Delphi Digital: Feasible Improvements for veToken

The veToken economics pioneered by Curve is one of the best incentive adjustment mechanisms to date, but there is still room for improvement.

The veToken economics pioneered by Curve is one of the best incentive adjustment mechanisms to date, but there is still room for improvement.Original Authors: Jeremy Ong and Duncan Reucassel

Original Compilation: DeFi Path

Key Points

veToken economics incentivizes liquidity providers to become long-term stakeholders in DEX protocols. This is achieved by giving more rewards and governance power to those who lock up the underlying tokens.

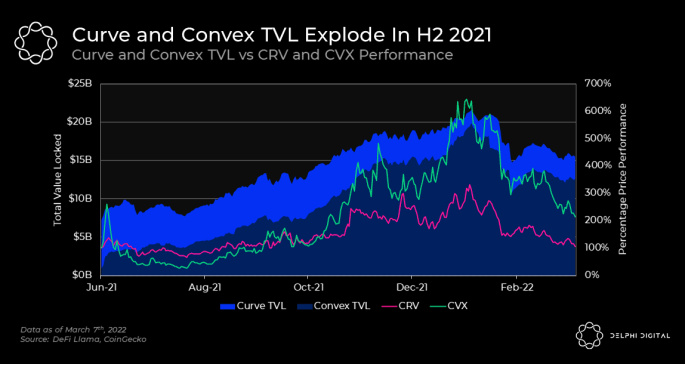

Curve and Convex created a powerful flywheel that caused token prices and TVL to soar in the second half of 2021. This brought hype to the veToken model and attracted both supporters and critics. This article aims to examine these criticisms in detail.

We leverage our extensive research on the Curve/Convex relationship to develop an alternative approach to the veToken model. This alternative is illustrated through a hypothetical token called "GOV," which will be discussed in this article.

The goal of our proposed approach is to reduce centralization while still maximizing the core attributes of veToken: rewarding the most long-term and focused participants, without excluding contributors who cannot bear the illiquidity risks inherent in traditional veToken economics.

Curve and veToken Economics

The rise of cryptocurrencies and tokenization has opened up the design space for protocol economics, allowing projects to incentivize specific behaviors. However, many DeFi protocols reward all token holders equally, regardless of the value they add to the project. More often than not, there is little requirement to lock up tokens in exchange for governance rights and protocol revenue. We believe that optimal design aims to dilute speculative capital while rewarding long-term oriented participants.

We see one model that encourages this behavior as the implementation of vote-escrow introduced by Curve. This model allows CRV holders to lock their tokens as vote-escrowed CRV (veCRV) for a maximum of 4 years. The longer users lock their CRV, the more veCRV they receive. In exchange for bearing liquidity risk and removing CRV supply from the market (demonstrating their long-term commitment to the platform), veCRV holders are entitled to three main benefits:

Proportional sharing of fees generated by Curve.

Enhanced CRV rewards for liquidity provision positions (up to 2.5x).

Governance and gauge weight voting rights. Importantly, gauge weight determines how Curve allocates future releases.

This series of incentives creates a positive flywheel. The more long-term oriented users are (measured by their veCRV), the more rewards they will receive. This flywheel is one of the most important drivers of the veToken model, which we will explore in detail in the next section.

Curve's long-term value proposition is to become the deepest and most liquid venue for trading stable assets. Its goal is not necessarily to become the primary DEX for everyday exchanges, but to empower stablecoin projects to build large liquidity reserves. This means that their primary users in terms of supply are liquidity providers.

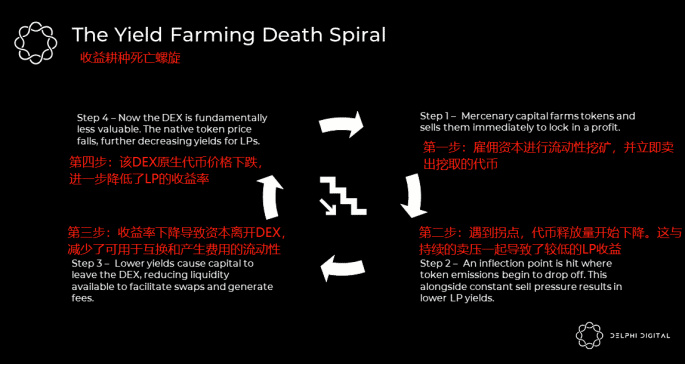

Many failed yield farming schemes have been ruined due to unsustainable token releases and the dilution of speculative capital. Here is an example that veToken economics aims to avoid:

An initial liquidity mining program is launched, followed by speculative capital depositing large amounts solely for mining, then dumping the rewards.

