Messari Research Report: How to Value Curve Finance?

Use discounted cash flow and comparable analysis to assess the profitability potential of its core AMM products.

Use discounted cash flow and comparable analysis to assess the profitability potential of its core AMM products.Author: Francois-Xavier Lord

Original Title: 《Curve Finance -- Valuation Report》

Compiled by: Dong Yiming, Chain Catcher

1. Introduction

Curve Finance is undoubtedly a pioneer in DeFi. Upon its launch, Curve disrupted the traditional market with its innovative DEX, which sparked unprecedented levels of efficiency for trading assets pegged to one another. With a clear product-market fit, the protocol was able to guide its growth by introducing its CRV governance token, bringing a robust tokenomics system into the mix.

Today, Curve's monthly trading volume exceeds $6 billion, and even more impressively, it has achieved the highest TVL among all DeFi projects, surpassing $19 billion. Nevertheless, strong competition is brewing, and many challenges still remain.

This article will introduce Curve Finance and the key metrics behind its core AMM product and CRV token.

2. About the Project

1. Overview of Curve Finance

Curve Finance was launched in January 2020, about two months after Michaele Egorov published the "StableSwap" white paper on November 10, 2019. The vision for the project stemmed from Egorov's realization that decentralized exchanges (DEXs) at the time did not provide an effective trading medium for like-kind assets.

The launch of Curve Finance aimed to solve this issue through a decentralized trading algorithm, which is optimized for low-slippage swap contracts between stablecoins or similarly valued assets (e.g., wBTC / renBTC). The protocol is designed around an automated market maker (AMM) system specifically built for low-slippage trading and stable income for liquidity providers (LPs). This is partially achieved by adopting a unique combination of constant and invariant functions.

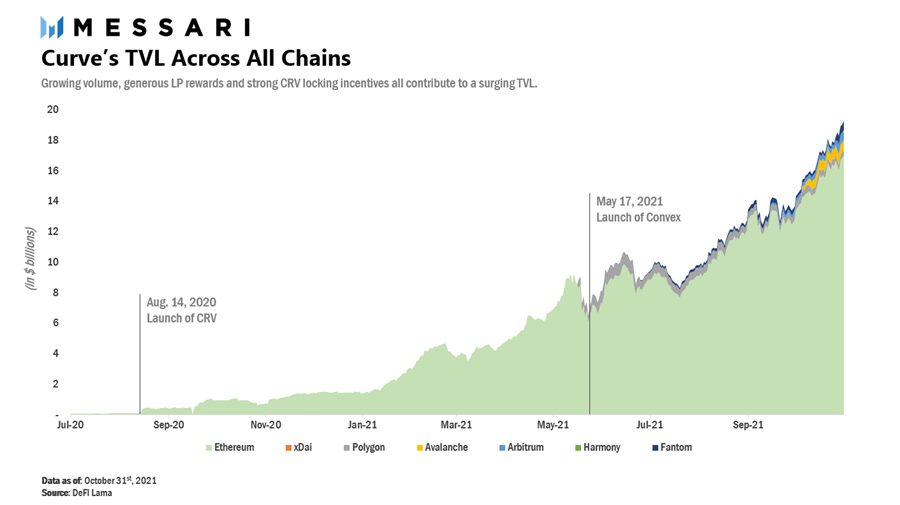

Initially, Curve had little traction in the first few days after launch, with deposits reaching $2 million and daily trading volume hitting $1 million. In August 2020, the launch of Curve's native governance token, CRV, marked a significant turning point for the protocol. In the first week following the release of its CRV token, Curve witnessed a threefold increase in its TVL, rising from $137 million to $413 million. Since then, Curve has accumulated $19 billion in TVL, making it the largest DeFi protocol in terms of deposits today.

Until recently, Curve focused solely on pegged asset trading pairs, with top mining pools dedicated to maintaining assets pegged to stablecoins, BTC, and ETH. On June 9, 2021, Egorov released a white paper for an AMM system with a dynamic pegging mechanism. This sparked Curve's expansion into non-pegged assets, known as "Curve V2."

As of this writing, Curve now offers over 40 different official liquidity pools, with some of the most popular being tricrypto2 (USDT / wBTC / WETH) and 3pool (DAI / USDC / USDT). However, it is important to note that pegged asset trading still remains the core of the protocol, accounting for the majority of daily trading volume.

2. Uses of the CRV Token

CRV is the governance token of the Curve protocol, primarily used to incentivize liquidity for the protocol. Curve benefits from increased capital as it provides more trading liquidity, thereby reducing slippage for end users.

CRV tokens can be used for voting, staking, and increasing rewards. Voting allows users to participate in community and official DAO votes. Staking enables depositors to earn 50% of all trading fees generated by the protocol. Boosting allows LPs to increase their CRV rewards by up to 2.5 times.

To access all these features, token holders need to lock their CRV in Curve to use it as voting escrow CRV (veCRV). The longer CRV is locked in Curve, the more veCRV is generated. For example, locking 1,000 CRV for one year will yield 250 veCRV, while locking the same amount for four years will yield 1,000 veCRV. Thus, the longer the lock-up period, the greater the user's voting power and rewards. This is designed to align token holders with the long-term success of the protocol.

