How to arbitrage from the crypto market using contract funding rates?

The funding rate is a mechanism that ensures the price of perpetual contracts stays close to the underlying index or price, where there are many arbitrage opportunities.

The funding rate is a mechanism that ensures the price of perpetual contracts stays close to the underlying index or price, where there are many arbitrage opportunities.Original Author: kasper vandeloock, Quant Trader at Musca Capital

Original Title: 《Profiting from inefficiencies in the crypto markets: funding rates》

Translation by: Hu Tao, Chain Catcher

Back to the good old days of 2015-2016, if you were an ambitious trader with arbitrage experience, you could easily earn a few percent profit by simply arbitraging the price differences between two cryptocurrencies across different exchanges.

However, today, it is much more difficult to profit using simple arbitrage strategies. Since then, the industry has matured significantly. First, the total market capitalization of cryptocurrencies has grown from $10 billion in early 2016 to nearly $3 trillion by the end of 2021. Secondly, exchanges have greatly improved. This has certainly attracted many quantitative traders from traditional finance to seize the opportunity (such as Alameda Research, Wintermute, MNGR, etc.).

However, even with all these big players joining the fray, small firms/individuals can still take advantage of many inefficiencies. Let’s look at some examples of delta-neutral strategies that exploit these market inefficiencies, particularly in collecting funding (from perpetual contracts).

What is the difference between delta-neutral and market-neutral?

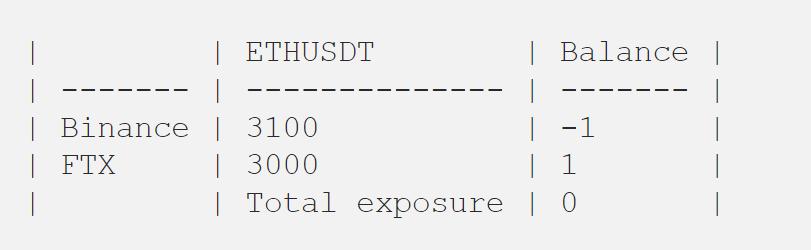

Delta-neutral is a strategy where the total exposure to a specific asset is zero. For example, suppose you find a price difference between Binance and FTX.

One way to profit from this is to borrow 1 ETH on Binance and sell it. Then, buy 1 ETH on FTX and send it back to Binance to repay your loan. This way, you have no risk exposure but can still make a profit.

However, market-neutral is a bit different. It simply means that your total exposure to the asset class market is zero. In most cases, you would choose a portfolio of assets within the same category; in this example, we are using layer 1 Ethereum and Cardano.

Collecting funding rates

So, what exactly is a funding rate? A funding rate is a mechanism that ensures the price of perpetual contracts stays close to the underlying index or price. If the trading price of a perpetual contract is higher than the underlying index, long positions pay funding to short positions. If the perpetual contract trades below the underlying index, short positions pay funding to long positions. The funding rate paid/received is determined by the following formula:

*Position size * ((Contract price - Index price) / Index price) / 24-hour time-weighted average price*

Here is an example from FTX, but the formula varies by exchange depending on their funding rate intervals.

How do we profit from this mechanism?

In the following example, we set a stable funding rate of 0.0198%/hour for Bitcoin (BTC) perpetual contracts (i.e., BTC-PERP). This means that longs will pay shorts. To collect this funding rate, all we need to do is short BTC-PERP to earn the hourly fee on our position.

However, of course, this exposes us to BTC price risk, which we want to avoid. So we buy 1 BTC in the spot market to hedge our initial short position. Since we now hold 1 BTC and are short 1 BTC-PERP, changes in the price of BTC will not affect our capital.

During this 24-hour period, we will earn a total of $309.09 without any BTC price risk exposure.

But how can we make more profit from this strategy?

- Cross-exchange funding arbitrage

- Altcoins

- Using leverage

- Optimizing EV plays

Cross-exchange funding arbitrage

There are and will always be slight differences between perpetual contracts across exchanges. This is not because there are more buyers than sellers in a specific market, but because they:

- Use different weights for their indices (see the example of how to calculate funding prices);

- Pay funding rates at different intervals (e.g., hourly on FTX, every eight hours on Binance);

- Some traders cannot access certain trading platforms, leading to price discrepancies.

Because of this, you can find opportunities where the funding rate on one exchange is positive while on another it is negative. Most of the time, these opportunities arise after significant price fluctuations when traders have to close out positions.

One example today is Algorand (ALGO), which saw its price surge by 20%, leading to several large short liquidations. This sudden spike was driven by the token listing on the South Korean exchange "Upbit." These opportunities are usually quickly arbitraged, but the returns you can get are certainly substantial.

In the first example, we hedge our perpetual contract short position by buying spot on the same exchange, whereas here we can go long ALGO-PERP on Huobi and earn 1.5%/hour, while shorting the same amount of ALGO-PERP on FTX and earning 0.0015%/hour (due to the positive funding rate).

Remember, you must rebalance your collateral on the exchange to avoid liquidation.