Initially, this leads to a reflexive rise. As TVL and the "hype" around the project increase, token prices will also rise. This can further enhance the yield on deposits, as yields are paid in the native token, continuing the cycle.

Eventually, a tipping point is reached where token incentives begin to decrease, while speculative capital continues to sell the tokens they mined. As token releases decline, this selling leads to a decrease in yields for liquidity providers.

Ultimately, a reflexive downward cycle begins to take effect as liquidity exits the DEX, fundamentally losing value. Lower liquidity means the DEX cannot support as much trading volume, resulting in fewer fees. This leads to further devaluation of the fundamentals and a drop in the price of the native token, further reducing LP yields.

The veToken model avoids this situation by aligning liquidity providers' long-term interests with those of the protocol.

To earn 2.5x rewards on Curve, liquidity providers must hold a certain amount of veCRV corresponding to their liquidity. This incentivizes LPs not to sell their tokens but to:

Purchase positions of CRV on the open market and lock them.

Lock all or part of their earned CRV liquidity rewards.

This also encourages liquidity providers on the Curve platform to become long-term stakeholders and supporters of Curve's success—rather than adopting a strategy of speculative mining and dumping.

Moreover, this not only incentivizes LPs to lock for the 2.5x growth rewards but also encourages them to accumulate as much veCRV as possible. This is because veCRV sets the gauge weight, allowing holders to direct token releases to the pools where they have funds (more veCRV = greater influence on token releases).

We have seen that the accumulation of CRV occurs not only among large LPs but also at the protocol level through Convex. Various protocols are leveraging the large amounts of veCRV held by Convex to accumulate CVX to incentivize their liquidity pools, ensuring long-term liquidity.

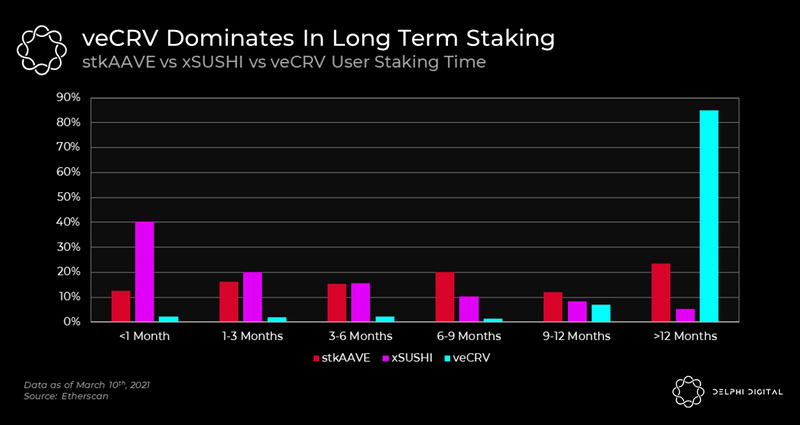

Through the elongated distribution schedule of CRV (over 300 years, releasing 15% per year) and the combination with veToken economics, it has been able to incentivize a group of very sticky liquidity providers and token holders. This can be illustrated by the lock-up times/holdings between stkAAVE, xSUSHI, and veCRV.

In addition to the economics, veCRV also provides time-weighted governance power to lock-up participants, which aligns the incentive mechanisms well (the longer the lock-up time, the greater the impact on governance). This part will be elaborated on later.

Market Response: Liquid Staking Derivatives and Convex

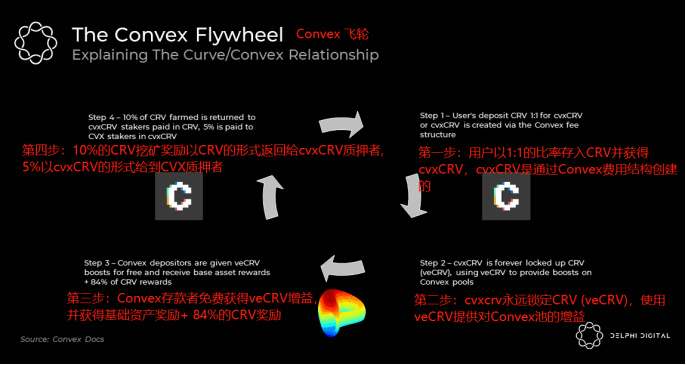

Given the immense utility of veCRV and its apparent lack of liquidity, the market has responded through Convex. Convex offers an irredeemable, liquid veCRV staking derivative called "cvxCRV." If holders wish to maintain liquidity, they have no way to do so with regular CRV, as all governance rights and fees belong to veCRV. Convex capitalizes on this by allowing users to lock their CRV permanently within Convex in exchange for cvxCRV. cvxCRV is a highly liquid and yield-generating token, with returns coming from the underlying veCRV fees, Convex platform fees, and CVX releases.