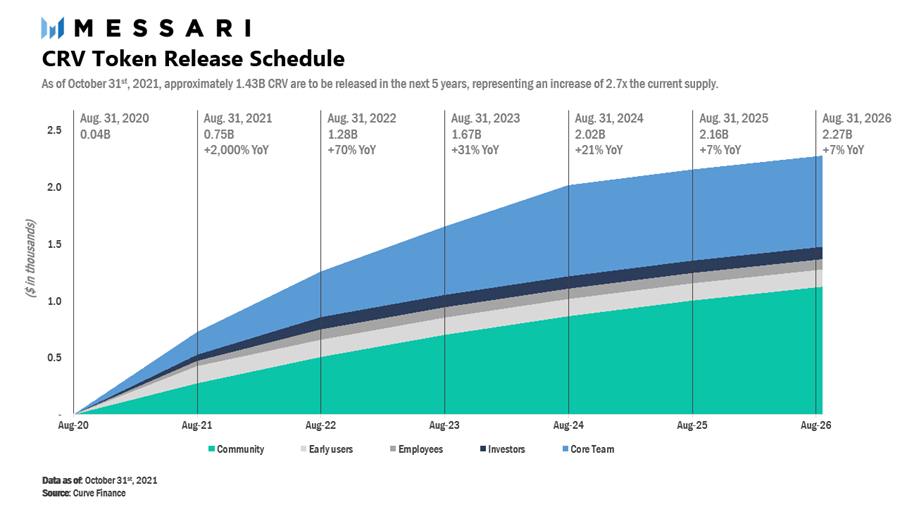

3. CRV Token Supply

Token Distribution

The initial supply of CRV at launch was approximately 1.3 billion, accounting for 43% of the total maximum supply of 3.03 billion. The initial allocation to various groups is as follows:

- 5% to pre-CRV liquidity providers, with a 1-year vesting period;

- 30% to shareholders (founders and investors), with a 2-4 year vesting period;

- 3% to employees, with a 2-year vesting period;

- 5% to community reserves.

The remaining 57% of the maximum supply will be gradually released as incentives for future liquidity providers.

Although 1.3 billion were initially supplied, due to their respective vesting schedules, the effective circulating supply of CRV at launch was zero.

From this timeline, it is clear that the inflation rate of CRV released in the coming years will significantly increase. As of October 31, only 28% of the supply was in circulation, but this number is expected to reach 2.27 billion within five years, a growth of 2,700%. Note that this is higher than Uniswap's 2,200% and Sushiswap's 13% increase in circulating supply over the same period.

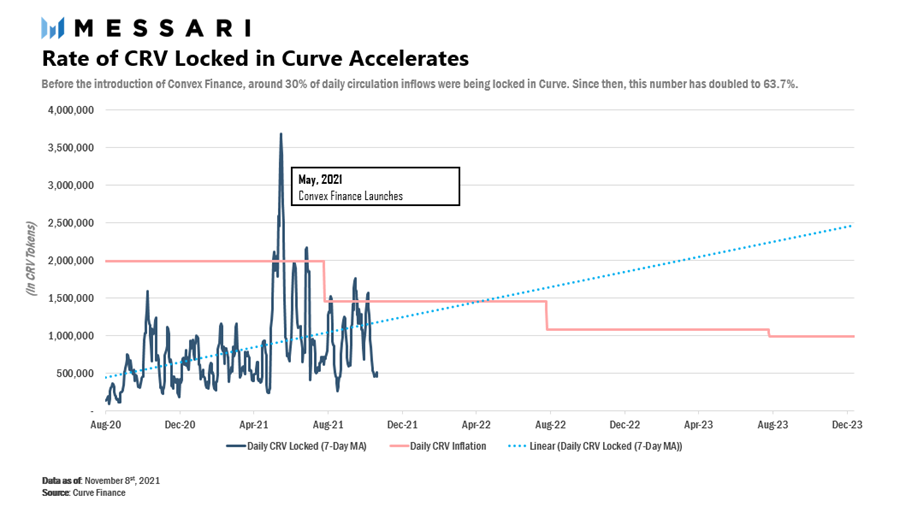

Circulating Supply and Convex Finance

Since veCRV is a non-transferable non-liquid token, the locking of CRV significantly reduces its circulating supply. At the time of writing, approximately 350 million CRV tokens are locked in Curve for voting, with an average lock-up period of 3.7 years, accounting for about 42% of the total issuance. This high locking rate of CRV tokens is partly attributed to the launch of Convex Finance in May 2021.

Convex Finance is a protocol that allows Curve liquidity providers to earn higher CRV rewards by leveraging the deposits of other CRV token holders within Convex. Deposits on Convex are irreversible. However, users receive cvxCRV tokens as deposit receipts. Unlike the non-transferable veCRV, cvxCRV has differentiated characteristics that are freely tradable. Users holding cvxCRV can earn a share of their trading fees on Curve as well as higher CRV rewards. Additionally, they can earn extra rewards in CVX (the governance token of Convex). Currently, the platform accounts for over 40% of all veCRV on Curve.

