The Dream of the One Ring for Algorithmic Stablecoins: After LUNA, there will be no next UST

In fact, whether something is considered stable or not is not a binary issue. Combining the advantages of stability and traditional stablecoins, like UST, is not necessarily a bad thing.

In fact, whether something is considered stable or not is not a binary issue. Combining the advantages of stability and traditional stablecoins, like UST, is not necessarily a bad thing.Author: 0x137, Rhythm BlockBeats

Before the article begins, let me tell you a story:

In April 2015, top investment bank Goldman Sachs led a nearly $50 million investment in a tech startup. Just three years later, its market value skyrocketed 60 times to $3 billion, with annual profits of about $10 million. Their business was simple: in the ever-changing blockchain industry, they provided a stable asset.

This company is Circle, which now has a market value of $9 billion, and its flagship product USDC has a total issuance of over $50 billion. In an industry where everyone shouts the slogan "de-Bank," this seemingly "outdated" bank has reaped the largest dividends in the industry with the lowest risk.

Stablecoins, the most basic area of the blockchain industry, have seen nearly a hundred projects emerge in just two years, with a total market value soaring to $200 billion. From the early, pure hedging function to now being the absolute foundational asset of all ecosystems, it is like the One Ring in Middle-earth, enticing everyone's desires. It bridges all public chain ecosystems, drives countless protocols and applications, and is an essential infrastructure in the crypto space, undoubtedly the largest track.

Long before this field emerged, institutions had already laid their groundwork here. Behind Circle are not only Goldman Sachs but also internet giants like Baidu and mining behemoths like Bitmain. Tether is backed by Bitfinex, and MakerDAO's DAI is supported by a16z. This is not surprising; creating a stablecoin project requires not only substantial startup capital as backing but also strong market-making capabilities. For this reason, the stablecoin track has always been a feast for institutions, and people seem to be able to only watch as big capital divides this fertile land, until the emergence of algorithmic stablecoins.

Algorithmic stablecoins brought a new narrative: breaking free from the constraints of backing and relying on algorithms to achieve anchoring. This is a change born for the people, allowing everyone to share in the cake of the stablecoin track through a decentralized stabilization mechanism. However, in this revolution of algorithmic stability, countless projects have perished on the road to conquering Middle-earth.

Currently, UST is gaining momentum, becoming the "Lord of the Rings" that has seized the crypto ring. This algorithmic stability leader, waving the banner of decentralization, has reignited hope for the future of algorithmic stability. A few days ago, NEAR completed a $350 million financing at an astonishing speed and immediately revealed its algorithmic stability plan: binding NEAR with USN and launching its own Anchor. Suddenly, everyone believed that UST's success indicated that the path of algorithmic stability is feasible and worth pursuing.

But is the reality really like this?

To clarify this issue, I discussed it from the perspectives of VC, Builder, and Investor with Mable Jiang, a partner at Multicoin, Yang Mindao, the founder of dForce, and 0xSoros, a true Bitcoin expert.

I will tell you below why LUNA is difficult to replicate and why decentralized algorithmic stability may very well be a dead end.

Mission Impossible - Recreating LUNA

Amid accusations of "Ponzi schemes" and "air drops," LUNA created a large stablecoin ranked third in the crypto market with nearly zero collateral. You must admit, this is an incredible business miracle. However, despite its learning value, the most dangerous aspect of a business miracle is that it can lead you to mistakenly believe that you can also create miracles.

The mechanism of algorithmic stability is indeed very tempting, but LUNA is just a lucky one among dozens or hundreds of projects; most algorithmic stability projects are still in dire straits. Now, for public chains to replicate the next miracle following LUNA's path seems to be an impossible task.

Why is algorithmic stability so enticing?

Whether on-chain stablecoins or off-chain fiat currencies, the terms "seigniorage" cannot be avoided in design, issuance, and circulation. Today, it refers to the economic phenomenon where the currency issuer accumulates wealth through currency depreciation after absorbing equivalent wealth, simply put, it is printing money. Since ancient times, this has been the most profitable business because it captures the dividends of the entire social economic activity.

