Building Quantitative Models to Explore Ethereum: From Digital Oil to Digital Nation

DeFi protocols hope to use ETH as collateral to create other assets, such as DAI and synthetic assets, to serve as a reserve currency that allows users to trade and raise funds.

DeFi protocols hope to use ETH as collateral to create other assets, such as DAI and synthetic assets, to serve as a reserve currency that allows users to trade and raise funds.The author of this article is Electric Capital, translated by Baize Research Institute.

The 5 Most Popular Views in the Ethereum Community Today:

ETH is a digital commodity

ETH is a non-sovereign digital store of value

Ethereum is a payment network

ETH is a productive financial asset

Ethereum is a digital nation, and ETH is the reserve currency

4 Ways to Assess the Value of Ethereum:

Adoption rate

Network fees

Market multiple of earnings (or similar metrics) that the market can bear

Market share of the entire crypto market

Below, we provide a quantitative framework for each viewpoint. Our goal is not to propose a price target for ETH; rather, we aim to understand what these narratives mean for Ethereum and the expectations of market participants regarding various return scenarios.

Key Assumption: The Ethereum London Upgrade Will Be Successful

We expect a successful transition to PoS and the implementation of EIP 1559.

Due to upcoming monetary policy changes, we assume a fixed ETH supply of 115,000,000 in our calculations.

We assume that average transaction revenue will decline by 80% to 95% compared to the levels in Q1 2021 due to network upgrades and Layer 2 solutions.

Internet-Level Growth Rates

- Technologies invented after the internet, such as smartphones and social media, often develop faster than the internet itself. We generally assume growth similar to the internet, rather than faster.

- From January 2016 to January 2021, Ethereum's transaction volume grew at a compound annual growth rate of 161%. From 2020 to 2030, our model uses compound annual growth rates of 44% and 63%.

Lower Average Transaction Fees

The average transaction cost in Q1 2021 was approximately $31 (with a median transaction fee of about $17)¹

Efforts are underway to reduce transaction fees. Layer 2 scaling solutions, the release of ETH 2.0, the transition to proof of stake, and future network upgrades are all aimed at improving user experience by increasing throughput and lowering fees.

Our assumption in the following models is that average transaction fees will decrease by 80% to 95%, resulting in estimated average fees between $2 and $7 (while also assuming that network value increases significantly, which implies a substantial increase in transaction volume driven by these transaction fees).

Viewpoint 1: In the Digital World, ETH is a Commodity

A common saying is that ETH is similar to oil. Oil powered us through the industrial age, but we are now in the software age, and ETH could become the fuel for the digital economy. With the upcoming network changes and the progress of DeFi over the past year, this comparison sounds increasingly relevant:

Like oil, ETH "burns" when used.

Like oil, demand for ETH comes from various, diverse use cases:

(1). Participation in DeFi.

(2). Securing the ETH 2.0 network.

(3). Issuing, buying, selling, or transferring digital assets, such as ERC20 tokens, including stablecoins and NFTs.

(4). Performing computations using the EVM.

(5). Storing value in alternative asset classes.

(6). Creating cross-chain bridges, where ETH will be held.

- Like oil, the supply of ETH is limited, and supply growth should significantly slow down in the near future.

(1). EIP 1559 will burn ETH that was previously sent to miners.

(2). The transition to PoS will require locking up a large amount of ETH, resulting in a one-time supply shock and a lasting change in circulating supply.

(3). Upcoming network upgrades may consume more ETH than network issues, further reducing supply.

- Like oil, geopolitical factors will affect demand, and sentiment will cause volatility.

The above statements also apply to many other commodities, so we considered the total value of global oil reserves and the proven reserves of other limited supply commodities to roughly estimate the potential value of the Ethereum network.

The table below shows the price of ETH if Ethereum's market cap reaches the market value of natural resources (assuming known reserve units for these commodities and a fixed supply of ETH).

For example, if ETH becomes as valuable as copper in the global economy, then each ETH would be worth $63,913.