Before Convex, about 30% of the tokens issued daily to LPs were voting locked. After the introduction of Convex, this number doubled to 63.7% as the daily inflation rate gradually decreased. Therefore, Convex has only strengthened the already strong incentives for users to vote lock CRV. Thus, while inflation is expected to be relatively high, the impact on actual circulating supply should be relatively mitigated.

4. Recent Upgrades and Initiatives

Here are some notable recent updates for the protocol: - Launch on Layer 2 solution Polygon: In April 2021, Curve launched its first liquidity pool on Polygon, one of Ethereum's primary scaling solutions. This implementation aims to provide users with a cheaper alternative for asset swaps compared to the standard layer 1 mainnet. Although the Curve DAO is not on the same chain, LPs still benefit from CRV token rewards. Additionally, through collaboration with Polygon, selected Curve depositors are also eligible for MATIC token rewards.

- Curve V2: In June 2021, Curve expanded its core stablecoin AMM to non-pegged assets by introducing Curve V2 and the tricrypto pool. The new formula of the protocol retains the general form of the original StableSwap but makes some adjustments to accommodate assets with different pricing. This milestone positions Curve favorably in the broader traditional DEX market.

- Launch on Harmony: The proposal for Curve's launch on Harmony was approved in September 2021, and on October 12, Curve officially launched on the smart contract network Harmony. Note that Harmony allocated $2 million worth of ONE tokens to incentivize potential use cases for Curve on its platform.

- Other multi-chain launches: During 2021, Curve also launched on several other protocols, such as xDAI, Avalanche, Arbitrum, and Fantom. This is part of Curve's overall strategy to make the protocol as widely available as possible and to become a core building block of each ecosystem.

3. Traction

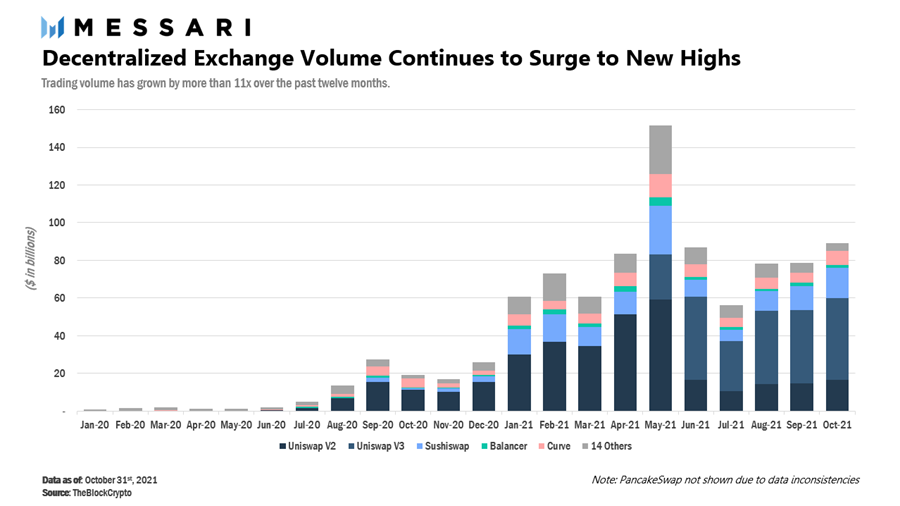

In the past 12 months, the total trading volume of decentralized exchanges has surged to $980 billion, a year-on-year increase of over 11 times.

This growth is driven by a continuous influx of capital and users into the crypto economy, along with soaring asset values, with the total market capitalization of cryptocurrencies now approaching $3 trillion.

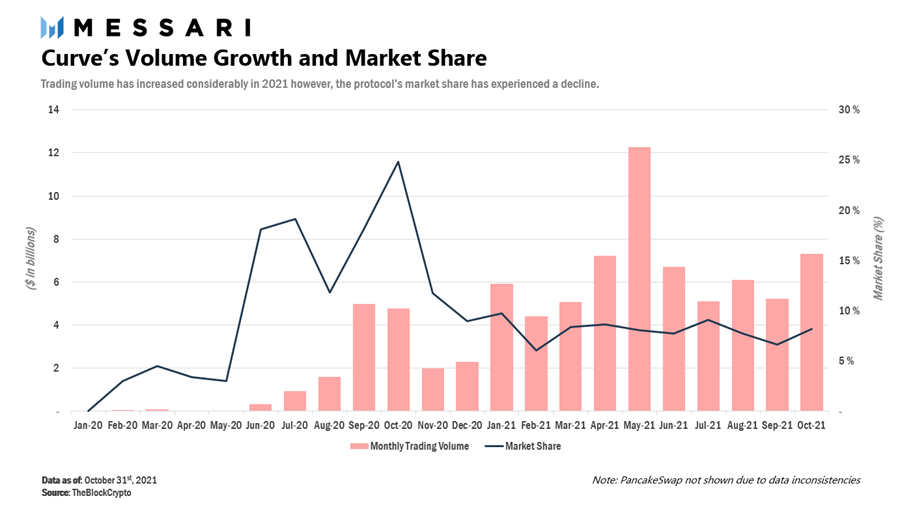

Curve has been able to capitalize on this trend, with its average monthly trading volume in 2021 increasing 3.8 times compared to 2020 (reaching $650 million), making it the third most popular DEX, with a current market share of 8%.