Currently, there are three main types of stablecoins in the crypto world: fiat-backed, crypto asset-backed, and algorithmic stablecoins.

Fiat-backed stablecoins achieve anchoring through 1:1 exchange with fully collateralized fiat currency, generally charging around 0.1% seigniorage during the minting or redemption process. Considering the volatility of crypto assets, stablecoins like DAI that are backed by crypto assets adopt an over-collateralization mechanism, with profits coming from transaction fees and interest paid by holders.

The reason why algorithmic stablecoins like UST are so enticing is that they have the highest seigniorage among the three. By introducing a volatility-linked token, algorithmic stability turns all funds flowing into the system into seigniorage, commonly referred to as "Print money out of thin air." This mechanism greatly reduces startup costs and enhances anchoring speed to some extent, but it also comes with inherent fragility.

Since DeFi Summer, algorithmic stability projects have sprung up like mushrooms, trying to capture the dividends of stablecoins through this mechanism. However, from IRON to BAC to FEI, this battlefield can be described as littered with corpses, with very few algorithmic stability projects surviving, and if we talk about winners, it seems only UST remains.

What Does a Public Chain Need to Become the Next LUNA?

After the news of NEAR launching algorithmic stability broke, we seemed to see a trend: public chains also hope to combine the LUNA-UST model to attract external capital and promote ecosystem development. But when discussing whether there will be a next LUNA, one sentence from 0xSoros left a deep impression on me: "UST's success today is the result of timing, location, and harmony; the next LUNA may still be LUNA, and even if not, it won't be another public chain."

Indeed, LUNA's success is a product of team operation, capital boost, and timing. It is like saying that replicating Apple is not that simple. So, what does NEAR need to become LUNA?

First, it needs accurate positioning and the right timing. The Terra team's initial positioning was always very precise: the financial market. Therefore, we see that whether it was the previous offline retail or now the Anchor on-chain bank, the team has been working hard in the UST application market. LUNA was fortunate to catch the wave of DeFi Summer and the public chain narrative. Before this, the offline retail market for UST had always been difficult to open up, but after packaging itself as an L1 public chain, the application scenarios for UST suddenly opened up.

Second, team operation is crucial. The best card played by the Terra team LFG (LUNA Foundation Guard) is Anchor, which may be the most successful advertising marketing in the history of the crypto field. In a highly volatile market, being able to provide stable, high-return savings services over the long term is very attractive, capturing investors' strongest emotion—fear—when the market is down. Now, anyone looking for stable passive income in the crypto market first thinks of Anchor.

The market value of UST has a direct linear relationship with the TVL of Anchor. The above image is from Coin MarketCap, and the below image is from DeFi Llama.

Additionally, collaborating with the right people at the right time is also crucial. For example, the collaboration between UST and Abracadabra was a key to unlocking the crypto market for UST. In the latter half of last year, Abracadabra launched Degenbox on Ethereum, providing deposit leverage for UST users in the form of Loop, significantly increasing Anchor's 20% APY by several dozen points, making UST much more attractive in competition with stablecoin giants like USDC and DAI. Now, whether on Curve on Ethereum or Trader Joe on Avalanche, UST is among the top TVL players.

Of course, the most critical factor is the powerful capital push behind LFG. The success of UST is backed by strong "money power." When LUNA experienced a death spiral in May last year, without LFG's support, UST would have likely met the same fate as other algorithmic stablecoins. If Anchor hadn't received substantial subsidies, UST wouldn't have the strong Lindy effect it has today.

