Messari: In-depth Analysis of Uniswap's Market Performance and Progress in the First Quarter

Uniswap's main focus in the first quarter of 2022 included growth on Polygon, exploring multi-chain layouts, and the overall decline in trading volume in the cryptocurrency market.

Uniswap's main focus in the first quarter of 2022 included growth on Polygon, exploring multi-chain layouts, and the overall decline in trading volume in the cryptocurrency market.Original Title: State of Uniswap Q1 2022

Original Author: Jerry Sun, Messari Researcher

Compiled by: iambabywhale.eth

Key Points:

- Due to a decrease in market interest in cryptocurrencies and NFTs starting in Q4 2021, total trading volume and corresponding liquidity provider fees declined in Q1 2022.

- Polygon, as the latest supported blockchain for Uniswap V3, has become the largest market for trading volume outside of Ethereum; additional liquidity mining incentives in the next quarter should continue to help drive sustained growth.

- The community is exploring further expansion to Celo and Gnosis.

- The Uniswap Grants program issued its largest wave of grants in history during its 6th round, including Grants proposals that began at the end of 2021.

Macroeconomic Perspective

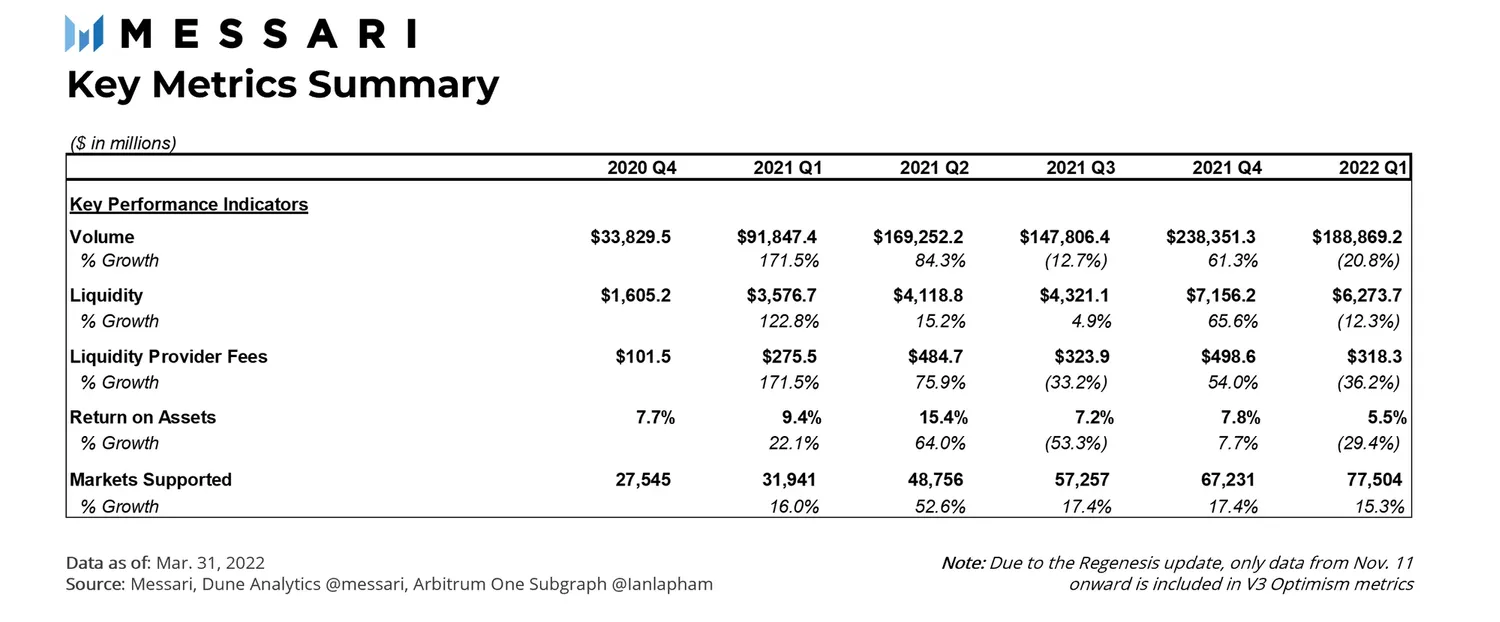

Overall, Uniswap's trading volume in Q1 2022 decreased by 53.5% compared to the previous quarter. This corresponds with the global crypto market reaching a peak market cap of $3 trillion in Q4 2021, which then fell back to $2 trillion. When token prices rise, trading volume typically increases with the growing interest of retail traders; conversely, when token prices fall, retail investors lose interest. Unlike the NFT resurgence and historical highs of Bitcoin and Ethereum prices in Q4 2021, trading activity in Q1 2022 was much calmer.