In exchange for providing high-yield liquid tokens, Convex utilizes all the incentives, governance rights, and gauge weights provided by the underlying veCRV for the platform and CVX holders.

Convex's core product allows Curve LPs to deposit their LP tokens within the platform. Depositors can earn higher yields (up to 2.5x), in return, Convex charges a percentage fee (10%) on CRV mining, which is then paid to cvxCRV holders. Additionally, another 5% of the CRV mined through Convex is returned to CVX stakers in the form of cvxCRV. This creates the flywheel shown in the diagram below.

Convex also allows CVX holders to gain governance and gauge weight over the underlying veCRV. CVX holders can vote on governance and receive incentives from third-party systems to direct their votes toward specific weight releases (also known as "buying votes," "voting incentives," "bribery," "lobbying," etc.). If you want to delve deeper into the relationship between Curve and Convex, you can refer to our previous article.

Throughout 2021, Convex undeniably played a positive role in the overall metrics of Curve's TVL and token price. However, Convex's liquid staking derivatives caused a massive supply shock to CRV, as users rushed to hand over their tokens to the Convex platform, which locked them permanently.

Alternative Approaches to veToken Economics

The remainder of this report will discuss common criticisms of veToken economics and how these criticisms can be addressed through an alternative implementation. For simplicity, we will illustrate using a hypothetical token called GOV.

This hypothetical GOV token will have the following main design features, each of which will play a role in leveraging the incentive adjustment lessons learned from Curve while aiming to avoid the emergence of a single, dominant, Convex-like proxy voting system.

It will utilize a three-token structure, combining features of Curve and governance similar to Sushiswap:

GOV represents the unstaked underlying governance token, similar to CRV. It does not provide voting rights and has no smart contract system fees.

xGOV represents the transferable governance token obtained by staking GOV, similar to xSUSHI. xGOV provides liquidity risk for GOV and entitles holders to a share of smart contract system fees and governance power.

vxGOV represents the non-transferable governance token obtained by locking GOV, similar to veCRV. vxGOV entitles holders to a larger share of smart contract system fees and governance power.

It will avoid requiring a proxy voting system (similar to Convex entities) to be "whitelisted" by the governance layer.

It will allow long-term staked positions (vxGOV) to terminate early with penalties (i.e., it will allow "exit" from the protocol DAO).

It will provide an in-protocol voting incentive (also known as "bribery") mechanism.

We will discuss this three-token GOV model and demonstrate how it addresses the criticisms that have emerged from our research on Curve/Convex, including comments from MonetSupply and Hasu on MakerDAO governance forms in a discussion.

1 Reduced Investor Base Due to Long-Term Locking

One argument against veTokens is that long-term locking makes it difficult for entities like index funds and trusts to incorporate these tokens into their products, reducing the potential "governance base" of the protocol. While it can be argued that this may reduce participation from certain entities, we believe this is a case of quality over quantity. The primary use case for trust and index products is speculation. When it comes to governance, these entities become apathetic and non-growth stakeholders.

In our view, having a few highly engaged stakeholders is better for a community than having a large number of passive and disinterested stakeholders. The entire point of veToken economics is to shift governance power from short-term thinkers to long-term oriented participants.

Another argument is that "during the transition of ownership, governance security will significantly decline when large holders stop re-locking tokens in preparation for sale." However, this argument assumes that there will be no other governance participants stepping in to fill the gap. Additionally, the framework of "governance takeover" seems inaccurate. Those who engage in "takeovers" are the largest stakeholders in the game due to their locked veCRV holdings, thus naturally incentivizing them to make positive changes to the protocol.

Our position is that by directing governance power to those who invest the most in the platform, the incentive effects far outweigh the downsides of excluding speculative entities from governance. Furthermore, the transfer of governance power from disinterested large holders who wish to stop re-locking tokens to new stakeholders filling the gap is a healthy practice.

