The essence of the Uniswap and SushiSwap rivalry: Who can bring greater returns on funds?

Uniswap attempts to improve the capital efficiency of its LPs through mechanisms such as "concentrated liquidity," while SushiSwap leverages horizontal expansion methods like lending and universal vaults.

Uniswap attempts to improve the capital efficiency of its LPs through mechanisms such as "concentrated liquidity," while SushiSwap leverages horizontal expansion methods like lending and universal vaults.This article was published on Blue Fox Notes.

Earlier this year, Blue Fox Notes wrote about “Uni Left, Sushi Right,” and it is now basically developing in that direction. The two have taken different development paths. Uniswap is deeply exploring AMM, while Sushiswap is horizontally exploring more areas (such as lending, crowdfunding).

The Puzzle of Sushiswap

Currently, Sushiswap's puzzle includes DEX (multi-chain AMM, not only Ethereum but also BSC, Heco, etc.), Kashi lending and margin trading, BentoBox, crowdfunding platform MISO, and more. Some of these pieces have their own ideas.

Sushiswap's puzzle, Sushiswap

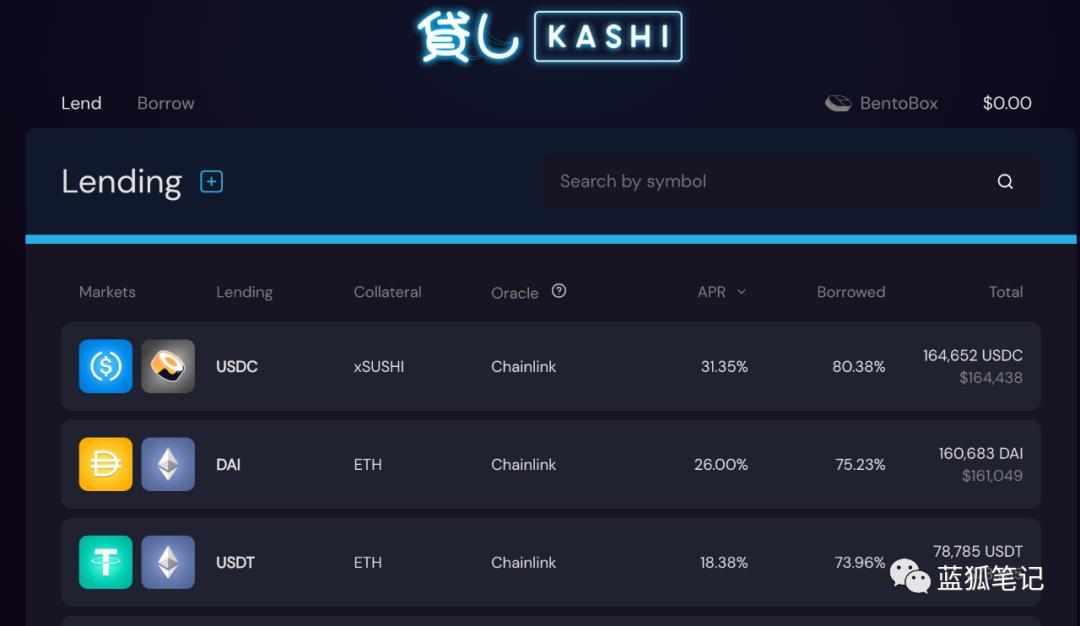

Kashi

Kashi is the first major horizontal expansion in the Sushi puzzle. It is a lending and margin trading platform.

Sushiswap's Kashi, Sushiswap

Unlike Compound and Aave, Kashi adopts a "isolated" lending pair model. In Compound and Aave, not all assets are eligible to enter their platforms. Once an asset enters their platform, users can deposit collateral and use it to borrow various other assets on the platform. In this model, its asset pool has integrity. If an asset suddenly drops significantly, the entire protocol will bear the corresponding high risk. For example, currently, Compound has a total of 9 assets including ETH, DAI, USDT, Comp, 0x, etc. Users can deposit any of these 9 assets (such as BAT) and borrow any of the 9 assets (such as USDC) based on the corresponding collateral ratio. If BAT drops significantly, it will affect the entire protocol.

Kashi does not copy this lending model but adopts a token pair model similar to DEX, where each lending pair is mutually isolated. For example, the RUNE/SUSHI lending pair. Users deposit one token and then borrow another token. This means that if one lending pair encounters a risk event, it will not affect other lending token pairs. Through this model, Kashi achieves risk isolation.

Kashi's interest rate design is also dynamically adjusted based on its target asset utilization rate. Its current utilization target is around 70-80%. If there is a significant deviation, its interest rates will fluctuate greatly. For example, if the utilization rate reaches 100%, its interest rate will double every 8 hours; if it is only 0%, it will be halved every 8 hours.

Moreover, Kashi V2's design introduces two important points: first, anyone can create their lending pairs. This effectively opens the lending market to users, which logically may lead to a larger market scale. How this will evolve in practice remains to be seen. Second, users can go long or short on various assets, and it will allow users to do so as long as they have sufficient collateral, even utilizing flash loan features.

From the above plans, Kashi aims to follow a different model from the current mainstream lending, attempting to take a more community-oriented grassroots approach. Additionally, its addition of margin trading is also beneficial for improving asset utilization, thereby attracting more users.

