How does Liquity achieve a 110% collateralization rate and more efficient capital liquidation compared to MakerDAO? | DeFi Catcher

Liquity has advantages such as not requiring auction bots, no governance, and low collateral rates.

Liquity has advantages such as not requiring auction bots, no governance, and low collateral rates.This article is an original piece by Chain Catcher, authored by Loners Liu.

Stablecoins serve as the cornerstone of the DeFi world, with the stablecoin DAI generated by MakerDAO being integrated into almost every existing DeFi application. However, after the events of March 12 last year, the premium issue of DAI and MakerDAO's inefficient liquidation mechanism reflected its vulnerabilities. In May last year, Robert Lauko, a former blockchain researcher at Dfinity, designed a lending protocol called "Liquity" based on Ethereum, which includes automated instant liquidation, target price anchoring without manual governance, and a liquidation collateral ratio of only 110%.

The Liquity team released the latest version of its white paper in February this year, which has undergone significant changes in mechanism design compared to the first version. Chain Catcher interprets the latest white paper and combines it with practical experiences from the testnet to introduce this issue's DeFi catcher project, Liquity.

1. Background and Introduction of the Liquity Protocol

Current lending protocols typically charge borrowers interest rates to maintain the peg of issued stablecoins, which may lead to short-term high rates that are unfavorable for borrowers. Generally, governance token holders need to manage the economic parameters of their systems (e.g., setting rates) to achieve the best interests of the protocol. In practice, on-chain governance has always been a challenging and controversial topic, with most users participating in voting primarily for governance rewards.

Moreover, due to the design of collateral auctions and fixed-price liquidations, lending protocols often require users to over-collateralize, further resulting in low capital utilization. Finally, due to the lack of direct arbitrage cycles, stablecoins generated by various protocols typically cannot be redeemed at face value and cannot guarantee fixed prices.

Liquity, on the other hand, has advantages such as no need for auction bots, no governance, and low collateral ratios. Users can autonomously complete operations such as collateralization and redemption through the Liquity protocol. In terms of liquidation, Liquity is divided into three parts: stable pool liquidation, debt redistribution, and global liquidation.

Liquity announced the completion of a $2.4 million seed round financing led by Polychain Capital in September last year, with participants including a_capital, Lemniscap, and 1kx. Liquity was developed by a small team of five, with founder Robert Lauko being a former blockchain researcher at Dfinity, and early employees including Ashleigh Schap, who previously handled business development at MakerDAO.

2. Main Advantages of the Liquity Protocol

1. Zero Interest Rate

Unlike Maker, Liquity does not have a stable fee/interest rate mechanism; however, minting users need to pay a one-time issuance fee and a one-time redemption fee when redeeming collateral. Chain Catcher tested the issuance on its Kovan testnet, where the current one-time issuance fee is 10 LUSD (LUSD is a stablecoin pegged to the US dollar, used to pay loans on the Liquity protocol), equivalent to $10.

However, redeeming the underlying asset Ethereum is not unconditional; this fee is generated based on a specific algorithm, as shown in the figure below:

In general, the redemption fee is related to two variables: one is the time interval since the last redemption operation, and the other is the percentage of the amount of LUSD redeemed relative to the total issuance. In other words, the shorter the time interval since the last redemption operation, the higher the fee, which gradually decays as the interval since the last redemption activity lengthens, ultimately approaching zero. The higher the percentage of LUSD redeemed relative to the total issuance, the higher the fee paid. Each generated redemption fee will be deducted from the redeemed collateral asset ETH.

To incentivize the growth of the stable pool's scale, the system will reward core contributors in the system with part of the revenue in the form of growth tokens (GT). In the Liquity system, core contributors refer to third-party front-end developers and LQTY providers in the stable pool.

As a protocol layer, Liquity will outsource the front-end operation interface to third parties and attract multiple third parties to provide development based on an incentive model (which has not yet been finalized). Anyone can participate, and in return, they can receive growth reward tokens GT, which follows a deflationary model with halving occurring once a year.

2. 110% Ultra-Low Collateral Ratio

Initially, Liquity's official design strictly executed commands in the liquidation process, triggering liquidation only when the collateral ratio fell below 110%, providing better security for borrowers' funds.

However, on the Ethereum mainnet, if liquidation is strictly conducted according to the collateral ratio, attackers can create many small collateral Troves (vaults for storing collateral, similar to Maker's Vault) and block the system by slowing down the liquidation order. Currently, the Ethereum gas limit is 12.5m; unless a minimum size limit is set for the collateral amount, even if Liquity allows for a maximum of 90-95 Troves to be liquidated at once, it will still be unable to liquidate collateral in a timely manner due to network congestion.

