Liquidity Singularity: Tokemak and Its Sustainable Liquidity Protocol

Tokemak is a decentralized market-making protocol, a novel DeFi primitive designed to create a liquidity infrastructure layer for DAOs, new DeFi projects, market makers, exchanges, and advanced users.

Tokemak is a decentralized market-making protocol, a novel DeFi primitive designed to create a liquidity infrastructure layer for DAOs, new DeFi projects, market makers, exchanges, and advanced users.Author: Ben Giove

Compiled by: 8btc

DeFi operates on liquidity. Whether it's decentralized exchanges, money markets, or stablecoins, liquidity is the necessary fuel driving these applications.

Despite its importance, liquidity can be a fickle resource in the cryptocurrency economy. The costs of acquiring and retaining liquidity are high, and capital is profit-driven, with market makers primarily concentrated among whales and institutions. Essentially, this is inefficient and unsustainable.

If we want DeFi to reach its full potential, this issue needs to be addressed, which is where Tokemak comes into play.

Tokemak is a decentralized market-making protocol, a novel DeFi primitive designed to create a layer of liquidity infrastructure for DAOs, new DeFi projects, market makers, exchanges, and advanced users.

This is arguably a tall order. But can it meet its expectations?

Let’s wait and see.

The Liquidity Problem

Before we dive into Tokemak itself, let’s take some time to better understand the nature of liquidity within DeFi. As mentioned, liquidity is both necessary and problematic. It is expensive, profit-driven, and concentrated in the hands of a few entities.

Few things exemplify this relationship better than liquidity mining.

While it has been an effective strategy for guiding the growth of the entire DeFi ecosystem, with the TVL of DeFi on Ethereum increasing from $1.15 billion at the start of the Compound program in June 2020 to $114 billion today, liquidity mining represents a huge cost for protocols.

For example, since the launch of its program, Compound has increased its value locked from $597 million to $10.81 billion. This growth has allowed the protocol to operate more effectively. Increased liquidity means Compound can offer greater borrowing amounts to its depositors.

However, to provide incentives for attracting this liquidity, Compound has distributed over $271 million worth of COMP tokens. This means that Compound has essentially been operating at a loss during this period, compared to the $29.1 million in protocol revenue earned during the same time (currently all allocated to reserves). The program has also come at the cost of downward pressure on COMP prices, as rewards entering the market are often sold off by yield farmers.

In addition to being costly, liquidity is also profit-driven. Capital is always in search of the highest risk-adjusted returns, and many high-yield sources are largely attributable to token rewards. When token rewards diminish or end, capital leaves to chase the next opportunity.

A prominent example of this mercenary nature is Uniswap. During the two-month liquidity mining program from September to November 2020, LPs were incentivized with UNI rewards, but the protocol's TVL dropped by nearly 49.5%.

How Tokemak Works

Having understood the nature of liquidity issues within DeFi, let’s delve into Tokemak itself. The protocol is complex, so let’s look at the key components and participants within the system and how they interact.

Token Reactors

Each asset supported by Tokemak has its own token reactor. Reactors serve as hubs that aggregate deposits of specific assets, forming connections between liquidity providers (LPs), depositors, and liquidity directors (LDs), who allocate their staked TOKE to the reactor to determine where these assets are deployed (which will be detailed below).

The purpose of the reactor is to "balance," or keep the value of deposits from liquidity providers as close to a 1:1 ratio with the TOKE staked by liquidity directors as possible. To incentivize this, the protocol algorithmically adjusts the interest rates paid to LPs and LDs (currently both are compensated through TOKE rewards). When the value of assets within a reactor exceeds the TOKE staked, the yield for LDs will increase to attract more TOKE and balance the reactor. Conversely, when the reactor is over-staked, the yield for LPs will be adjusted upwards to incentivize more liquidity provider deposits.

While reactors have not yet gone live, their creation will initially be determined by governance votes from TOKE holders. In the future, the team intends to eventually support permissionless reactor creation.

Liquidity Providers

As mentioned, liquidity providers are participants who deposit assets into the protocol through reactors. This concept is similar to providing liquidity for DEXs, but users deposit directly into Tokemak rather than through a front-end interfacing with the protocol, simplifying the complexities of being an LP.

Liquidity providers earn yields in the form of TOKE rewards and receive "tAssets" upon providing, representing a 1:1 tokenized claim on their respective deposits, similar to Compound, Aave, or Yearn.

