Detailed Explanation of Mars Protocol: Decentralized Lending Protocol on Terra

Mars aims to provide lending avenues for any Terra-based digital assets and create robust mechanisms to appropriately incentivize optimal utilization.

Mars aims to provide lending avenues for any Terra-based digital assets and create robust mechanisms to appropriately incentivize optimal utilization.Original Author: David Shuttleworth, Consensys

Original Title: 《Mars Protocol: Decentralized Lending and Borrowing on Terra》

Compiled by: Ze Yi, Chain Catcher

The core function of Mars Protocol is to operate like a traditional bank, attracting deposits, providing loans, and managing liquidity shortages and bankruptcy risks, all through fully decentralized on-chain capabilities. One of its main features is that it allows completely permissionless lending and borrowing, as well as pre-approved, permissioned lending to whitelisted entities, without the need for collateral. The latter is a novel mechanism that expands market demand for deposits and helps create a positive feedback loop for ecosystem participants.

Ultimately, Mars aims to provide lending pathways for any Terra-based digital asset and create robust mechanisms to appropriately incentivize optimal utilization.

Overview

Traditional credit infrastructure suffers from inefficiencies, misaligned incentives, and rigid imbalances of interests. For example, loan initiation fees can be very expensive for borrowers, fund disbursement can take weeks, and generally, a large amount of collateral or credit is required to obtain a loan, which can create high barriers to entry. Additionally, traditional banks typically offer depositors a "high-interest" savings account with 0.5%, then quickly convert users' deposits into external loans, yielding returns several orders of magnitude higher than what is given to users. In this scenario, banks capture most of the profits from loans.

Decentralized projects have been developing ways to correct this imbalance, with Anchor being one of the most notable, a decentralized lending protocol on Terra that offers users up to 19% annual interest rates. However, a key distinction here is that Anchor operates as a "savings-as-a-service" protocol with predictable rates, while Mars functions as a credit protocol with dynamic rates. Furthermore, Anchor relies on the yields from proof-of-stake assets to generate fixed income, while Mars can use any Terra asset as collateral, centering yields around the actual utilization of the protocol.

Ultimately, one issue in the space is that they often require collateral for users to obtain credit lines. Therefore, borrowers in such protocols are also lenders; there are no direct borrowers since collateral is a prerequisite.

Mars is a fully decentralized on-chain credit infrastructure that supports permissionless and permissioned lending, as well as unsecured lending. Interest rates are algorithmically priced based on the utilization of reserves. This means that as the supply and demand for Mars' deposit reserves change over time, the prevailing loan interest rates will automatically adjust. Over time, this functionality will be handed over to Mars governors, allowing token holders to fine-tune the rates. The goal is to democratize the protocol and enable the community to determine the best path forward, unlocking potentially greater responsiveness and capital efficiency.

