The Secret of the Largest Liquidity Center in DeFi: Analysis Report on the Yield Aggregator Convex

Curve is the largest decentralized exchange in DeFi.

Curve is the largest decentralized exchange in DeFi.Source: The Muse Museum

Convex Finance launched on Ethereum on May 18, 2021, and its platform token CVX was listed on Binance yesterday. As of today, it has become the undisputed leader in the DeFi yield aggregator space with a total locked value (TVL) of $18.2 billion (the second place, Yearn Finance, has a TVL of only $5.6 billion). Achieving such success in just six months is closely tied to its backing by the Curve platform, but the key lies in Convex's perfect solution to the binary paradox in traditional finance—"under the premise of unchanged risk, asset liquidity and yield are often mutually exclusive." The financial innovation story of Convex Finance begins with the decentralized exchange Curve.

What is Curve?

Curve is the largest decentralized exchange in DeFi, primarily optimized for low-slippage trading between "similar assets," with a total locked value exceeding $20 billion and daily trading volumes in the hundreds of millions on Ethereum and Polygon. Similar assets refer to assets that have the same price, whether they are stablecoins pegged to the US dollar or different variants of the same asset, such as BTC and wBTC. At the same time, Curve has integrated lending protocols and synthetic asset protocols like iEarn, Compound, and Synthetix, providing additional yields to liquidity providers while improving capital utilization. This Lego-like financial combination is one of the great attractions of DeFi.

What has made Curve the No. 1 in DEX?

Let’s consider what issues users face when using DEX for asset exchanges or as liquidity providers for dual-token mining. Undoubtedly, users care more about asset trading slippage and transaction fees; as liquidity providers, the market-making mechanism of DEX can lead to impermanent loss due to unilateral price fluctuations, which can severely erode the profits from liquidity mining.

The three points mentioned above—slippage, transaction fees, and impermanent loss—become even more intolerable in stablecoin exchange scenarios. The trading volume of stablecoins is often larger, people are more sensitive to transaction fees, and it is hard to accept that 1 USDT can only be exchanged for 0.9 USDC. (Impermanent loss refers to the losses incurred from participating in dual-token mining compared to simply holding the tokens when prices fluctuate, essentially involving selling when prices rise and buying when they fall, rather than being a true loss.)

The importance of stablecoins in the DeFi ecosystem is self-evident; the development of stablecoins complements the growth of the DeFi ecosystem. With the rise of new public chains, the variety of stablecoins such as USDT, USDC, DAI, UST, and similar assets like BTC/WBTC and ETH/stETH is increasing, leading to a growing demand for exchanges between different types of stablecoins and similar assets.

Curve adopts an innovative AMM model (combining constant product market makers and constant sum market makers), initially focusing on the niche of stablecoin exchanges, achieving large-scale and low-slippage token swaps. Due to the scale of trading volume, Curve can offer a low transaction fee of 0.04% (compared to Uniswap's 0.3%), and the low slippage in exchanges translates to extremely low impermanent loss risk for liquidity providers.

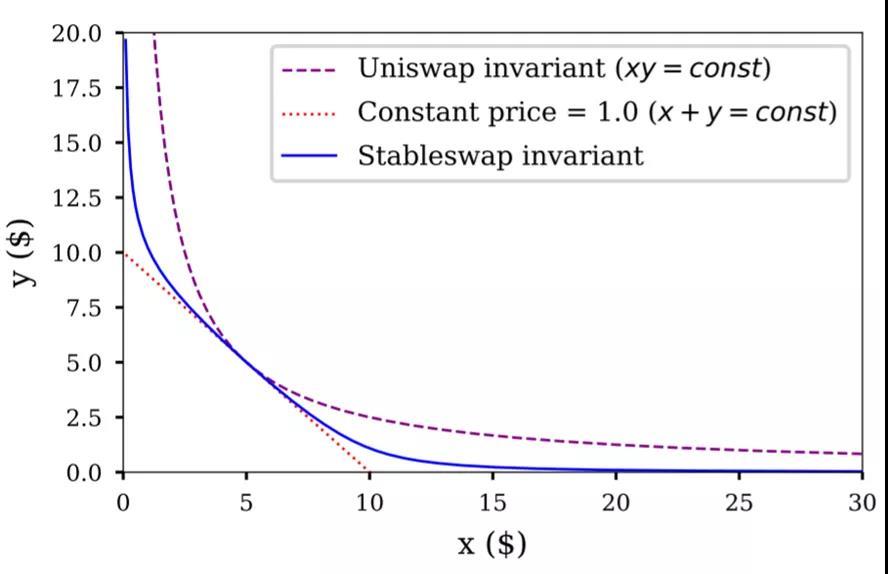

We analyze the innovation of Curve's AMM model. In the diagram (below), the coordinates represent the ratio of two assets in the pool, and the slope reflects the current asset exchange ratio, i.e., asset price. It is visually evident that xy=const is a hyperbola, and as x changes, the slope continuously changes. To maintain a relatively stable asset price, extremely deep liquidity is required, which is very difficult to achieve in practice. On the x+y=const curve, although the slope is equal everywhere, there is a risk of one asset being completely consumed, leading to liquidity exhaustion.