Moreover, we believe the GOV model significantly alleviates this issue by providing an equivalent of liquid staking within the protocol, xGOV.

vxGOV (the veCRV version of this model) is designed to be the most attractive to liquidity providers and long-term oriented investors, which makes sense as vxGOV holders are the most important stakeholders in the ecosystem.

On the other hand, this does not mean that other participants cannot bring value and should be excluded from participation. This is where xGOV comes into play.

xGOV is a staked GOV position with liquidity. It can earn a share of the fees generated by the smart contract system while gaining governance capabilities. This allows potential value-adding stakeholders to still participate and contribute to the relevant ecosystem, while long-term and focused participants retain most of the power and fees through holding vxGOV. The exact fee distribution and resulting annual rates will depend on many factors. However, vxGOV will enjoy more benefits than xGOV.

We believe that xGOV-style tokens help bridge the gap and attract a group of people who benefit the project without bearing the illiquidity risks associated with long-term veCRV-style positions (vxGOV).

2 Staking Derivatives

Another common argument against veTokens is the liquid staking derivatives that arise from them. These staking derivatives allow token holders to forfeit governance rights in exchange for fees and short-term liquidity benefits. This, in turn, has two potential negative effects:

The fragility of the "soft peg."

The potential emergence of a dominant "proxy voter" holding a large proportion of governance power, especially in the case of whitelisting.

In our previous research on the relationship between Curve and Convex, we were primarily concerned about the fragility of the liquid staking derivatives' peg to the underlying governance token.

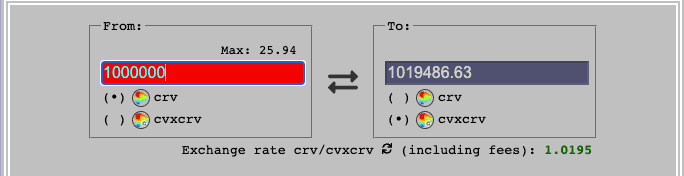

The "peg" between cvxCRV and CRV is maintained through liquidity mining incentives targeted at Curve's stablecoin exchange pools. This pool facilitates low-slippage trading between the two assets within a strict range. If you want to understand how these pools differ from traditional X*Y=K AMMs, we recommend reading Curve's stablecoin pool paper. To illustrate this, let's delve into some data.

At the time of writing this report, Curve's liquidity pool includes 17.43 million CRV (29.76% of the pool) and 41.13 million cvxCRV (70.24% of the pool). Despite this imbalance, cvxCRV only has a 2% discount on CRV in a trade of 1 million CRV.

Notably, out of 188 million circulating cvxCRV, only about 41 million are in this stablecoin exchange pool, and most (~76.87%) are staked for protocol rewards.

Notably, out of 188 million circulating cvxCRV, only about 41 million are in this stablecoin exchange pool, and most (~76.87%) are staked for protocol rewards.

Without a way to redeem each cvxCRV for the underlying CRV, we believe this soft peg will continue to deteriorate over time. This will suppress new CRV locking, as users find it cheaper to buy cvxCRV through Curve pools than to convert 1:1 on the Convex platform.

While this is a structural issue, let's look at what Convex can do to help strengthen the peg.

Currently, 10% of all CRV mining rewards on Convex are returned to cvxCRV stakers. This percentage could be increased to a maximum of 15%. This would increase the returns generated from these mining rewards.

The Convex DAO could use a portion of the protocol's veCRV holdings to vote perpetually on gauge weights for the cvxCRV/CRV pool to incentivize LPs.

Fees flowing into the protocol treasury are currently set to 0%. This could be raised to a hard-coded limit of 2% and used to purchase cvxCRV, helping to maintain the peg.

While the peg is crucial, we believe that the earning potential of cvxCRV must also be considered when reviewing it. Even if the peg may break, if cvxCRV can continue to provide attractive yields, it will still hold value.

3 Governance Centralization

Regarding governance centralization, we agree that allowing a protocol to control over 50% of governance power is unhealthy. However, we believe this is a special case for Curve/Convex and not a general issue with the entire veToken economy. Given the novelty of Convex at its launch and its influence over Curve's whitelist, Convex was able to capture over 50% of veCRV. Without the first-mover advantage and the ability to block competition through whitelisting, Convex would have faced fierce competition from the start. In the future, we urge protocols intending to adopt veToken economics to launch without whitelisting. This would promote competition among several Convex-like protocols and maximize decentralization.