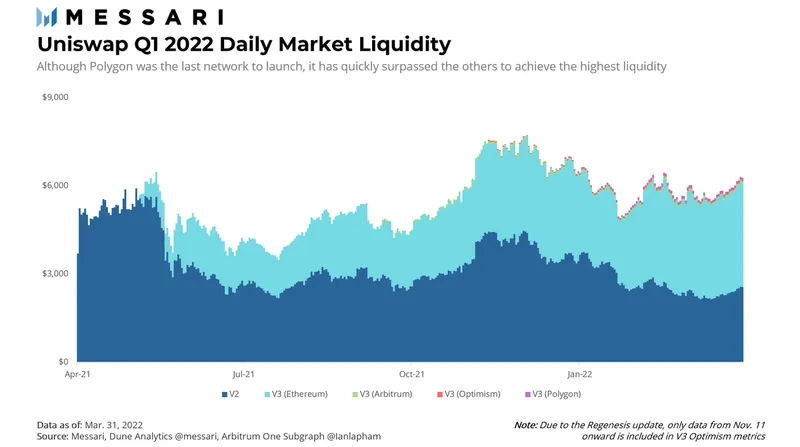

Overall market liquidity decreased in Q1 2022, but the decline was less severe than that of trading volume. Uniswap V2 was the only network to experience a liquidity decline this quarter, dropping by 25.7%, while all other networks saw nominal growth. The decline in V2 liquidity indeed aligns with the decrease in retail trading volume, as V2 includes more long-tail token pairs. Meanwhile, market liquidity grew significantly in Uniswap's so-called scaling solutions, particularly Polygon. Compared to the end of Q4 when it was just launched, liquidity on Polygon increased by nearly 81.7%, while liquidity on Arbitrum and Optimism grew by 72.9% and 34.7%, respectively.

Given the lack of liquidity mining incentives for users in Q1, Polygon's liquidity growth is particularly impressive. For context, when the initial governance proposal was made, the Polygon team reserved up to $15 million for liquidity mining, with an additional $5 million set aside to support the ecosystem. As of the first week of April, these incentives have now been implemented. Only time will tell how much of a boost it will provide to Polygon's existing success.

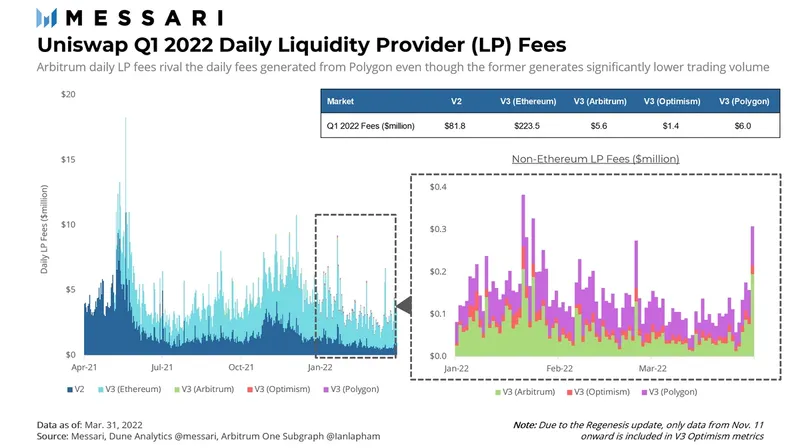

After a 54.0% increase in Q4 2021, daily LP fees in Q1 2022 decreased by 36.2%, resulting in end-of-quarter figures similar to those at the end of Q3 2021. The anomaly in Q4 2021 figures was related to the popularity of NFTs in the mainstream and the new highs of Bitcoin and Ether. Among non-Ethereum chains, Arbitrum and Polygon brought significant gains, while Optimism lagged behind. The data indicates that there are more blue-chip token pairs trading on Polygon (thus lower fees), while popular trading pairs on Arbitrum have higher fees.