Given that the Liquity system heavily relies on fast and effective liquidation, the design of the liquidation system allows for the liquidation of any number of Troves. In extreme market conditions, liquidation bots will prioritize larger Troves, while smaller Troves can remain unliquidated for a longer time. For a lending protocol, what matters is not the quantity of liquidations but the amount of outstanding debt.

3. Debt Warehouse Transfer

If the LQTY in the stable pool is completely consumed during liquidation, Liquity will automatically transition to the second phase of liquidation. In this phase, the system will redistribute the remaining under-collateralized "vaults" to all existing "vaults," proportionally reallocating their collateral ratios. This means that the higher the collateral ratio of a "vault," the more debt and collateral it will receive "from the liquidation position." The debt warehouse transfer mechanism ensures that the system does not experience a chain reaction of liquidations.

Assuming a very extreme situation where the overall system's collateral ratio falls below 150%, the debt warehouse transfer will not solve the liquidation problem. The system will initiate recovery mode.

4. Design of Recovery Mode

Although liquidations in liquidity are primarily conducted by offsetting a Trove's debt with the stable pool, if the stable pool is empty or entirely used up during liquidation, the system will redistribute debt and collateral. Therefore, as a second line of defense, all Troves collectively contribute to the system's solvency.

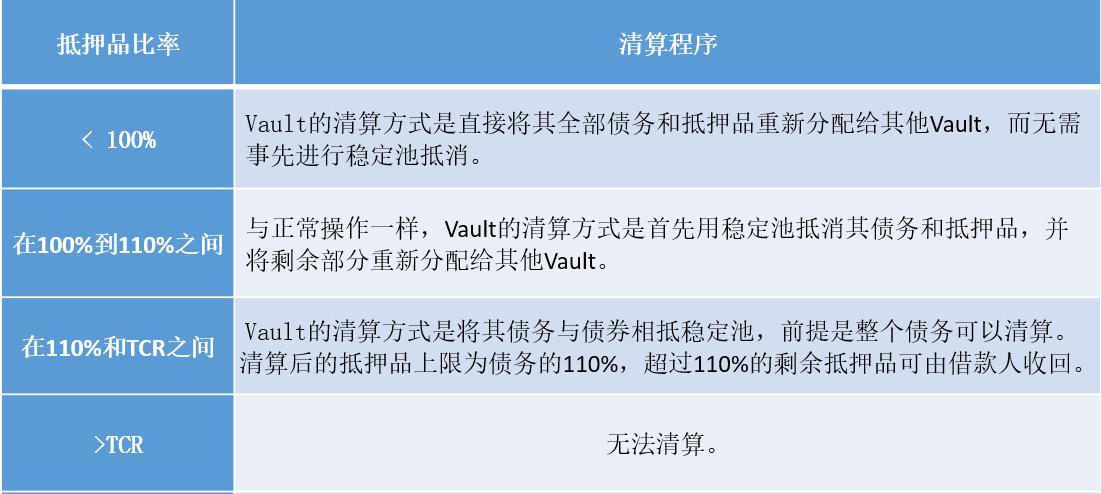

To ensure that the entire system has enough collateral to absorb liquidations, Liquity has introduced a recovery mode. If the Total Collateral Ratio (TCR) falls below 150%, this special operational mode will be triggered, extending the conditions for liquidating Troves. In recovery mode, if a Trove's collateral ratio is below TCR, it can be liquidated. In normal mode, only Troves below 110% will be liquidated.

In the initial version of recovery mode, Troves with collateral ratios as high as 150% could be liquidated. However, we changed the threshold to TCR (defined as TCR below 150%) because liquidating Troves with collateral ratios between TCR and 150% would actually worsen the system's overall collateral ratio.

After relaxing the strict liquidation order, any Trove with a collateral ratio below TCR can now be liquidated when the system enters recovery mode. The maximum liquidation loss can reach 50% of the Trove's debt, which is quite harsh for borrowers. In fact, this excessively high liquidation penalty is not a necessary condition to incentivize stability providers: as long as the trading price of LUSD is below its hard cap of $1.10, liquidation should be profitable as long as the value of the collateral being liquidated is 110% of the liquidation debt.

In recovery mode, the upper limit of liquidation losses is set at 110% of the collateral. Any remaining portion, i.e., collateral above 110% (below TCR), can be reclaimed by the liquidated borrower using the standard network interface.

This means that if a borrower's Trove is liquidated, they will face the same liquidation "penalty" (10%) in recovery mode as in normal mode. Liquidation of Troves exceeding 110% only targets the stable pool (i.e., they can be exempt from redistribution) and requires that all debts can be liquidated at once.

In recovery mode, the liquidation mechanism is described by the following rules:

These changes incentivize stability providers to increase deposits during recovery mode, thereby improving the system's overall collateral ratio.