On Reflexivity and Imitation: "Speculation is Devouring the World"

The world of Bitcoin speculation is like a video game with infinite lives, where the goal is to keep playing rather than to win.

The world of Bitcoin speculation is like a video game with infinite lives, where the goal is to keep playing rather than to win.The author of this article is Matti, translated by Babit. In this article, Matti explains the phenomenon of "speculation is consuming the world" through the theory of reflexivity, which is also happening with Tesla, Bitcoin, and DeFi.

The theory of reflexivity describes how "cognitive function" (world → thought) and "manipulative function" (thought → world) influence each other (sometimes interfering with each other). In other words, participants' perspectives influence the process of events, while the process of events influences participants' perspectives.

Imitation is the intermediary of this process, and the market is a concentrated expression of desire. Viewing the market as a universal model that people can imitate, the reflexivity of assets is essentially a side effect of imitation.

Imitation is a form of communication; humans are inherently imitative. As mentioned in the previous article, imitation allows reflexivity to shape the world according to our will; humanity cannot exist without imitation.

The corrective power of reflexivity is driven by desire, and when satisfaction is limited, desire is endless. Durant wrote:

"…… Achievement can never satisfy, nothing is more deadly than the realization of ideals."

These desire-driven pursuits keep the world in motion. When discussing desire, it is inevitable to mention money. The price signals mediating human communication are expressed in money. Desire, imitation, reflection, and money—all are interconnected.

"Everything else can only satisfy one desire; only money is absolutely good…… because it is the abstract satisfaction of every desire." (Schopenhauer)

Money regulates the information of the price system------the market. Hayek explained: "Describing the price system as a mechanism for recording changes is not merely a metaphor." In a sense, the abstract Hayekian market may be the first instance of bidirectional scalable information transmission.

The invention of computers and the internet triggered an information revolution. We find ourselves mastering the actual mechanisms of recording and creating change.

Optionality is consuming the world

When Arjun Balaji published the narrative "Speculation is consuming the world", I was the first to notice it, a rephrasing of Marc Andreessen's "Software is eating the world". Arjun's tweet (possibly) refers to the increasing number of people playing with stocks and cryptocurrencies, as well as the differences between fundamentals and valuations.

So what does "speculation" really mean?

The speculation discussed in this article refers to a practice where money is not a means to achieve a goal, but the goal itself. According to this definition, speculators are not directly trying to participate in shaping the world, but are trying to guess how the world will shape itself next.

For example, Fiskantes enters the market to buy a goat because he wants to make goat cheese. (This is more of an investment than speculation)

Su Zhu acquires all the goats because he suspects that the market's demand for Fisky goat cheese products will drive up the demand for goats. (This is more speculation than investment)

Speculators focus on signals and take action based on others' market interactions. Their primary goal is to increase money. In the above examples, Fiskantes also wants to make money, but he intends to create a product.

Thus, we can describe speculation as trading that is not directly connected to output/product. Let's look at a trickier example:

Hasu wants to buy a moderately sized house, so he seeks an investment to make money. He decides to buy and hold shares of Fisky's goat cheese.

Although people might consider this an investment, it is largely speculation. This indicates a false dichotomy between speculation and investment. Everyone engages in some form of speculative activity to some extent.

For the purposes of this article, I want to conceptualize speculation based on optionality. Therefore, when we say "speculation is consuming the world," we refer to people's preference for unlimited options, where money becomes more valuable than anything anyone could do with it.

People achieve diversification by investing in stocks like AMZN (Amazon), TSLA (Tesla), and (FiskyGoatCheese) Fisky goat cheese, as the founders and employees of these companies have relinquished (some) optionality.

If Fisky spends his time making goat cheese, he will give up some optionality but will create potential optionality for Su Zhu, Hasu, and many others. The trades that Su Zhu and Hasu engage in also create optionality for others, and so on.

What I understand by "speculation is consuming the world" is that optionality is consuming the world. This is reflected in the increasing number of people participating in the stock market and the crypto and over-financialized economy.

There is a hypothesis that computers are a major driver of optionality. To understand today's market, we will explore computers and the digital world and the relevant optionality they create.

Uncertainty breeds optionality. Then, optionality brings more uncertainty to outcomes. Uncertainty makes optionality more valuable, and so on. The more uncertain we are, the more we seek answers.

Infinite possibilities and infinite competition

Compared to the infinite temptation of imitation, the physical world's atoms seem limited. Computers and the internet are the driving forces behind mass replication and mass competition.

In the digital world of bits, replication is ubiquitous. This is reflected in two aspects: the instantaneous replication of files and code, and the replication of human behavior (and desires) towards one another.

A popular counter-narrative simplifies technology to information technology and describes the obsession with screens as a retreat inward. The phrase "software is eating the world" has become a catchphrase.