Furthermore, for Sushi token holders, a point of concern is whether Kashi can capture value for Sushi tokens. Kashi's lending income mainly comes from the interest paid by borrowers and liquidation profits. Of this, 90% goes to asset providers (lenders), 1% to Kashi developers, and the remaining 9% is distributed to xSushi holders.

BentoBox

BentoBox was originally a treasury for lending protocols, but it has since extended to serve as a treasury for all dApps. The treasury of BentoBox comes from various assets deposited by users. Once users deposit their funds into BentoBox, various protocols can utilize these assets. In other words, BentoBox has become a treasury for various dApps. Kashi is the first lending protocol built on BentoBox.

Sushiswap's BentoBox, Sushiswap

There are several benefits to pooling user funds together:

Reducing Transaction Costs

Currently, the cost of approving token usage across various protocols is high; each time a new protocol is entered, approval is required, which incurs significant costs. All dApps based on the BentoBox protocol can save this cost; users need to click to authorize but do not need to pay gas fees. This means that tokens only need to be approved once to be used across all protocols on BentoBox, allowing dApps based on BentoBox to avoid multiple authorization fees.

This is beneficial for users to deposit their funds into BentoBox, for users to use dApps based on BentoBox, and for Sushiswap to retain users.

Improving Capital Efficiency

Since BentoBox's treasury is open to various protocols, it can develop various user scenarios based on it, logically bringing various potential benefits to users. For example, based on BentoBox, there can be not only lending services but also margin trading, options, wealth management, and more.

Additionally, if the treasury funds on BentoBox are idle, it can also earn fees by providing liquidity for SushiSwap. This means that users who deposit funds into BentoBox can not only earn returns from a specific protocol but also potentially earn from providing liquidity or other wealth management services. For instance, Kashi users who deposit funds into BentoBox can earn Kashi's lending returns and may also earn from providing liquidity or other wealth management services.

Of course, BentoBox requires a positive cycle within its ecosystem. The more funds users deposit into BentoBox, for example, initially driven by Kashi, the greater the attractiveness of developing dApps based on BentoBox, which will encourage more protocol developers to consider building various dApp applications based on BentoBox's treasury. This essentially benefits the Sushi ecosystem, as it will bring more users and generate more revenue, thus forming a larger ecosystem.

Therefore, from this perspective, Kashi and BentoBox are key to whether Sushiswap can shed the Uniswap label in the future. If Sushi succeeds in this endeavor, Sushiswap's character will undergo a complete transformation. It will move towards a ubiquitous DeFi ecosystem, rather than just being a DEX.

Issuance Platform

This point was also introduced by Blue Fox Notes in “Sushi's MISO: Expanding DeFi Boundaries,” which is a platform for issuing new projects. Compared to various independent IDO platforms, as long as Sushiswap is slightly better in mechanism and has a closer connection with its platform (for example, providing token incentive support), then its attractiveness for new project issuance may surpass current IDO platforms.

The importance of an issuance platform for a community-rooted DEX like SushiSwap is greater than for Uniswap. This is another puzzle that Sushiswap needs to get right.

The Essence of the Uniswap and SushiSwap Rivalry

Uniswap is currently the king of AMM model DEXs on Ethereum. This is indisputable, whether in terms of trading volume, locked asset amount, or others.

Uniswap has also launched its V3 roadmap and plans to go live soon. Among them, the most impressive is its mechanism designed to enhance LP's capital efficiency. It introduced the concept of "concentrated liquidity," allowing LPs to customize the price range for providing liquidity. Logically, this mechanism will greatly improve LP's capital efficiency. This is indeed impressive in the DEX of the AMM model.

If successfully implemented, will this have an impact on Sushiswap, Curve, Balancer, etc.? After all, funds will flow to more efficient places. This will put certain pressure on other DEXs.

However, "concentrated liquidity" is not perfect; one of the issues is that due to its flexibility, it requires LPs to customize settings and actively manage funds, as once the set price range is exceeded, their funds will be idle. Not all LPs have the time to specifically make such settings. If some LPs are unwilling to actively manage, perhaps SushiSwap is more suitable for these fund providers.

However, this is not the core of the issue; it is not the essence of the Uniswap and Sushiswap rivalry. The essence of the rivalry between SushiSwap and Uniswap is who can bring greater returns to funds and who has higher efficiency.

Uniswap's approach is focused on enhancing AMM, improving LP's capital efficiency through mechanisms like "concentrated liquidity." This is a depth strategy. On the other hand, SushiSwap aims to enhance capital efficiency through lending (Kashi) and a universal treasury (BentoBox). This is a horizontal expansion strategy.

From the current situation, Uniswap has a deeper user base and network advantages, making it the undisputed winner. However, if Sushiswap can achieve higher capital efficiency through Kashi and BentoBox, it is not entirely without the opportunity to reverse the current situation.

For LPs, is it more profitable to provide liquidity on Uniswap? Or is it more profitable to deposit funds in Sushiswap's BentoBox? If, in practice, providing funds on SushiSwap is more efficient and yields higher returns, then why wouldn't they deposit their funds into the SushiSwap ecosystem? Conversely, if BentoBox fails to prove itself, then its funds will flow to Uniswap, further widening the gap between the two.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles