First-Class Cabin: A Detailed Explanation of the Product Mechanism and Economic Model of the DeFi Lending Protocol Alchemix

The highlight of Alchemix's design is the self-repayment of debt supported by future earnings to enhance returns; the project is currently collaborating with multiple ecosystems to enrich the protocol's gameplay.

The highlight of Alchemix's design is the self-repayment of debt supported by future earnings to enhance returns; the project is currently collaborating with multiple ecosystems to enrich the protocol's gameplay.Author: First Class Warehouse

Alchemix is a lending platform backed by future earnings, enabling self-repaying debt with no liquidation risk. The main purpose of the protocol is to enhance yields, and current business data shows promising performance.

Investment Overview

Alchemix Finance is a synthetic asset lending platform supported by future earnings, allowing for self-repaying debt and no liquidation risk, which is a highlight of the protocol's design. The principle is that users deposit assets into yield aggregation protocols for farming, and future earnings are tokenized in the form of synthetic assets called alToken. The protocol automatically deducts the user's incurred debt when earnings are returned; the alToken borrowed by users is pegged 1:1 with collateral, significantly reducing the impact of market price fluctuations and eliminating potential liquidation risks for collateral.

From a product business logic perspective, the main use of Alchemix is yield enhancement, achieved in two ways: first, by lending assets to increase user capital leverage; second, by accelerating pool earnings through the Transmuter redemption mechanism. The key to driving Transmuter’s yield acceleration is the value of alToken. The more diverse the application scenarios for alToken, the higher its value, leading to more funds deposited in the Transmuter; conversely, if alToken lacks mining or other application scenarios, the assets in the Transmuter will be completely exchanged. Therefore, the attractiveness of Alchemix products is closely related to the application scenarios of alToken.

The Alchemix team members are anonymous, but based on the backgrounds of the founders and initial financial supporters, they are likely seasoned professionals in the DeFi space, familiar with DeFi mechanics, which is a positive human resource for the protocol's development. Recently, Alchemix has gained developmental benefits by deeply participating in the Curve ecosystem, accelerating the growth of protocol assets, which also reflects the foresight of the team and community decisions.

Alchemix is currently collaborating with multiple ecosystems to enhance the protocol's competitiveness. From the perspective of ecosystem development, it can enrich the protocol's gameplay and allow for more efficient utilization of user funds, which is an advantage brought by DeFi Lego. However, these protocols have only recently launched and have not yet been tested by the market, so there are still significant risks involved.

In summary, Alchemix is worth paying attention to.

Note: The final evaluation of [Attention]/[No Attention] by First Class Warehouse is based on a comprehensive analysis of the project's current fundamentals according to the First Class Warehouse project evaluation framework, rather than a prediction of the future price fluctuations of the project token. There are many factors that influence token prices, and project fundamentals are not the only factor. Therefore, one should not assume that a project marked as [No Attention] will necessarily see its price drop. Additionally, the development of blockchain projects is dynamic; if a project we have marked as [No Attention] undergoes significant positive changes in its fundamentals, we may adjust it to [Attention]. Conversely, if a project we have marked as [Attention] experiences significant negative changes, we will alert all members and may adjust it to [No Attention].

Basic Overview

Project Introduction

Alchemix Finance is a synthetic asset lending platform supported by future earnings, helping users access future deposit earnings in advance by creating synthetic asset tokens. In other words, users can use 100% of their principal to farm yields on other DeFi protocols while also borrowing some funds for other investments, thereby leveraging their earnings.

Basic Information

Source: Coingecko

Project Details

Team

The Alchemix team is anonymous and was built by a developer known as Scoopy Trooples, who currently serves as a co-founder of Alchemix. Their Twitter bio states: "Tech and futurism enthusiast." They have 56,000 Twitter followers, indicating a small but notable social influence.

Figure 2-1 Scoopy Trooples Twitter Account

Andre Cronje (AC), the founder of Yearn and a crypto "weather vane," has tweeted in support of Alchemix and provided much feedback to the team. As a result, the project is viewed by social media users as part of the "AC system," bringing it some popularity.

Figure 2-2 Scoopy Trooples' Tweet

Funding

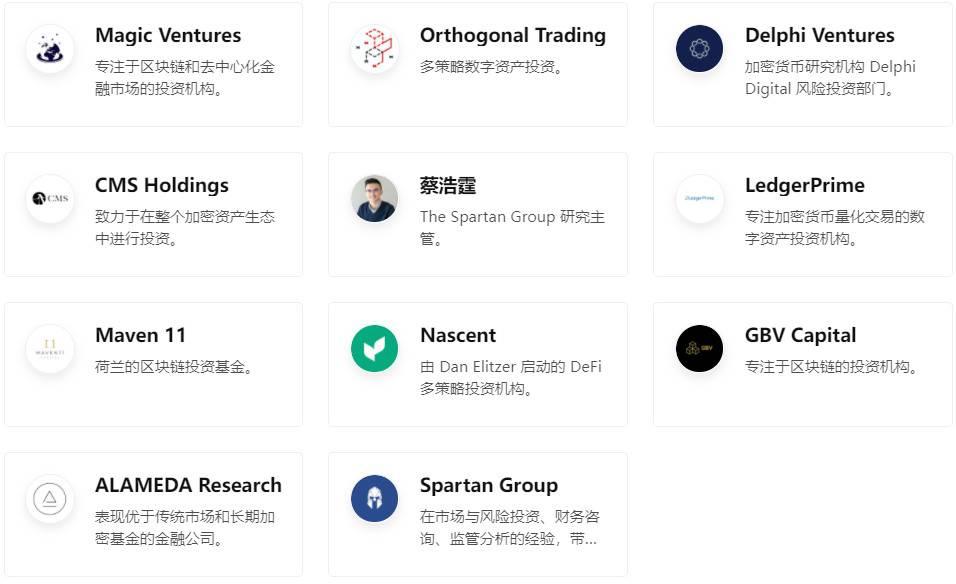

Seed round investors include eGirl Capital, DCV (DeFi Chads Ventures), and Weak Simp Capital, with specific investment amounts unknown. eGirl Capital originated from Twitter, with a diverse team that is mostly anonymous and has a certain level of crypto recognition, coming together due to a shared taste for memes and crypto culture. Confirmed identities in the fund include Eva Beylin, a board member of The Graph fund, and Alchemix founder Scoopy Trooples is likely also a member of eGirl Capital.