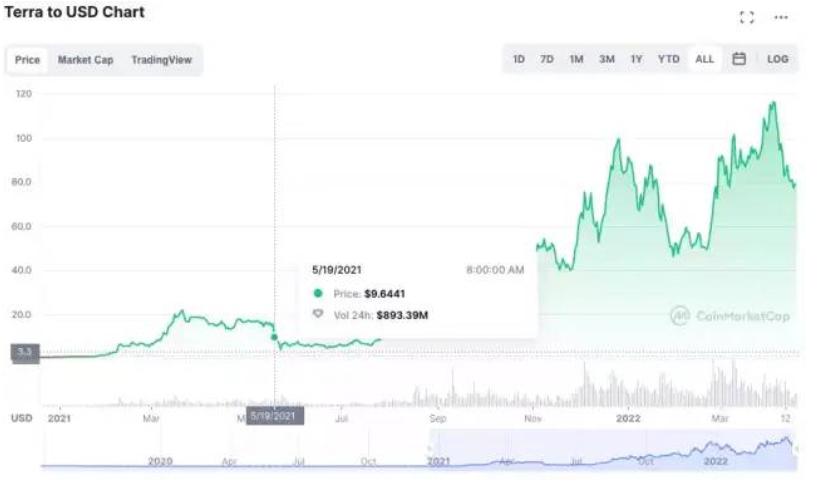

The death spiral of LUNA was triggered on May 19, and LFG later announced reserves of hundreds of millions to support LUNA's price. The image is from Coin MarketCap.

As a witness to the industry, you can actually feel that the current crypto market is no longer suitable for the growth of new algorithmic stability. The stablecoin track has become a red ocean, not only lacking enough time to establish a Lindy effect but also having fewer large projects willing to collaborate with you. In this environment, the Matthew effect between large and small projects is even more pronounced. You can ask yourself a simple question: with the same APY, would you rather take the risk for the new algorithmic stablecoin USN or hold the well-established and consensus-driven UST?

Is It So Easy for Public Chains to Engage in Algorithmic Stability?

Regarding public chains entering the algorithmic stability space, dForce founder Yang Mindao has a viewpoint: "Moving from application to public chain and from public chain to application are two completely different concepts." There is a key question here: the dilemma of general-purpose public chains entering the application space.

First, we need to clarify why public chains want to enter the application space. Undoubtedly, it is to drive ecosystem development. For example, the BNB chain supports Pancake Swap to promote its DeFi ecosystem. However, we find that the DeFi projects in the BNB ecosystem cannot compare with Ethereum DeFi in terms of individual project strength or overall activity level.

Of course, there are factors of timing, but the more critical reason is the degree of decentralization. For a developer, the probability of success in DeFi development on Ethereum is actually higher than on the BNB chain. A simple example is Sushi; after optimizing its product model, Sushi dealt a huge blow to Uni in a very short time. But it is different on the BNB chain; Pancake has direct support from Binance, which puts it on a different starting line and creates a gap in strength with other competitors. When developers know their chances of winning are low, they will no longer attempt new projects. This is why many public chains prefer to set up foundations to fund projects rather than doing projects themselves.

So why did LUNA, as one of the three major public chains, succeed in creating a stablecoin?

In fact, in this proposition, LUNA's success is not about creating a stablecoin with a huge market value but telling a successful public chain story. It is important to note that LUNA is essentially a financial application chain built using Cosmos SDK, born to do finance, so creating its own stablecoin is a natural thing.

Before transitioning to a public chain, LUNA's story primarily promoted the offline retail market, but after the rise of public chain narratives, LUNA saw better application scenarios for UST and gradually packaged itself as a public chain. Here, the public chain narrative serves to assist in promoting UST, aiming to find more application scenarios for UST.

After transitioning to a public chain, UST indeed gained more application scenarios. From Mirror to Anchor, the Terra team created a series of application scenarios for UST and actively collaborated with other ecosystems to promote UST. Therefore, you will find that although the Terra ecosystem has only about twenty applications, it occupies nearly $20 billion in TVL. Ultimately, LUNA does not care about the quality of its ecosystem as long as UST has enough application scenarios.

The Terra ecosystem has a TVL of $19 billion but only 27 applications. In contrast, the Avalanche ecosystem has nearly 200 applications but a TVL of only about $9 billion. The image is from DeFi Llama.

However, for a general-purpose public chain like NEAR, the purpose of launching algorithmic stability is completely opposite to that of LUNA. The use of USN is to promote the development of its public chain ecosystem, attract more talent, and build better applications.