In addition to the growing numbers, Curve has also successfully become the most significant DeFi protocol in terms of TVL. As of October 31, 2021, Curve's TVL reached an impressive $19.3 billion, growing over 13 times since the beginning of the year.

The surge in TVL can be attributed to several factors, including increasing trading volume, generous LP rewards, strong voting lock incentives, and rising asset values. Additionally, the introduction of Curve to other protocols/scaling solutions has positively impacted this metric. As of October 31, 2021, the market capitalization of these secondary markets was approximately $2.4 billion, accounting for about 12.2% of the TVL.

4. Valuation Method

Curve can be evaluated for its core AMM product's profit potential using discounted cash flow and comparable analysis.

CRV Supply for Valuation Purposes

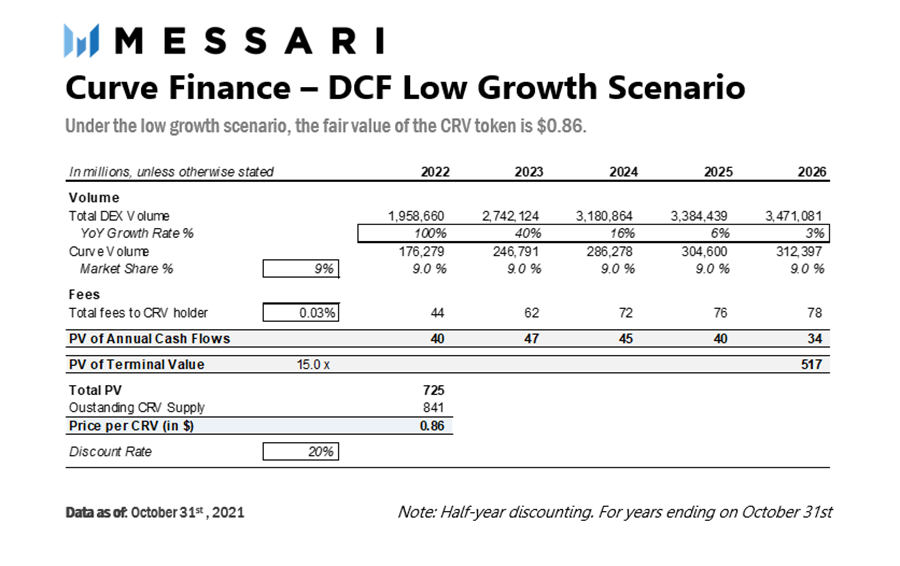

Although only voting-locked CRV tokens can generate cash flows from the protocol, the valuation is based on the total circulating supply. This is because freely floating, unstaked CRVs have the option to collect trading fees at any time. This represents an effective base of 841 million tokens as of the valuation date of October 31, 2021.

