What is the value of the DAO fundraising tool Juicebox?

The core function of Juicebox is a fundraising tool.

The core function of Juicebox is a fundraising tool.Author: echo_z, Chain Teahouse

Since the second half of last year, the development of DAOs has given people hope for decentralized human cooperation. The ConstitutionDAO bidding for the constitution, AssangeDAO rescuing Julian Assange, and UkraineDAO aiding Ukrainian civilians have transformed the will of Web3 users into massive funds amounting to millions and tens of millions of dollars.

Alongside this, tools serving various DAOs have also developed. A complete toolset required by a DAO includes: member management, currently mostly achieved through Discord; governance voting, primarily relying on Snapshot and Aragon; and fund management, such as the programmable treasury Juicebox.

The core function of Juicebox is as a fundraising tool, which sets flexible financing, fund allocation, and exit mechanisms. Juicebox has gained some reputation by serving ConstitutionDAO and AssangeDAO, yet it is often misunderstood due to its unlimited token issuance economic model. What are the strengths and values of this project?

Chain Teahouse attempts to analyze Juicebox's product functions and token economics, exploring the project in depth. Below is a TL;DR for quick understanding; of course, if you want to delve deeper into Juicebox, it is recommended to read the full text.

TL;DR

1) Product Function: Pure functionality, the core being "fundraising tool," allowing project parties to set key parameters such as exchange rates and redemption rates to achieve different financing forms.

2) Token Economics: Unlimited issuance but not devaluation, requiring project parties on the platform to contribute 2.5% of withdrawal fees, using these fees to purchase newly issued tokens at prices far above market value, thereby increasing the overall redeemable amount of tokens and realizing appreciation for early investors.

3) Investment Analysis: Advantages include high certainty in the track, solid fundamentals, and low current valuation; risks lie in the single functionality and lack of operational promotion, which may lead to losses in competition.

1: Product Mechanism

The core function provided by Juicebox is "fundraising." A one-time donation only requires collecting funds, but if it is a fundraising activity that needs to operate continuously (such as financing an operating company), it is not easy, involving at least the following steps: collecting funds from the public, allocating fund flows, distributing shares/tokens to the public, and public exit.

What Juicebox does is provide a unified tool platform for the above steps, allowing users to set parameters at different stages to achieve flexible financing and exit mechanisms. The simplest form for each project is: the project party initiates financing, pre-defining the fund flow in the contract; the public invests ETH and exchanges for corresponding project tokens (currently only supporting investment via ETH); the public burns tokens to redeem a certain amount of ETH.

By setting core parameters, the specific financing forms of the project party can vary greatly. These core parameters include:

Cycle Duration (financing cycle) and Target (financing goal) determining the financing cap.

Distribution (fund allocation) and Reserve Rate (reserve rate) specifying the use of funds.

Discount Rate (discount rate) and Bonding Curve Rate (bonding curve exchange rate) determining the token economic model.

Each parameter's setting can have a huge impact on the nature and consequences of financing, which will be explained and exemplified below.

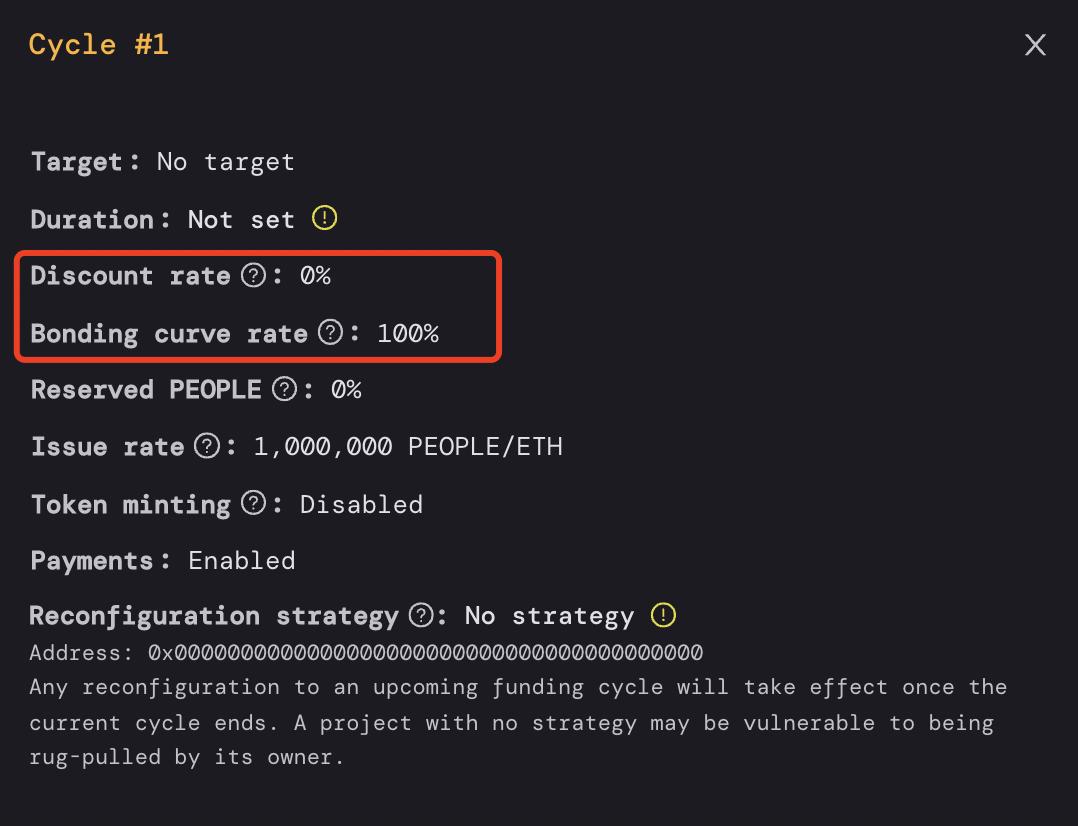

1.1 Cycle Duration & Target ------ Determining Financing Cap

Cycle Duration is the time validity of a financing plan, ensuring that the plan does not change within a certain period. The project party can also choose not to set this parameter and change the financing plan at any time, but this requires the investing public to bear more risk. After one cycle ends, the next Cycle can be initiated, theoretically allowing for an unlimited number of financing rounds.

Target is the financing amount goal within a specific financing cycle; for this amount, the financing project party can pre-program which addresses the funds will be allocated to, which is the maximum amount the project party can utilize; any amount exceeding the financing target is considered Overflow, which users can redeem according to their investment ratio.

Setting Cycle Duration and Target clarifies the limits on both time and amount for financing, suitable for projects with clear funding needs. Additionally, the setting of Overflow provides broad participation for the public, where financing is not first-come, first-served, but rather allocated proportionally.

