Bitcoin is not a currency; it is a new type of financial game

It is clear that BTC is not a virtual currency that can be issued and dominated by a single company; it is more like a commodity, as well as an asset and property right.

It is clear that BTC is not a virtual currency that can be issued and dominated by a single company; it is more like a commodity, as well as an asset and property right.This article is sourced from CryptoYC Labs.

JP Koning once published a blog post summarizing the mechanisms that prevent chain letters from sustaining themselves in the two old eras (the mail era): the Problem of Dishonesty and the Problem of Non-Fungibility. This article argues that Bitcoin, as a new type of "chain letter," perfectly solves these problems.

Chain Letters: A Hierarchical Game Based on Social Networks

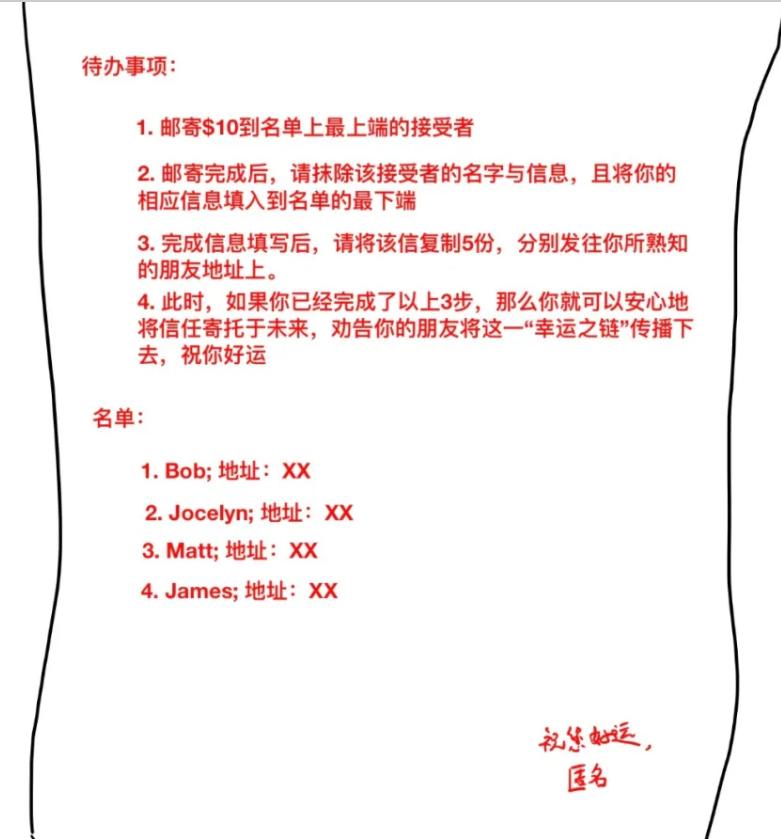

Let's play a game called "Chain Letter."

Imagine one day you receive a letter that says: "Hello, this is a letter from the 'future.' If you sincerely and truthfully follow the instructions below, you will receive compensation in the near future, bringing you exponential returns. So, boldly invest in your 'future'!" Then, on the back of the letter, you find a to-do list and a list of names.

In fact, many people might be reluctant to fall for this at first, but it's just a matter of $10—how much of a sacrifice could that be? Some might take a gamble and go along with it. However, those who are a bit smarter will realize: the potential returns can be calculated; as the chain spreads, the list will automatically shrink, and your name will appear at the top, receiving payments from others. So, let's calculate the potential returns.

