTC loans of $750 million to help UST re-peg," and at the same time, 22,189 BTC (worth approximately $750 million at the time) were transferred from the LFG address. Later that evening, another transfer of 30,000 BTC was made to the same address. In the following hours, these 52,189 BTC were transferred to Gemini, after which it was impossible to determine whether these Bitcoins were sold to support the UST price or transferred to other wallets.

Similarly, the remaining 28,205.5 BTC of the LFG foundation, after being transferred to Binance on May 10, also cannot be determined whether these BTC were sold to support UST or transferred to other wallets.

In response to the community's doubts, the LFG foundation has not disclosed specific details regarding the disposal of these over 80,000 BTC.

4. Regardless of whether LUNA collapses or UST de-pegs, why did the Terra team mint a large amount of additional LUNA?

In addition to the unclear whereabouts of the 80,000 Bitcoins, the Terra team minted over 60 trillion additional LUNA between May 10 and 13, which is completely unreasonable and violates the spirit of blockchain.

Based on the above, the community has raised doubts: the collapse of LUNA and UST in the Terra project may essentially be the result of the project team cashing out at high prices. Why didn't Terra directly sell LUNA at high prices? Because most LUNA tokens are actually held by the project team; if the project team directly sold LUNA in the secondary market, the maximum market value of $40 billion could not cash out over 80,000 Bitcoins (worth over $3.2 billion at the time), let alone minting $18 billion of UST. Moreover, financial protocols like Mirror and Anchor, which lock in UST liquidity with high yields, strongly supported the realization of their cash-out actions. This is similar to major shareholders cashing out in the securities market; they often do not directly sell in the secondary market but use collateralized loans—mortgaging shares to banks to obtain funds.

Conclusion

The collapse of UST should serve as a warning to other similar algorithmic stablecoin projects, such as Waves' USDN. In the Waves public chain ecosystem, the annualized interest rate for borrowing stablecoins like USDT and USDC in the Vires lending protocol has been as high as 40% for some time, raising questions in the community about what this is used for and how such high stablecoin borrowing rates can be accepted.

Each type of stablecoin has its advantages and disadvantages. Fiat-pegged stablecoins have drawbacks such as centralization, opacity, and regulation, but they also have advantages like high capital efficiency and ensuring the peg; over-collateralized stablecoins are stable, decentralized, and resistant to censorship, but they have low capital efficiency. Although algorithmic stablecoins have gone through several generations of development and evolution, there has yet to be a successful case of "too big to fail."

In the core mechanism design of algorithmic stablecoins, there may still be much practical exploration needed. At least the following aspects need to be considered:

First, the choice of underlying assets for algorithmic stablecoins. Taking UST as an example, it uses LUNA as the corresponding underlying asset during minting and burning, but is the consensus around LUNA itself already strong enough? This may have consensus within the Terra ecosystem, but the consensus around burning LUNA to mint UST is not strong enough in the broader crypto community, in the traditional consumer market in South Korea, or in the global financial sector. The degree of decentralization of LUNA tokens is too low and highly concentrated, making it hard not to feel that the project team, when LUNA's price was high, could not sell in the secondary market and thus minted UST to cash out at high prices, which is undoubtedly a high-risk event for subsequent holders and users of UST.

Second, what collateral (burning) parameters can balance safety and capital efficiency? Again taking UST as an example, burning $1 worth of LUNA to mint 1 UST is much more capital efficient compared to over-collateralized stablecoins like DAI. It did not choose globally recognized assets like BTC or ETH as the underlying minting assets and did not set a collateralization rate above 100%. The setting of collateral (burning) parameters needs to consider not triggering insolvency during price fluctuations of the underlying assets.

Third, the demand for stablecoins and the sequence of minting and how to regulate it. Since it is a stablecoin, theoretically, it has no investment value; if it does not have sufficient utility or use cases, it is difficult to maintain its consensus. Therefore, I feel that it may be necessary to strictly control the minting quantity based on usage demand and usage rate to manage overall risk. This should not be a false demand set to lock in circulation but rather a genuine equivalent.

We cannot dismiss the future prospects of algorithmic stablecoins just because of the failures of current projects. Economist Friedrich August von Hayek wrote in "The Denationalization of Money": "I believe that humanity can do better than gold in history."

In the crypto world, there may emerge an algorithmic stablecoin that gains sufficient consensus, just as Bitcoin has achieved its influence and recognition today. Perhaps, like Bitcoin, consensus will arise in that way—who knows?

Risk warning

Risk warning Risk warning

Risk warning

Popular articles