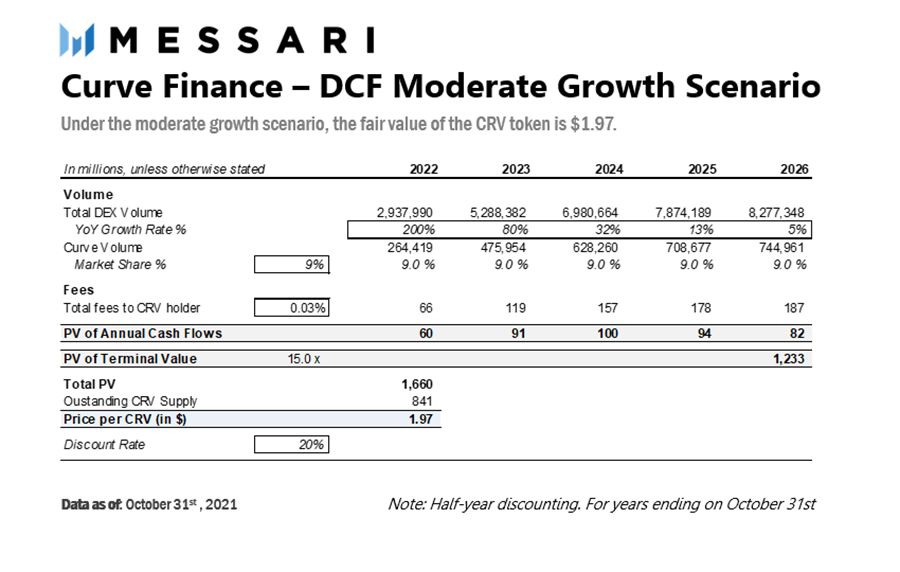

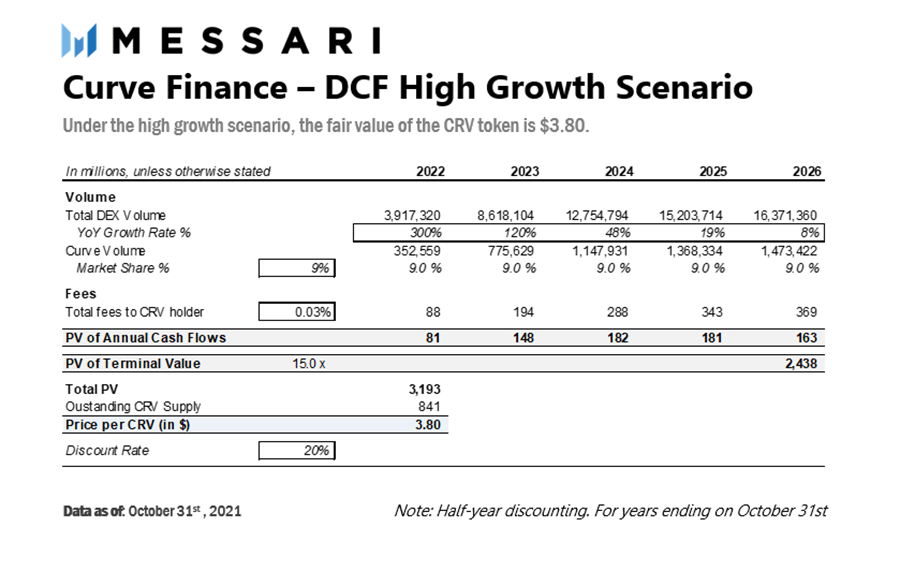

Discounted Cash Flow Model

The discounted cash flow analysis is based on the protocol's projected growth over five years. In this case, the model values the portion of cash flows attributable to token holders, which corresponds to 50% of total trading fees.

1) Projected Trading Volume

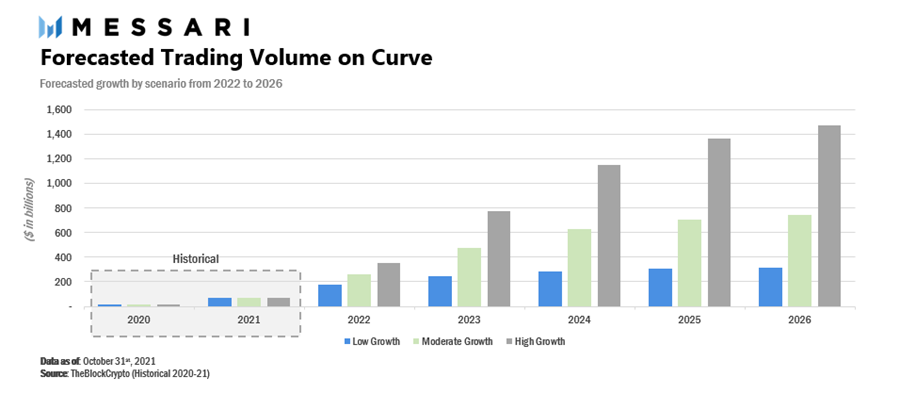

Clearly, trading volume is a key driver of Curve's value, as it directly drives the fees collected from the protocol. To provide an analysis of a range of potential CRV values under different market conditions, this report forecasts three different sales growth scenarios.

For each scenario, the total DEX trading volume for 2021 is used as a starting point. During the forecast period (2022 to 2026), the annual growth rate declines by a factor of 2.5 each year.

To obtain Curve's trading volume, the protocol is assigned a fixed market share of 9% of the total DEX trading volume. Below is a summary of Curve's projected trading volume for each scenario: - Low growth scenario: Curve's trading volume grows at a rate of 100% in 2022, gradually declining to 3% by 2026, resulting in a total trading volume of $312 billion in 2026. This scenario represents a slowdown in the growth of the crypto ecosystem and/or a decrease in overall DEX usage in favor of CEX.

- Moderate growth scenario: Curve's trading volume grows at a rate of 200% in 2022, gradually declining to 5% by 2026, leading to a total trading volume of $744 billion in 2026. This scenario implies continued growth in DeFi and/or an increase in trading adoption on L2s/other smart contracts.

- High growth scenario: Curve's trading volume grows at a rate of 300% in 2022, gradually declining to 8% by 2026, resulting in a total trading volume of $1.47 trillion in 2026. This would represent extremely optimistic growth for Curve. For example, this scenario could represent the successful implementation of ETH 2.0, which would significantly lower gas prices and trigger a major shift from CEX to DEX.

To provide a more intuitive perspective: the total trading volume of all DEXs over the past 12 months has reached approximately $979 billion, with Curve's share being $69.7 billion. Additionally, the total trading volume of the world's largest centralized exchange (CEX), Binance, exceeded $7.7 trillion in 2021. At the time of writing, DEXs account for approximately 7% to 9% of the total trading volume of CEXs.

Below is a visual representation of Curve's projected trading volume under each growth scenario: (blue for low growth scenario, green for moderate growth scenario, gray for high growth scenario)

2) Discount Rate

The discount rate used for cash flows from 2022 to 2026 is set at 20%, based on the perception of the protocol's risks and progress to date. At the end of the forecast period, a 15x exit multiple is applied to the projected free cash flows for 2026, consistent with the P/E ratios of publicly listed traditional exchanges.

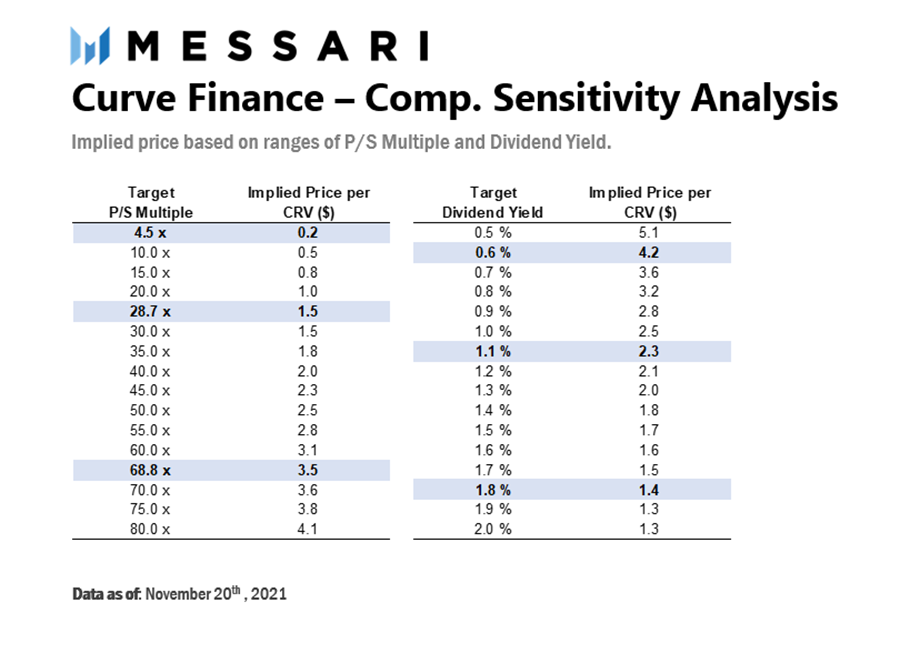

Comparable Analysis

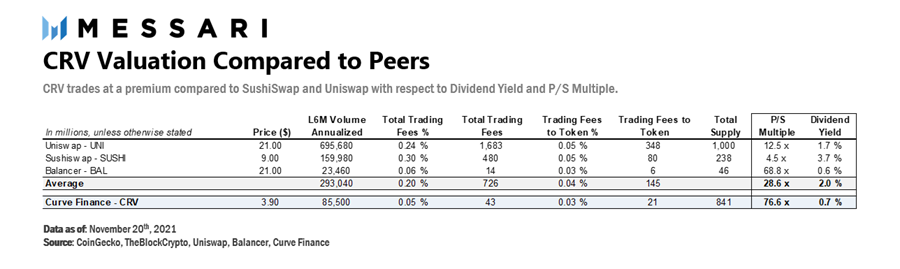

This report compares the valuation of Curve Finance with some of its closest competitors: Uniswap, Sushiswap, and Balancer. The metrics evaluated for each project are price-to-sales (P/S) ratio and dividend yield.

1) Price-to-Sales Multiple

The price-to-sales multiple is based on the total trading fees generated by each protocol from their trading volume. This includes the portion paid to liquidity providers and the portion paid to token holders.

The annual trading volume used is derived from annualizing the trading volume of each project over the past six months. This is done to provide a more current perspective given the rapid growth of DEXs over the past year.

The estimated weighted average trading fees are applied to the trading volume based on recent protocol activity. Uniswap uses a rate of 24 bps, Sushiswap 30 bps, Balancer 6 bps, and Curve 5 bps (see model source).

2) Dividend Yield

The dividend yield represents the direct cash flows generated by the protocol attributable to token holders. This metric is calculated by dividing the annualized trading fees for token holders by the total market capitalization. The percentage applicable to trading volume varies by project. - For Curve, half of all trading fees belong to veCRV holders, equivalent to 2.5 bps.

- For Sushiswap, 5 bps of trading volume is paid to xSushi holders.

- For Uniswap, the protocol currently does not pay a portion of fees to token holders, but UNI governance can choose to enable this feature. Therefore, for the purposes of this analysis, it is assumed that 5 bps of protocol fees are paid to UNI holders, similar to Sushiswap.

- For Balancer, the protocol also currently does not pay a portion of fees to token holders, but governance may vote to introduce protocol fees. For the purposes of this analysis, the same rate as Curve is applied due to the similarities between the two projects.

3) Benchmarking Results

From the table above, it is evident that Curve's trading price has a significant premium in terms of price-to-sales multiple. This is partly due to its significantly lower fee structure based on trading volume compared to Uniswap and Sushiswap (5 bps vs. 30 bps).

In terms of dividend yield, Curve's trading price is lower than that of Uniswap and Sushiswap, which can also be explained by the lower trading volume token fees. Note that when lowering the rates of UNI and SUSHI to match Curve, their dividend yields drop to 0.8% and 1.9%, respectively.

Curve's trading appears consistent with Balancer, and both protocols have very similar fee structures and products.

5. CRV Token Valuation

Discounted Cash Flow Analysis

Below are the DCF analysis results for each of the three scenarios:

According to the DCFs, the fair value of CRV is $0.86 in the low growth scenario, $1.97 in the moderate growth scenario, and $3.80 in the high growth scenario. At equal weighting, the average target price per CRV based on the present value of expected cash flows for token holders is $2.21. Readers can adjust the model based on their estimates.

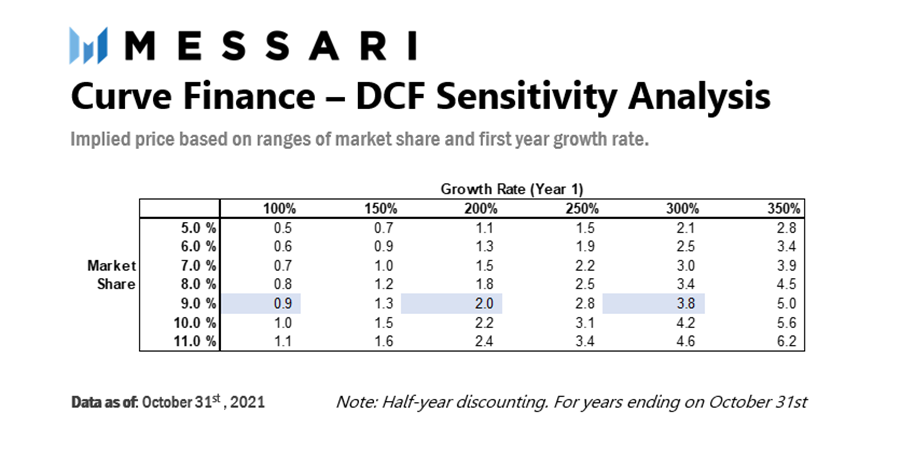

DCF Valuation Sensitivity Analysis

The table below lists various implied values for CRV based on a range of market shares and first-year growth rates. The scenarios used in the above valuation model are highlighted in blue.

Comparable Valuation Sensitivity Analysis

The table below shows the range of implied values for CRV based on a set of P/S multiples and dividend yields. The scenarios used in the valuation are highlighted in blue.

CRV Valuation Premium

Based on the valuation methods detailed in this report, Curve's trading appears to be highly premium. Below are some potential explanations the market may consider when evaluating CRV: - Limited circulating supply: At the time of writing, approximately 42% of the issued supply of CRV is locked in Curve for voting, with an average lock-up period of 3.7 years. This significantly reduces the number of CRVs in circulation, which, given current demand, may lead to a higher price per CRV. However, note that the introduction of Convex mitigates this effect, as cvxCRV tokens can be freely transferred while veCRV cannot.

- Demand for voting rights: Due to token holders' ability to vote on liquidity reward allocations, there is strong demand for CRV, with many competing stakeholders vying for control over incentive distributions. The demand for this purpose has become so significant that it has even led to the monetization of veCRV voting rights. In fact, in August 2021, Yearn's founder Andre Cronje launched a voting bribery platform that allows token holders to receive compensation for supporting specific weight standards. For example, veCRV holders can earn a certain amount of MIM, FTM, or CREAM by allocating their voting power to pools corresponding to these protocols. This illustrates the undeniable value and immense demand associated with the voting rights of the CRV token.

- Boosting features: As indicated by Curve's very high TVL relative to its trading volume, it is clear that the community values Curve's token rewards more than its core trading fees. This report does not emphasize the boosting and voting features used by CRV to gain additional liquidity rewards. However, they may represent the most significant driving force behind the current demand for CRV.

- Third-party token rewards: Through collaborations with other protocols, many mining pools on Curve offer additional token rewards. This leads to higher APYs for liquidity providers and may represent a valuable competitive advantage.

- Community fund: The initial allocation of CRVs allows for approximately 150 million CRVs to be reserved for community-led incentives. Currently, this account holds about 124 million CRVs, valued at approximately $479 million.

6. Competition

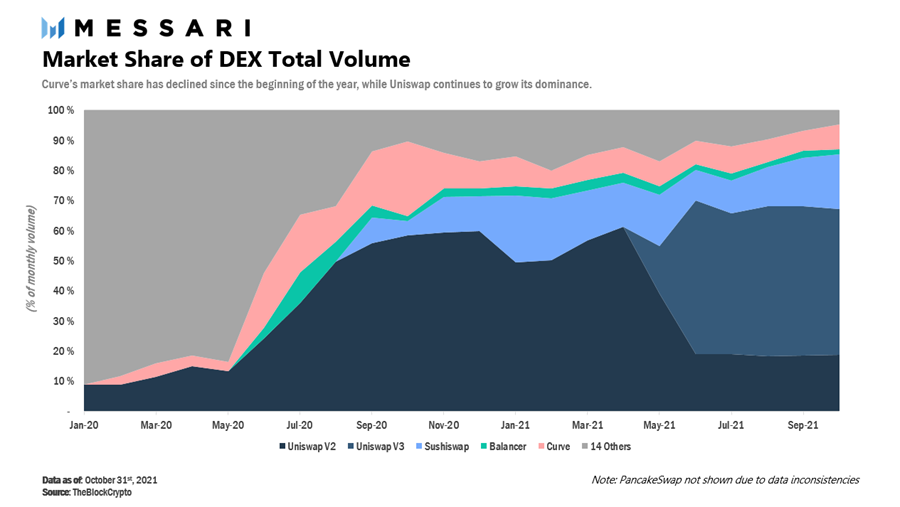

The DEX market has made significant progress over the past year, and competition continues to intensify. Below is the evolution of market shares among the top competitors in the field:

In terms of the percentage of total volume, Curve's market share declined in 2021, dropping from around 10% in January to 8% in October. In contrast, Uniswap continued to expand its dominance in the field, increasing its market share from 49% to 67% during the same period, an increase of 18%.