At this point, NEAR will encounter the same problem as the BNB chain: when a public chain engages in applications, it can have a negative impact on the ecosystem. First, to promote USN, NEAR needs to build a driving engine for it, such as the upcoming NEAR version of Anchor. It is not an exaggeration to say that this application will inevitably become the core driver of USN, making it difficult for other applications in the NEAR ecosystem to compete with it.

Once there is an engine, USN will also need a complete set of financial services such as lending and savings, so NEAR will also need to build lending and savings applications for it. This way, NEAR can easily stifle the development of its DeFi ecosystem. Even if USN succeeds, NEAR's original intention to promote ecosystem development can easily fail.

Of course, you could argue that NEAR's decision is to seek a new narrative for itself, which is not inherently wrong. After all, facing the approaching Ethereum Rollup army, the narrative of new L1 public chains being fast and cheap seems to have lost its footing. However, copying LUNA's old path and attracting capital and stabilizing market value through algorithmic stability is, to put it bluntly, a very straightforward pump-and-dump game.

However, this is not the main problem that USN will face. Whether to engage in the algorithmic stability space or not, NEAR's move is based on the assumption that "LUNA's path has been successful." In other words, NEAR believes to some extent that by linking algorithmic stability with the native token and launching an Anchor, its market value and ecosystem will inevitably see significant growth. But is the reality really like this?

The Path Public Chains Should Imitate, LUNA Has Already Abandoned

LUNA's story is reminiscent of the French Revolution led by Napoleon, who, after seizing power under the banner of democracy and republicanism, crowned himself emperor. The UST, which succeeded in expanding its market value while waving the flags of decentralization and democratization, has now returned to the traditional stablecoin backing path. A project making a significant shift often realizes that the old path is no longer viable, and UST's current search for backing is no different.

What Problems Did UST Encounter?

The previous doubts about UST were mostly related to the term "Ponzi." To find UST's problems, we might as well review OHM and other once-thriving DeFi 2.0 projects that were also seen as Ponzi schemes.

The reason why OHM and other DeFi 2.0 projects ultimately became true Ponzi schemes boils down to two aspects: liquidity and backing.

In fact, OHM also aimed to create a decentralized stable savings coin, but unlike various stablecoins anchored to fiat, OHM did not seek to anchor to other assets but aimed to achieve price stability through building a massive savings pool. However, we have seen that the crypto market has never bought into OHM's narrative. No matter how the team tried, they could not find a widely applicable scenario for OHM. Without liquidity, OHM became a speculative game for holders, who would unlock and leave once they made enough profit.

On the other hand, OHM's method of building savings is also very different from algorithmic stability. OHM does not have a redemption mechanism; once users mint OHM through Bond, they cannot redeem their assets with OHM. In other words, the savings absorbed by the protocol are not used to directly back OHM; the project merely promises to conduct buybacks through "protocol backing" when OHM's price drops, providing a safety net for holders. But we all know that this so-called "protocol backing" has never occurred.

Currently, UST faces similar problems. Behind UST's massive market value lies a concerning Anchor TVL. Although UST has widespread applications in ecosystems like Ethereum and Avalanche, the liquidity provided by these ecosystems is far from sufficient. Most people hold UST solely for the 20% stable APY.

Out of UST's total market value of $17 billion, over $14 billion is locked in Anchor, generating a 20% APY annually. It is important to note that the income generated solely from PoS staking and UST lending cannot fill this huge gap, especially since most of the borrowed UST eventually flows back into Anchor for looping.

Currently, Anchor is losing over $4 million daily. Earlier this year, LFG announced another $500 million injection into Anchor, but less than two months later, it burned through $140 million. Rhythm previously conducted a detailed calculation in "Is Anchor a Ponzi Scheme with Stablecoin Interest Rates as High as 20%?" According to the current loss rate, Anchor can only support itself for at most three more months.

Even with LFG's continuous injections, Anchor's savings are still depleting. The image is from Dune Analytics.

In short, the only backing for UST now is LFG and the "money" power behind it, providing infinite bullets to maintain UST's liquidity. But if LFG stops injecting money into Anchor, the $14 billion UST will have nowhere to go. If this situation occurs, the consequences would be beyond imagination.

Faced with this terrifying dilemma of sustainability, LFG must start seeking solutions. The issues to be resolved are still the two mentioned earlier: backing and liquidity.