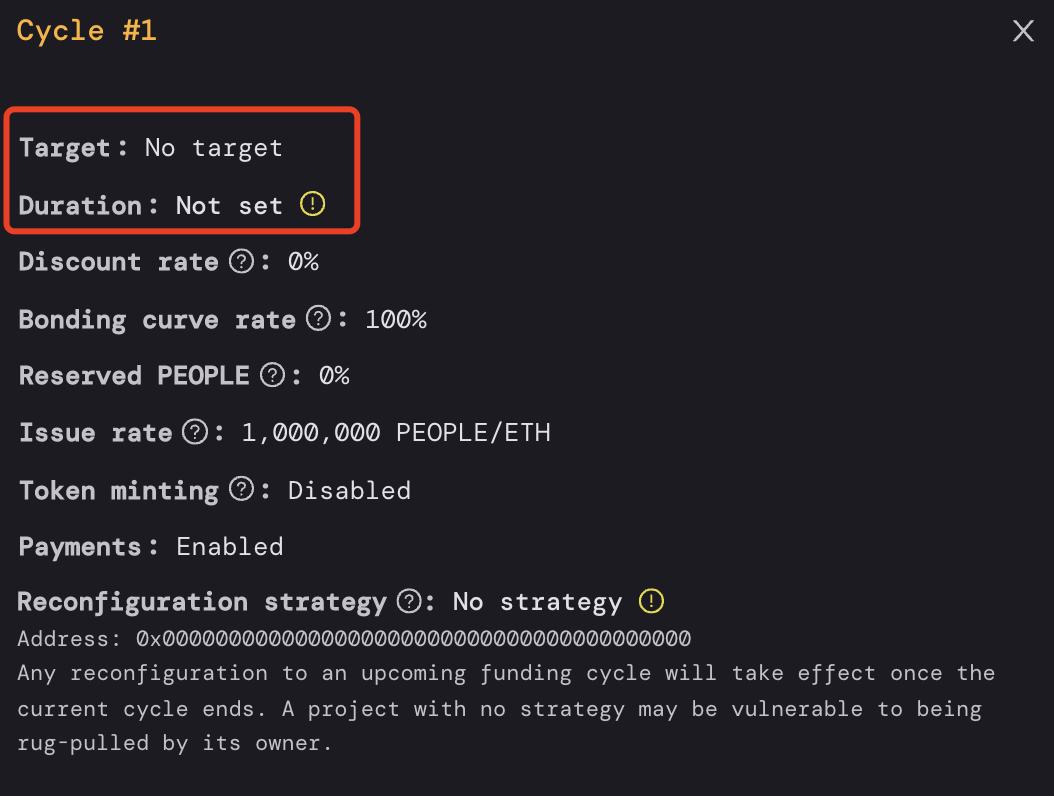

The following image shows the first round of financing for ConstitutionDAO, where neither Cycle Duration nor Target was set. Since the bidding for the constitution copy did not have a clear funding need, the financing also did not set a cap, effectively resulting in unlimited financing, with the public bearing relatively higher financial risks.

Source: https://juicebox.money/#/p/constitutiondao

However, after the bidding failed, the core team of the project converted all funds into Overflow, allowing users to redeem proportionally. In retrospect, the project party's actual decision ultimately ensured the safety of users' funds, but the financing form itself lacked protection for user funds.

Same source

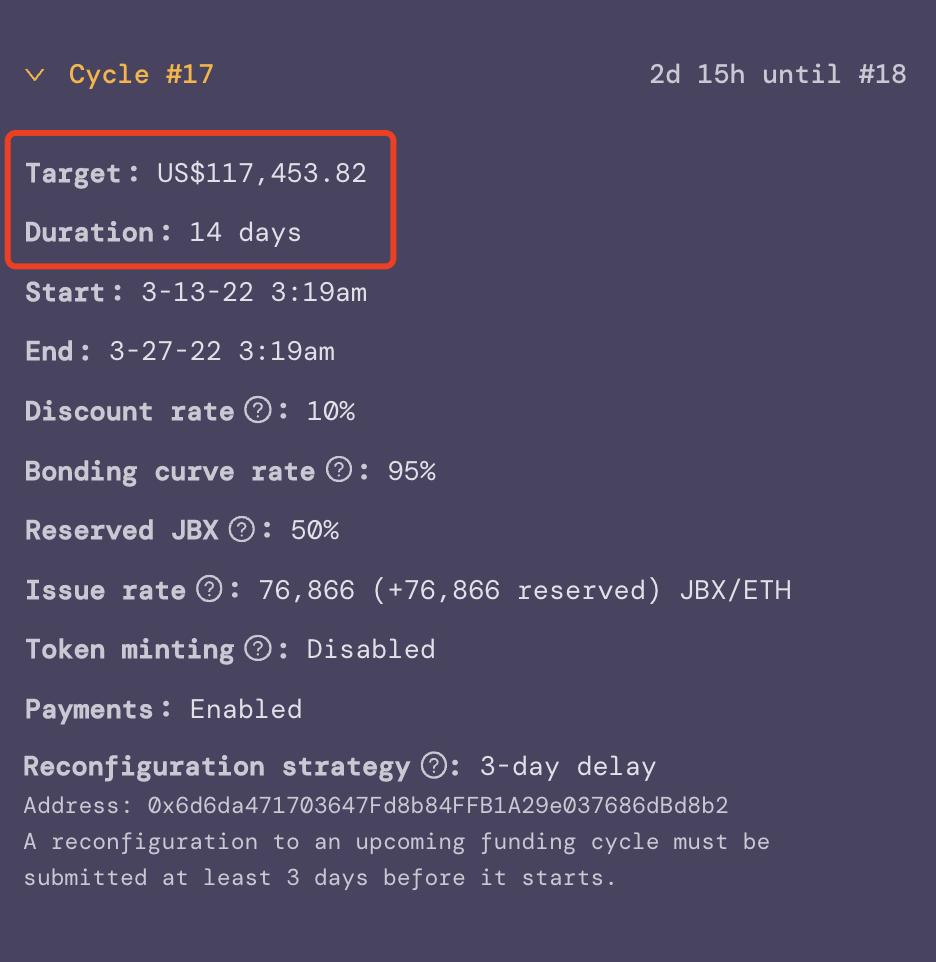

Now let's look at a contrasting example with a financing cap set. The following image is the latest round of financing for JuiceboxDAO, which is also the 17th round. JuiceboxDAO is a DAO established by the Juicebox project party, built on Juicebox, for all project fund management and salary distribution, serving as a typical case of company fundraising operations.

Each round of financing for JuiceboxDAO specifies clear financing goals and cycles, with its financing purposes also very clear, primarily as company expenses, including salaries for the founding team/contributors or payments for third-party tools. The financing amount mainly consists of salaries, subjectively determined by the founders, raising about $80,000 to $200,000 approximately every two weeks, which is not excessive for a crypto team’s expenses.

Source: https://juicebox.money/#/p/juicebox

Comparing ConstitutionDAO and JuiceboxDAO, we can see that the parameters of Cycle Duration and Target determine whether financing has clear time and amount limits, with different settings suitable for different types of financing.

ConstitutionDAO's financing was aimed at participating in the bidding, which inherently had no target cap, adopting an unlimited financing form, requiring retail investors to bear higher risks. In contrast, JuiceboxDAO's form is suitable for financing projects with clear funding needs, such as company operations.

1.2 Distribution & Reserve Rate ------ Specifying Use of Funds

The success of financing hinges on the future flow of funds, which is also a type of business plan presented by the financing project party to the public.

Through Juicebox, project parties can specify in the contract which addresses the funds within the financing target will be allocated to, which is the Distribution function. Additionally, project parties can set a Reserve Rate, meaning that a portion of all funds raised in this round of financing will have additional allocation purposes.

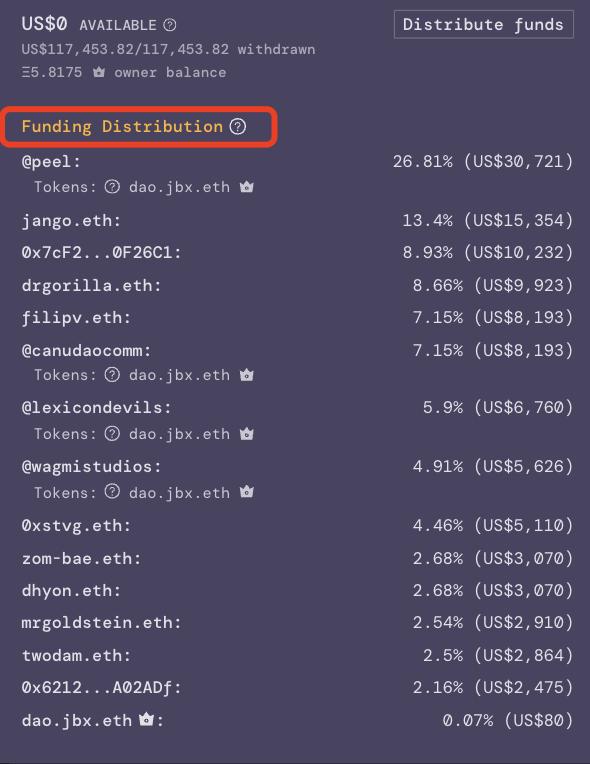

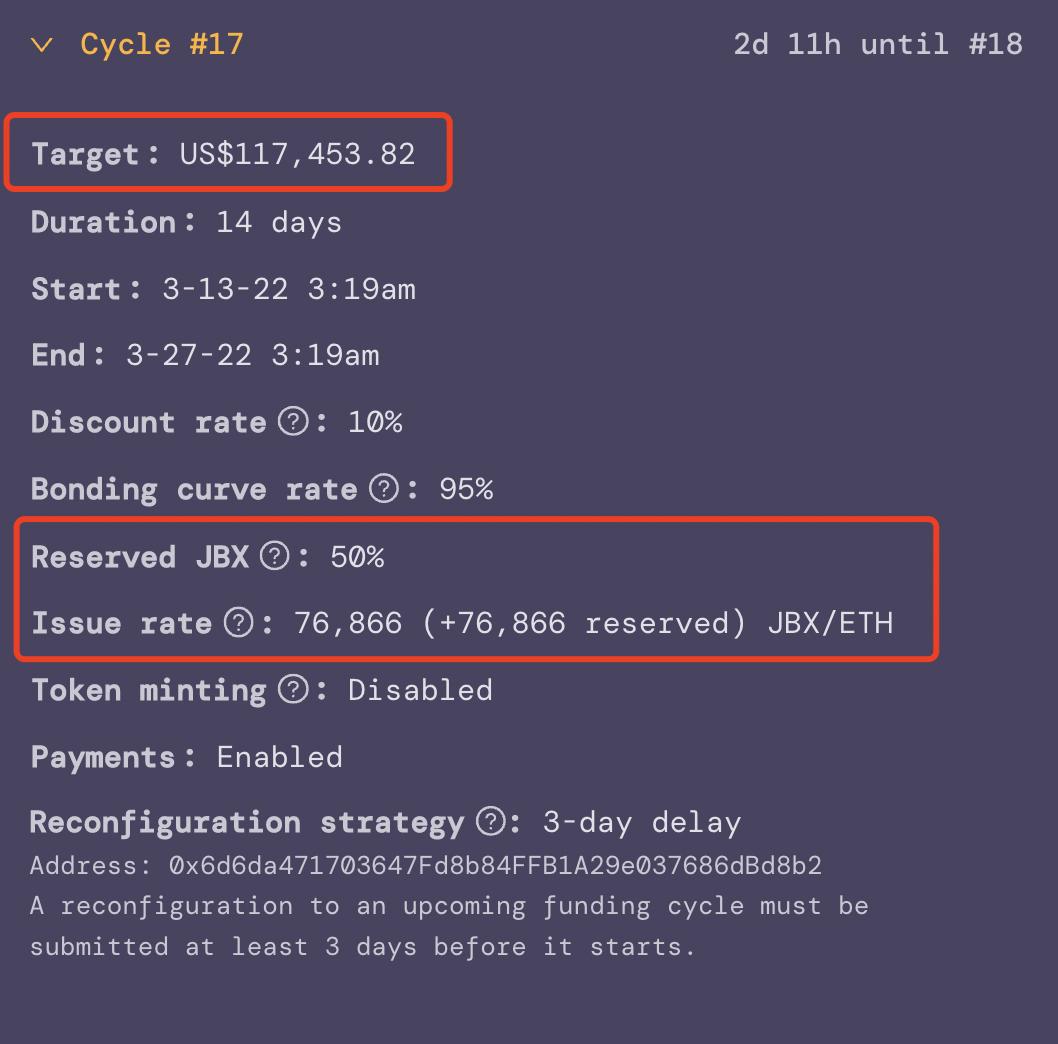

Taking the latest round of financing for JuiceboxDAO as an example, the amount within the financing target will be automatically transferred according to the table below, completing fund allocation. This round of financing raised $117,000, which has been fully allocated.

In this round, JuiceboxDAO set the Reserved Rate at 50%, meaning that 50% of all new investment funds will ultimately be allocated according to the following ratio, with the vast majority flowing to the JuiceboxDAO address.

It is worth noting that the amount used for Distribution is fixed; on one hand, it will not grow indefinitely with the increase in investment amounts, and on the other hand, it can be transferred from the previous round's Overflow, ensuring sufficient funds. For example, in JuiceboxDAO's latest round of financing, it actually only raised ~6 ETH, but the actual allocated funds amounted to $117,000, which was transferred from historical Overflow. The Reserved portion is proportional to the investment amount and is uncontrollable.

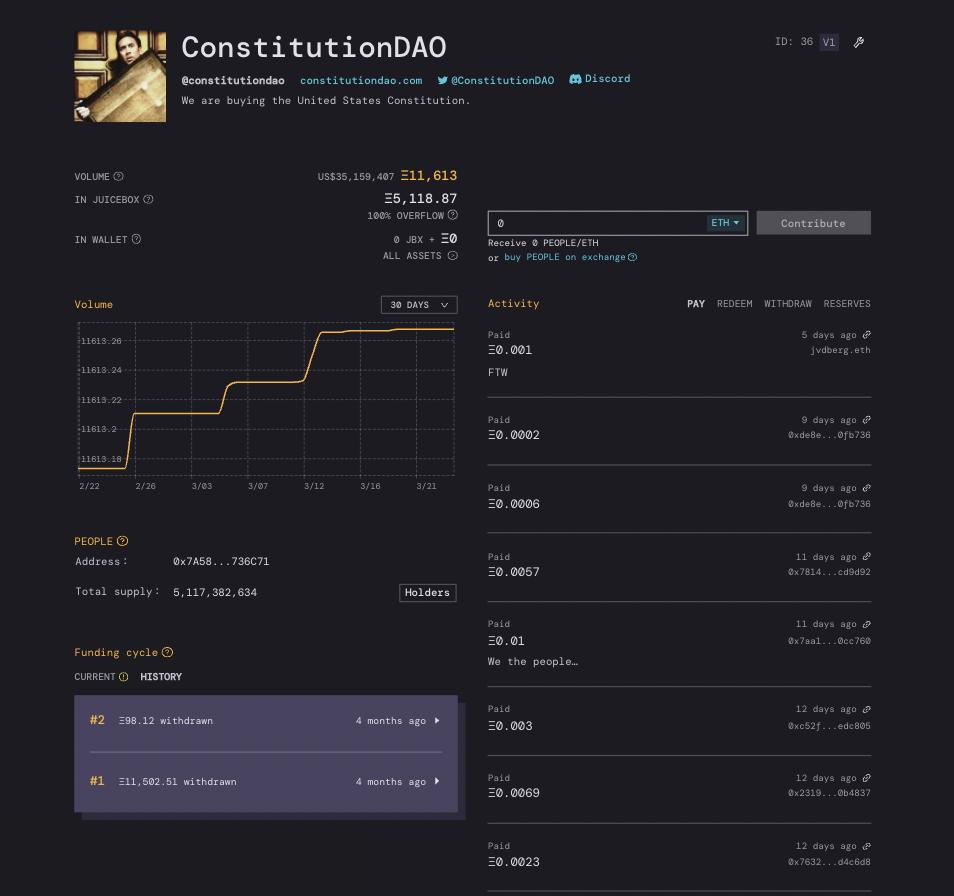

Of course, the above situations can only occur on-chain. Observing the financing page of ConstitutionDAO, one cannot find the Distribution and Reserved Rate sections, as its fund usage occurs off-chain during the bidding. This aspect also represents the capability boundary of all DAO tools; once off-chain funds are involved, trust in the project party becomes essential.

ConstitutionDAO Financing Page

1.3 Discount Rate & Bonding Curve Rate ------ Shaping Token Economic Model

These two numbers can be considered magical generators that shape the project's token economic model and will have a profound impact on the project's development.

Discount Rate is the depreciation rate of project tokens in future financing rounds, essentially determining the subsidy amount for future users compared to current users, which can be used to incentivize early investments. The exchange rate in the first round of financing for all projects is fixed, with 1 ETH exchanging for 100,000,000 project tokens, while subsequent exchange rates are determined by the Discount Rate.

For example: Suppose a project's parameter setting has a Discount Rate of 10%, then in the first round of financing, investing 5 ETH can obtain 5,000,000 project tokens, while in the second round, investing 5 ETH can only obtain 450,000,000 tokens (5,000,000 * 90%). This value carries a FOMO effect; the larger the value, the more depreciation occurs in later investments.

Bonding Curve Rate is the exchange curve for users burning project tokens to redeem ETH, determining the losses for early redemptions, which can be used to incentivize users to keep their funds in the project.

For example: Suppose a project sets its financing target at 1 ETH, and both a and b invest 5 ETH, resulting in a total of 10 ETH in the treasury, with the financing target of 1 ETH allocated by the project party, leaving 9 ETH available for redemption as Overflow.

Assuming the Bonding Curve Rate is 50%, if a redeems first, they can redeem a maximum of ~2.5 ETH, while the remaining ~6.5 ETH can be fully redeemed by b.

If the Bonding Curve Rate is 100%, then regardless of who redeems first, both a and b can redeem a maximum of 4.5 ETH.

Discount Rate and Bonding Curve Rate are core parameters for setting project incentives. A higher Discount Rate and a lower Bonding Curve incentivize users to enter early and exit late, increasing the project's FOMO index; conversely, users can enter and exit more freely.

Using ConstitutionDAO and JuiceboxDAO to observe the differences in settings.

In the first round of financing for ConstitutionDAO, the Discount Rate was 0%, meaning the exchange rate in one round of financing was the same as in this round, while the Bonding Curve Rate was 100%, meaning that during redemption, regardless of the order, users could redeem corresponding shares according to their holdings. For users, there was no difference in entry timing.

ConstitutionDAO's First Round Financing Parameters

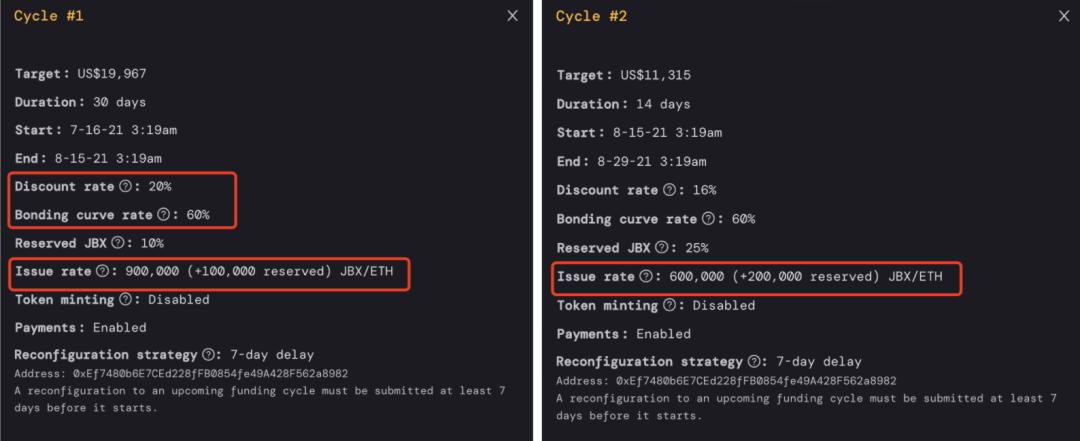

In contrast, JuiceboxDAO clearly incentivizes users to enter early and exit late. As shown in the following image, the first round of financing set the Discount Rate at 20%, with the first round's exchange rate fixed at 1 ETH for 10,000,000 JBX, and since 10% is reserved, users actually receive 900,000 JBX.

In the second round, the exchange rate is 80% of the first round, with 1 ETH only redeeming 800,000 JBX, and with a 25% Reserve Rate, users can actually only receive 600,000 JBX.

Looking at the Bonding Curve Rate, the first two rounds were set at 60%, meaning early redeeming users can only redeem about 60% of their share of the Overflow, with later redemptions yielding more shares.

JuiceboxDAO's First and Second Round Financing Parameters

The token economic model of JuiceboxDAO itself will be detailed in section 3. At this point, we can at least see that changes in the entry exchange rate and redemption exchange rate will have a huge impact on retail investors' entry choices.

1.4 Future Function Expansion

The above functions are all built on the V1 version. This version's token economic design has some common characteristics, including: project tokens can be issued infinitely without limits, new users can always enter and invest, and only the portion in Overflow can be redeemed by users, etc.

The team is developing the V2 version, which will allow for changes in the above characteristics. The core functions of V2 will include: setting a token cap and the exchange rate for each ETH, allowing termination of financing, and permitting project parties to mint and burn tokens at any time, etc.

The core changes in the V2 version revolve around setting the token economic model, aiming to achieve more flexible and free financing forms and economic models.

2: Token Economics

The token economic model of Juicebox is implemented by JuiceboxDAO, which is also built on the Juicebox project, using the current V1 version, namely the unlimited issuance model.

It is important to note that the current total supply of JuiceboxDAO tokens is approximately 2.47 billion, while CMC and Coingecko both show it as 1.17 billion, with the difference not being extracted in the contract and thus not recorded. Based on market prices, JuiceboxDAO's current valuation is about $17 million.

2.1 Value Capture: Unlimited Issuance but Not Devaluation

The token JBX of JuiceboxDAO is not a functional token, serving only governance purposes. DAO governance is conducted through voting on Snapshot, with voting weight corresponding to the share of JBX held.

Without functional utility, where does the value of JBX come from? The answer is: it comes from new investors purchasing newly issued JBX at high prices, with the platform mandating project parties to buy as a fee, essentially taxing the platform to subsidize early buyers.

In section 2.3, the roles of Discount Rate and Bonding Curve Rate are illustrated using JuiceboxDAO as an example. In fact, the Discount Rate largely determines the "appreciation rate" of JBX.

The Discount Rate for JuiceboxDAO's first round of financing was 20%, the second round was 16%, and the latest round is 10%. Although the values are gradually decreasing, the Discount Rate compounds multiplicatively, meaning after two rounds of 10%, it can only redeem the initial 81% of JBX.