Figure: Comparison of various assets and the corresponding price of Ethereum

Limitations of Comparing ETH to Commodities

The number of substitutes for oil (coal, solar, hydro, nuclear, etc.) is limited, but cryptocurrencies can fork, and new cryptocurrencies can be created. For this statement to hold, one must believe that Ethereum's network effects will make it the preferred, dominant solution, and that crypto networks will ultimately have power law or winner-takes-all market distribution.

The production of digital commodities is often cheaper than that of physical commodities, so when comparing ETH to oil, even if ETH becomes as important to the global economy as oil, its value may still be lower than that of oil.

The supply and monetary policy of Ethereum can change, meaning that while supply may be limited in the near future, it could technically grow (or shrink) one day.

Viewpoint 2: ETH is a Non-Sovereign Digital Store of Value

The notion of "digital gold" has been embraced by many BTC investors. With the upcoming Ethereum upgrade, there are four reasons to believe this narrative is relevant to Ethereum:

Like BTC, ETH has characteristics that make it superior to gold. Cryptocurrencies are easier to obtain, transport, and transfer, and are more convenient for buying and selling goods and services.

The supply growth of BTC and ETH is lower than that of gold:

Annual supply growth:

Gold: 2.5%

BTC: 1.75%

ETH: After EIP 1559, it may be less than 2% per year, possibly lower or negative.

- ETH is easier to build on than BTC, which generates powerful network effects.

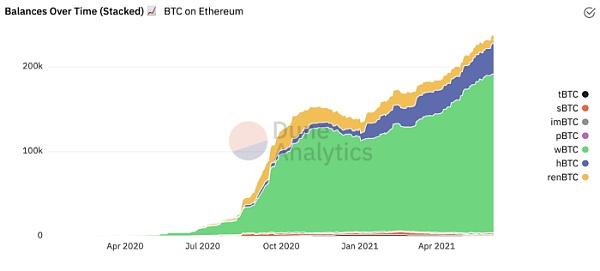

Due to its programmability, ETH has become the reserve currency of DeFi, processing more transactions today than any other network. BTC has already seen more demand for programmability: as of May 2021, over 1% of the BTC supply has been "wrapped" onto Ethereum² to enable programming and trading on the Ethereum network. An increasing amount of BTC is being used on Ethereum:

Figure: The amount of BTC on the Ethereum network

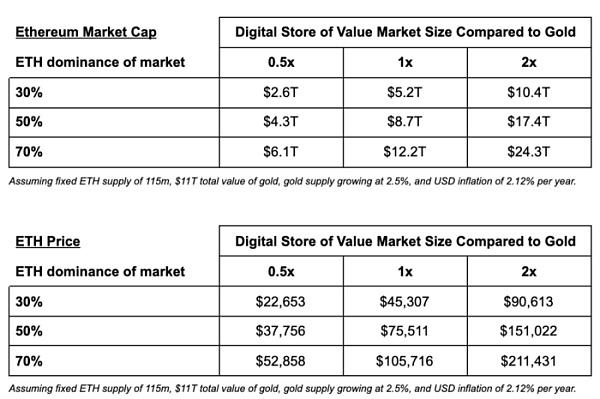

- The global digital store of value market may be larger than the gold market.

(1). More utility and accessibility can expand market size ------ Today, the total supply of gold above ground is valued at about $11 trillion³. Valuable digital stores reduce friction, provide better access and programmability, which could increase the total market size compared to gold.

Using the example of U.S. taxi and limousine services and Uber, this is an imperfect but relevant comparison. In 2009 (the year Uber was founded), the U.S. taxi and limousine service market was $9.4 billion, growing at a compound annual growth rate of 3.2%.

By 2021, after companies like Uber improved the user experience, the U.S. ride-hailing and taxi market grew to an estimated $47 billion, with an estimated compound annual growth rate of 11.7%.

(2). Investors are concerned about inflation, increasing demand for quality stores of value ------ With record levels of money printing in 2020, many believe that inflation and/or fears of inflation could drive up the prices of fixed supply assets.

(3). The younger generation prefers to hold cryptocurrencies over gold ------ While an estimated 12% of Americans hold gold, among millennials with savings over $50,000, 25% already own some form of cryptocurrency, and an additional 42% are interested in purchasing cryptocurrency.