While Uniswap, as the most mature and widely used DEX, certainly benefits from its network effects, much of this continued success can be attributed to the technological innovations brought by the Uniswap V3 protocol. This new iteration of Uniswap was launched on May 15, 2021, introducing the concept of concentrated liquidity, allowing LPs to create markets within customized price ranges. Since deposits are deployed in the most commonly used portions of the asset pricing curve, this targeted liquidity provision approach (similar to Curve) allows for higher capital efficiency. Thus, it enables Uniswap to compete directly with specialized DEXs like Curve that target narrower price ranges.

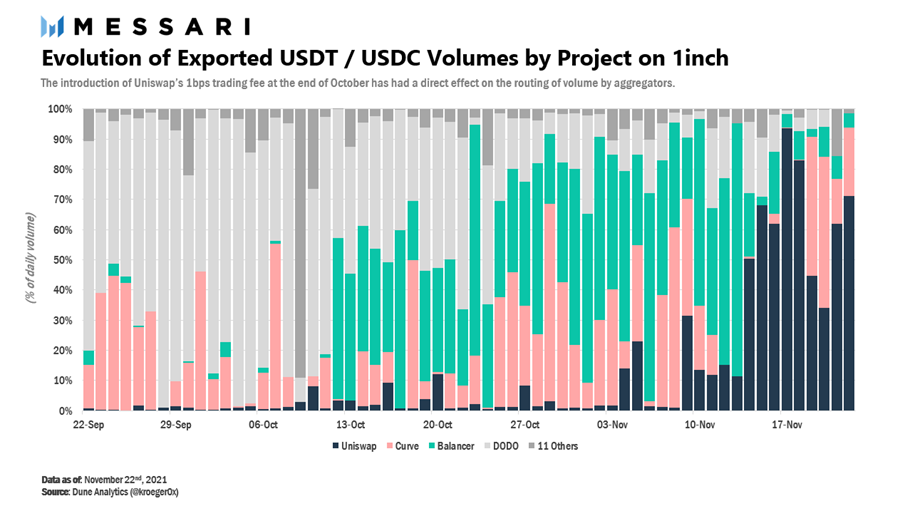

Additionally, on October 29, 2021, Uniswap increased its fee tier by 1 bps in a unanimous vote, allowing the protocol to compete more effectively on stablecoin trading pairs with lower fees. This is clearly reflected in the trading volume of USDC / USDT on the 1inch DEX aggregator, which seems to have a direct impact on the volume on that platform.

In October, Uniswap's average share of stablecoin trading volume was 2.6%. After this measure was implemented, its share rose to over 50% in recent days. This example highlights the fiercely competitive nature of the stablecoin trading market—platform profits are thin, and users are price-sensitive.

Thus, Curve faces strong competition from other DEXs like Uniswap, which are continuously innovating to provide higher efficiency and better pricing.

7. Risks

Here are some of the main risks that Curve Finance faces in the medium to short term: - Intensifying competition: As mentioned in the previous section, one of the biggest risks Curve faces is the increasing competition from other DEXs. As Curve attempts to challenge others in non-pegged asset trading through the introduction of Curve V2, competitors like Uniswap are improving their protocols to compete more effectively in non-pegged asset trading pairs and stablecoins.

- Relatively high inflation: The release supply of CRV will increase by 2.7 times over the next five years. While these rewards are necessary to attract and retain liquidity, they are far higher than the expected inflation of Uniswap and Sushiswap. This will inevitably have a dilutive effect on token holders. However, note that this risk can be partially mitigated by increasing CRV voting lock on Curve.

- Governance: Since veCRV holders have the right to vote on liquidity rewards, many users and groups are attempting to purchase large amounts of CRV equity to increase incentives for selected pools. This has the potential to be detrimental to the Curve ecosystem, as token rewards shift from high-capacity pools to other less relevant pools. Recently, the controversial stablecoin protocol Mochi utilized this feature to launch a governance attack on Curve. This required the protocol's developers to activate an emergency DAO to reduce rewards for Mochi to prevent a spiral feedback loop.

8. Conclusion

Curve's robust tokenomics leverages the protocol's reward system, driving user demand for CRV, which has led to a surge in its TVL over the past year. However, on the other hand, despite the growth in trading volume, the protocol is experiencing strong competitive resistance on its core AMM product and is currently losing market share to competitors like Uniswap. This situation highlights the apparent disconnect between the cash-generating potential of the protocol's core AMM product and its current trading price.

Nevertheless, with the introduction of non-pegged asset trading and multiple integrations with scaling solutions and emerging smart contract protocols, Curve has demonstrated its willingness to continue innovating and remain at the forefront of the rapidly evolving DeFi ecosystem.