Ignoring the Bonding Curve, all funds in Overflow are redeemed according to the share of JBX held, so the Discount Rate does not devalue JBX, but rather makes newly issued JBX devalue while early purchased JBX appreciates, subsidizing early investors with the high price of newly issued tokens.

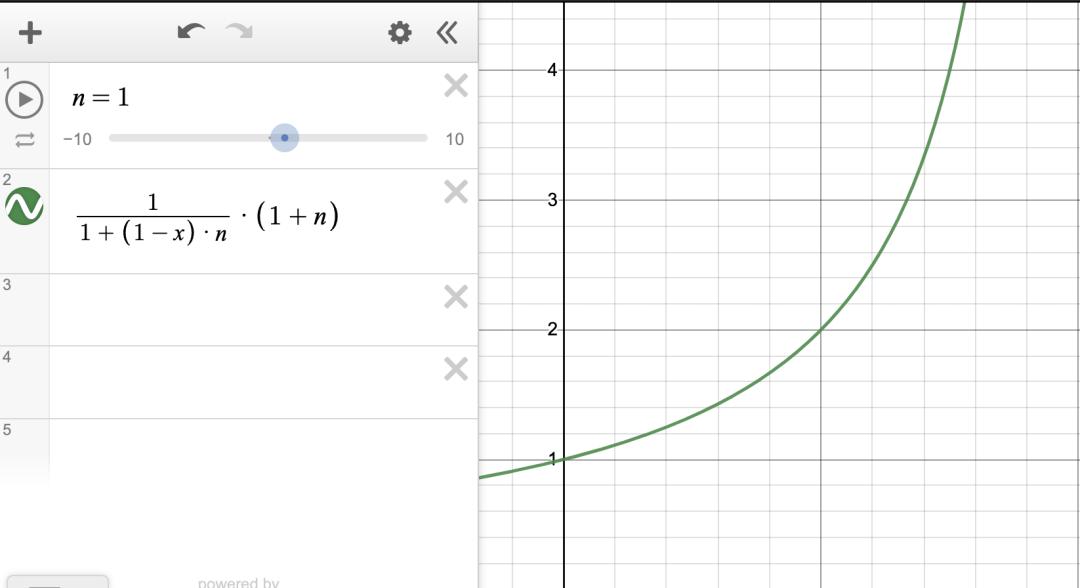

The author has plotted graphs with Discount Rate and future new fund amounts as parameters to illustrate this (the following does not consider Bonding Curve Rate and Reserved Rate).

In the following graph, n represents the new fund amount as a multiple of the original, assuming n=1; x represents the Discount Rate, and y represents the total redeemable amount of funds. As the Discount Rate increases, y will significantly increase.

Address: https://www.desmos.com/calculator/9mz7ffd4fl

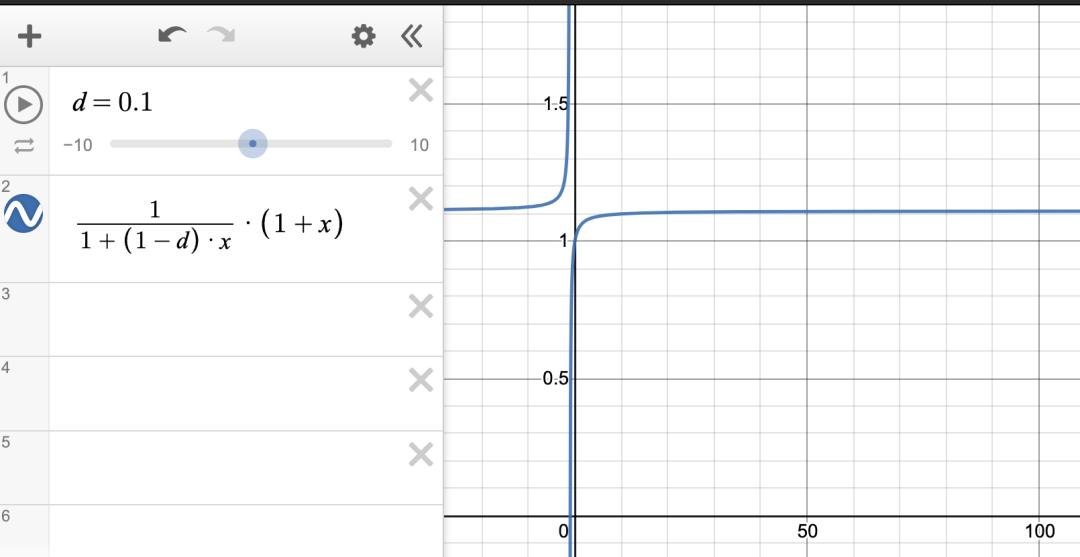

In the next graph, d represents the Discount Rate, assuming d=10%; x represents the new fund amount as a multiple of the initial investment, and y represents the total redeemable amount of funds. As x increases, y will also continue to increase, though the increment will become smaller.

Address: https://www.desmos.com/calculator/y2wmg5pat6

Thus, when the Discount Rate is greater than 0, as the amount of new investment increases, early JBX will become more valuable. Of course, this temporarily ignores other effects caused by Bonding Curve Rate and Reserved Rate, or assumes Bonding Curve Rate=1 and Reserved Rate remains unchanged.

This creates an interesting phenomenon: JBX can be issued infinitely but does not devalue. This is essentially because the Discount Rate causes the price of newly issued tokens to be higher than the current redemption price, with the funds from new investors used to subsidize early investors.

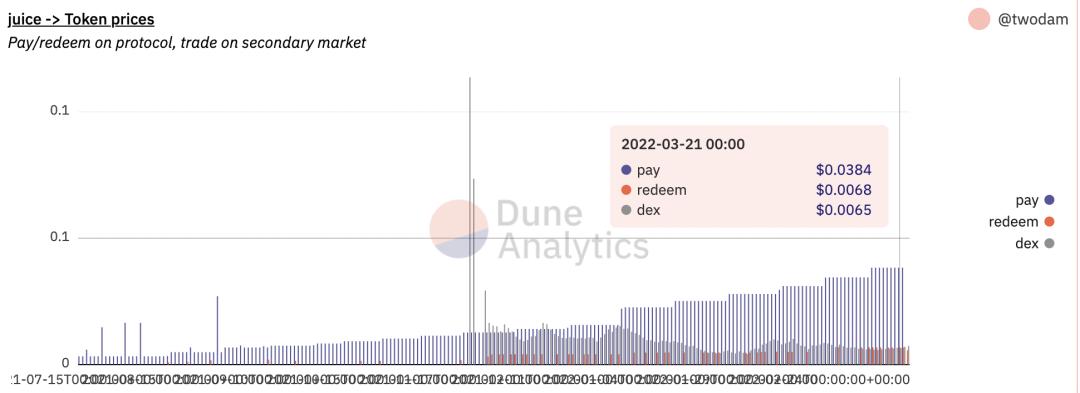

The historical issuance price, redemption price, and trading price shown in the following graph indeed confirm this phenomenon. The issuance price gradually rises, always far above the redemption price; meanwhile, the redemption price is also slowly climbing, currently close to the secondary market trading price.