Using altcoins

Compared to top tokens like BTC or ETH, the index and contract price differences for altcoin perpetual contracts are typically larger, especially after significant price fluctuations. This is beneficial for us as it offers higher returns, but this strategy comes with some risks.

First, you need sufficient liquidity; if you cannot easily build a position without low market impact, you should not trade.

One positive factor that many people do not consider when using this strategy on altcoins is that often the price difference between the index and the contract is not the only profit factor. Altcoins often have price discrepancies between different exchanges because many of these tokens carry higher risks than major tokens, thus having lower priority for arbitrage…

Some of these higher risks include:

- Slower networks

- High transaction validation requirements

- Deposits disabled by certain exchanges

- Low liquidity

However, this is good for us because these price discrepancies will be arbitraged over time, and it also makes using spot hedges cheaper.

You might find things like high transaction validation requirements strange, but tokens like Ethereum Classic (ETC) require a lot of block validation data because "cheap" networks are prone to hacks. What do I mean by this? In the past, hackers used third-party mining services to rent large amounts of GPUs to mine on ETC until they took over at least 51% of the network to execute a 51% attack. In other words, they had more than 51% of the hashing power of the network, allowing them to falsely validate transactions on the blockchain and transact from wallets they do not own. For a more detailed explanation, I recommend this article.

Using multiple alternative trading platforms

By alternative trading platforms, I mean decentralized exchanges (DEX) such as:

- Mango markets (Solana)

- Perpetual Protocol

- dYdX

Most of these platforms do not have much liquidity and offer some interesting opportunities. Of course, there is a problem: most of these platforms are built on Ethereum, which currently has very high fees. Additionally, you need to have funds on the platform to execute trades; otherwise, the opportunity may disappear once your funds arrive.

Moreover, most of these platforms require you to deposit funds into smart contracts, so you also face the risk of losing your collateral if the platform is hacked.

Most people would argue that this could also happen on centralized trading platforms, but compared to a few years ago, these platforms have improved significantly. They use a combination of hot/cold wallets, they have large insurance funds, stablecoins like USDT and USDC may be frozen, and the number of hacks on CEX has drastically decreased over the years, despite more funds being deposited onto them.

Using leverage

For example, the most obvious approach is simply to use a certain amount of leverage on perpetual contracts and borrow enough USD/tokens as margin to hedge.

This will require a lot of rebalancing. The main issue is that it lacks capital efficiency.

You will see that most platforms only accept stablecoins like USDC/USDT/BUSD for contract trading. So, suppose you want to short 3 BTC worth $50,000/BTC; you need enough funds to buy 3 BTC and short 3 BTC, which is about $300,000, not the optimal strategy.

Platforms like FTX have an interesting feature that allows you to use any token as collateral for your contract account. This makes it easier to improve capital efficiency.

Suppose you want to execute the same trade, shorting 3 BTC on FTX and buying 3 BTC in spot; we have $150,000 in capital.

The current weight of BTC is 0.975, which means if we have $150,000 in BTC, we can use ($150,000 * 0.975) = $146,250 in collateral to trade futures contracts.

So you will automatically be forced to use leverage. Now, because we are using non-USD as collateral, we need to make trade-offs. Once your balance breaches the -$30,000 threshold, FTX will automatically start liquidating your tokens. Make sure you have enough collateral to maintain your account.

In this case, if the price of BTC drops, that will not be an issue. However, if the price of BTC rises to $9,750, you will run into problems. Therefore, ensure that you have rebalanced your position before reaching that level to always keep your delta at 0.

You can find the calculation method for FTX collateral here, but don’t forget to consider the IMF factor to avoid liquidation when using non-USD collateral.

Optimizing EV plays

The benefit of funding is that it is easy to maximize EV (expected value); you know exactly when you will be rewarded, and you can calculate the funding rate with high certainty (see the funding rate calculation example at the beginning of the article).

Create a data frame where you can place all potential trades you can make, which could be a simple funding collector or cross-exchange funding arbitrage. Calculate how much it pays per hour, compute the costs it will incur, such as trading fees and withdrawal fees, and multiply it by the probability based on previous trades.

Furthermore, considering that you can profit from market-making fees, do not wait until the trade is completed to check if it is more profitable.

This type of strategy is profitable because it can execute many profitable trades, occasionally incurring small losses, and there are many ways these trades can go wrong.

- Poor position management

- Order failures or poor execution

- Trades disabled by the market

- Connection issues

- Deposits/withdrawals disabled or slowed

- CEX/DEX downturns

- Liquidation risk when using leverage

- False data

- Trade failures => Example

All these topics should have their own articles, and I will not elaborate on them in this article. However, if you decide to try executing one of these strategies, be sure to consider these risks and think about how to avoid them.

Conclusion

By leveraging small inefficiencies, there are many opportunities in the crypto market. Unfortunately, it is not as easy as it was a few years ago when a simple arbitrage could yield substantial profits, but this indicates that the space is evolving.

The enormous profits that can be derived from exploiting these inefficiencies are still available; you just need to think a bit more than before :)

Related Reading: 《Perpetual contracts can do more than hedge risks; a detailed explanation of how to profit from funding rates arbitrage》