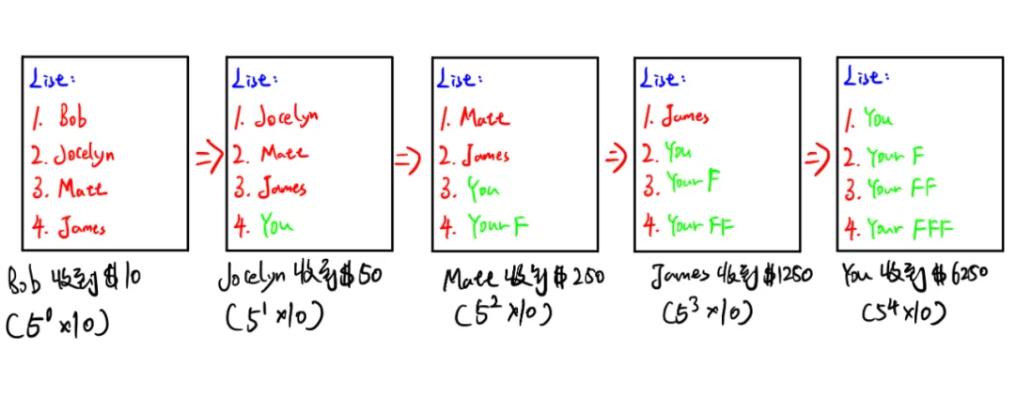

Initially, the list you receive consists only of Bob, Jocelyn, Matt, and James—four unrelated people. According to the game rules, Bob will receive your $10, but what about Jocelyn, Matt, and James? When you place your name at the bottom, the five friends who receive your letter will each send $10 to Jocelyn according to the second list, resulting in a total of $50 (5^1 X 10).

Using the same calculation, Matt will receive $250 from 25 strangers ($10 each), which is $250 (5^2 X 10); James will receive $1250 from 125 strangers ($10 each), which is $1250 (5^3 X 10); finally, when it’s your turn to reach the top of the list, you will receive $6250 from 625 strangers ($10 each), which is $6250 (5^4 X 10).

At this point, you might be surprised that you only spent $10, yet it could potentially yield $6250. Where does all this extra money come from? How does this happen? Starting from the second list, your friends (Your F) begin sending money to Matt.

In the next round, your friends' friends (Your FF) send money to James, and finally, when it’s your turn at the top of the list, it’s your friends' friends' friends sending you a total of $6250.

Yes, this is fundraising from 625 strangers, and apart from that, no additional value is created. They are just like you, willing to take a small risk for a larger reward, participating in this game.

But the most important principle is that this game is based on zero-sum game rules. In other words, your profit is someone else's loss, and for individuals, it’s just a $10 loss; ultimately, due to the game rules, a powerful trickle-up effect is formed, bringing exponential returns to players at the top of the list.

This is an exponential reproduction, based on a base of 5! However, this terrifying reproduction process is built on two important assumptions:

- The recipients voluntarily participate in the game, and the cost of trust is ignored, meaning the trust cost is zero;

- Every participant in the game deletes names and sends emails according to the rules, with no one privately altering the order of the list to benefit themselves and exit early, meaning no one cheats.

If we do not have these two assumptions, chain letters in reality would quickly stop reproducing. If there are no subsequent participants investing money and the chain of propagation breaks, early birds profit while latecomers lose.

On one hand, the first assumption indicates that the operation of this game heavily relies on personal credit networks. If I am the propagator, I have a profit incentive to persuade my friends to trust it, thus securing my future returns, but this carries a certain probability. On the other hand, the second assumption indicates that the game rules are fragile. Even if I can persuade my friends to participate, I cannot guarantee they won’t cheat and quietly remove my name to replace it with theirs.

JP Koning once published a blog post summarizing the mechanisms that prevent chain letters from sustaining themselves in the two old eras (the mail era): the Problem of Dishonesty and the Problem of Non-Fungibility, and he argues that Bitcoin, as a new type of "chain lock," perfectly solves these problems.

- Problem of Dishonesty

In chain letters, this problem means that some people maliciously alter the list in the letter or create false information within the list to attract more funds, or some may not send money but merely forward the letter to profit. These are all acts of dishonesty from individual nodes.

