The Curve War upgrades the battle for CVX, and the exciting power struggle continues

The original Curve War seems to have turned into the Convex War, with CVX becoming the most important and popular character in the Curve War.

The original Curve War seems to have turned into the Convex War, with CVX becoming the most important and popular character in the Curve War.Author: 0x137, @ Rhythm BlockBeats

The Curve War, which erupted as early as August 2020, has not received enough attention for a long time. However, with the emergence of Convex, the situation has changed dramatically, and various protocols have begun to compete for the influence of CVX. The atmosphere of war has become increasingly intense, and CRV, CVX, and YFI have also shown strong performance in the past month. Why is there a Curve War? Who are its main participants? Who are the biggest winners?

Why is there a Curve War?

Curve, as a stable AMM focused on low slippage, issues governance token CRV as an incentive for providing liquidity, thereby increasing the liquidity depth of various stable pools on the Curve platform and maintaining the peg capability of the stablecoin. From this perspective, Curve seems no different from other DeFi 1.0 protocols that rely on liquidity mining.

However, Curve has a very key mechanism that greatly differentiates it from traditional liquidity mining: by locking CRV, liquidity providers (LPs) can correspondingly obtain veCRV, which has actual governance significance for the liquidity incentives on the Curve platform, possessing the power to change the "gauge weights."

In other words, the liquidity incentives for each mining pool on the Curve platform will be determined by the voting power of veCRV. The more veCRV holders vote for it, the higher its liquidity incentives will be. As a result, CRV has become an important component of the returns that other protocols offer to their stakeholders. To increase their APY/APR, these protocols have to accumulate veCRV in various ways to compete for the liquidity incentives of Curve, leading to the protracted Curve War.

Strictly speaking, the Curve War is a mercenary war. veCRV holders cannot vote for a specific mining pool out of thin air; to do so, the protocol must offer them sufficiently enticing "bribes."

For example, if you vote for the MIM (Abracadabra platform stablecoin) mining pool, you can receive corresponding SPELL tokens (the native token of Abracadabra). In the latest round of Votium voting, the total "bribe" from the Abracadabra platform even reached $969,000.

Amidst the intense conflict, the warring parties continue to develop new strategies to accumulate veCRV, and the Curve War has entered a heated phase. The early history of the Curve War is detailed in the article “A Power Struggle Around Curve”.