Figure 2-3 Seed Round Investors

- On March 14, 2021, Alchemix announced it raised $4.9 million, led by CMS Holdings and Alameda Research, with Immutable Capital, Nascent, and others participating, at a cost of $700/token, with an estimated total sales volume of 7,000 tokens;

- On March 18, 2021, Alchemix raised another $3.1 million in strategic financing, led by the investment department of the crypto consulting firm Spartan Group, with Delphi Ventures, Nascent, CMS Holdings, Maven 11, and Genesis Block Ventures participating.

The two rounds of financing totaled $8 million.

Figure 2-4 Alchemix Participating Institutions

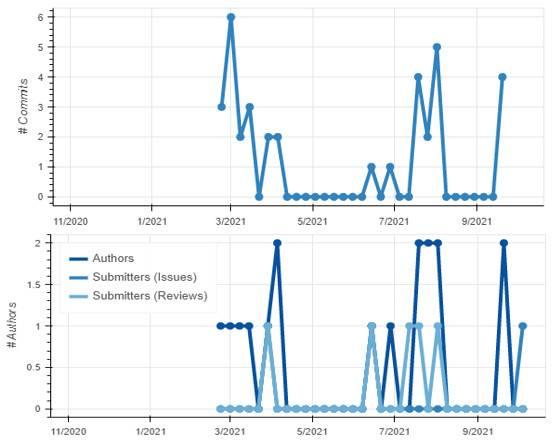

Code

Figure 2-5 Alchemix Code Repository Iteration Status

The Alchemix code repository has only 35 commits, and the daily maintenance personnel for the code repository are 1-2 people, indicating that the Alchemix team may be quite small. However, the product construction of Alchemix is relatively simple, and the technical implementation is not very difficult.

Business Mechanism

Alchemix Finance is a synthetic asset lending platform supported by future earnings, helping users access future deposit earnings in advance by creating synthetic asset tokens. In other words, users can use 100% of their principal to farm yields on other DeFi protocols while also borrowing some funds for other investments, thereby leveraging their earnings.

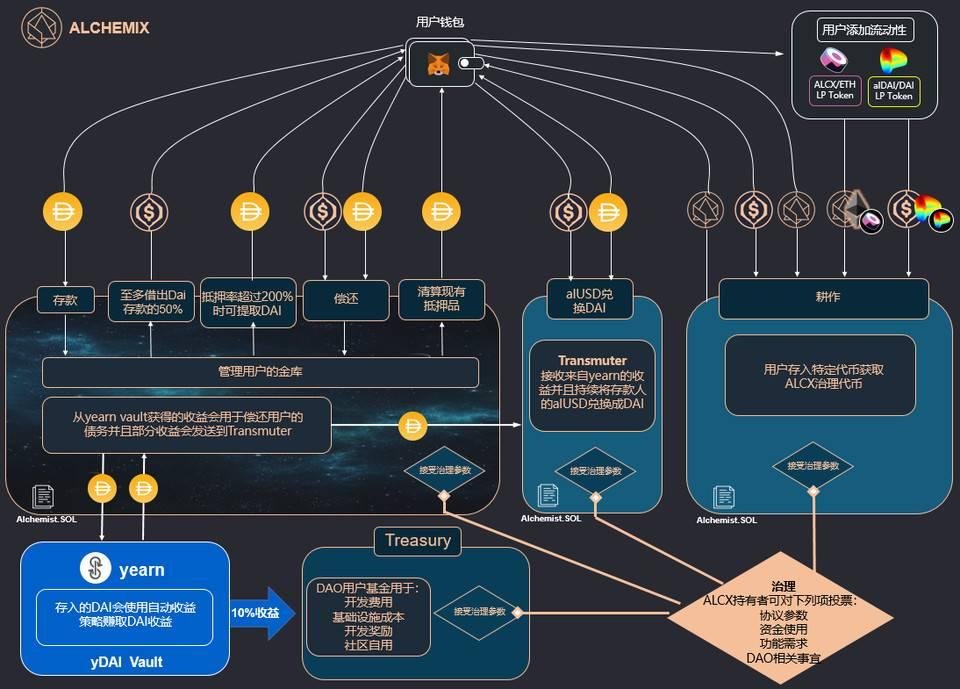

The first version of Alchemix is based on DAI as the underlying asset. Users can deposit DAI into the Achemist smart contract to mint synthetic stablecoin alUSD up to 50% of their deposit value, which can be placed in the Curve pool for liquidity provision or other operations; the deposited DAI will be deployed to the yield aggregation protocol Yearn's yDAI vault for yield farming. When the Alchemix contract receives earnings from the yDAI contract, 10% of the earnings will be sent to the DAO, and 90% of the earnings will be proportionally used to repay all users' debts, ultimately clearing all user debts automatically.

The following diagram illustrates the Alchemix product architecture, which mainly includes Vaults, Transmuter, Treasury, and Farming.

Figure 2-6 Alchemix Platform Architecture

Vaults

Vaults are where user assets are managed and are the core of Alchemix's lending logic. The process is as follows:

- Deposit collateral: Users need to deposit DAI into this contract, and this DAI will be deployed to Yearn's yDAI Vault for liquidity mining to earn yields;

- Borrowing: Users can mint alUSD up to 50% of their deposit value, equivalent to debt, with a minimum collateralization ratio of 200%;

- Repayment: 90% of the earnings obtained from yDAI will be periodically used to repay all deposit users' debts until the debts are cleared;

- Withdraw collateral: When the vault's collateralization ratio is above 200%, users can withdraw the excess DAI. As the protocol repays more debts, users can withdraw more collateral DAI; alternatively, users can also directly repay debts with alUSD or DAI and withdraw collateral at any time.

Transmuter

Transmuter is primarily where alUSD is exchanged for DAI, meaning users can use this contract to convert their alUSD into DAI at any time. Since 90% of the earnings obtained from yDAI will be sent to Transmuter and distributed according to the proportion of alUSD held by users, these earnings will be used to reduce users' liabilities until the debts are ultimately cleared.

For example, suppose Alice is the only deposit user, and she deposits 1,000 DAI in Alchemix, with a maximum borrowing limit of 500 alUSD. At this point, her assets are 1,000 DAI + 500 alUSD, her debt is 500 alUSD, and her net asset value is 1,000 DAI. This DAI will be placed in the yDAI vault to earn interest. After a while, Alice earns 100 DAI in interest from yDAI, and the Alchemist.sol smart contract will withdraw this interest, sending 10 DAI to the Treasury and 90 DAI to Transmuter. At this point, Alice's asset balance is 1,000 DAI + 500 alUSD, her debt will change to 410 alUSD, and her net asset value will be 1,090 DAI.