Software transcends physical attributes; it can create new worlds and connect distant places in the physical world. Thus, the speed of signal propagation in the network is faster, and the imitative and reflexive processes are also quicker.

People imitating each other leads to competition. Competition is a form of validation that ensures that a person's object of desire is genuinely worthy of their attention. Validation from peers mediates self-validation. When people do the same thing, we feel reassured.

This competition has been upgraded in the world of bits; this competition has always existed but is fundamentally non-lethal (for now).

"…… Digital networks are powerful amplifiers of existing realities…… they allow for endless conversations, and they are amplifiers of intense competition that exists between individuals…… this includes the permanent pursuit of attention, as everyone tries to become a model for others through the number of 'likes' or 'followers'." (Antonio Machuco Rosa)

Through the interface of social media, we enter a global talent show where strangers and acquaintances compete. As software permeates our daily lives, we begin to gradually turn inward, staring at screens that have become mirrors.

Before people turned computers into our (almost) entire world, computers were used to inform people about the world. In terms of the market, software initially served as an interface to enter the market. Software inevitably becomes the market, and the market inevitably becomes software.

Introducing financial markets into social media is a mimetic trap. We gain recognition not only through increasing money but also through likes. Money is likes, and likes are money.

If Schopenhauer were alive today, he might say on Twitter:

"The digital world…… is always ready to become any object defined by the desires or various wishes they wander." and "Everything else can only satisfy one desire; only computers are absolutely good…… because they are the abstract satisfaction of every desire."

By enabling uncontrolled imitation, reflexivity, and the ensuing competition, computers have also enhanced our ability to create and sustain financial bubbles.

Charlie Munger once quoted the famous "Lollapalooza effect," another name for reflexive behavior turning into financial frenzy. Imitation is the reason for the occurrence of the Lollapalooza effect:

"… Munger used public auction bidding as an example of the Lollapalooza effect. Participants are compelled to bid due to reciprocity ("I should buy because I've been invited to the auction"), consistency ("I've always said I like this, so I must buy it"), commitment bias ("I've already bid, so I must continue"), and social proof ("I know buying is good because my peers are doing it")."

Sometimes the Lollapalooza effect can produce positive outcomes, which is when the madness of the crowd manages to turn into the wisdom of the crowd. In fact, the frenzy of the internet bubble propelled the development of the internet.

As markets begin to exist in the digital realm, our ability to create Lollapalooza effects multiplies as we can actually enter the market through screens. The digital age allows for infinite competition and infinite possibilities.

A plethora of optionality and a lack of direction are hallmarks of the digital age. This means "probability and statistics are the primary ways to understand the world…… random walks define what the future looks like." In such a world, it is nearly impossible to replicate or imitate.

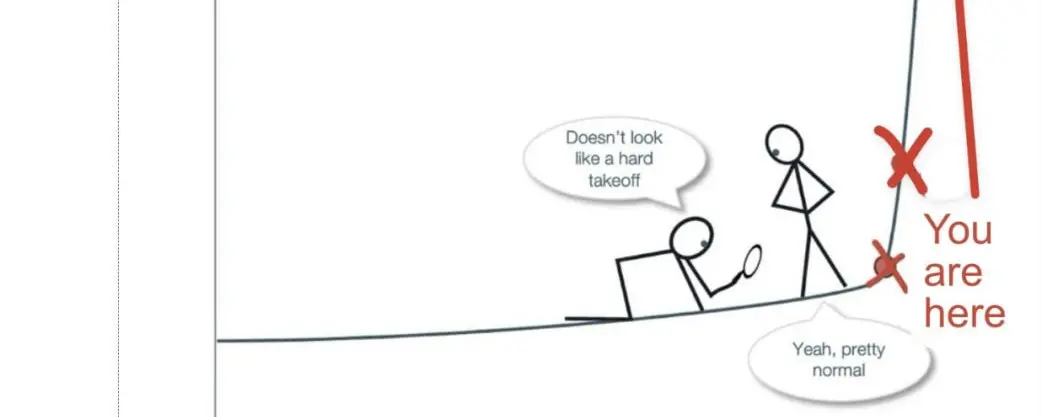

The ultimate race to the front

Competition in the digital realm is different; the games we play in the world of bits seem infinite. Like a video game with infinite lives, the purpose of this game is to keep playing rather than to win.

The modern world is more malleable (and probabilistic) than ever. That is to say, our interpretations of the world are more malleable, rather than the world itself undergoing significant changes.

So we return to the concept of reflexivity, where information flows from one thought to the world and interferes with the flow of information in another way. The barriers between price and narrative are becoming increasingly indistinct.

Preference functions, no longer correctly informed by belief functions, are melting into a shapeless mass. "Pumpamentals" become the fundamentals, prices become news, and then fundamentals (possibly) follow prices.