- Problem of Non-Fungibility

Similarly, when I am at the top of the list, I am the safest and quickest to receive returns. In other words, the lower the level, the more likely participants are to encounter a break in the chain letter, increasing the probability of failure. Therefore, there is a risk premium based on hierarchical ranking. Additionally, I cannot sell this ranking position to others for profit, meaning it is non-fungible, and I cannot create a market; I can only patiently wait to reach the upper levels of the list.

Despite this, "the greatest technical advantage of chain letters lies in their decentralization. Each node or participant is independently responsible for receiving, copying, updating, distributing, and marketing the chain letter. Without a central planner to prosecute, it is nearly impossible for authorities to stop its spread." However, with fewer new participants, latecomers, and those at lower levels losing their initial investments, the chain will break and disappear.

Therefore, we can call chain letters a hierarchical game based on social networks.

Bitcoin: A Non-Hierarchical New Financial Game Based on Price Ranking

Back to Bitcoin.

At this point, we notice that Bitcoin believers often chant HODL (hold on for dear life), which is quite similar to the participants in the chain letter! Thus, in the following article, I will reanalyze the intrinsic price logic of Bitcoin from the perspective of financial games, dispelling the myth that it is merely "currency."

As early as 2018, JP Koning, a long-time researcher of central banking, noticed that Bitcoin closely resembles a chain letter. Of course, it is well-known that chain letters, due to their strong infectiousness and fundraising ability, have long been classified by many governments as being on the same blacklist as Ponzi schemes and pyramids, all sharing the commonality of being zero-sum games, with distribution determined by entry order, having a hierarchical degree of advantage and disadvantage, and the rule of early birds eating late birds.

The dishonesty problem in chain letters corresponds to the double-spending problem, which has never occurred to date, as miners ensure the security of data on the chain. However, regarding the non-fungibility problem, Bitcoin proposes a completely different solution: as described in its white paper, Bitcoin was designed from the beginning as a peer-to-peer payment system, capable of holding, transferring, and trading. In this process, my 1 BTC and your 1 BTC have exactly the same properties, making BTC fungible.

This payment system is like a giant airplane, where the "seats" have been manufactured early on (the seats, which total a constant number of 21 million Bitcoins), and each seat is physically equal and allowed to be bought and sold (the amount of BTC and its corresponding public key are written into the block).

At the beginning, this system, like fiat currency, indeed had no intrinsic value. When you buy and hold at a certain price, the system automatically locks your "seat," which is merely a segment of unchangeable code on the chain, and this has nothing to do with the price you bought in at.

Yes, the price you buy in at has nothing to do with this payment system; your price is entirely determined by market participants, reflecting a collective expectation of future returns. Thus, in the earliest days of Bitcoin, with few participants, Bitcoin was nearly worthless because the collective expectation of returns was still very low. (In May 2010, a programmer named Laszlo Hanyecz famously used 10,000 BTC to buy two pizzas worth about $20 from Papa John.)

Of course, in BTC, there is no distinction between first-class and second-class seats; only the purchasing power determines the level.

Bitcoin, as an investment tool, is fundamentally different from stocks and bonds. Stocks have dividends and a socially fair fundamental value, reflected in the present value of a company's future cash flows, while market fluctuations around this fundamental value represent speculative value.

Similarly, bonds have legally binding interest redemption commitments, and their fundamental value is also based on the discounted cash flows of creditors. However, Bitcoin is not a debt; it is an asset without creditors, much like gold. As the father of value investing, Benjamin Graham, said: "In the short run, the market is a voting machine, but in the long run, it is a weighing machine."

For Bitcoin, it does not possess any self-capital regeneration ability to reflect its fundamental value; it is purely a voting machine.

Apart from the funds provided by investors themselves, there are absolutely no other sources of income. Therefore, it is a financial game that resembles a chain letter: the profits of early buyers are built on the interests of later investors, with everyone hoping to cash out before a collapse. In my view, BTC is a 100% zero-sum voting machine, the world's first giant "Keynesian beauty contest" that anyone globally can easily participate in!