It is important to note that when funds enter Transmuter, the user's debt is only reduced as an accounting issue; this process does not destroy alUSD tokens but merely reduces the alUSD debt based on the user's deposit balance. Therefore, the Transmuter contract will continue to hold DAI, and alUSD will remain in the user's hands. Users still need to use Transmuter to convert their alUSD into DAI. Thus, it is necessary to ensure sufficient DAI in Transmuter to execute users' exchange operations, which means Transmuter will assume two roles:

Price Stability Mechanism

Alchemix allows users to repay debts directly with DAI or alUSD. The benefit of this approach is that when the market price of 1 alUSD is lower than 1 DAI, users can purchase alUSD at a discount from the market to repay their debts, as the protocol sets 1 alUSD = 1 DAI, helping users achieve arbitrage. From the perspective of market supply and demand, when the price of alUSD is lower than DAI, it will increase the purchasing demand for alUSD, stimulating the price of alUSD to rise and helping it return to its pegged state; the opposite is also true. The price peg between DAI and alUSD is maintained through market supply and demand.

Yield Accelerator

In terms of the state of Transmuter, two scenarios may arise:

- DAI supply < alUSD debt, in which case it will be supported by yDAI interest until all alUSD debts are redeemed;

- DAI supply > alUSD debt, and the excess DAI will be reinvested into Yearn for yield. To ensure DAI exchange, the community voted to keep 5 million DAI as a buffer, with 90% of the remaining earnings reinvested. Since yDAI earnings are shared among Transmuter users, and there is no distinction between user funds and the funds accumulated in Transmuter itself, this situation will actually accelerate the earnings of deposit users.

The sources of DAI in Transmuter are, on one hand, the earnings from Yearn, and on the other hand, users directly using DAI to repay debts. When the DAI supply exceeds the debt, it will accelerate Alchemix deposit earnings, creating a scale effect. Therefore, the more funds deposited in Transmuter, the more substantial the DAI earnings, and the factors attracting users to deposit DAI are based on their bullish outlook on alUSD. The more diverse the application scenarios for alUSD, the higher its value; conversely, if alUSD lacks mining or other application scenarios, the assets in Transmuter will be completely exchanged. Therefore, the attractiveness of Alchemix products is closely related to the application scenarios of alUSD.

Treasury

The Treasury is the address that controls the protocol's earnings. 10% of the earnings generated by Yearn will be allocated to the Treasury as a development fund for the project's future, mainly used to support the ongoing development of the protocol, pay server costs, marketing, and other expenses. The specific use of funds in the Treasury will be decided by ALCX holders through voting.

Farming

Farming is currently the main way to acquire ALCX tokens, where users can stake ALCX/ETH SLP tokens or stake ALCX tokens to earn ALCX governance token rewards.

Products

Alchemix currently has three products: Vault, Swap, and Farm.

Vault

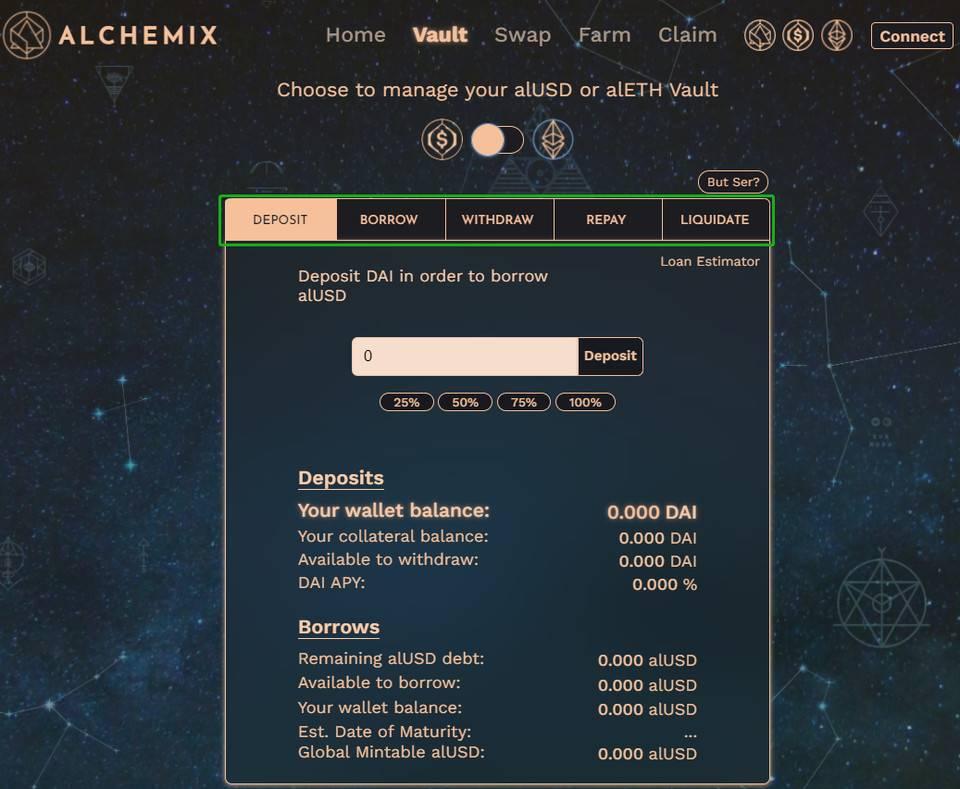

Vault is mainly used to manage user assets, allowing for deposits, borrowing, withdrawals, repayments, and liquidation operations. It is important to note that the liquidation mechanism in Alchemix differs from that of other lending protocols; Alchemix's liquidation refers to the process where users can choose to use collateral in the contract to pay off alToken debts when they lack funds to repay. When a user's debt is cleared, they can withdraw the remaining collateral in the contract at any time. In fact, the protocol itself cannot liquidate users, but users can self-liquidate.

Figure 2-7 Vault Product Interface

Alchemix currently supports two types of collateral: DAI and ETH. Due to the higher volatility of ETH assets, users can only borrow up to 25% of the funds in alETH when borrowing.

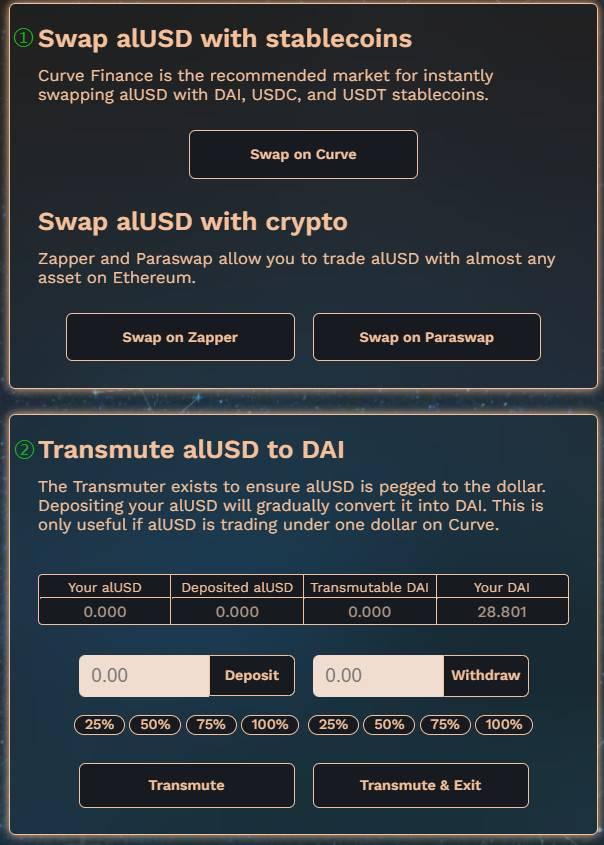

Swap

This product primarily facilitates the exchange of alUSD with other cryptocurrencies, divided into two parts: ① Internal loop, exchanging alUSD for DAI in Transmuter; ② External loop, achieving the exchange of alUSD with stablecoins or other cryptocurrencies in the market. Alchemix integrates Curve, Zapper, and Paraswap to provide users with direct exchange ports.

Figure 2-8 Swap Product Interface

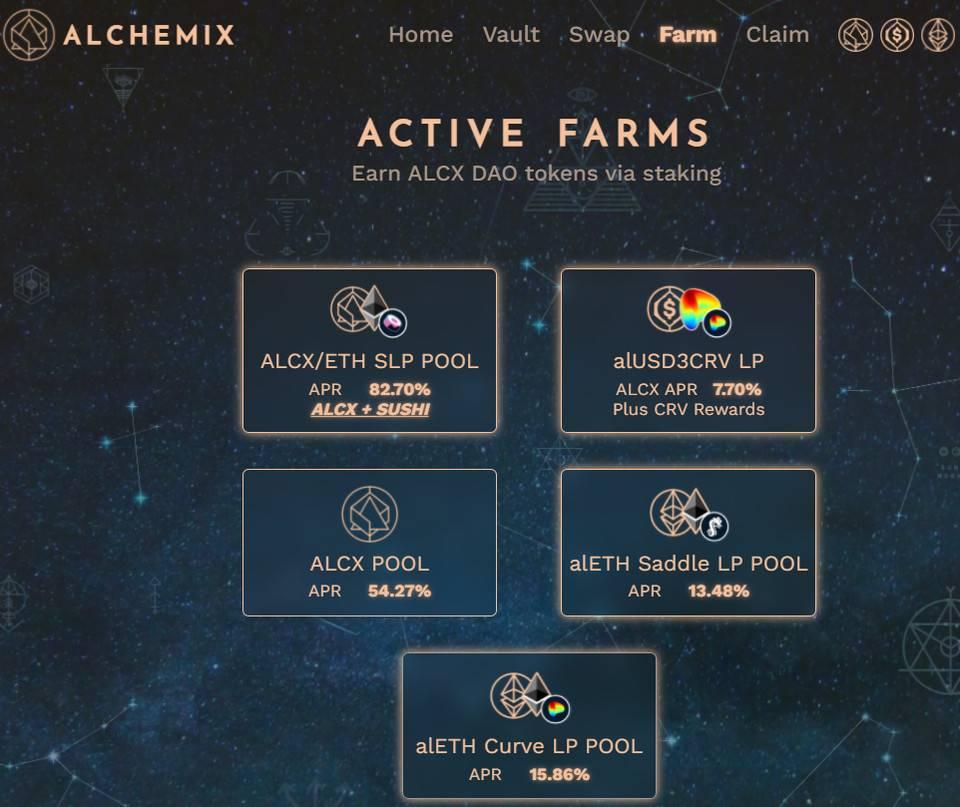

Farm

Users can stake ALCX/ETH SLP tokens or stake ALCX tokens on this page to earn ALCX governance tokens.

Figure 2-9 Farm Product Interface

Alchemix DAO

The development fund of Alchemix DAO comes from the Treasury, where 10% of the earnings generated by Yearn will be sent to the Treasury. Alchemix adopts decentralized governance, sending governance signals through Snapshot, with ALCX holders as decision-makers determining the direction of the protocol's development and the use of Treasury funds. After Alchemix DAO matures, the development team will present their complete vision for on-chain governance and transfer control of protocol parameters to the community.

Governance Process

Community users discuss protocol matters and propose protocol modification suggestions in the Discord governance channel [governance]. Once a clearer plan is established, community members can draft a formal proposal in the [forum] to solicit community feedback. If it gains majority support, it can be formally voted on Snapshot, and developers will conduct due diligence to ensure the protocol's security and implement modules.

Ecosystem

OlympusDAO and Bond

Alchemix has partnered with Olympus to build a bond program, with 10% of liquidity mining rewards allocated to this program. The purpose of the bond program is to reduce liquidity mining rewards, thereby adjusting token supply.

Bonds can help users with arbitrage, and the program primarily targets the ALCX-ETH SLP pool. When ALCX-ETH SLP holders find a significant bond discount, they can purchase bonds. Bonds have a 7-day vesting period, after which they can be exchanged for ALCX at a certain price discount (averaging about 6%-7%). The higher the price of ALCX, the more it incentivizes LP holders to purchase bonds. When calculating bond prices, the intrinsic price of the protocol is used rather than the market price, meaning that bond prices are determined by the LP token value and the number of unexercised bonds. The specific pricing logic can be referenced in the "Issue 143 Olympus" research report. The more unexercised bonds there are, the lower the discount for bondholders, and vice versa, adjusting user enthusiasm for purchasing bonds.

Olympus will provide the bond program and maintenance to Alchemix, and in return, Olympus will charge a 3.3% service fee on all sold ALCX bonds.