We are fully focused on the numbers on the screen; for those in favor of optionality, everything else is basically unimportant.

Mark Spitznagel of Universa employs a well-known tail hedging strategy that is unrelated to actual positions but is related to meta-positioning. He describes it as a roundabout approach, focusing on indirect means rather than assessing the purpose itself.

In such an uncertain world, we can only amuse ourselves. We confuse our preferences with those of others. The world becomes a Keynesian beauty contest. We try to guess what others are guessing, and then we try to guess what others are guessing that others are guessing…

Staying in the game is more important than winning. In a world of instant replication and infinite replication, the Lollapalooza effect is amplified, and it is important not to be the last one left inside.

When a person realizes the outcome of the game, timing becomes crucial. The world becomes the ultimate race to the front, where being early means being right.

People care less about the actual meaning of signals and focus more on receiving signals before others. It's as if we try to explain our own signals, changing them when we propose a new explanation, which results in further changes.

The biggest trade in trading history (perhaps of all time)

Another explanation might be that optionality is just an illusion, and all bets are merely a macro bet, as the world shrinks due to interconnection. In 2008, Thiel wrote:

"Recent extreme valuations may be an indirect measure of how narrow the road ahead of us is."

Thiel pointed out that the vision of a globalized world can only lead to two outcomes: utopia or dystopia. Crazy valuations are either signs of utter despair or blind hope born from a lack of alternatives. The meta-theory of investment in our era is digital ascendance. A less cynical way of saying it is that fundamentals follow prices.

Thiel predicted that after the impending crisis, globalization would either intensify or retreat. Separating the political agenda of globalization from globalization itself, actual globalization has not reversed.

Globalization can be understood as homogenization and replication. While the political agenda seems to be on hold, the world has not stopped globalizing or imitating.

On the contrary, imitation has intensified. To this day, the statement "the greatest investment of our time remains the investment that is most leveraged to true globalization" remains a valid and successful investment thesis.

The longer the post-2008 boom lasts (with TSLA and AMZN reaching all-time highs), the greater the urgency to abandon the old economy. Market optimism persists in the two (contradictory) main beliefs of the new economy.

First is the technological rescue brought by the talents of Musk, Bezos, and other great entrepreneurs. The second is the massive redistribution propagated through modern monetary theory (MMT) and unconditional basic income (UBI) memes.

Thiel anticipated that the 2008 financial crisis would destroy the "ideological scaffolding" of bubble formation. Ironically, we have actually doubled down, and it seems we are stubbornly moving in one direction.

The money printing machine has become unprecedentedly brutal, China is pushing forward with full force, Web 2 is being replaced by Web 3, and we have abandoned hedge funds in favor of passive investment strategies.

The same bubble, new names; imitation and replication have no boundaries in the globalized world of bits, and all bets are one bet.

As the road ahead narrows, Wall Street is replaced by Twitter and Reddit. The fruits of our era's over-financialization are no longer left to bankers in Zegna suits.

Software is unleashing a monster ------ Bubble Skura, where all bubbles are rolled into one gigantic monster.

"Investors who limit themselves to what seems normal and reasonable in human history are utterly unprepared for the miracles and wonders they now find themselves in. The twentieth century was great and terrible; the twenty-first century will be even greater and more terrible. In a world where ordinary economic cycles are broken, classic investment strategies no longer work." (Peter Thiel)

Traditional views are of no help. Perhaps it is true; we may live in a new paradigm where bubbles are mathematically impossible. The world does not care what it is; it mainly cares what it might be. In the face of relentless revisionist forces, those things that can become something are more valuable than those that are already something. Can someone escape the flywheel?

This explains Thiel's hypothesis that "the greater the valuation differences between rounds of financing for startups, the greater the degree of undervaluation," where fundamentals follow prices. In the digital age, the power of reflexivity becomes unstoppable, and the Lollapalooza effect can indeed transform an automotive company into the world's largest sustainable energy and automation company.

Through this explanation, we run simulations. The market exists within the digital structures we run on our computers. Computers, like money, have become the abstraction of every desire, as they are proxies for what we yearn for within. Digital technology allows us to change reality according to our will more than ever before.

"For policymakers and investors, the challenge is how to find a way out between outdated wisdom and nihilism."

In a world that superficially seems to offer many choices but actually offers very few, it is no wonder that people prefer money and optionality. But some money is better than others, and some fantasies are more absurd than others.

For us to understand what might happen in the future, we need to imagine that the internet bubble actually occurred in a globally interconnected, massively imitative digital world. The most surprising plan would be the winning plan.

Since the market and financial world cannot calculate the apocalypse, it is not worth placing the opposite bet.

Risk warning

Risk warning Risk warning

Risk warning