If ETH becomes the leading digital store of value, it could gain immense value (even as the runner-up to BTC).

Our approach to this framework is to:

Provide a range of total market size for digital value storage compared to gold

The proportion of that market that ETH could capture.

Observations on Comparing ETH to BTC

BTC has already dominated the market, and network effects may prevent other cryptocurrencies from gaining market share.

Concerns about energy-intensive mining operations may favor chains with proof-of-work alternatives.

It remains unclear whether there can be two "gold" currencies or if digital value storage is a winner-takes-all market. The precious metals market suggests that leading stores of value can capture up to 70% of market share.

Viewpoint 3: Ethereum is a Payment Network

Like a payment network, Ethereum has millions of users paying fees to process their transactions. If Ethereum becomes a standalone global payment network, we can assess its value by estimating its transaction volume and transaction fees (validator revenue) and comparing it to existing payment networks like Visa and Mastercard.

When estimating possible transaction volumes and fee ranges, we considered the following factors:

In the 12 months ending December 2020, Visa⁶ and Mastercard⁷ processed $17.7 trillion, with an average transaction cost of 2.5% to 3%.

As of October 2020, Ethereum's transaction volume (including ERC20 tokens) was $989 billion, with transaction spending of $1.64 billion (0.17% of transaction volume).

In May 2021, Ethereum processed stablecoin transactions worth $20 billion to $30 billion daily ($7.3 trillion to $11 trillion annual run rate) and about $10 billion daily in ETH ($3.7 trillion annual run rate), with average miner revenue of about $60 million per day ($21.9 billion annually). Fees from stablecoins and ETH accounted for about 0.16% of transaction volume.

As of Q4 2019, the PE multiples for Visa and Mastercard were 38 and 37, respectively. We use pre-pandemic multiples as more "typical" multiples.

We can estimate a range of potential Ethereum network value by assuming a 37x price-to-earnings ratio and inferring fees from transaction rates and volumes.

Again, our goal is not to assert ETH's potential value. The idea is to build an intuition about what people must believe to justify ETH having certain potential value in the future. Is it more reasonable to think Ethereum's transaction volume could reach $5 trillion or $30 trillion? Are fees more likely to drop to 0.5% in a timely manner or all the way down to 0.01%?

Differences Between Ethereum and Payment Networks

Ethereum has a native currency, which differentiates it from today's payment networks. If users need to hold ETH to use the network, Ethereum's valuation may differ from that of payment networks.

Ethereum can handle more than just simple payments: it is a platform capable of computing very complex financial contracts.

Ethereum is non-jurisdictional and cross-jurisdictional, so users may be willing to pay a premium for a non-sovereign solution.

Viewpoint 4: ETH is a Productive Financial Asset

The transition to PoS will allow validators to generate cash flow with their capital, meaning ETH will have value as a productive financial asset. To create a cash flow model, we considered the following points:

Transaction fees and block rewards may represent substantial revenue ------ Fees paid to miners grew from $46 million in 2019 to $630 million in 2020, exceeding $2.4 billion in Q1 2021.

Future average transaction fees may decline compared to Q1 2021 ------ Reduced fees mean lower revenue for validators, and adoption may accelerate as high fees deter users.

Proof of stake profitability will be higher than proof of work ------ The upcoming transition to proof of stake, if successful, will no longer require highly specialized, expensive machines to mine transactions, nor the energy-intensive PoW machines. For simplicity, we assume a 100% profit margin.

Here are two frameworks for estimating the price of ETH based on future cash flows:

Discounting all validator income cash flows generated from 2021 to 2050 to estimate the net present value of ETH today.

The price-to-earnings multiple of Ethereum's revenue in 2030.

Method 1: DCF of validator income and net present value of the Ethereum network.

(Translator's note: DCF stands for Discounted Cash Flow, which evaluates the value of an asset based on the present value of its future cash flows.)

Method 2: PE multiple of transaction fee income and the value of the Ethereum network in 2030.

(Translator's note: PE multiple refers to the price-to-earnings ratio, which generally indicates that a lower PE is better, meaning a shorter time period for investors to recoup their investment.)