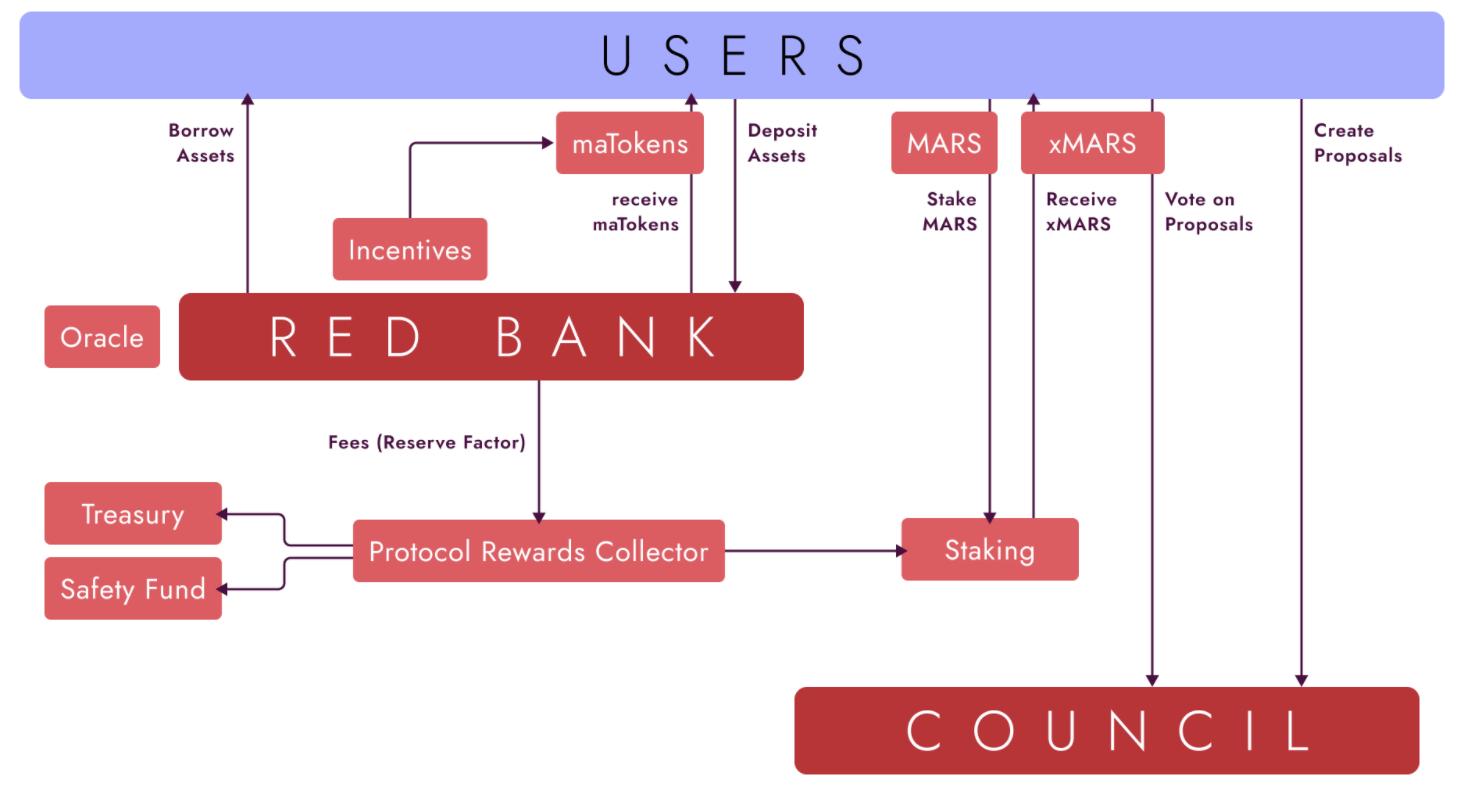

Overall, there are four key agents in the Mars ecosystem: lenders, collateral borrowers, unsecured borrowers, and governors. Generally, users can deposit their digital assets (especially CW20-based) to earn dynamic interest by lending or borrowing against their deposited collateral. Additionally, whitelisted projects can borrow from Mars in the form of unsecured loans. Mars governors ultimately approve which projects can participate and establish the criteria for potential projects to be whitelisted.

Digging deeper, Mars Red Bank is a feature within the protocol that supports non-custodial, permissionless lending. Users deposit funds into the protocol, which are injected into Mars' liquidity pool. In return, users receive $maAssets, representing their share in the liquidity pool, allowing them to share in the fees.

Moreover, users can choose to borrow from the protocol using their deposits as collateral. As utilization (i.e., total deposits vs. total outstanding loans) changes, the protocol algorithmically adjusts the rates paid to lenders and borrowers. This mechanism helps ensure capital efficiency and reduce bankruptcy risks. Thus, Red Bank loans serve a dual purpose, generating yield while also being collateral for borrowing.

A feature that helps prevent bankruptcy is Mars' liquidation mechanism. While not novel, it establishes a predetermined maintenance margin, allowing loans to be liquidated when the collateral relative to its outstanding debt (i.e., loan-to-value ratio) falls below a certain value.

An additional feature is that anyone can repay a portion of a borrower's debt, and repayments do not necessarily have to come from a specific wallet address. Mars incentivizes this behavior by providing such users with an equivalent amount of borrowed collateral and bonuses. Users can then choose to receive liquidity tokens (transferred from the borrower) or receive the underlying asset (which triggers the destruction of the borrower's liquidity tokens). This incentivizes capital injection during market volatility and allows speculators the opportunity to earn substantial returns when timing is right.

The protocol's Field of Mars feature allows certain whitelisted addresses to borrow funds without collateral, which can be seen as a pre-authorized, permissioned lending service. The innovation here is that it enables dApps to build on top of Red Bank, such as leveraged yield farming and liquidity-as-a-service.

In general, most credit protocols only offer collateralized loans. This limits capital efficiency and targets only a small segment of the user market. As a result, the rates offered to users are ultimately relatively low. By enabling whitelisted unsecured loans, Mars expands the market to non-deposit borrowers, thereby increasing demand and utilization among borrowers.

Ultimately, the yields obtained by lenders are significantly higher than those from strictly collateralized loans. While whitelisted entities can borrow without collateral, Mars mitigates its risk exposure by providing liquidation logic, ensuring that given loans can be repaid under any market conditions. This logical framework is overseen and approved by the governance body.

Allowing dApps access to Mars' liquidity increases its composability and creates more demand for deposits. This creates a positive feedback loop where additional demand for liquidity will continuously exert pressure on utilization, thereby increasing the yields paid to lenders and further incentivizing their willingness to lend out capital.

Token Economics

$MARS is the native token of the protocol, primarily used for fee sharing and governance. In short, users can stake their $MARS tokens to receive $xMARS tokens. The $xMARS tokens then allow holders to earn a portion of the protocol's interest rate income and grant voting and proposal rights. Mars' governance is broad, with decisions including asset listings, risk parameters, fiscal spending, and whitelisting new wallets.

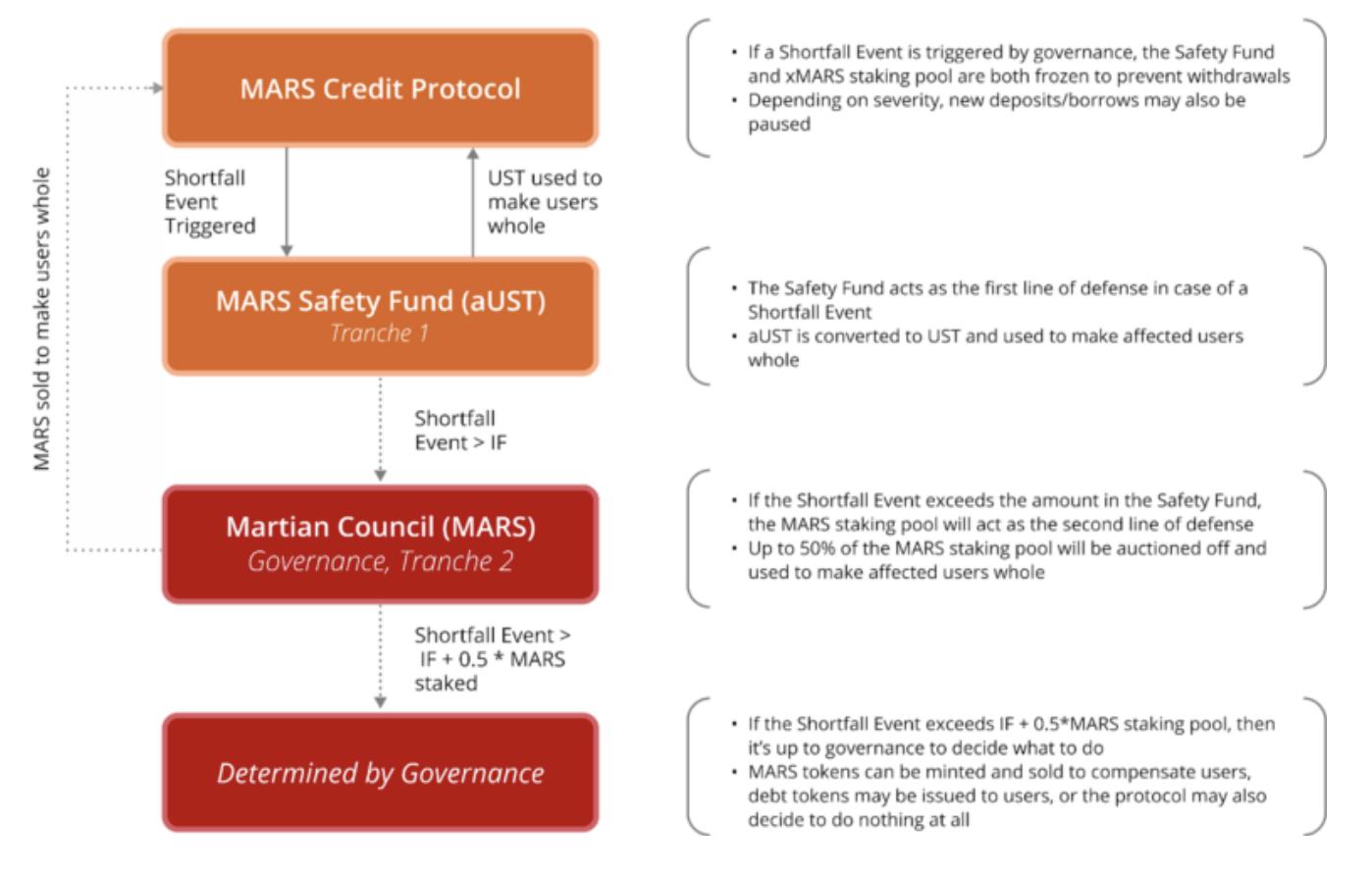

An interesting aspect of Mars governance is the concept of "incentivized voting." In short, voters will be directly affected by the outcomes of their decisions, whether positive or negative. Positive outcomes will earn $MARS token rewards, while negative outcomes may lead to the sale of up to 30% of staked tokens in the event of a shortfall. This mechanism helps guide rational decision-making and reduces malicious or wasteful proposals, as voting in support of such proposals would harm the economic interests of voters.

Another new mechanism of Mars is that it creates an incentive safety fund composed of reserve assets to guard against shortfalls. Generally, a shortfall occurs when a borrower's debt value exceeds the value of their collateral, leading to a deficit for lenders. While common in any form of lending, these events can lead to infrastructure collapse if not properly accounted for. Mars addresses this by incentivizing $xMARS holders to contribute to the reserve fund pool and earn fees for staking tokens within it. Even in the event of a shortfall, these stakers may sell up to 30% of their shares to help Mars maintain solvency. With proper risk management and sufficient inflow of lender funds, this could represent a net positive position for users with a higher risk appetite.

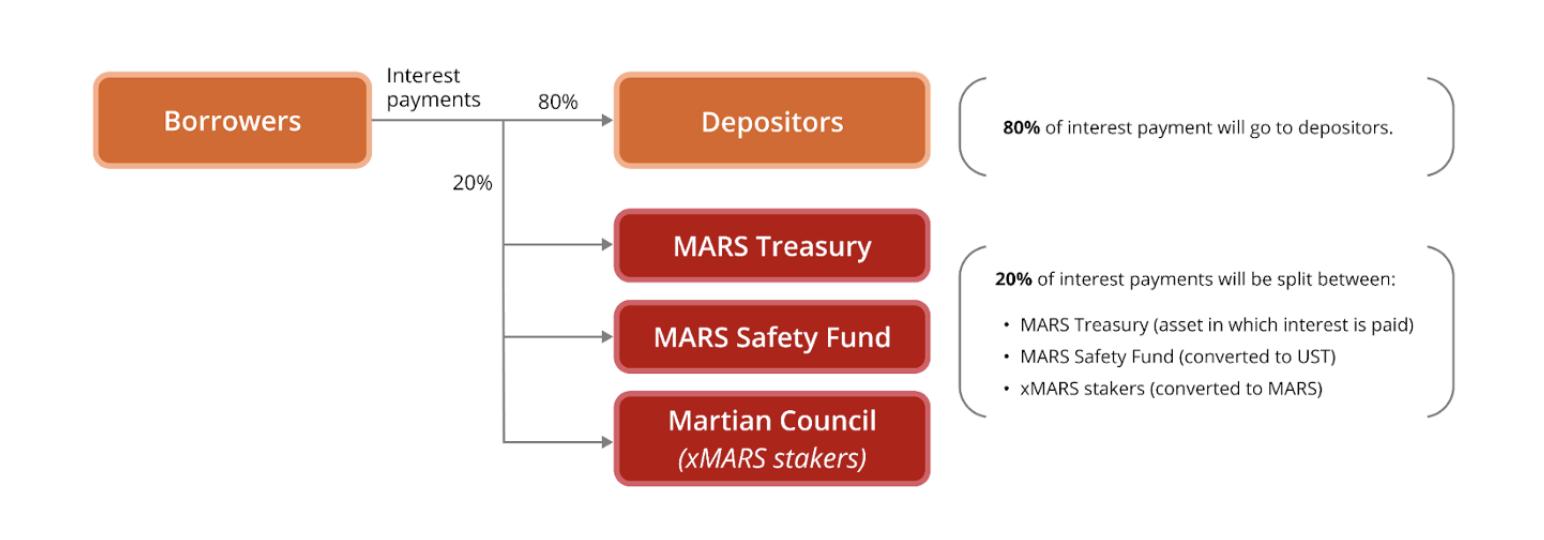

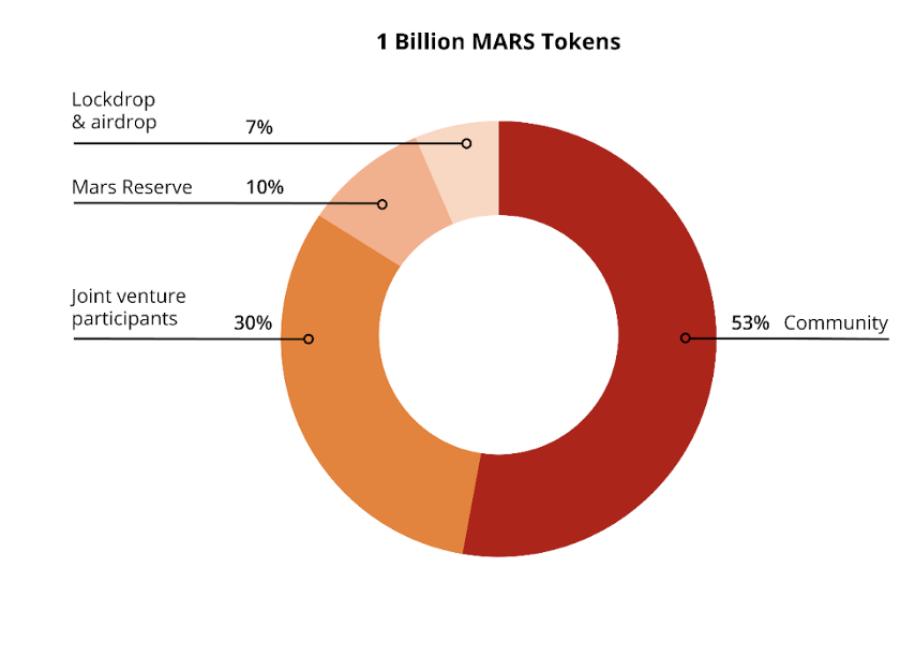

In terms of the value circulation of the tokens, 80% of interest payments are distributed among lenders; 10% is allocated to safety fund participants; and 10% is allocated to $xMARS stakers, with a total token supply of 1 billion, distributed as follows:

Overall

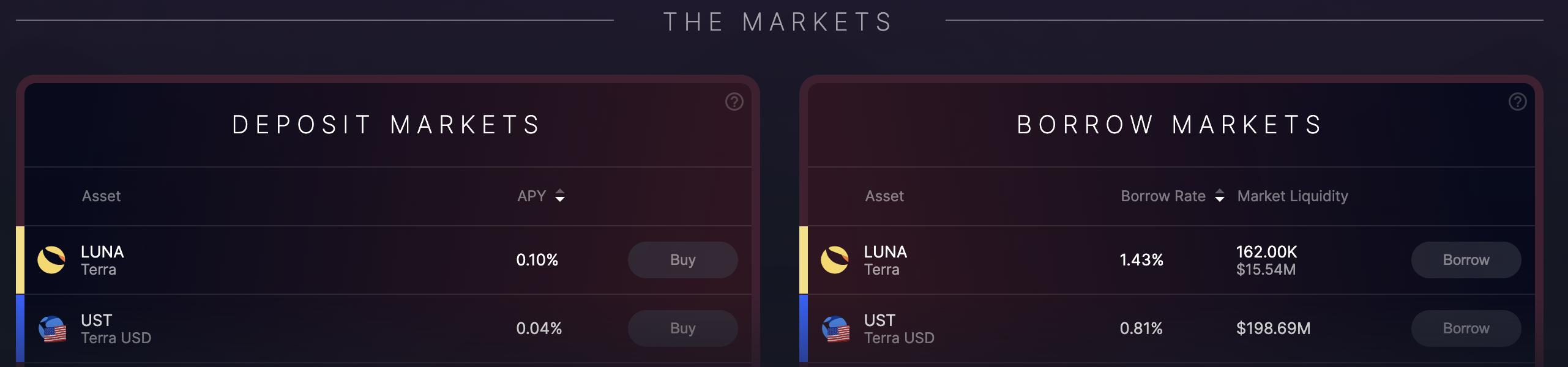

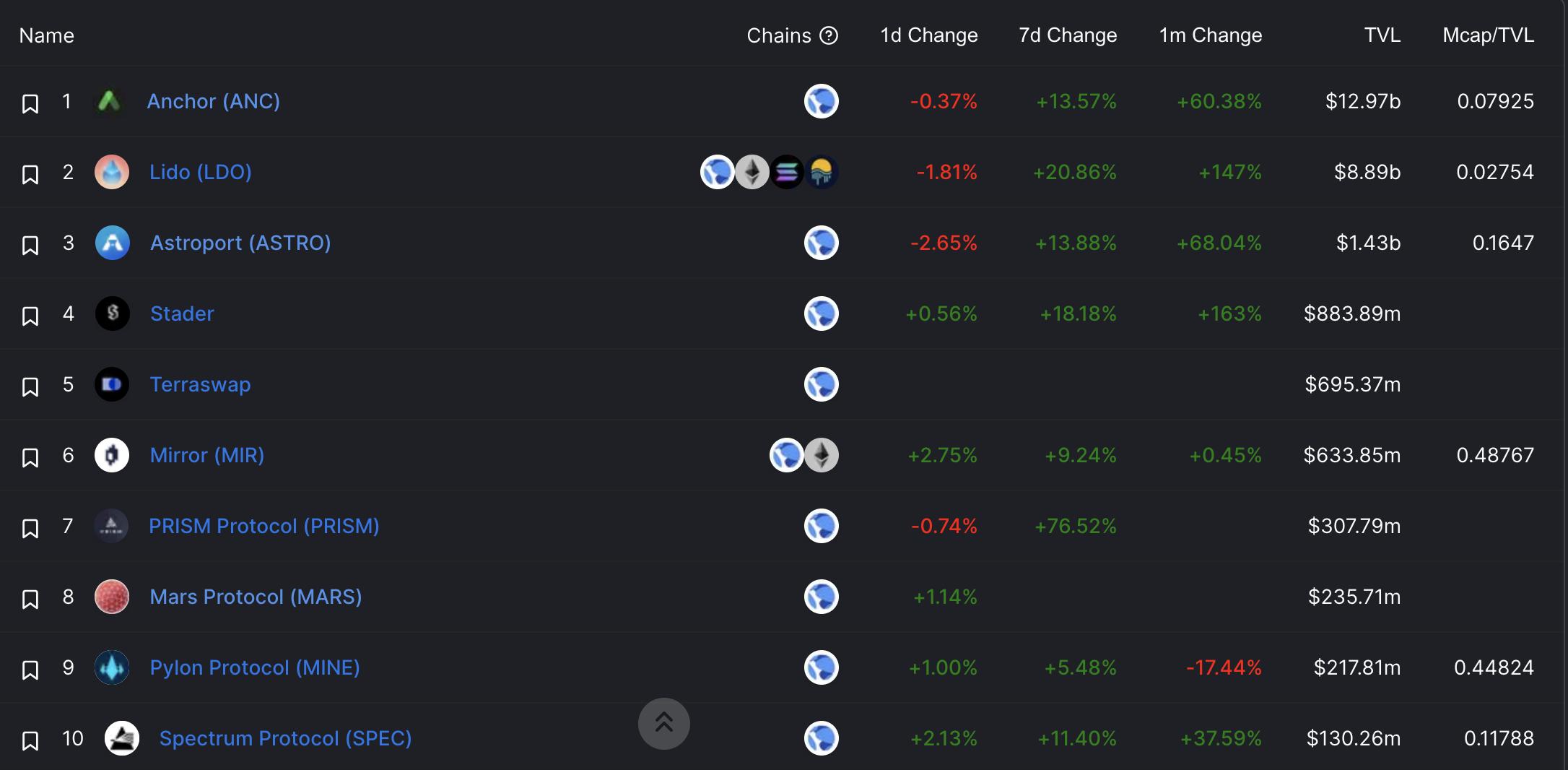

While the protocol is still in its early stages, the TVL is approximately $235 million, placing Mars among the top 10 in terms of TVL within the Terra ecosystem.

Currently, only $14 million in loans remain outstanding, accounting for about 6% of the TVL. Given the surplus in reserves and low utilization, this should make borrowing relatively cheap. It will be interesting to see how utilization changes over time and how interest rates adjust to incentivize borrowing.

One very risky aspect of the protocol is enabling unsecured loans. While Mars' approach is innovative and helps improve lender yields, a potential flaw lies in its liquidation logic. Developers of whitelisted accounts can freely choose their liquidation logic, and while it requires approval from Mars' governance body, it assumes that those voting have the necessary knowledge to review the proposal. If the majority of voters lack such knowledge, the protocol faces significant risks. Besides potentially whitelisting the wrong counterparties, unsecured loans may also be whitelisted without sufficient liquidation logic.

Additionally, there are several aspects of risk-reward voting that may affect and limit governance participation. For example, voters may abstain from voting out of fear of being associated with proposals that could lead to unintended negative outcomes. While this feature does help curb proposals that deliberately harm the protocol's health, it may also deter voting on otherwise beneficial proposals due to concerns over economic penalties.

Risk warning

Risk warning Risk warning

Risk warning