Kidnapping BTC, Sharing Life and Death with the Crypto Market

Since LFG needs to find backing for UST, what assets are the most suitable?

First, fiat currencies are definitely excluded because holding them would create counterparty risk, leaving UST with no decentralization at all. Therefore, the backing asset must be chosen from the crypto market, making BTC a very natural choice. In February of this year, LFG spent $1 billion to start continuously purchasing BTC, even directly driving up BTC's price.

As the asset with the strongest Lindy effect in the crypto field, BTC is almost regarded as a fixed income by people. LFG's choice to purchase at this time is also a bet on BTC's future, even though they have only bought over $1 billion worth.

LFG's current purchases show that BTC accounts for 70%, USDC for 16%, and there are small amounts of USDT and LUNA. The image is from LFG's official website.

However, simply spending money is not enough. To ensure that the value of savings keeps pace with UST's market value growth, a new backing mechanism must be established. In the future, when users mint UST using LUNA, part of the LUNA will no longer be destroyed but used to purchase BTC, allowing UST's backing to grow alongside its market value.

To ensure that its BTC savings do not deplete quickly, LFG has also employed a little trick, forcing users to buy BTC elsewhere. When users want to redeem 1 UST for $1 worth of BTC, they must pay a 1% fee. This way, unless UST becomes unpegged, BTC savings will only increase.

Many people see LFG's purchase of BTC as akin to exposing its own vulnerabilities, as buying backing as an algorithmic stablecoin seems contradictory. However, Do Kwon has woven a compelling narrative for UST: BTC, as the asset with the highest consensus in the crypto field, can increase other ecosystems' users' trust in UST, further expanding its liquidity and application scenarios. Although the new backing mechanism somewhat reduces the driving force for LUNA, it allows UST's cake to grow larger, which is beneficial for LUNA in the long run.

From this perspective, LFG has indeed made a good move, finding a win-win or even multi-win path for UST. Under the new backing mechanism, BTC's success means UST's success, and UST's failure means BTC's failure. In the future, the growth of UST's market value can not only drive LUNA but also boost BTC. Isn't this a win-win situation?

With such a narrative, LFG has no need to stop at BTC, as this new mechanism can also be applied to other assets. Recently, Terra announced a partnership with Avalanche, allowing AVAX holders to directly mint UST in their ecosystem using AVAX. For this, the founders of both ecosystems even sat down for an AMA. It is worth noting that AVAX does not adopt an inflationary economic model, and its total circulation has a hard cap. If UST's market value continues to grow, AVAX's scarcity will increase. For UST, it can enjoy the increasingly active ecosystem dividends of Avalanche and find more application scenarios.

It is no exaggeration to say that UST does not want to fight alone in the future; it aims to coexist with the entire crypto market.

Eliminating 3Crv, Attempting to Establish Nuclear Deterrence

With a solution for backing, LFG also needs to address UST's liquidity issues. The stablecoin track is a battle for market value, and the core of this battle is liquidity.

Before Curve emerged, the survival environment for small stablecoin projects was extremely harsh, as almost no major protocols were willing to take risks to provide liquidity for them. As a result, many new algorithmic stability projects encountered varying degrees of depegging before they could even initiate the flywheel effect. Curve is undoubtedly the hero that has enabled the stablecoin track to thrive. Most algorithmic stability projects that have survived to this day owe their existence to Curve, as any new project that gets on Curve can somewhat solve its liquidity issues.

There is a very key liquidity pool on Curve called 3Crv, which consists of the three major stablecoins: USDT, USDC, and DAI, and is one of the largest stablecoin pools in the current crypto market, with a TVL exceeding $3.5 billion. The reason Curve is hailed as the hero of the stablecoin track is that it allows other stablecoins to establish their own sub-pools based on the 3Crv pool. Regardless of whether you are a new project, as long as you establish a sub-pool here, you can immediately enjoy the best liquidity in the market. Therefore, when you search for stablecoin pools on Curve, you will mostly see the format XXX-3Crv, and UST is no exception.