Curve's AMM model, known as Stableswap invariant, balances the advantages and disadvantages of both approaches, achieving relative stability in asset exchange prices over a larger range while ensuring that the asset pool does not run out of liquidity. (Curve incentivizes the composition ratio of assets in the pool to approach a balance point, avoiding excessive deviation from the equilibrium position. For example, assets deposited below the balance ratio and those withdrawn above the balance ratio will receive higher yields.)

(n represents the number of assets (in this case, n=2), and A is a "scaling factor" parameter that determines how similar the function is to the constant product function. The lower the value of A, the closer Curve's function is to Uniswap's function.)

Source: Curve White Paper

Curve's Token Economic Model

CurveDAO officially launched on August 13, 2020, introducing the governance token CRV. The maximum supply of CRV is 3.03 billion tokens, of which 62% will be allocated to community liquidity providers, 30% to the project team and early investors (with a vesting period of 2-4 years), 5% as community reserves, and 3% to employees with a 2-year vesting period.

Distribution of released CRV, Source: Curve Official

CRV currently has three main uses: community voting, staking to earn community governance fee shares, and increasing liquidity pool yields (up to 2.5 times). The prerequisite for achieving these uses is to lock CRV and obtain veCRV. Compared to conventional DAO-governed DEX protocols, Curve's innovation lies in adding a time function to the CRV locking rules: veCRV=CRV*T/4 (where T is the locking period in years), meaning the longer CRV is staked, the more veCRV one receives; to obtain a 1:1 ratio of veCRV, CRV must be locked for 4 years. It is important to note that this staking behavior is irreversible and veCRV is non-transferable.

It is not difficult to see that in Curve's customized usage rules, high mining yields and community governance fee sharing are what users want, while the irreversibility of CRV locking is what users dislike. This creates a conflict between liquidity and yield; to achieve higher yields, one must sacrifice current liquidity. This situation seems reasonable, but must it really be this way?

Convex says "NO!"

According to its official website, Convex is a yield aggregator dedicated to simplifying the use of Curve, but simplifying the operational process alone is not enough to leave other yield aggregation applications behind. Its true value lies in solving the problem of liquidity and yield being mutually exclusive in the Curve protocol and providing higher yields than the Curve protocol for users with small amounts of capital, ultimately allowing small contributions to accumulate into significant results!

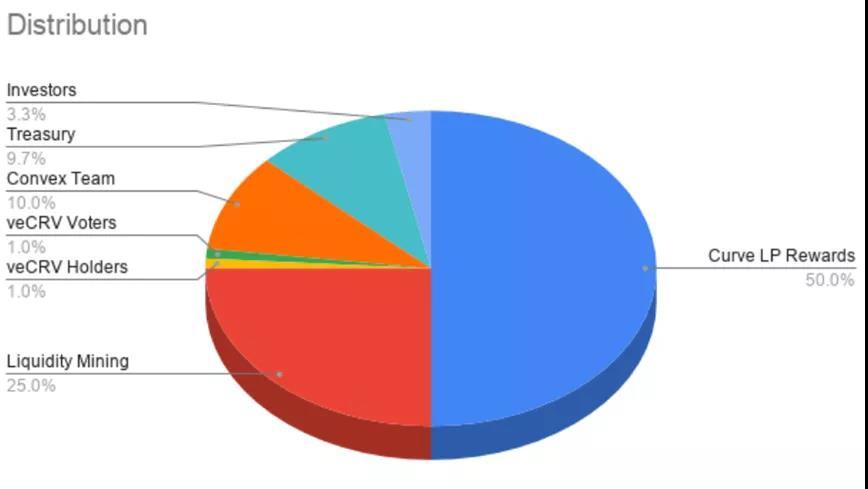

But what is intriguing is how Convex achieves this. First, let’s look at Convex's token economic model. The protocol token of Convex is CVX, with a maximum supply of 100 million, of which 50% will be allocated to users providing liquidity to the Curve platform through the Convex platform (enhancing returns for initial liquidity providers), 25% for liquidity mining incentives in CVX/ETH and cvxCRV/CRV pools (the establishment of these pools significantly improves the liquidity of cvxCRV, one of the means by which Convex addresses the liquidity shortage of veCRV), 10% to the Convex team, 9.7% to contracts, 3.3% to early investors, and 2% airdropped to veCRV holders.

CVX distribution rules, Source: Convex Official

cvxCRV is essentially a mapping of veCRV on the Convex platform, which can be obtained by staking CRV on the Convex platform, and staking one CRV yields one cvxCRV, eliminating the time function of veCRV. The underlying reason is that the Convex protocol chooses to lock all CRV on the Curve platform for 4 years, which is often difficult for individual users to bear.