The current locked liquidity in the bond program has reached $2.7 million, and due to good performance, the latest proposal passed by the community (on October 24) has changed the bond program issuance curve to 15% (approximately 2,400 ALCX/week), increasing the supply for the bond program; after the Tokemak Reactor goes live, the issuance curve will change to 30% (approximately 4,800 ALCX/week).

Tokemak and tALCX

tALCX is the deposit certificate (i.e., LP token) for the liquidity allocation protocol Tokemak. The Tokemak protocol consists of multiple Reactors, which are comprehensive token pools. These assets will be deployed as liquidity across various trading pairs on various exchanges, guided by governance token TOKE holders, who will benefit from guiding this liquidity. ALCX will become one of the first projects on Tokemak, enhancing the liquidity of ALCX trading pairs, initially providing $3 million of ALCX as operational reserves. Additionally, the team has created a tALCX mining pool and allocated 5% of mining rewards to it.

Bribes and Convex

Curve is an important exchange venue for Alchemix's derivative token alToken, providing CRV rewards to liquidity providers. Moreover, to enhance CRV governance participation, Curve has proposed a rewards multiplier program, where the multiplier is related to relative voting weight. The higher the multiplier, the higher the weight and the more generous the rewards, thus incentivizing the continuous fermentation of Curve bribery.

On August 29, founder Scoopy Trooples explained in the community forum that he allocated $6,000 worth of tokens for Bribe incentives within two weeks, resulting in a slight increase in Gauge weight and rewards (around 2% at that time). To gain more weight and rewards, he proposed to allocate 400 ALCX weekly to incentivize veCRV voters to vote for the Gauge, which was approved on August 31, with these tokens funded from the Treasury.

On October 24, the community passed the latest proposal to change the bribery weight reward to 12% of liquidity mining rewards (approximately 1,900 ALCX/week), targeting alUSD3CRV and alETH.

Alchemix has reached a partnership with the yield protocol Convex, where users can stake veCRV tokens on Convex to obtain deposit certificates cvxCRV. Through this series of operations, users can access Curve trading fees, CRV bonus rewards, and CVX token rewards, maximizing user earnings.

d3 Alliance

Alchemix plans to form a new Curve pool with stablecoin protocols Frax and Fei, concentrating resources through the d3 alliance pool to provide deep liquidity among the three tokens, with the three teams controlling over 500,000 CVX, creating more effective competitiveness. Based on this proposal, Alchemix will distribute ALCX reward tokens of 1,900 ALCX/week and CVX voting rights evenly among alUSD3CRV, alETH, and d3 pools.

In summary:

- Alchemix is a synthetic asset platform supported by future earnings, but it essentially remains a lending protocol that allows users to borrow assets through over-collateralization. The main difference from mainstream lending protocols lies in the method of interest repayment and the types of borrowed assets.

- From a product logic perspective, the primary use of Alchemix is to amplify user earnings, achieved by lending assets to increase user capital leverage and accelerating pool earnings through the Transmuter redemption mechanism.

- The product construction of Alchemix is relatively simple. Although it initially gained some popularity due to the "AC concept coin," its subsequent development has been relatively slow. The real driver of Alchemix's growth has been its bundling with the Curve ecosystem, fully leveraging the Lego-like properties of DeFi to form an ecological alliance. The benefit of this approach is that it increases the diversity of the protocol, enriching the application scenarios of ALCX while maximizing the efficiency of user capital utilization.

Development

History

Table 3-1 Major Historical Events of Alchemix

Contract Vulnerability Incident Report

On June 19, 2021, some users of the Alchemix alETH vault discovered that even with a 25% collateralization ratio, they still had no outstanding debt. Additionally, nearly 2,000 ETH of debt limits were released for minting new alETH again. Upon discovering this issue, the team immediately took action, suspending the minting of new alETH until the problem was identified and a solution was provided.

Investigations revealed that there was an issue with the deployment script of the alETH vault, which accidentally created another vault, and Achemist used incorrect data across multiple vaults, leading to incorrect yield calculations based on erroneous data, and all 4,300 ETH calculated incorrectly in Transmuter were used to repay users' debts.

The scope of losses from this vulnerability was limited to alETH supporters, with individual users and Yearn funds unaffected. To restore system solvency, the team decided to: 1) temporarily increase protocol fees to cover the debt gap, with this income going directly into Transmuter to support alETH; 2) introduce some ETH from the Treasury into Transmuter; 3) sell some DAI from the Treasury for ETH and add it to Transmuter.

To reward users who returned ETH/alETH during this incident, the team will airdrop ALCX tokens and special edition POAP NFTs at a 1:1 ratio. All ETH returned to the Alchemix multi-signature address will be allocated to the new alETH Transmuter; all alETH returned to the Alchemix multi-signature address will be burned.

Current Status

Treasury Performance

The Treasury supports the sustainable development of Alchemix, with its initial income source being 10% of Yearn's earnings and 358,959 ALCX tokens pre-mined. According to the latest data from Etherscan, the current status of the Treasury holding address is as follows:

The Treasury currently holds assets including 286,000 ALCX, 261 ETH, and 504,000 DAI, with a total asset value of approximately $130 million. Additionally, the Treasury has some assets allocated to other protocols for appreciation, including about 2.25 million DAI on Convex and 15,000 ALCX locked on Abracadabra. Based on market prices, the Treasury's total assets are currently approximately $140 million. From its earnings perspective, the current earnings strategy is quite appropriate, and the earnings are considerable.

Alchemix Earnings Performance

Alchemix's current business (i.e., accepted collateral types) is divided into DAI and ETH, with the following business data:

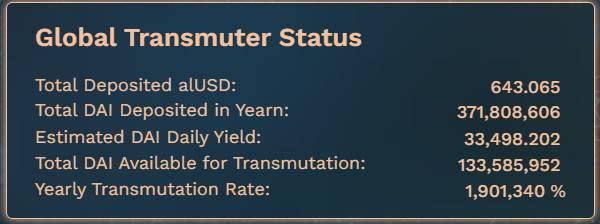

Figure 3-1 DAI Business Data

From the performance of the DAI business, the total amount of DAI currently in Yearn is approximately $372 million, and the total amount of DAI in Transmuter is approximately $134 million, indicating that the principal deposited by users is about $238 million, which corresponds to a leverage of 1.6 times; since the Alchemix contract allows users to borrow 50% of the DAI supply, this gives users 2 times leverage. In this case, the current leverage for DAI is around 3.2 times, and based on the current APY yield of 4.55% for yDAI, Alchemix's annualized yield is 14.56%.