Stablecoin pools on Curve almost all utilize the 3Crv pool. The image is from Curve WebApp.

The UST-3Crv pool is the second-largest stablecoin pool on Curve, with a TVL exceeding $1.3 billion, of which UST accounts for $570 million. To be honest, this level of liquidity is already quite good compared to other algorithmic stability projects, but for UST, a TVL of less than $600 million is still insufficient to alleviate its concerns, as no matter how high the TVL is, it is merely a player benefiting from others. While the three giants in 3Crv have taken on considerable risks, they have also gained substantial benefits by providing liquidity for other projects.

Comparison of the TVL of the UST-3Crv pool and the 3Crv pool on Ethereum's mainnet Curve. The image is from Dune Analytics.

When discussing this issue, Multicoin partner Mable Jiang told me: "Just like oil supports the dollar, having BTC as UST's backing is ultimately limited; the rest needs to be resolved through force." Mable pointed out an important aspect here: force. The reason the dollar is the international reserve currency today is that it possesses strong military and financial power, enabling it to compel most international commodity transactions to be settled in dollars. For USDT, USDC, and DAI, the 3Crv pool is their nuclear weapon in the stablecoin market. Any stablecoin that wants to grow and stabilize must connect to the 3Crv pool, making these three giants the reserve currency in the crypto field, controlling the largest liquidity in the market.

If UST wants to solve its liquidity problem, why not become the one providing the food? Recently, UST collaborated with Frax and Redacted Cartel to establish the 4Crv pool, aiming to completely replace 3Crv. Regarding the Curve War, Rhythm has detailed it in "The Curve War Upgrade CVX Battle, the Exciting Power Struggle Continues." Here, you only need to know that although the task is daunting, the combined CVX held by these three exceeds 40% of the total, making it possible to overthrow 3Crv.

The 4Crv pool consists of UST, FXS, USDT, and USDC. Upon closer inspection, you will notice that DAI is absent, and LFG's intention is clear: to eliminate DAI. After UST began accepting backing, DAI, which is backed by crypto assets, has become a direct competitor to UST. By squeezing out DAI's market value, UST can more easily obtain a position as a reserve currency in the crypto market and alleviate some pressure on Anchor. Of course, it is not easy to take down a stablecoin giant backed by a16z, but for UST to survive, it must do so.

Fairly speaking, after accepting backing and establishing 4Crv, LFG has indeed found a new and correct direction for UST. However, whether these solutions for backing and liquidity will be effective in the future remains uncertain. In summary, the current path for UST is unprecedented; if it is to succeed, it seems only UST can achieve it. Choosing to imitate the old path that LUNA has abandoned at this time is not very appropriate.

Decentralization and Backing: The Curse of Algorithmic Stability

Stablecoins like DAI, which are backed by crypto assets, tell a good story of decentralization: fiat-backed stablecoins always carry counterparty risk, and a single subpoena could be fatal. Thus, the crypto market indeed needs a decentralized stablecoin. However, for algorithmic stability, decentralization is not its most attractive aspect.

The story of algorithmic stability is about democratizing the stablecoin track, allowing ordinary people to directly enjoy the dividends of stablecoins. However, whether it is the fallen revolutionary martyrs like IRON and BAC or the large but unstable emperor like UST, it seems that none have escaped the paradox of decentralization and backing.

Purely decentralized algorithmic stability is destined to be a Greek tragedy.

"Rich families feast while the poor freeze to death" perfectly describes the current stablecoin track. The institutional-backed stablecoin giants enjoy the best resources in the industry and reap the largest dividends, while the algorithmic stability projects from humble beginnings die one after another.

Just this week, Circle, the issuer of USDC, announced a new round of $400 million financing and formed a strategic partnership with BlackRock to further promote USDC's application scenarios in traditional finance. On the 14th, Circle even submitted an application to operate as a bank in the U.S. In fact, whether it was Visa before or now BlackRock, we find that for traditional institutions, accepting digital stablecoins like USDC is not a difficult choice.