A notable feature of providing liquidity through Tokemak is that LP deposits are one-sided. Unlike traditional services provided through DEXs (like Uniswap or Sushiswap), where LPs need to deposit a specific asset pair, in Tokemak, liquidity providers are shielded from impermanent loss, with the risk transferred to liquidity directors.

Liquidity Directors

Liquidity directors (LDs) determine the allocation of liquidity. To participate, LDs deposit TOKE into the protocol. They can choose to allocate their staked TOKE to one or multiple reactors or proportionally across all reactors within the system.

After deciding on one or more reactors, LDs can vote with their TOKE to determine which exchange liquidity will be directed to. The voting power of an LD is proportional to their total TOKE share in a given reactor. At the end of the period, liquidity is directed to a venue, on a weekly basis, known as a cycle.

Initially, the protocol plans to support liquidity directed to Uniswap V2, SushiSwap, 0x, and Balancer. In the future, the project aims to expand liquidity directions to include more venues, such as Uniswap V3, and will have the capability to allocate to exchanges on other blockchains and layer twos.

Like LPs, LDs are compensated in the form of TOKE rewards. However, liquidity directors face significantly greater risks than providers, as they are participants in the system and are subject to impermanent loss.

While Tokemak abstracts the complexities of providing liquidity, the protocol cannot eliminate the risk of impermanent loss.

Instead, this risk is transferred from liquidity providers to liquidity directors.

If an asset faces impermanent loss and liquidity providers cannot withdraw the full value of their deposits, the protocol will first extract asset reserves from the relevant reactor. If this is insufficient, the TOKE rewards paid to the LDs of the reactor will be redistributed to the LPs. If the reactor is still under-collateralized, as with Aave, the collateral TOKE allocated to the reactor will be reduced and used as a last resort to compensate LPs.

Bundled Compositions

With these concepts, we can understand how the system operates.

? Simply put, liquidity providers deposit assets into token reactors, and liquidity directors stake TOKE to choose the direction of liquidity.

Launching Tokemak: Cycle Zero

Tokemak not only has a unique design but its launch is equally intriguing. The protocol's launch at both financial and community levels is conducted through a series of new mechanisms collectively referred to as "Cycle Zero," ultimately involving the distribution of 5 million TOKE (5% of total supply) to participants.

There are three distinct events within Cycle Zero:

1. Degenesis

Degenesis is the first event of Cycle Zero, a week-long fair launch activity where participants can contribute ETH or USDC in exchange for TOKE. This allows Tokemak to begin building its reserves of protocol-controlled assets (PCA) and acquire commonly used "base assets" to pair with reactor assets when liquidity is directed to exchanges.

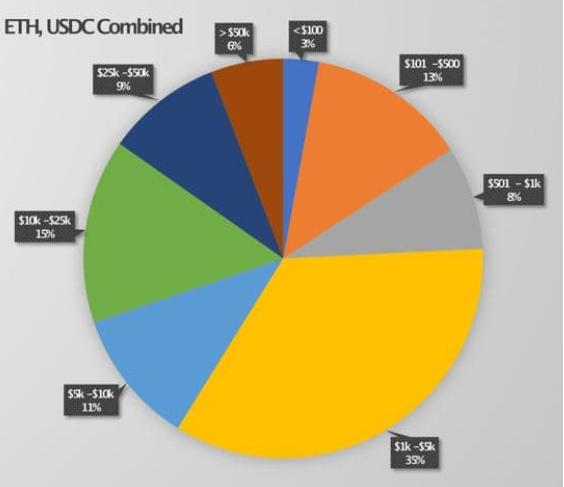

Source: Tokemak Medium

Degenesis has proven to strike a balance in attracting both small and large users, with 65% of the ETH and USDC contributions being $5,000 or below.

2. Farming

The second phase of Cycle Zero is farming. This is another mechanism for the protocol to accumulate base assets and allows it to build liquidity for TOKE itself. Tokemak is currently incentivizing three single-asset pools, including ETH, USDC, and TOKE, as well as rewarding TOKE/ETH pairs on Uniswap V2 and SushiSwap with TOKE.

Currently, the yield for the ETH and USDC pools is between 20-25%, the TOKE pool yield is around 100%, and the TOKE/ETH pair yield is at 525%. In the first two weeks of farming, the ETH and USDC pools were "private," meaning they were only available to Degenesis participants.

3. Reactor Staking Event (C.O.R.E)

The third and final phase of Cycle Zero is the Reactor Staking Event (C.O.R.E), which will bring the first batch of reactors online. This event includes a week-long voting period where token holders will choose the first five reactors to be supported by the protocol.

Adoption and Integration

Although Tokemak is just getting started, it has already seen significant traction.

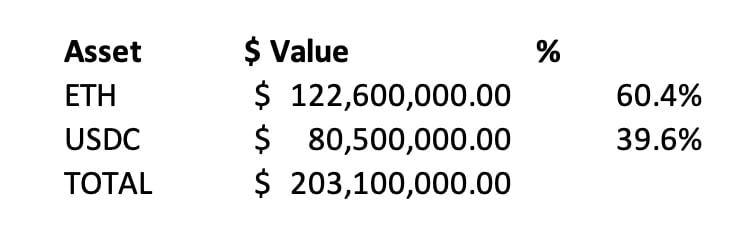

The protocol has accumulated $203.1 million in PCA from Degenesis and Genesis pools, including $122.6 million in ETH (60%) and $80.5 million in USDC (40%).

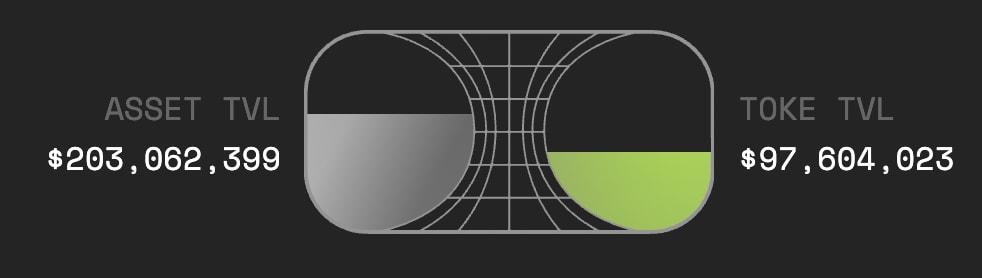

In addition to building its PCA inventory, Tokemak has also managed to attract substantial liquidity for TOKE. Currently, there is $96 million worth of TOKE in the staking pool, as well as TOKE/ETH pairs on Uniswap V2 and SushiSwap.

This means that if the protocol were to go live today, the total balance of PCA to TOKE would tilt in favor of the former at a ratio of 2:1.

Tokemak has also begun integrating with other DeFi protocols. The TOKE/ETH pair on SushiSwap is part of the exchange's Onsen farm and is being incentivized with TOKE and SUSHI rewards. While only $353,000 worth of LP tokens are staked on SushiSwap, with yields showing "only 297%," while the yield on the Tokemak interface is 523%, this does indicate a close relationship between the two protocols.

Additionally, TOKE has been accepted as collateral for Rari Capital's "Token Mass Injection" pool on Fuse (an independent money market protocol), allowing holders to unlock the value of their TOKE through lending.

Tokenomics and a New Paradigm for Liquidity Provision

Tokemak is a fascinating protocol with paradigm-shifting implications on several different levels.

First, Tokemak democratizes the process of liquidity supply and market making. Through one-sided deposits and protection against impermanent loss, Tokemak provides a simplified, risk-minimized way for everyday users to create liquidity. Furthermore, through the liquidity direction of TOKE, users can access market-making opportunities that would not be available through other means.

Another captivating aspect of Tokemak is TOKE itself. As we know, TOKE plays many different roles within the protocol, including:

- Governance of the Tokemak DAO

- Incentives for LPs, LDs, and asset deposits

- A backstop for the protocol in the event of extreme impermanent loss

- Direction of liquidity or tokenized liquidity

The last point is particularly interesting, as holders are able to direct liquidity for an asset and guide it to a destination of their choosing, TOKE can be seen as tokenized liquidity. This means that TOKE is not just a governance or utility token, but a unique digital commodity.

Moreover, by holding TOKE, holders or entities possess the right to access liquidity within the system, making the token a high-value resource for various entities and turning liquidity into an infrastructure layer that anyone can leverage.

For example, DAOs (which the team believes will be the ultimate users of the protocol) can hold TOKE in their treasuries to ensure and direct liquidity to their tokens, rather than initiating an inflationary liquidity mining program.

Given its scarcity, with only 100 million TOKE in existence, there are also thoughts that we may see some lines of "TOKE wars," where protocols compete to acquire TOKE.

Do those who control TOKE control the liquidity of DeFi?

Conclusion

Tokemak is an intriguing new protocol. With its innovative design, unique launch, and significant target market, Tokemak could become an important liquidity infrastructure for the broader cryptocurrency ecosystem.

This emerging protocol is still in its very early stages, as they have not fully launched on the mainnet yet; however, as they continue to build this infrastructure, it is worth keeping a close eye on.