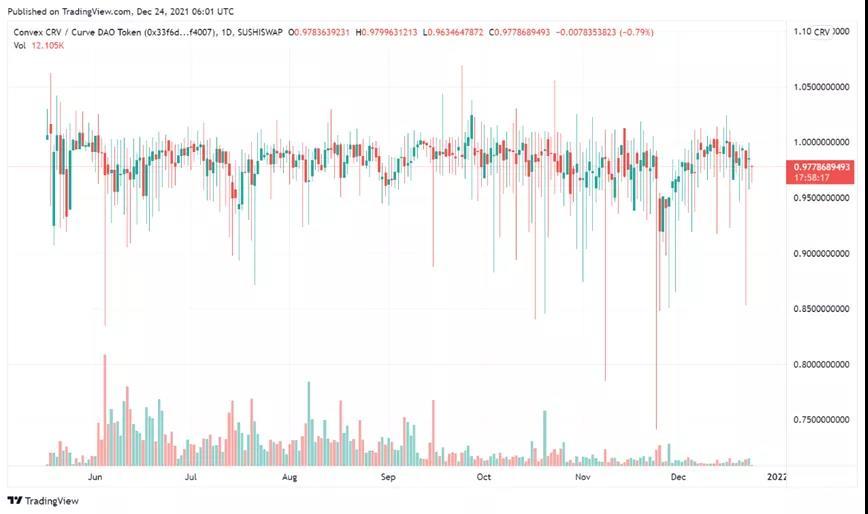

At the same time, the Convex protocol itself allows for the circulation of cvxCRV and uses its own protocol token CVX as an incentive, creating a liquidity mining pool for cvxCRV/CRV, significantly improving its liquidity. On SushiSwap, cvxCRV can be exchanged for CRV at nearly a 1:1 ratio. This process is somewhat similar to asset securitization, transforming inherently illiquid assets (veCRV) into highly liquid securities (cvxCRV), with Convex playing the role of a bank.

cvxCRV/CRV maintains a basic 1/1 ratio, Source: SushiSwap

To summarize, as a rational holder of CRV tokens, there are four choices. First, simply hold CRV and wait for the price to rise; second, go to Curve to stake CRV for veCRV, gaining voting rights and management fee shares from the Curve protocol but sacrificing liquidity; third, go to Convex to stake CRV for cvxCRV, allowing one to enjoy the highest yields and CVX without sacrificing liquidity, although a 16% fee will be charged on accelerated yields; fourth, go to SushiSwap to provide liquidity, earning SUSHI, transaction fee shares, and CVX incentives. The third and fourth choices are based on the Convex platform.

Four choices for CRV holders and their corresponding yields

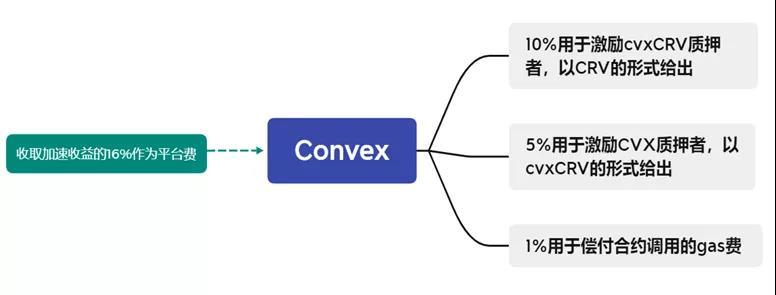

We attempt to delve deeper into the reasoning behind the successful operation of the Convex model, which fundamentally cannot be separated from the price support of CVX. If the price of CVX drops too low, the yield from the third choice will decline, and the decrease in liquidity mining yields on SushiSwap may trigger a liquidity shortage for cvxCRV. Therefore, the Convex protocol still needs measures to reduce the circulating supply of CVX and cvxCRV—Convex charges a 16% fee on accelerated yields as a platform fee and uses this as a basis to incentivize CVX and cvxCRV holders to stake their tokens.

However, the advantages of the Convex protocol are not limited to the improvement of liquidity for cvxCRV compared to veCRV. The Convex protocol can also aggregate funds to enhance liquidity yields in Curve. This is easy to understand; small retail investors cannot obtain enough veCRV to increase liquidity pool yields, and Convex once again plays the role of a bank, pooling scattered funds to concentrate efforts on "big projects," allowing users to enjoy accelerated yields without even needing to lock CRV.

16% of the platform fee is mainly used to incentivize stakers of cvxCRV and CVX

By addressing the pain points of using Curve, the Convex protocol has attracted an increasing number of users, while the emergence of Convex will also promote a continuous increase in the amount of CRV locked. The optimistic expectations for the price of CRV will further boost user numbers. The positive feedback loop between Convex and Curve has established its strong competitiveness in the stablecoin exchange space, with a TVL of $18.2 billion indicating that it has become an important source of yield in the DeFi ecosystem, but the attempts of "financial geeks" do not stop here.