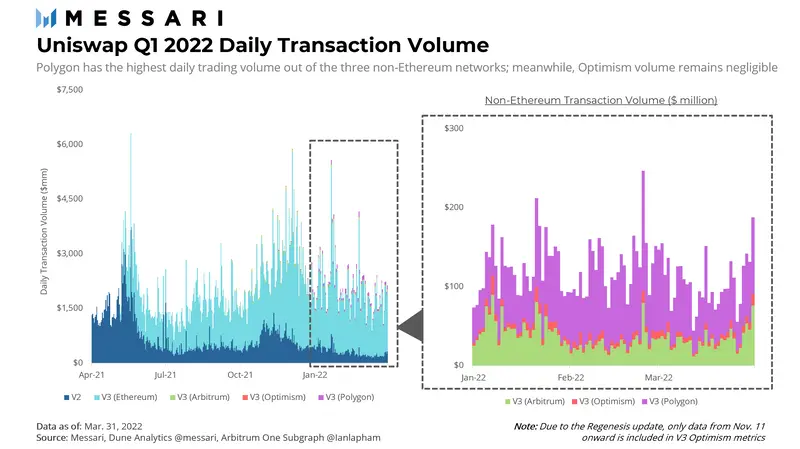

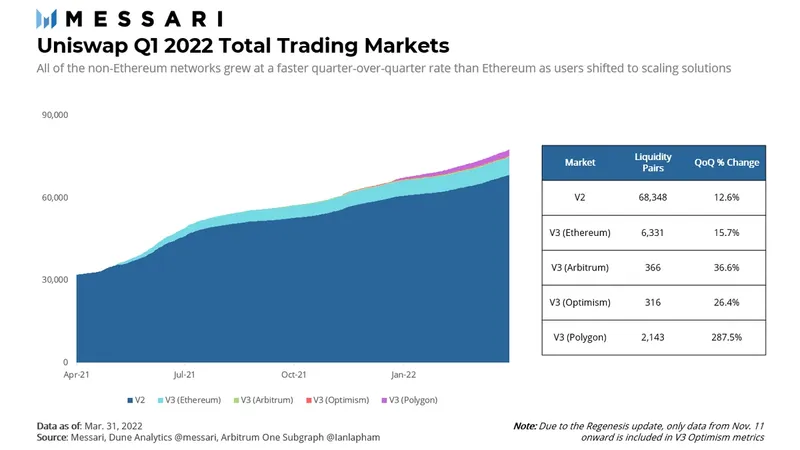

In terms of total trading market numbers from Uniswap V2 on Ethereum to all trading pairs on every non-Ethereum network, the total continued to climb compared to the previous quarter. Uniswap V2 continues to dominate the entire market. Uniswap V3 on Ethereum and Polygon accounts for 11% of active markets, while Optimism and Arbitrum remain negligible. Similar to market liquidity, Polygon experienced the fastest growth in Q1, with an increase of nearly 300% compared to the previous quarter. Given all the data, it is clear that Uniswap has found a "new home" on Polygon.

Microeconomic Perspective

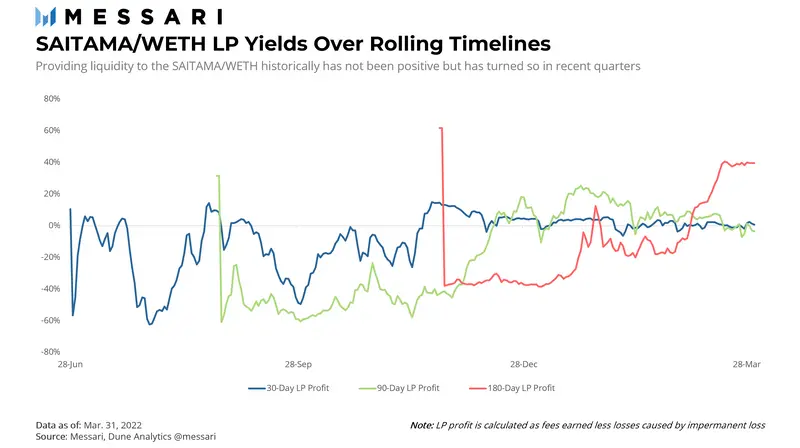

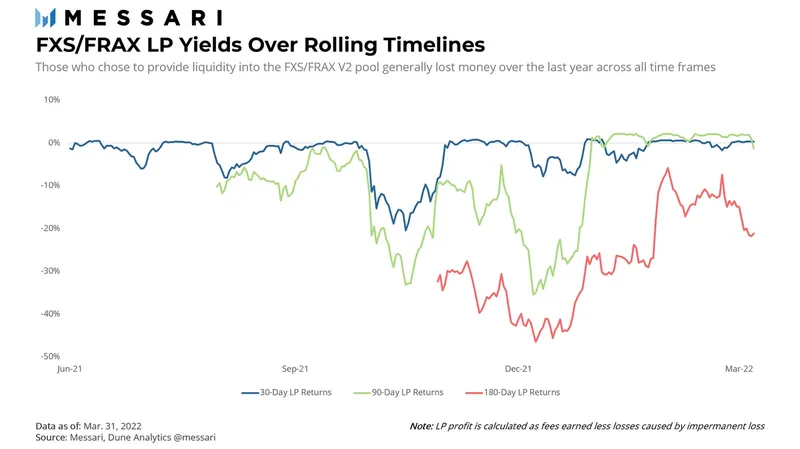

The four most active markets in Q1 2022 were USDC/WETH, USDT/WETH, SAITAMA/WETH, and FXS/FRAX. Among these, the relationship between liquidity provider returns and impermanent loss is considered particularly important by the editor.

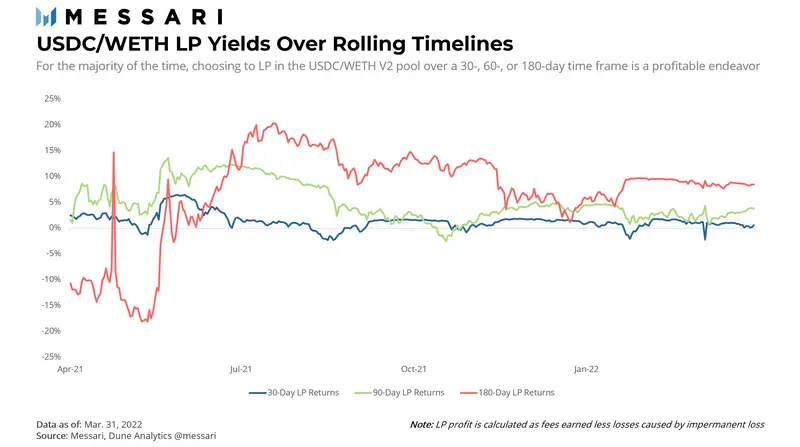

Messari measures LP returns by distinguishing three scenarios, assuming users provide liquidity for 30 days, 90 days, and 180 days, with the return on the day of liquidity withdrawal minus the impermanent loss compared to the token value before providing liquidity, which is the LP's yield.

Taking the USDC/WETH market as an example, over the past 365 days, users providing liquidity for 180 days had a negative yield on 52 days when withdrawing liquidity, while this number was 45 for users providing liquidity for 30 days, and only 12 for those providing liquidity for 90 days. In Q1 2022, only users providing liquidity for 30 days experienced losses when withdrawing liquidity between January 22 and 27 and on March 5; all other LP positions would have been profitable.

However, the outlook for the SAITAMA/WETH and FXS/FRAX trading pairs is not optimistic. The data shows that although these two trading pairs rank high in trading volume, their liquidity providers have been in a loss position for most of the time, with FXS/FRAX only recently achieving a partial break-even for LP positions in Q1, while long-term liquidity providers have remained in a loss position.