Source: https://dune.xyz/twodam/Juicebox-Projects

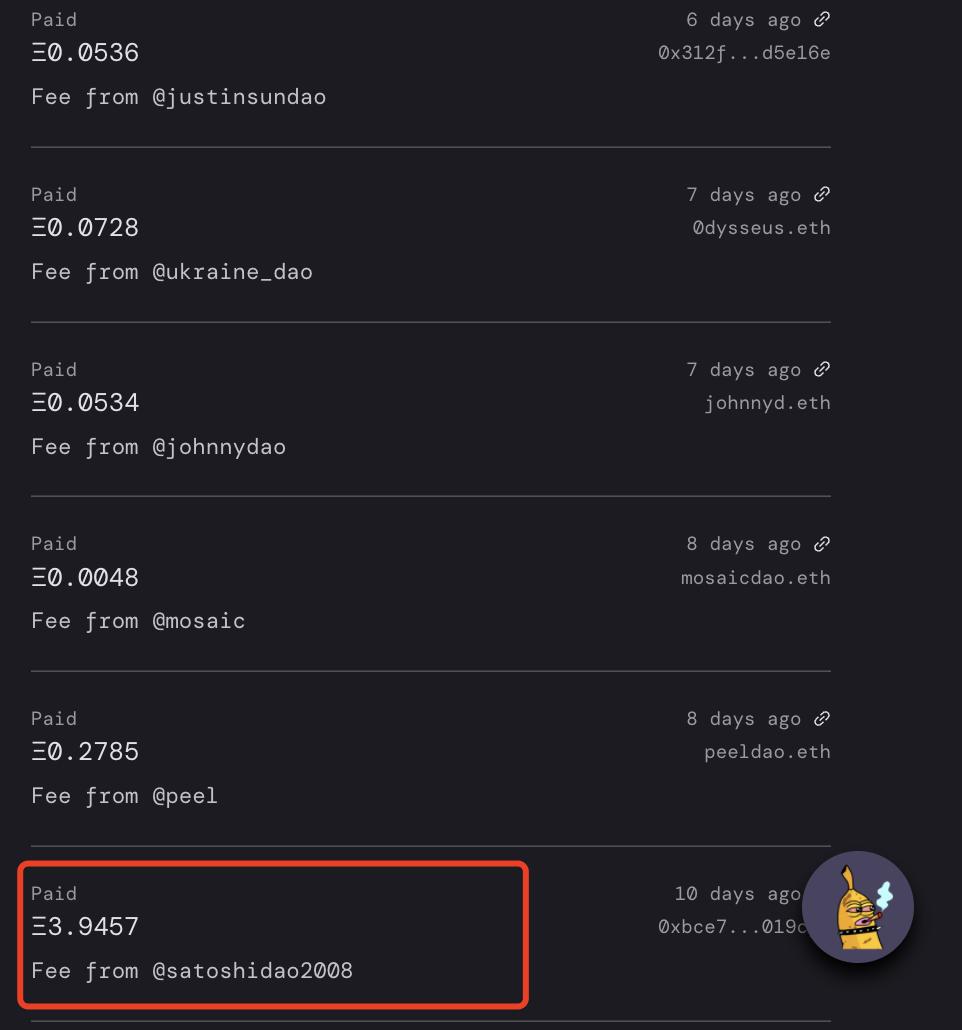

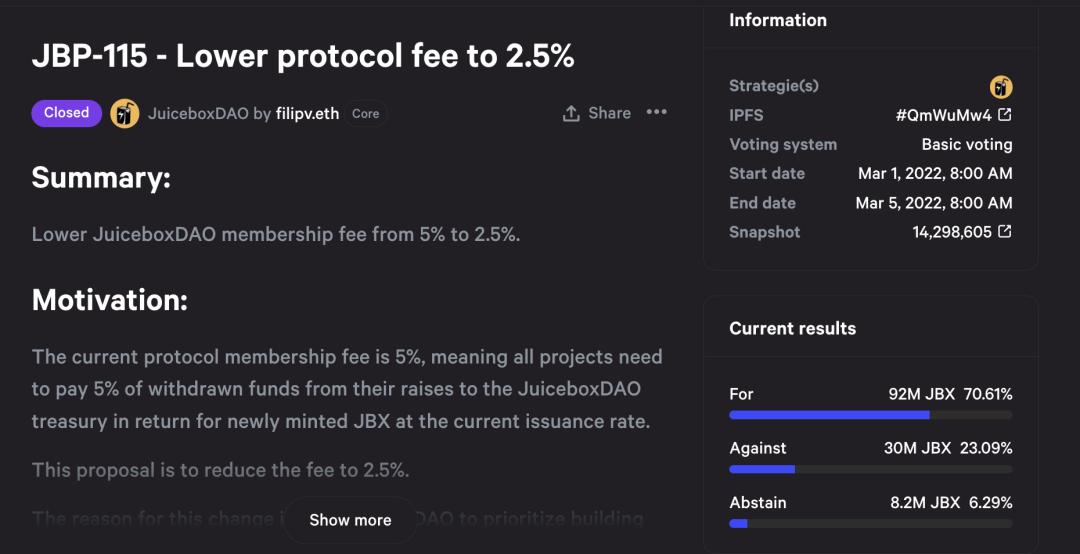

So, since the issuance price is far above the market trading price, who would still participate in investing? Indeed, the current actual investments mostly do not come from individual investors but from the fees Juicebox charges project parties on the platform: 2.5% of the financing amount extracted by each project from Juicebox (initially 5%, reduced to 2.5% through voting in March this year), which will be converted into new investments for JuiceboxDAO and exchanged for a certain amount of JBX according to the current financing parameters, becoming JBX holders.

For example, in JuiceboxDAO's latest round of financing, ~6 ETH primarily came from project fees, with the main costs coming from a project called SatoshiDao.

Source: https://juicebox.money/#/p/juicebox

In summary, the price of newly issued JBX is not the real price but rather a disguised fee charged by the platform for projects built on Juicebox, essentially a form of platform taxation.

For investors, there is no need to mint new tokens, as the secondary market offers better prices. The appreciation of JBX relies on an increasing number of new projects joining Juicebox, pushing up the redemption/market price.

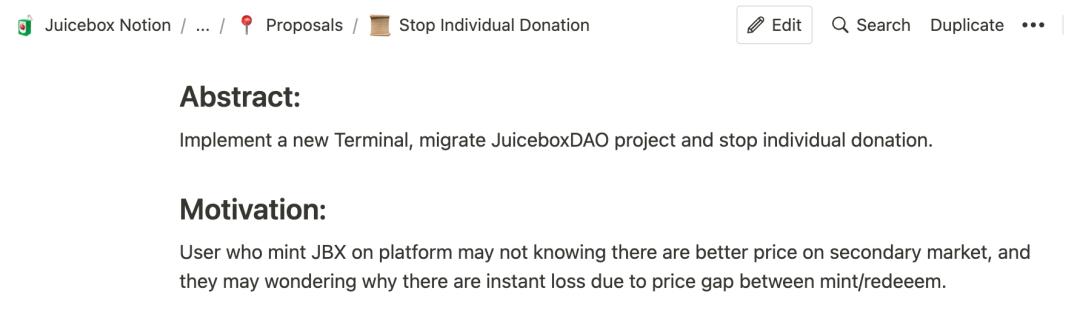

In fact, according to a proposal from March, individual investors accounted for only 1.8% of the total new funds in the past three months, and community proposals have suggested directly closing individual investment channels, guiding retail investors to purchase JBX in the secondary market.

Source: https://www.notion.so/Stop-Individual-Donation-4d74a422264149f4b085630488664c97

2.2 Dynamically Adjusted Token Distribution

Each round of financing for JuiceboxDAO will issue new JBX tokens, and the token distribution will dynamically adjust according to the parameters set for each financing round, mainly divided into three parts: 1) Pre-allocation of the Target financing amount; 2) Retained allocation of new funds in each round of financing; 3) Allocation of tokens redeemed by new investors.

Returning to the latest financing information for JuiceboxDAO can help better understand the above distribution.

1) The Target financing amount is allocated to multiple on-chain addresses according to the predetermined Distribution plan, primarily as salaries for employees/contributors. It is important to note that this round of financing only raised ~6 ETH; the $117,000 here comes from the Overflow of previous financing rounds. The team injected historical Overflow into the new round to complete the Target, with the remaining portion and new funds entering the new Overflow.

2) Reserved JBX, which is the retained portion of new financing, is approximately ~3 ETH, with about ~75% flowing to the JuiceboxDAO on-chain address, and the rest evenly distributed to employees/contributors.

3) Tokens redeemed by new investors will yield 76,866 JBX for every 1 ETH invested. The 2.5% withdrawal fee charged by Juicebox for all projects built on Juicebox will be treated as new investment for JuiceboxDAO, equivalent to platform tax, and is currently the main source of income for JuiceboxDAO.

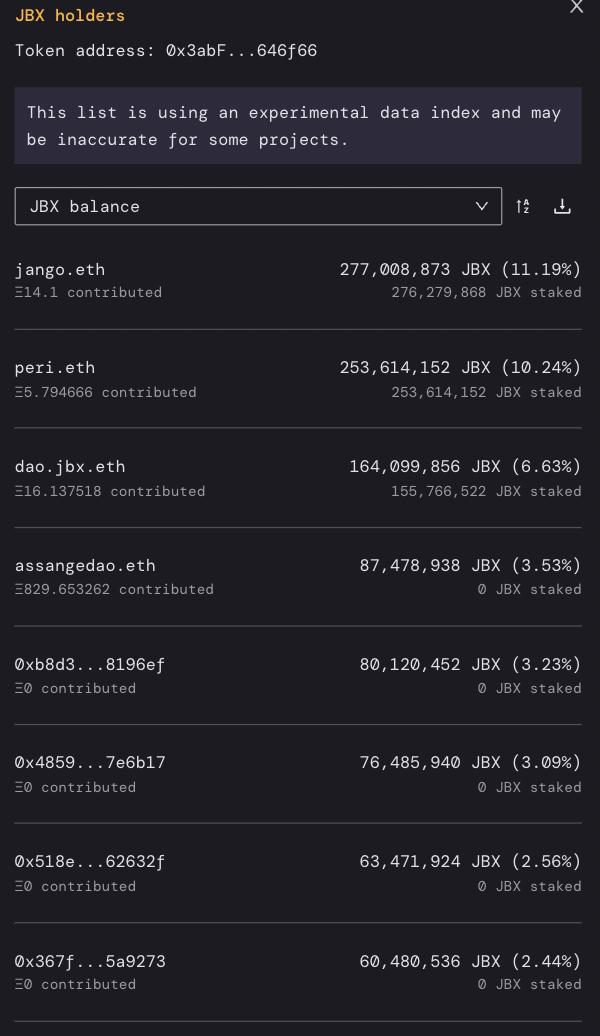

The above distribution will dynamically adjust, and the current overall token distribution status is shown in the graph, with founder jango and another core member peri each holding ~10%, JuiceboxDAO holding ~7%, and the rest held by other paying DAOs or investors.

Source: https://juicebox.money/#/p/juicebox

3: Operational Status

3.1 Business Scale

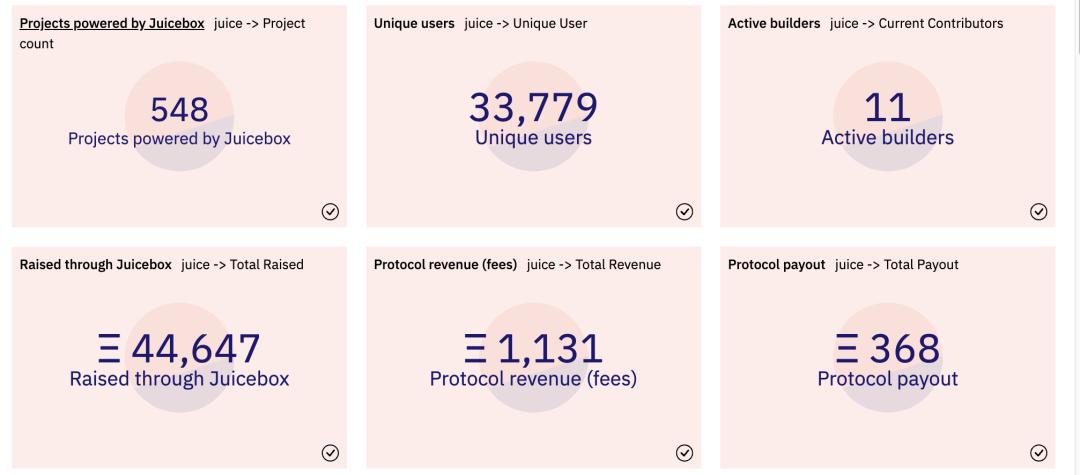

Juicebox went live on ETH in July 2021 and has currently deployed ~550 projects, raising a total of ~44,647 ETH, approximately $160 million.

Source: https://dune.xyz/twodam/Juicebox-Protocol-Overview

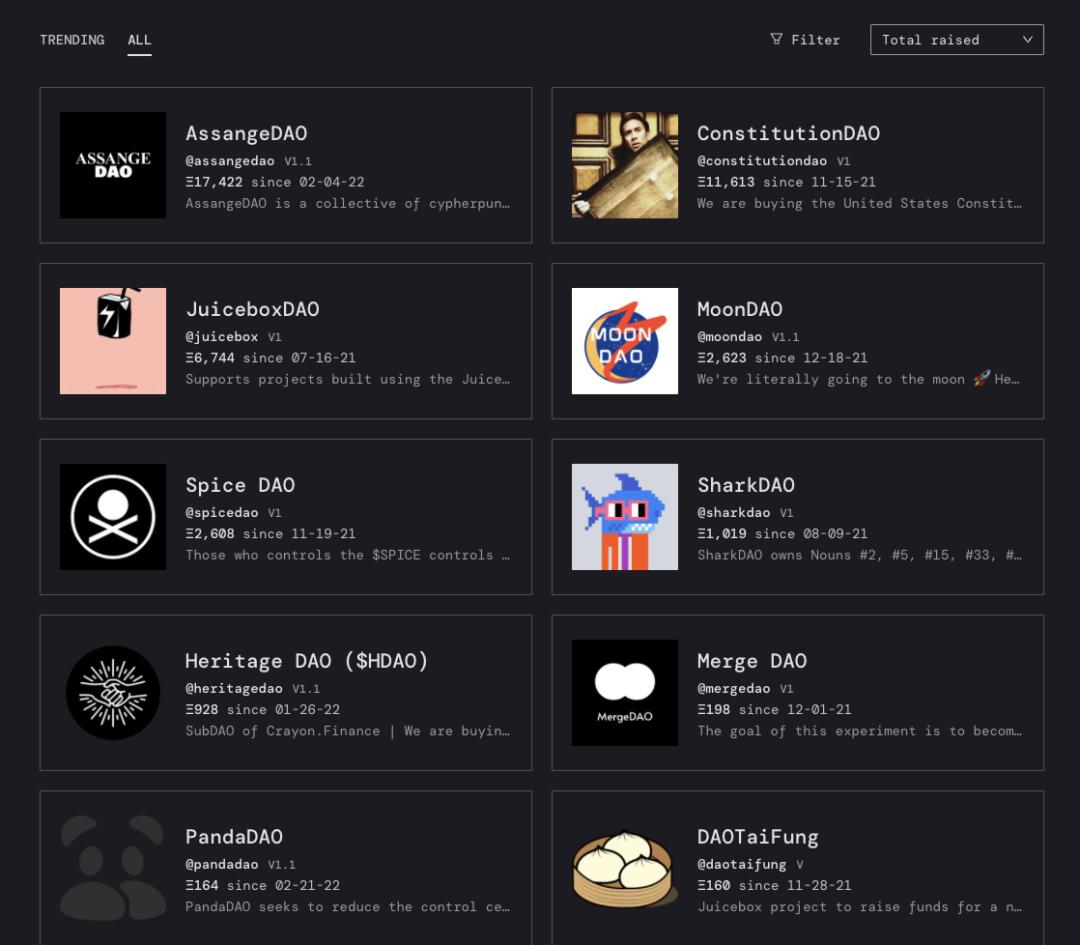

The cumulative financing amount of the Top 10 projects ranges from 160 to 17,422 ETH, equivalent to approximately $500,000 to $53 million. The vast majority of other financing amounts are very small.