It is precisely for this reason that the new SEC chairman Gary Gensler stated: "Bitcoin came into existence as mining began as an incentive in validating a distributed platform…is not a security."

Clearly, BTC is not a virtual currency that can be issued and dominated by a single company; it is more like a commodity, as well as an asset and property right. In terms of regulatory guidelines, it also categorizes virtual currencies into utility tokens and security tokens, which have been recognized as distinguishing standards, further regulating ICOs in the future.

However, even if BTC becomes a commodity, why has the price of Bitcoin surged so dramatically? It has been 10 years since Bitcoin Pizza Day, and while Papa John continues to operate globally, BTC has soared to $60,000, with its market capitalization rising from less than $10 billion in 2017 to $100 billion in 2019, and reaching $200 billion in September 2020, skyrocketing to $1 trillion in April this year.

No other asset's price increase can compare to Bitcoin's. To explain this, I will use the earlier example of the airplane.

If this giant airplane has only 20 seats, the average price of the top ten seats might only be $20, while the average price of the 10th to 12th seats might be $80.

At this point, with few participants and low pricing, it is held and promoted by the main believers. However, as Bitcoin enters the public eye and is "discovered for its value" ("Blockchain, as an advanced technology," "a secure and efficient payment system"), the 12th to 18th seats are snatched up by a flood of incoming funds, with an average purchase price possibly reaching $500.

A few years later, Bitcoin attracts mainstream capital ("Bitcoin, gradually maturing as a value-saving tool," "a high-return asset for hedging inflation"), and the average price for the last two seats might be $1,000. First, this example is merely used to clarify the internal price logic and implies an assumption: that everyone is a long-term holder, and once they hold, they can resist the temptation of asset price increases and do not sell their BTC. Thus, we would have a graph like this.

From the graph, we can see that when the final market price rises to $1,250, new buyers purchasing at this price have an average asset inflation level of 0, while players who bought in at $10 have already seen their asset inflation level increase by 125 times.

In other words, if you believe that Bitcoin will become popular worldwide and you can obtain a quality price, then go ahead and buy boldly! Because your returns are always built on the backs of later participants. Early birds buying and holding at a specific price have expectations of future returns, and in this zero-sum game, these expected returns are entirely determined by the bidding of later participants.

In this bar chart sorted by price, we can clearly see that Bitcoin has transformed the hierarchical list order of traditional chain letters into a non-hierarchical price order, yet it remains a game where early birds eat late birds, and this game has a strong self-reinforcing effect and long-tail effect.

These two very special effects, unique to our era, permeate every transaction in this game, and their crazy price increases and daily fluctuations drive more outsiders to participate.

Thus, this is a game that everyone can access at any time, a 7x24 hour global casino, a peer-to-peer payment network that keeps sovereign entities at bay, a non-hierarchical new financial game based on price ranking.

Or, as Zoltan Pozsar described it, "the reincarnated dollar silver bank"… Yes, no matter how you want to describe it, whether you hate it or love it, it will always be there, and its lifespan can easily outlast the bull and bear markets in the real world, possibly even longer than sovereign nations. So, in my view, it is an incredible invention.

At the end of the article, I would like to quote a passage from JP Koning to conclude this article.

"You might ask, what principle motivates Bitcoin to become electronic cash? One of the biggest tricks played by Bitcoin's creator, Satoshi Nakamoto, is to persuade everyone that his invention is like a banknote, while it is actually a new type of zero-sum financial game.

Zero-sum games are too unstable to serve as a basis for a universally accepted medium of exchange. However, even if it has never been widely recognized as a 'stable price' currency, that does not mean Bitcoin lacks other advantages. If we should be grateful to the inventor of poker, perhaps we also owe a debt of gratitude to Satoshi Nakamoto."