As for Uniswap V3, the most active trading pairs were USDC/WETH, USDC/USDT, and WBTC/WETH, which together contributed 61% of V3 market trading volume, reflecting the trends among Ethereum as the cornerstone of smart contract networks, the stablecoin market, and the two largest cryptocurrencies by market capitalization.

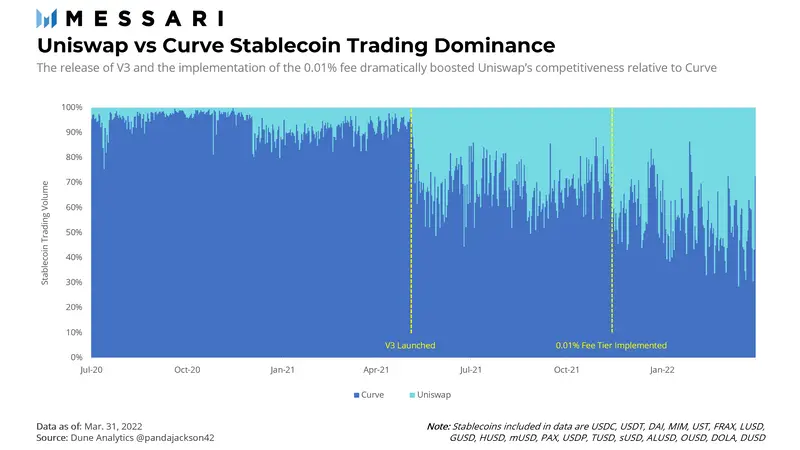

For the USDC/WETH trading pair, Uniswap V3's yield was 12%, three times that of the same trading pair in V2. For the USDC/USDT trading pair, after implementing a 0.01% trading fee, the trading volume saw a significant increase. In Q1 2022, the trading volume for the USDC/USDT trading pair grew by 60% quarter-over-quarter and by 114.1% compared to Q3 2021, more than doubling in nine months, with 87.3% of the trading volume coming from the 0.01% fee liquidity pool. Meanwhile, liquidity only grew by 11.2%.

Before the trading fee dropped to 0.01%, the trading volume of the USDC/USDT trading pair on Uniswap V2 and V3 accounted for 30% to 33% of the combined trading volume of Uniswap and Curve for that trading pair. After the trading fee dropped to 0.01%, the median of that ratio reached 48.3%, nearly on par with Curve. Messari indicates that considering capital efficiency, Uniswap now appears to be more competitive than Curve.

For the WBTC/WETH trading pair, trading volume in the 0.05% fee liquidity pool decreased by 28.9%, but liquidity grew by 57.3%. The trading volume in the 0.3% fee liquidity pool remained nearly flat, but liquidity only grew by 13.7%. This suggests that due to the cooling of the market, investors may choose LP positions in Bitcoin and Ethereum that can generate sustained returns and reassess market conditions when better opportunities arise.

Uniswap Grant Program

In Q1 2022, Uniswap launched the sixth and seventh rounds of the Grant program, with the sixth round providing funding of $2.4 million, more than 2.5 times the previous high of $946,000. Notable projects include the off-chain governance project Other Internet ($1 million), the Uniswap community analysis program Unigrants ($250,000), the esports team Team Secret (attracting gaming audiences, $112,500), and the Basel Art Fair (setting up a cryptocurrency booth, $68,500).

Governance Updates

In the governance proposals of Q1 2022, the proposals to provide additional grants to Voltz for using Uniswap V3 and to deploy Uniswap on Celo and Gnosis were approved, while the proposals to deploy Uniswap V3 on Harmony and to allocate protocol revenue to UNI token holders were rejected by the community.

Conclusion

Uniswap's main focus in Q1 2022 included growth on Polygon, exploring multi-chain layouts, and the overall decline in trading volume in the crypto market. The question is, if trading activity decreases, will it be detrimental to Uniswap?

The answer is both yes and no; exchanges want to see healthy trading volumes, but the reality is that Uniswap can handle any adjustments in the crypto market well. The fact that users can enter LP positions and earn returns indicates that they will continue to participate in the protocol, and tracking how the protocol responds to the changing macro investment environment will be a top priority for the remainder of the year.