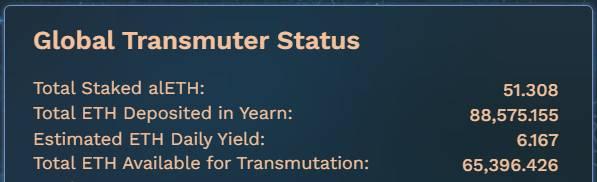

Figure 3-2 ETH Business Data

Currently, the amount of ETH in Yearn is 88,600, and the amount in Transmuter is 65,400, with user principal being 23,200. This indicates that users prefer to repay debts directly with ETH, thus amplifying user earnings by about 3.8 times. However, the Alchemix contract only allows users to borrow 25% of the ETH supply, giving users about 1.3 times leverage. Therefore, the current leverage for ETH is approximately 4.9 times, with yETH annualized yield at 2.5%, and Alchemix's annualized yield at 12.25%.

Bribe Performance

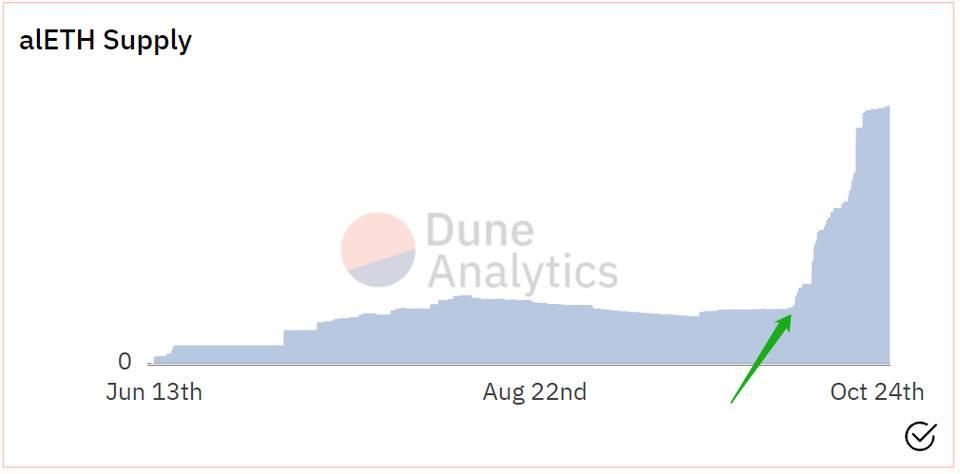

Since the stablecoin protocol Abracadabra brought significant results through bribery, Alchemix's bribery has also attracted market attention. According to data from Dune Analytics, the supply of alETH has been increasing rapidly since October 8.

Figure 3-3 alETH Supply Trend

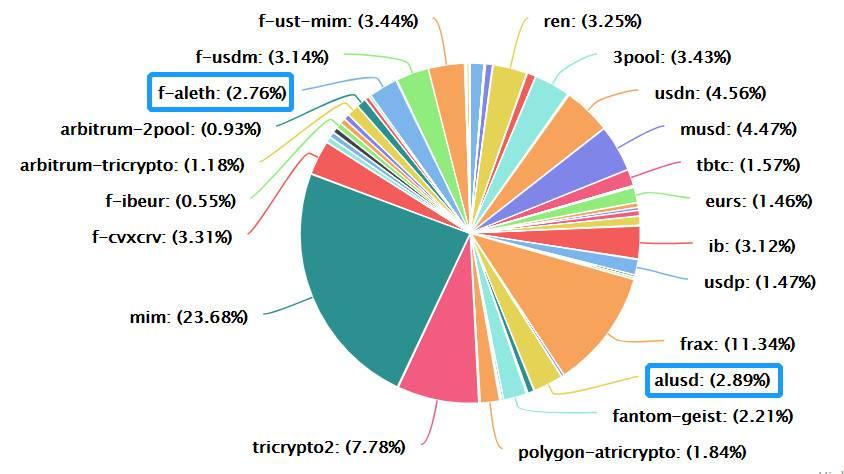

According to data from the Curve official website, Alchemix currently has two pools: alUSD and alETH. Figure 3-4 shows the relative voting share of these two pools on Curve, which will take effect on November 4, 2021.

Figure 2-10 Curve Relative Voting Share Chart

Table 3-2 Bribe Earnings Performance

Future

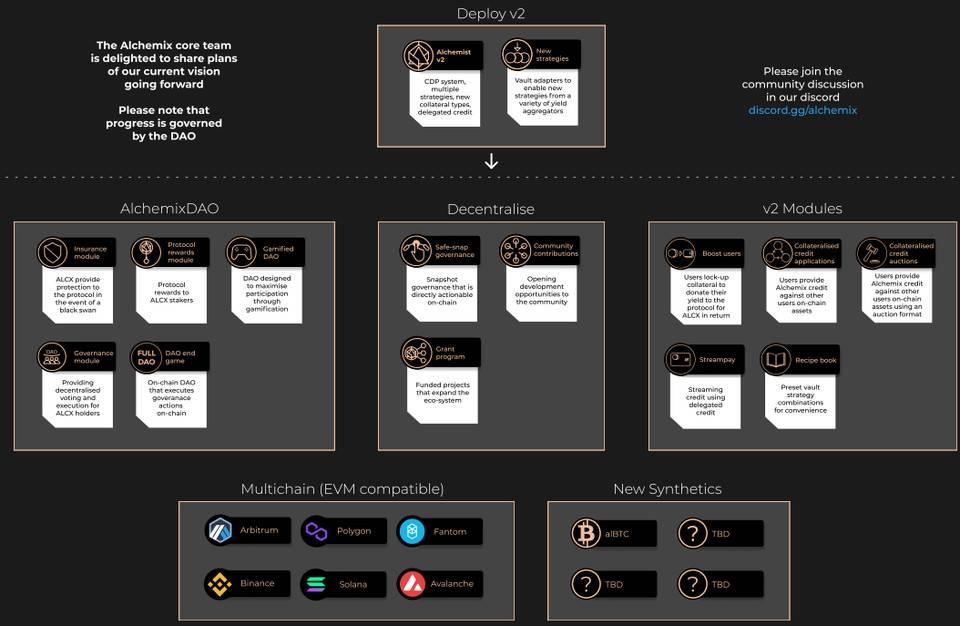

Alchemix released its latest version roadmap on October 8, as shown in Figure 3-4. The major product development directions in the future are: 1) Multi-chain; 2) Multiple synthetic assets.