First, USDC is 100% backed by the dollar, eliminating the risk of collateral value depreciation. Second, Circle has set up an open-source API interface for USDC to facilitate enterprises and institutions in integrating into its ecosystem. Most importantly, USDC's issuance is approved by the New York Department of Financial Services, so concerns about "a single subpoena" are somewhat alarmist.

In contrast, this is precisely the most fatal problem for decentralized algorithmic stability: it is challenging to gain support from large projects and institutions both within and outside the industry. In the relatively conservative traditional finance sector, no one is willing to accept a completely unbacked "air asset," and in the profit-first crypto market, similarly, no one will take unnecessary risks without economic incentives.

In this situation, to attract users, you must offer higher economic incentives, but if there is not enough strong financial backing, it can easily lead to collapse. Take Anchor, for example; if it weren't for that 20% APY, not many people would be willing to use UST. The money LFG has burned for this "marketing advertisement" could have supported several small DeFi projects.

Additionally, you need to rely on capital and teams to find better collaborations and gain broader application scenarios. Think about it: if an ordinary algorithmic stability project approached Avalanche and said, "Give me AVAX, and I'll give you an air token," would Avalanche really be willing to accept that?

"I believe KYC for stablecoin teams is quite necessary," is Mindao's view on stablecoin teams, and I completely agree. Regardless of whether it is algorithmic stability or not, if we count all the large stablecoins currently, each has a strong team operating behind it. Team authentication is a commitment to product safety; when your algorithmic stability project encounters problems, you cannot abandon users and the project.

Decentralization is a gradual process; therefore, in the current track closely connected to stability and security, we indeed need some centralization, at least for now. Without excellent teams charging ahead and strong capital burning money behind, relying solely on oneself to carve out a bloody path in algorithmic stability will likely become another Greek tragedy.

Does Algorithmic Stability Have a Future?

After purchasing BTC, UST has become a strange product in the stablecoin track—an algorithmic stability using a backing mechanism. Today's UST shares many similarities with the dollar.

Before 1971, the dollar, under the gold standard, resembled DAI or USDC, where each bill was backed by gold. At that time, the concept of "money" referred to gold. However, this system has a problem: it can easily run out of money. When gold reserves decrease, the Federal Reserve's ability to print money becomes more limited, or it becomes more prone to default. The dollar faced this situation after the Vietnam War, prompting Nixon to immediately announce the decoupling of the dollar from gold. Since then, the dollar has entered the Petro-dollar era, and the concept of "money" has changed.

After the dollar's decoupling, the Federal Reserve became a true money-printing machine, and the U.S. no longer had to worry about running out of money. However, to prevent inflation, the dollar needed to find sufficient liquidity and application markets. Therefore, the backing of the dollar has transformed into strong military and financial power, which is what Mable Jiang referred to as "force."

Thus, the notion that algorithmic stability does not require backing is unrealistic. As Yang Mindao said, "The path from over-collateralization to full collateralization, from zero collateral to partial collateralization is feasible; all roads lead to Rome, but the key is to find your liquidity backing." Without liquidity as backing, no algorithmic stability can succeed.

After "kidnapping" BTC and Curve, UST seems to have found its nuclear weapon. However, it is important to note that this operation is not something just anyone can accomplish. So, for ordinary algorithmic stability projects, is there really no other way out?

In fact, whether something is algorithmic stability or not is not a binary issue. Combining the advantages of algorithmic stability and traditional stablecoins, like UST, is not necessarily a bad thing. The efficient anchoring speed of algorithmic stability and its dual-token mechanism indeed have their merits for the current crypto market, allowing the protocol's token to have better value capture capabilities, with the key being to find a clear market positioning for it.

For example, as Rhythm mentioned in "THORchain's Non-liquidation Lending May Change DeFi," THOR.USD has a very clear positioning: it is linked to RUNE and collateralized by LP tokens on THORchain, specifically designed for providing non-liquidation loans. Similarly, stablecoins like MIM, which use interest-bearing assets as collateral, are born to improve capital utilization. If NEAR simply launches an algorithmic stability project with unclear positioning to "drive ecosystem development," it may not be advisable.

Ultimately, regardless of whether it is algorithmic stability, we must recognize who is backing the stablecoin in our hands.