In addition to concentrating voting power by holding the most veCRV, the current Convex architecture also heavily relies on the multi-signature identity of administrators to convert vlCVX votes into Curve DAO proposals and gauge weights. This constitutes another significant centralization issue, as a 3/5 multi-signature can effectively control over 50% of veCRV voting power.

In summary, we would like to emphasize several proposals that can reduce the risks associated with governance centralization as it relates to Curve/Convex.

Before implementing partial voting, if 51% of vlCVX votes in favor of a proposal, then all veCRV controlled by Convex will vote in favor in the Curve DAO. In this example, after implementing partial voting, only 51% of the protocol-controlled veCRV would vote in favor, while the other 49% would vote against.

Incentive Adjustments:

Convex's success is highly dependent on Curve. One way to value CVX is to calculate the present value of all future bribes that CVX can generate from the CRV releases it influences. Given Convex's dependence on Curve and the price of the CRV token, it seems unlikely that Convex stakeholders would act maliciously toward Curve.

So far, the relationship between Curve and Convex has primarily been symbiotic. This can extend to other protocols participating in the "Curve Wars," such as Frax, Terra, Redacted, Olympus, and other protocols actively accumulating more CVX. The veToken model and its ability to guide future CRV releases have united the top protocols in the entire space to collectively accumulate CRV/CVX and further adjust incentive mechanisms.

Trust-Minimized Proxy Voting:

While it's easier said than done (especially in conjunction with partial voting), teams building future versions of Convex or its equivalents should consider constructing systems in a trust-minimized manner. For example, the underlying governance power of veCRV is best transferred to vlCVX equivalents through smart contracts in a trustless manner.

4 Bribery and Short-Term Incentives

Bribery as a form of monetizing governance has stirred waves in the DeFi space—more specifically, to guide future token releases. Referencing a snippet from the MakerDAO forum: "As long as the bribery yield (bribe paid/CRV rewards) is higher than the percentage of CRV locked, veCRV holders can still benefit by diluting the unallocated holders."

One rebuttal to this argument is that when it comes to accepting bribes in exchange for weight voting, token dilution will occur regardless of whether bribes are received. In our view, the term "bribery" here is somewhat misnamed.

Jokes aside, there seems to be a knee-jerk negative reaction to bribery, which we believe is unwarranted. In the real world, bribery is referred to as "lobbying," which is a multi-billion dollar industry. At least in Web3, it appears that "lobbying" tends to be transparent, as it mostly occurs on-chain. Additionally, it is important to note that regardless of whether veToken economics are in place, these "incentivized voting methods" will emerge. We have already seen this in the case of the Bribe Protocol and Aave. We expect this trend to continue.

5 veToken Economics Increases the Cost of Defense Against Governance Attacks

To attack a veToken system through governance, an attacker must purchase and lock their voting power. This significantly increases the cost of the attack, as the purchased tokens cannot be reclaimed and sold. This is the foundation behind the veToken economic incentives.

However, critics of veToken economics argue that this is a double-edged sword, as it also raises the cost of defending against attacks. For example, if an attacker decides to purchase and lock enough vxGOV to gain 51% of the voting power, defenders will have to increase their voting power by re-locking vxGOV or purchasing more GOV to fend off malicious proposals.

We find this argument quite weak, as it is bidirectional. Considering that attacking a protocol utilizing veToken economics requires purchasing and maximizing locking for maximum impact, we see this as a net positive.

Providing significant governance power to lock-up participants can prevent attackers from borrowing the protocol's governance tokens and voting maliciously. In this case, attackers would only incur the impact of borrowing interest without facing the long-term downsides of poor decisions. Here is an old example where an attacker managed to influence MakerDAO's governance using flash loans. While this is an extreme case facilitated by flash loans, it still allowed the attacker to borrow tokens and vote on malicious proposals without incurring significant price risk.

We believe that veToken economics is one of the best defenses against such attacks—even if governance is centralized within Convex or similar protocols, as vlCVX holders are locked for 16 weeks, they will bear the consequences of harming Curve.

Learning from Curve/Convex to Formulate the GOV Model

We formulated our hypothetical GOV model based on extensive research on the Curve/Convex relationship.

Every change to the existing model has the potential to disrupt the flywheel that made Curve/Convex so successful in 2021. We believe that the following measures of the hypothetical GOV system can maintain the veToken flywheel while significantly alleviating some of the concerns raised in the previous section:

1 No Whitelisting

One of the main reasons Convex was able to hold >50% of governance power within Curve is the lack of competition. Given that Convex's design was the first of its kind, it had the opportunity to accumulate a large amount of veCRV before any competitors discovered it. At this point, it was already too late for other competitors, as Convex could leverage its veCRV power to control Curve's whitelist, effectively blocking further competition.