Figure 3-4 Alchemix Roadmap

The product development directions in the roadmap can be subdivided into:

- Development of AlchemixDAO, including building a more robust insurance module, governance module, and smoother on-chain governance process;

- Decentralization, including direct on-chain execution of Snapshot governance, funding protocols to expand the ecosystem, and opening development opportunities for the community;

- Implementation of v2 modules, including user incentive programs, credit limit delegation, flow payments, preset strategy combinations, etc.

In summary: Due to the fermentation of the Curve ecosystem, Alchemix has attracted market attention and brought good liquidity. The essence of Alchemix's product is to amplify yields, and the yield amplification effect is related to the scale of assets locked in the protocol. Therefore, Alchemix's current yield performance is quite considerable. Moreover, the community's management of Treasury funds has also achieved good results, providing ample financial support for Alchemix's sustainable development.

Economic Model

Supply

The Alchemix token is abbreviated as ALCX, and there is no hard cap on the total supply of ALCX. For the purpose of token distribution, the team has provided a token release plan, estimating a total of 2,393,060 ALCX to be released over three years:

- 15% of the total token supply (358,959 ALCX) is allocated to the DAO Treasury, with the community deciding its use;

- 5% (119,653 ALCX) is allocated for the bug bounty program, which will also be allocated to the Treasury address but used for bug bounties;

- The remaining 80% of tokens will be distributed through the Staking Pool contract.

Among these, the 20% allocated to the Treasury, i.e., 478,612 ALCX, is pre-mined; the tokens distributed through the Staking Pool will be divided into two parts:

- Alchemix founders, onboarding developers, and community developers will establish an independent equity pool to receive 16% of the block rewards;

- The remaining 64% will be distributed to liquidity providers.

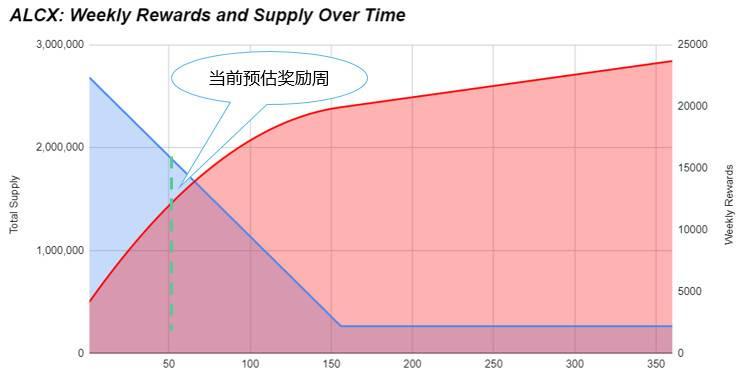

When ALCX is injected into the staking pool (Staking Pool), the first week's reward is 22,344 ALCX, with weekly rewards decreasing by 130 ALCX over three years; after three years, the average weekly reward will be maintained at 2,200 ALCX, with an estimated total annual token supply of 114,400 ALCX. (At the time of writing, it is estimated to be the 53rd week, with a weekly reward of 15,454 ALCX)

Figure 4-1 ALCX Liquidity Mining Plan

Distribution Channels

64% of ALCX tokens will be distributed to liquidity providers through the Staking Pool, with four initial distribution channels:

- 18% allocated to the alUSD-3CRV pool on Curve, aimed at establishing a deep liquidity pool for alUSD through Curve to enhance its utility;

- 60% allocated to LPs providing liquidity for ALCX/ETH on Sushiswap to promote ALCX liquidity;

- 2% allocated to the alUSD pool, which is an initial staking pool to incentivize users to hold alUSD, ensuring that the alUSD/DAI trading pair has sufficient liquidity;

- 20% allocated to ALCX stakers, allowing token holders to earn rewards simply by holding tokens.

As Alchemix continues to push into the market, the weights of these pools are also continuously adjusted. According to the documentation, as of October 24, 2021, the pool weight adjustment plan is shown in Table 4-1, with the second phase starting after the Tokemak reactor is launched:

Table 4-1 Liquidity Mining Token Issuance Plan

Note: The mining reward for the alETH Curve pool is 0%, as this portion of the reward will be compensated by Bribes.

Distribution

According to Etherscan data, the current total minted amount is 1,562,679, with the number of token holding addresses being 6,371. The total amount of tokens held by the top fifty addresses is 1.05 million, accounting for 67.41%.

Table 4-2 Status of the Top 50 Token Holding Addresses

The current circulating supply of ALCX tokens is relatively low, with most concentrated in the Treasury, which is pre-mined and mainly used to support the development of the protocol. The best trading depth for ALCX is currently on SushiSwap, followed by FTX.

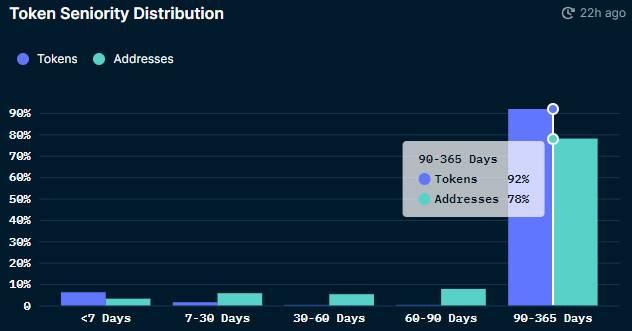

From nansen.ai data, currently, 78% of addresses hold 92% of the tokens, indicating a relatively concentrated token distribution with long holding times. This suggests that there are few new entrants, and most addresses are long-term holders, including institutional addresses.

Figure 4-3 ALCX Token Holding Address Distribution

In summary: The current market circulation of ALCX is low, with most tokens concentrated in the hands of long-term users, and retail investors entering the market are few; the circulating tokens in the market are mainly released through liquidity mining, and the current liquidity mining methods are becoming increasingly diverse, providing ALCX with richer application scenarios and offering users more diverse yield strategy choices.

Competition

Industry Analysis

Alchemix operates in the lending protocol sector, simulating traditional financial systems to understand the funding needs of different users and providing a platform for mutual fund flow among users, automatically calculating and adjusting market lending rates based on supply and demand. Currently, mainstream lending protocols connect borrowers and lenders through a pool model to quickly match lending needs. The driving force behind the development of lending products is the increasing demand for leveraged trading, and the prevalence of liquidity mining further stimulates the demand for stablecoin lending.