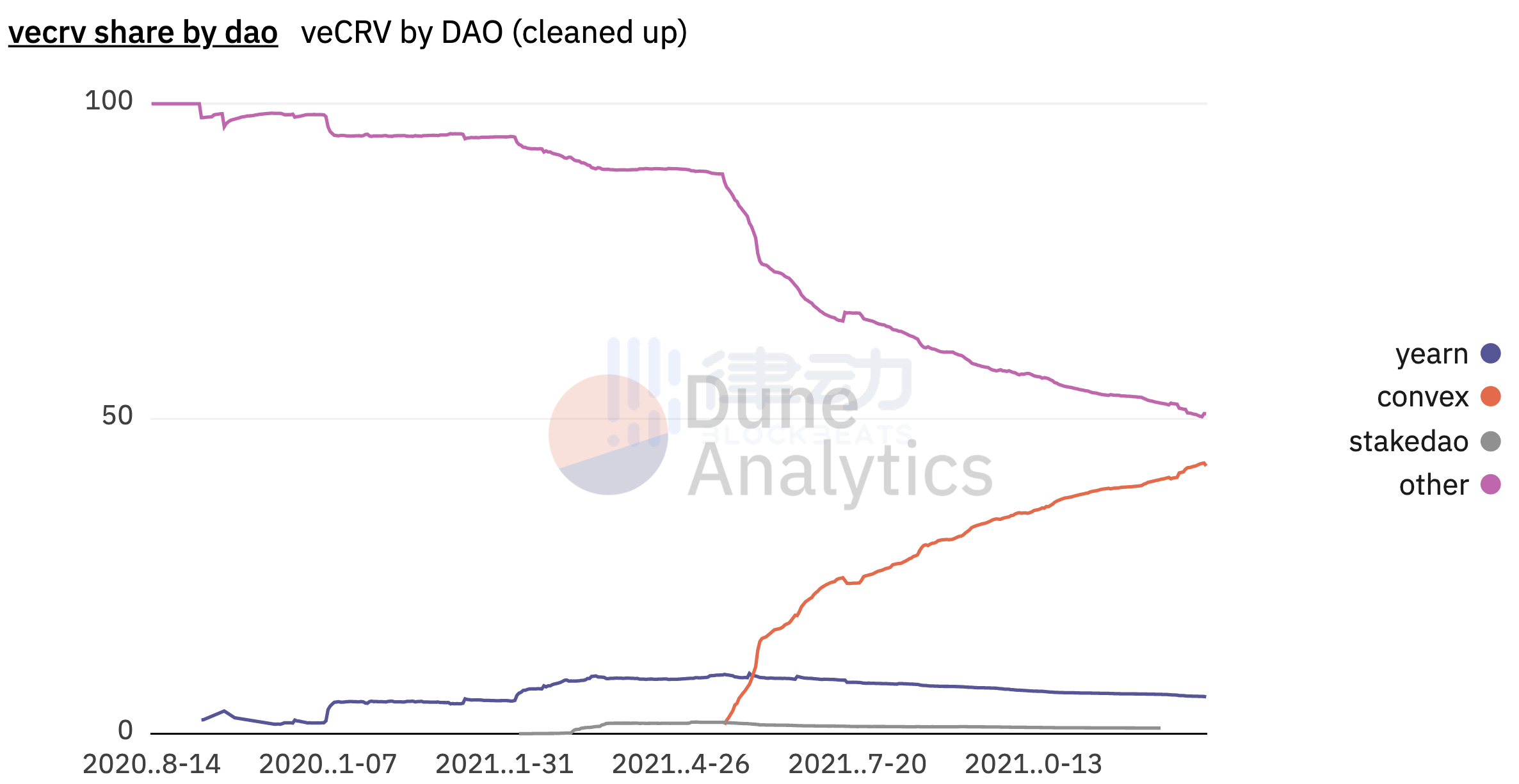

In fact, this war initially did not attract enough attention, as major participants like Yearn Finance and Stake DAO sold their CRV incentives on the market after obtaining them, which depressed the price of CRV and significantly reduced the attractiveness of the incentive mechanism. But everything changed with the emergence of Convex.

Convex: My Mercenary or the Mercenary I Hired

Convex is a DeFi protocol designed to optimize Curve's interest rates, aiming to lock as much CRV tokens as possible. CRV holders can permanently stake their tokens on Convex and receive an equivalent amount of cvxCRV as liquidity, allowing them to enjoy the same CRV incentives as veCRV holders while also earning additional CVX as a reward. The benefit for Convex is that it gains full governance rights over CRV from veCRV holders.

In just a few months, Convex successfully accumulated enough CRV and effectively determined the incentive distribution for mining pools on Curve, winning the first battle of the Curve War. However, for Convex, things are far from simple; addressing the value source issue of its governance token is also crucial.

Thus, Convex replicated Curve's model and created a nested mechanism: CVX is the governance token of the Convex platform, and by locking CVX, LPs can vote on Convex's veCRV governance decisions, meaning that controlling Convex is equivalent to controlling Curve.

More ingeniously, according to the current ratio, the protocol can acquire more gauge weight through one dollar of CVX than by directly purchasing CRV.

In the last round of Votium voting, for every dollar paid to vlCVX holders, the protocol could obtain $4.15 of CRV in its Curve mining pool. This has led to a significant increase in demand for CVX, with 142 million cvxCRV and 23 million CVX currently locked, and the value of CVX continues to rise steadily.

Additionally, Convex's token unlock schedule is also determined by the amount of CRV locked. When CRV locked reaches 500 million, the circulation of 100 million CVX will be fully unlocked, and every marginal CRV obtained by the platform after CVX emissions end will increase the CVX to CRV ratio, meaning that each CVX will increase its gauge weight for Curve's liquidity incentives.

Convex War

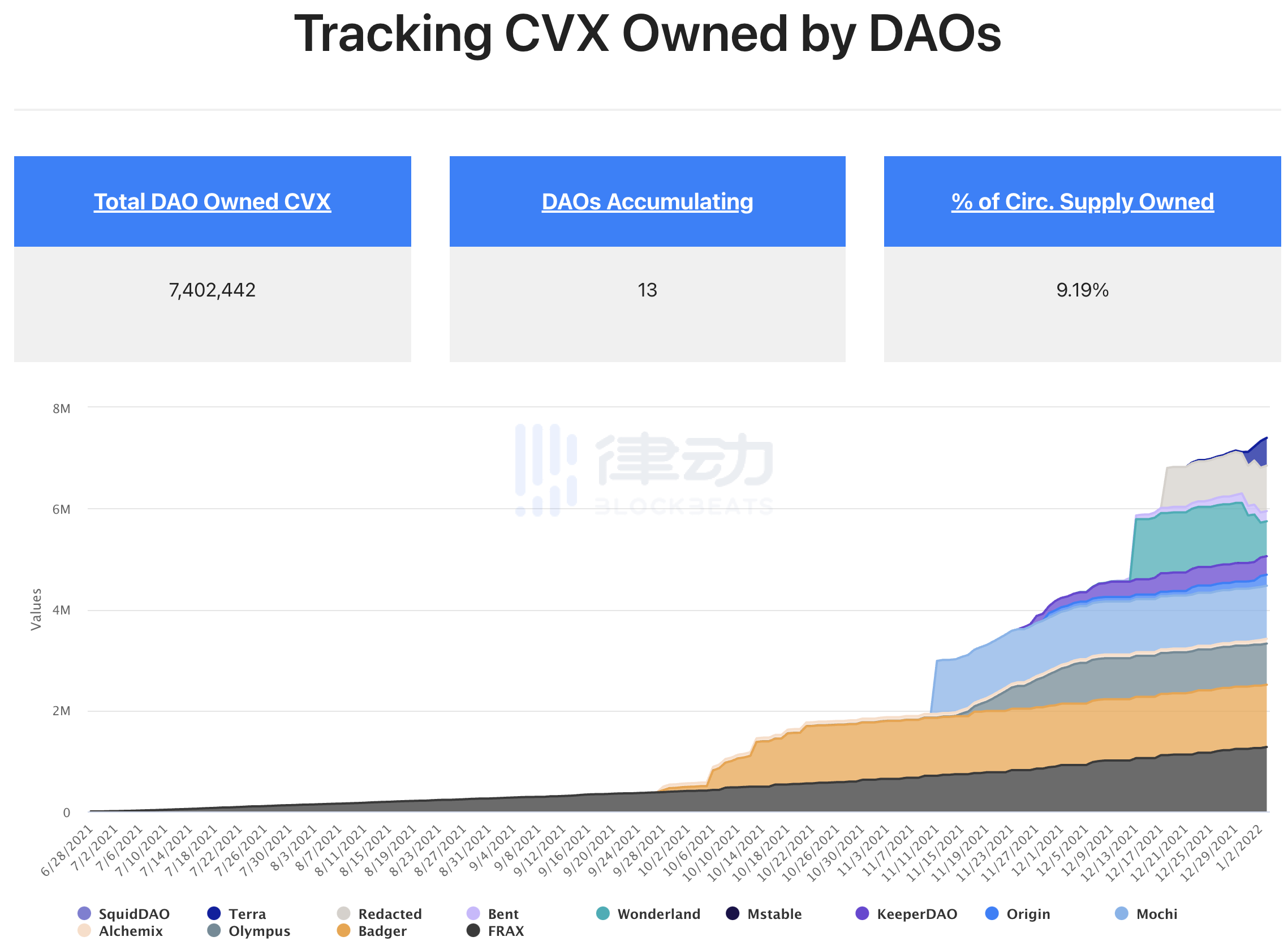

Now, to more efficiently compete for control of Curve's incentives, protocols have launched a new round of mini-wars on Convex. For stablecoin protocols like Alchemix, FRAX, Tribe, and Luna, they can obtain higher CRV incentive quotas through two avenues: bribing CVX holders or accumulating and locking CVX themselves.

Since one CVX actually controls multiple veCRV, directly purchasing CVX has become the best choice for protocols. However, the problem is that currently, less than 4% of CVX is available for purchase on exchanges (less than 4 million CVX), while the amount these protocols need to accumulate far exceeds the circulating supply. Therefore, protocols are employing various strategies to accumulate CVX in their treasuries.

Yearn Finance

Yearn's treasury also relies on providing liquidity to Curve mining pools to earn CRV rewards, but only 10% of the CRV rewards are locked by Yearn in the background to purchase more CRV, while the remaining 90% is used to reward supporting LPs. Clearly, this has caused Yearn to lose to Convex in the Curve War.

Now, Yearn has entrusted all of its veCRV to Convex in hopes of increasing the yield of its factory pools. It is important to note that this delegation does not transfer Yearn's own voting rights to Convex.

Olympus

The Olympus team also recognized the strategic importance of Curve early on. The team hopes to leverage Curve's voting power to enhance the yield of OHM treasury assets and achieve significant governance over the Curve ecosystem.

In its governance proposal OIP-43, the team proposed to increase the Olympus treasury's holdings of CVX by issuing CVX bonds. The Olympus team believes that being a pioneer in using CVX is a huge advantage: the CVX emission rate will decrease over time, making it more difficult and expensive to acquire CVX that holds equal control in the future.

Currently, Olympus DAO holds over 317,000 CVX, valued at $6.9 million.

Other Stablecoin Protocols

Protocols like Abracadabra, Frax, and Alchemix are more focused on providing "bribes" to CVX holders. In the last round of Votium voting, these projects ranked among the top: Abracadabra and Frax paid $2.23 million and $970,000 to holders, respectively, while Alchemix distributed $1.3 million in "bribes" between the alETH and alUSD stable pools.

Additionally, contracts related to the Frax development team have locked nearly 705,000 CVX; Abracadabra has also decided to allocate 5% of its weekly protocol fees to purchase and lock CVX.

The Rule-Breaking Mochi Inu

It must be acknowledged that war is rife with deceit, and there will inevitably be participants who break the rules and take advantage of the chaos. Last November, the Curve Emergency DAO discovered a protocol called Mochi Inu conducting a "governance attack" on Curve and swiftly intervened to cut off the related mining pools and their CRV incentives.

After promoting USDM as a "backed" stablecoin and joining the Curve mining pool, Mochi Inu minted $46 million of USDM using its unlimited Mochi tokens and exhausted DAI's USDM-3 pool with these USDM, purchasing a large amount of CVX with the profits obtained.

Its intention was quite clear: to control a large amount of CVX, expand the USDM-3 pool by increasing CRV incentives, thereby creating a flywheel effect. However, ultimately, due to a severe lack of collateral for USDM, the peg failed, causing significant losses for investors.

Mochi still controls about 1 million CVX tokens. Although Convex DAO has revoked Mochi's voting rights, Mochi can still earn substantial income through cvxCRV rewards in the future. Undoubtedly, this behavior contradicts the original intention of Curve's decentralization and exposes current issues within Curve.

To many, Curve has always been a protective umbrella for new stablecoins; without Curve, many protocols would struggle to establish themselves. However, it is precisely because of this role that Curve has become a target for some protocols to undermine. In the future, if the Curve ecosystem wants to strengthen and stabilize, it must address this issue.

Moat or Trojan Horse?

Unlike battlefields in the real world, blockchain has infinite space. So why do other protocols choose to besiege Curve's walls when they can build their own castles? The answer is simple— they cannot build a solid moat, as elaborated in the article “Variant Fund Co-Founder: How Web3 Applications Build Defensiveness?”.

In contrast, Curve, relying on its unique AMM structure and vast liquidity, can create a sufficiently solid application barrier. Additionally, whales, in order to gain greater voting power, will also choose longer CRV lock-up periods; currently, the voting lock-up period for CRV is 3.65 years. These advantages of Curve are difficult for other protocols to replicate, and the fact that no Curve fork can compete with it is the best evidence.

Curve has become a key infrastructure in the current DeFi space, and the protocol wars surrounding it have garnered more attention. Undeniably, by controlling a large amount of veCRV, Convex has made significant contributions to the development of the Curve ecosystem.

However, because of this, the original Curve War seems to have transformed into a Convex War, with CVX becoming the most important and sought-after role in the Curve War. Large protocols like BadgerDAO, Abracadabra, and OlympusDAO are continuously accumulating CVX in search of control over CRV incentives.

From this fundamental perspective, CVX has a higher value proposition than CRV itself: as CVX emissions gradually slow down, the intrinsic value of CVX as a "voting controller" continues to rise, prompting protocols to compete for control of Curve incentives through CVX, while CRV itself is somewhat sidelined. This inevitably leads us to ponder whether Convex is Curve's moat or a Trojan horse. Who is the true winner of this war?