Top 10 projects by financing amount on Juicebox, Source: https://juicebox.money/#/projects?tab=all

Juicebox's scale is not large in the crypto world, with a total supply of 2.4 billion tokens, a unit price of $0.007, and an FDV of about $17 million. However, Juicebox has already supported two well-known DAO organizations—ConstitutionDAO, which bid for the constitution copy, and AssangeDAO, which rescued Julian Assange, holding a place among DAO tools.

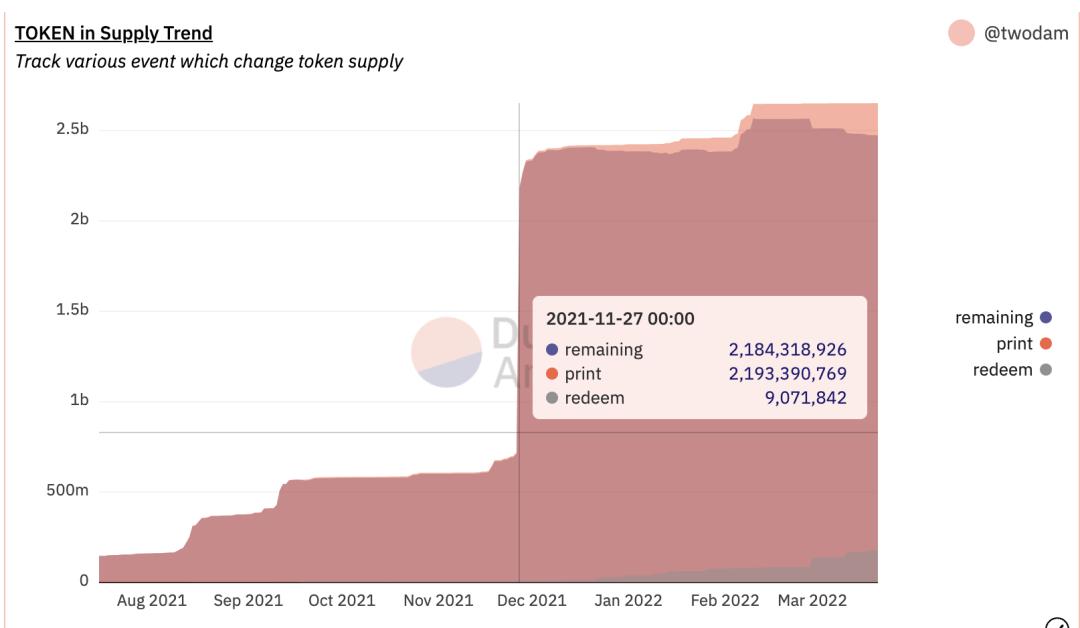

Juicebox first gained attention due to its association with ConstitutionDAO. On November 27, 2021, it experienced the first wave of surging prices, minting approximately ~1.48 billion JBX, accounting for about 56% of all minted amounts.

Source: https://dune.xyz/twodam/Juicebox-Projects

This surge coincided with the first peak date of People in the secondary market, likely driven by People.

However, since then, Juicebox's development has been relatively slow, with no particularly eye-catching changes in funding.

The team's planned future roadmap includes: enhancing education on product usage; creating dashboards to assist analysis; increasing L2 payment channels; developing functions to utilize Overflow for investment, etc.

Overall, the team's working style is relatively "laid-back and pragmatic," lacking large-scale promotional efforts and focusing on functional development. The project has not yet undergone an audit, existing somewhere between a grassroots experiment and a formal commercial product.

Perhaps due to the lack of promotion, the token price has performed poorly, currently close to the redemption price, equating to the token price reaching its lowest point. JuiceboxDAO has a balance of ~18 million dollars in the contract; simultaneously, with a total token supply of ~2.4 billion, the current token price is ~0.007 dollars, and FDV is ~17 million dollars, meaning each JBX is backed by approximately ~1.05 dollars worth of ETH.

3.2 Community Governance

Juicebox's community building is also quite earnest and simple, with strong spontaneity and weak FOMO characteristics.

The community's information disclosure is relatively sound, especially with professional dashboard construction, making the number of all projects on Juicebox, their financing amounts, and the financing history of each project clear at a glance. The smooth writing of this article is also thanks to the effectiveness of data disclosure.

Many of Juicebox's employees are contributors gradually recruited during the establishment process. Notably, there are several contributors from China, and the only foreign language channel in the Discord group is the Chinese channel.

Core governance issues are conducted on Snapshot, such as a proposal vote in March that reduced the withdrawal fee from 5% to 2.5%. The voting rate is around ~6%.

Proposal related to withdrawal fees

On March 11, the community just airdropped 100 million JBX, valued at about $700,000 at current market prices. The airdrop evaluation principle is 60% based on governance and 40% based on holdings. Future airdrops are expected to occur irregularly to reward users' contributions.

Additionally, the community is currently considering a staking plan.

4: Team and Financing

The team is very grassroots, with almost no public information available online.

The founder, jango, is responsible for writing smart contract code, and most of the early blogs and educational promotions for Juicebox were also completed by jango. Another core member, peri, is responsible for the front end, with the webpage used by ordinary users at https://juicebox.money/ being written by him. Both hold ~10% of JBX shares. Additionally, peri also founded an art-related TileDAO during the early establishment of Juicebox as the first experimental project.

According to Discord, there are currently ~20 community contributors, with part of the amount from each financing allocated as wages based on labor distribution.

Juicebox has not yet received any capital investment, relying on the amount raised in each round of financing for operational capital.

5: Summary: Advantages and Risks

Chain Teahouse believes that Juicebox's core advantages include:

1) It operates in the DAO tools sector, and the development of the DAO ecosystem will inevitably drive the foundational tools, with high certainty and a high ceiling for the track.

2) The product has already been put into practical use, and well-known AssangeDAO and ConstitutionDAO are both built on Juicebox, validating market demand and establishing a certain reputation foundation.

3) The value support behind the token is relatively solid, being one of the few projects where the ETH balance on the books exceeds the FDV.

At the same time, Juicebox also faces some uncertainties, including:

1) The product's functionality is purely single, which may lead to widespread adoption due to the extreme fundraising function, but it may also fall behind more comprehensive DAO tools that provide one-stop management for funds/proposals/members, such as SuperDAO, which completed a $10.5 million financing in January this year, with a valuation of $160 million.

2) The team's laid-back and pragmatic style is good for product development but lacks operational promotion investment; if faced with fierce competition, it may lose users.