Development

Lending protocols are cornerstone products of decentralized finance (DeFi), developing since 2018. MakerDAO introduced the first lending market, allowing users to deposit ETH as collateral to generate stablecoin DAI, later accepting more types of collateral; Compound popularized a wider range of asset lending, where lenders receive cTokens representing their deposits, which can be used as assets in other protocols; in 2019, Aave began competing with Compound by offering different interest rate models and more types of lending assets. In June 2020, the DeFi boom exploded, and the lending market became even more prosperous, with DeFi Lego building becoming increasingly complex. The current DeFi market size is approximately $100 billion, with the lending market size around $49 billion, accounting for 49%.

Figure 5-1 Development of the Lending Market

Classification

Lending protocols are typically divided into unsecured lending and over-collateralized lending, with the distinction being whether there are sufficient assets backing them. Due to the decentralized nature of DeFi, on-chain credit mechanisms are still imperfect, making unsecured lending difficult to implement, with a small market share; mainstream lending protocols, such as Compound and Aave, are primarily based on over-collateralized lending models, eliminating third-party involvement. Alchemix also adopts an over-collateralized lending model, allowing users to borrow assets at a certain collateralization ratio. The difference from mainstream lending protocols lies in the methods of debt repayment, the types of borrowed assets, and the liquidation methods.

Competitive Comparison

Debt Repayment Method

Mainstream lending protocols typically require borrowers to repay the loan + interest when withdrawing collateral, with the interest calculated automatically by the interest rate model; Alchemix primarily uses deposit earnings as the method of debt repayment. The logic behind this operation is that when users deposit collateral, this collateral will be farmed in a yield aggregation protocol to obtain more considerable earnings, which will bridge the debt. Once users clear their debts, they can withdraw their principal; of course, users can also choose to repay the borrowed assets directly, meaning that borrowing is essentially interest-free.

Types of Borrowed Assets

Currently, mainstream lending protocols are divided into two forms: borrowing stablecoins by collateralizing crypto assets and borrowing other crypto assets by collateralizing crypto assets, with typical representative projects being MakerDAO and Compound. MakerDAO allows users to borrow stablecoin DAI by collateralizing mainstream crypto assets like ETH, keeping DAI pegged 1:1 with the US dollar, enabling users to obtain relatively stable liquidity without having to sell their currently held tokens, which means they are bullish on the collateral; Compound, on the other hand, allows users to borrow existing crypto assets supported by the market by collateralizing mainstream cryptocurrencies, which can be stablecoins or other cryptocurrencies.

Alchemix generates synthetic assets alToken by collateralizing crypto assets, currently accepting DAI and ETH as collateral, with synthetic assets being alUSD and alETH. Moreover, in the future, it may accept other stablecoins as collateral to synthesize alUSD, meaning that the collateral behind alUSD will not only be DAI. From this perspective, the assets borrowed by Alchemix are directly linked to their underlying collateral, ensuring a 1:1 exchange between alToken and the native token.

Liquidation

Liquidation refers to the process of forcibly selling collateral when the value of a user's debt exceeds the safe line of collateral assets, which occurs due to the high volatility of crypto asset prices.

In MakerDAO, collateralized cryptocurrencies are used to borrow stablecoins, presenting a one-sided risk; in protocols like Compound and Aave, users can collateralize cryptocurrencies to borrow other more volatile assets, creating a two-sided risk for borrowers, as both the price changes of collateral assets and borrowed assets can lead to liquidation risks.

Although Alchemix also involves collateralized lending, the assets borrowed are pegged to the underlying assets, so the impact of market price fluctuations is relatively small. When the two become unpegged, the Transmuter redemption mechanism will help both return to their pegged state. Therefore, Alchemix does not have a rigid liquidation mechanism.

Yield

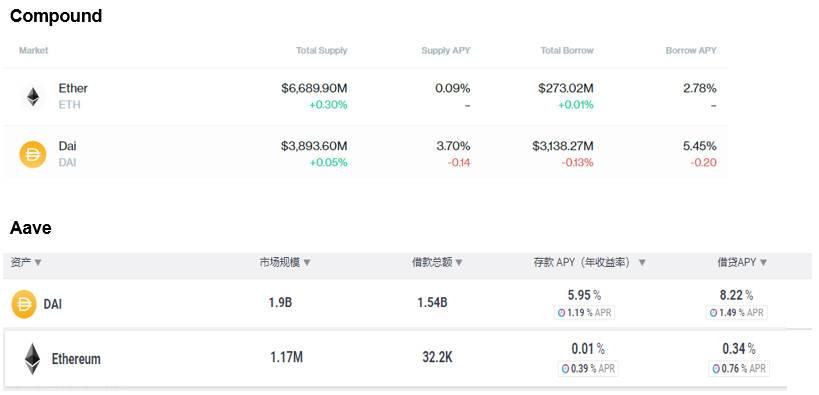

Yield is one of the critical indicators influencing user choices. The yields of Compound and Aave are related to capital utilization rates, and based on current yield performance, they are far below that of Alchemix, whose yield is referenced in section 3.2.2. As a yield amplifier, this is where Alchemix excels compared to conventional lending protocols.

Figure 5-2 Yield Performance of Compound and Aave

Application Scenarios

The purpose of lending is to obtain leverage, and Alchemix also provides users with leverage capabilities. From a business logic perspective, Alchemix offers interest-free, no-liquidation lending, focusing on a more niche yield enhancement business compared to mainstream protocols. The effectiveness of yield enhancement is closely related to the application scenarios of alToken. Currently, Alchemix is based on the yield aggregation protocol yearn.finance to achieve yield optimization, positioned above yield aggregation protocols, capable of absorbing users from aggregation protocols, lending protocols, or other projects with low risk and return ratios.

In summary: Although Alchemix is a lending protocol, it has significant differences from mainstream lending protocols, offering interest-free, no-liquidation lending services and focusing more on yield enhancement business, positioned above yield aggregation protocols, capable of absorbing DeFi's existing users.

Risks

Due to the permissionless nature of DeFi, smart contracts are often subject to attacks, so users must remain vigilant when using the protocol. Additionally, Alchemix is currently collaborating with multiple DeFi protocols to enhance competitiveness; however, if one protocol encounters issues, Alchemix will inevitably face some losses. Therefore, the potential risks faced by Alchemix are considerable.

Investment Analysis

Investment carries risks. The price data provided for entry is based on the author's understanding and recognition of the project and serves only as a demonstration reference, not as a basis for user investment decisions. Users should make investment decisions based on their understanding and recognition of the project. First Class Warehouse and the author of this article are not responsible for any profits or losses resulting from users' investment decisions.