Challenges in Estimating Future Cash Flows

The impact of Layer 2 changes on average transaction fees and transaction volume is unclear.

Given the volatility of cryptocurrencies, the market may demand a higher discount rate.

Today's cryptocurrencies are highly speculative, and their price-to-earnings ratios may differ significantly from those of traditional financial assets.

There is significant regulatory uncertainty that could lead to dramatic changes in adoption rates.

Viewpoint 5 (a): Ethereum is a Digital Nation

In many ways, Ethereum resembles a nation. It has citizens (wallets and users), a government (the Ethereum Foundation), a currency (ETH), companies (DAOs and Dapps), financial markets (DeFi), and relationships with other digital nations (bridges between different chains).

In this comparison between Ethereum and a nation, one can compare the velocity of Ethereum's currency circulation to that of other countries, where currency velocity is the ratio of nominal GDP to the money supply (M1, M2). To do this, we need to:

Define Ethereum's GDP.

Define Ethereum's money supply.

Measure the ratio of money supply to GDP in different countries.

Estimate what Ethereum's GDP might be in 2030 to calculate the potential value of the network.

Defining Ethereum's GDP

Three examples of goods and services produced and sold on Ethereum today are miner revenue, DeFi revenue, and NFT sales. The simple annualized GDP year-to-date for these three categories is $3.7 billion, $2.7 billion, and $8 billion, respectively, indicating a GDP of $14 billion for 2021. There is reason to believe these numbers will continue to grow:

- Miner revenue growth

- DeFi volume is growing

- NFT sales are continuously increasing

- In the future, other products and services may be produced and sold through Ethereum. For example, NFTs could technically be created and sold years ago, but they only recently took off. Similarly, in the 1990s, few could imagine that the internet would one day facilitate billions of video calls, video streaming, and other bandwidth-intensive applications.

Defining Ethereum's Money Supply

If Ethereum is a nation, then ETH is its money supply. The ETH supply is most similar to a country's M1 supply (the coins and paper money in circulation, along with other assets easily convertible to cash). However, unlike traditional banking systems, the supply of ETH is limited and cannot be created by commercial banks using their reserves to create loans.

Thus, while ETH is definitionally most similar to M1, we use M2 related to GDP in our framework.

(Translator's note: M2 refers to the broad money supply, which includes cash outside the banking system plus business deposits, household savings deposits, and other deposits. It encompasses all forms of money that could potentially become real purchasing power, typically reflecting changes in total social demand and future inflationary pressures.)

In a country, M2 consists of:

All currency held by the public

Demand deposits

Savings deposits

Small time deposits (under $100,000)

And retail money market securities.

Ethereum already has similarities to M2 components:

ETH and DAI in user wallets are currency held by the public.

ETH and tokens in exchange wallets are similar to demand deposits.

DeFi products like Yearn and Curve are savings deposits.

Locked DeFi deposits are time deposits.

DeFi products like Aave and Compound are money markets.

Measuring the Ratio of Money Supply to GDP in Different Countries

Countries have different dynamic relationships between money supply and GDP. We looked at the M2 to GDP ratios of several countries to create a range for our assumptions.

Figure: GDP of various countries/regions

We can use the comparability of M2 money supply and a range of GDP assumptions to calculate different scenarios for Ethereum and its programmable currency:

The challenge of this approach is that no one knows how much GDP Ethereum will create. There are many competing chains, each of which could capture a significant portion of its target industry. For example, consider NFTs as an area where Ethereum faces competition. NBA Top Shot is one of the largest NFT markets, built on the Flow blockchain rather than Ethereum.

In fact, meaningful GDP could be achieved solely through financial services and DeFi.

Viewpoint 5 (b): ETH Will Become a Global Digital Reserve Currency

Recently, two notable catalysts could trigger a shift in reserve currency and support limited-supply cryptocurrencies:

The emergence of new fiat currencies increases inflationary pressures on fiat currencies.

Growing global distrust in institutions.