Now that the market is aware of Convex's model, new projects should announce their transition to veToken-based models with a considerable lead time. This allows many market participants to prepare for their launch. As a result of competing from the start, we believe this will encourage two things:

A fairer governance distribution than Curve, as many projects will have the opportunity to accumulate the underlying GOV token. This makes it unlikely for a single entity to accumulate >50% of governance.

Additionally, it can encourage each project to focus on maintaining the peg of liquid staking tokens. Projects that can best maintain their peg will be able to continue accumulating GOV in the future. While Convex's cvxCRV has maintained its peg quite well so far, we firmly believe that the more competition, the better.

2 Rage Quit

We believe the appeal behind cvxCRV lies not only in its high annual yield but, more importantly, in its liquidity. Therefore, we have considered several different methods to retain the benefits of the veToken design while still providing potential liquidity for depositors when needed.

The first option is to make vxGOV positions transferable NFTs (like Solidly). While this greatly reduces the appeal of abandoning GOV tokens and moving to a Convex-like protocol, pricing these NFT positions would be challenging. We can also assume that sellers would be willing to discount these positions in the secondary market, which could reduce the appeal of locking GOV tokens.

If vxGOV positions can be purchased at any time, then for potential GOV buyers, the question "If I can directly buy the NFT at a discount, why should I lock GOV?" will be a fair one. With this in mind, we believe another better option is to introduce the ability to rage quit vxGOV positions with significant penalties. Projects can implement various strategies, and here are some potential ideas on how to implement a rage quit feature for our hypothetical vxGOV:

If you have maximally locked vxGOV and wish to exit, you will receive 50% of the GOV tokens, while the other 50% will be allocated back to the community. The penalty for rage quitting will decrease as your lock-up time decreases. The rewards for rage quitters can be distributed in several different ways.

Diamond Hands: The collected GOV is maximally re-locked and distributed proportionally based on the vxGOV controlled by each account. The benefit of this approach is to incentivize "diamond hands" and long-term commitment to the protocol, as these rewards will skew toward the stakeholders who invest the most in the protocol.

Treasury: This scheme requires some proactive financial management. For example, these funds could be used to purchase shares of other Convex or Redacted Cartel-like assets or establish a low-correlation asset pool.

Protocol-Owned Liquidity: As an extension of #2, the GOV in the treasury could be periodically deployed into liquidity pools for GOV tokens. This would help establish a strong liquidity foundation for GOV and represent "protocol-owned" liquidity, which will increase the sustainability of GOV in the long run.

We believe that parameters such as penalty ratios and GOV distribution will initially be dynamic, depending on the protocol's priorities. However, we believe that the effects of penalties should always be significant to ensure that governance power belongs to those with the most vested interests in the protocol.

3 Built-in Bribery

We believe that built-in bribery may increase the appeal of staking vxGOV individually rather than completely abandoning custodianship to Convex and similar protocols. We think this is particularly true for smaller investors.

Taking Curve as an example, before platforms like bribe.crv.finance existed, it was difficult for small veCRV holders to monetize their ability to directly release gauge weights.

Without a market, bribery must occur privately through OTC. This is problematic for several reasons:

For DAOs, reaching out to a single veCRV whale makes more sense than contacting 1000 smaller holders. This benefits whales rather than small users—so, not great.

Since these contacts usually do not occur on-chain, there is some counterparty risk. If a DAO preemptively offers a bribe, the veCRV whale may not fulfill their promise to vote for the agreed gauge. Conversely, if the veCRV whale votes before receiving payment, the DAO may not fulfill its promise to pay.

Off-chain bribery occurs behind the scenes, with opaque pricing, leading to inefficient pricing markets. Having an on-chain market can facilitate a healthier market for all participants.

With higher native vxGOV yields, we believe liquid staking derivatives will become unattractive. This encourages individual staking, increases decentralization, and creates more competition for liquid staking derivatives.

Conclusion

Our findings indicate that the veToken economics pioneered by Curve (thanks to Michael Egorov and the team) remains one of the best incentive adjustment mechanisms to date. We hope our analysis and recommendations can inspire projects implementing the veToken model. Our core goal here is to reduce centralization while still maximizing the core attributes of veToken: rewarding the most long-term and focused participants, while not excluding contributors who cannot bear the illiquidity risks associated with traditional veToken economics.