Data from Pew, Gallup, and Edelman indicates that many people around the world have lost faith in the institutions that underpin modern society—such as the media, public schools, and banks. This is not a side effect of the internet in the 1990s or social media in the 2000s. Trust in all these institutions has been declining since the 1960s.

On average, the status of reserve currencies has lasted for 100 years.

Historically, transitions of reserve currencies can occur in as little as 20 years. For example, gold went from being the preferred reserve currency, accounting for 60% of central bank foreign exchange reserves in 1980, to about 15% by 2000, while the dollar grew from around 28% to 60% during the same period.

Similar shifts occurred when the pound lost its reserve currency status after World War I, as well as with the French livre and the Dutch guilder before that. The status of these three currencies as reserve currencies lasted about 100 years.

Why Cryptocurrency, and Why ETH?

Cryptocurrencies are important because they possess the intrinsic properties of good money: they are durable, portable, divisible, uniform, and often have limited supply. When considering reserve currencies, we also need to consider three emerging characteristics: global demand, acceptability, and status as a reserve currency compared to other currencies.

Today's ETH has not yet achieved success on these three dimensions: global demand is very small compared to other currencies, even compared to BTC;

ETH is accepted as a payment method in very few places outside of cryptocurrencies; price volatility is high; other cryptocurrencies are competing with ETH; and central banks around the world are developing their own competitive digital currencies.

However, ETH stands out as a ready competitor that many businesses and nations may choose to hold in a timely manner.

- Demand for ETH is growing and diversifying:

(1). Investors want ETH to store value, earn passive income in DeFi, and invest in other crypto opportunities.

(2). Consumers want ETH to access different Dapps on the Ethereum network, buy and sell digital assets like art, gaming assets, insurance, etc., and transact with better privacy and anonymity.

(3). DeFi protocols want ETH as collateral to create other assets, such as DAI and synthetic assets, and to serve as a reserve currency to allow users to trade and raise funds.

(4). Builders and creators want ETH to accept payments from crypto users, to establish businesses that can only exist with programmable currency, and to monetize creative content without relying on platforms that may censor them.

(5). Other blockchains want ETH reserves to connect their chains to the largest ecosystem, Ethereum.

- ETH has already become the reserve currency of DeFi.

(1). On today's largest decentralized exchange, Uniswap, the amount of ETH is more than 3.5 times the total of the three most popular dollar stablecoins (as of May 2021). On Sushiswap, the multiple exceeds 4 times.

(2). By total value locked, the largest DeFi protocol is Maker, which locks over $12 billion of ETH as collateral for its stablecoin DAI.

(3). ETH is also the reserve currency for projects like Synthetix, where ETH is deposited as collateral to create synthetic assets.

(4). Over 1% (approximately $10 billion as of May 2021) of the Bitcoin supply has been wrapped for Ethereum, indicating that digital value storage and reserve cryptocurrencies require more programmability.

A currency with high demand has natural network effects, and Ethereum is first to market.

Supply growth is about to become limited, which means prices may rise with demand. Price increases help the reserve currency's network effects, as more people tend to buy and hold the currency when prices rise.

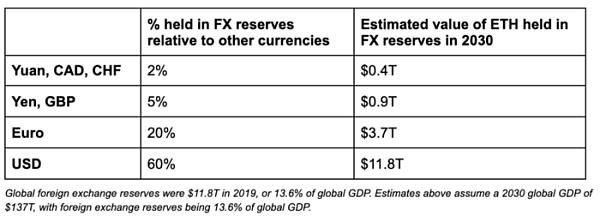

If ETH is to replace any current reserve currency, what would be the value of a global digital reserve currency by 2030? Based on its comparable reserve currency status, we can add the following amounts to the previous scenarios of Ethereum as a digital nation:

Research Needs to Note:

In the five viewpoints discussed above, four factors play a disproportionately large role in the future value of the network:

How optimistic your model is about the adoption of blockchain technology

The distribution of outcomes among different chains (winner-takes-all, power law, or fragmentation)

Network fees

The cash flow multiple the market is willing to pay

Original link: https://mp.weixin.qq.com/s/vHOWtu6SFv_x0ZzQ6ZJYhQ