Can DeFi really consume the financial world?

Software is devouring the world, and DeFi is devouring the financial world.

Software is devouring the world, and DeFi is devouring the financial world.This article was published on May 31, 2020, on Babit, authored by Sato Xi.

Author's Preface: "Software is eating the world, and DeFi is eating the financial world." We can easily understand the first half of this sentence, but what about the second half? What is DeFi? The author attempts to explain it through personal study notes. In this article, you will learn about:

- The origins of DeFi

- The three realms of DeFi decentralization

- The explosion of the DeFi world

- Will Ethereum continue to dominate DeFi or will a chaotic era of competition arise?

- The various risks involved in DeFi

- Some personal insights on DeFi projects, DeFi investment, and DeFi wealth management

Many people have experienced participating in P2P wealth management and stepping on landmines. Looking back, the so-called P2P wealth management is not truly point-to-point wealth management, but rather involves depositing funds into a centralized platform, which then manages the funds in a centralized manner. The funds on the platform are actually controlled by a single or a few individuals, so essentially, they are all pseudo-P2P.

"Power tends to corrupt, and absolute power corrupts absolutely."

This famous quote from British thinker Acton is well-known. Recently, a popular saying goes, "The dragon-slaying youth ultimately becomes the evil dragon," which conveys the same idea.

Although these statements may seem overly absolute, they are close to the truth in many cases.

Of course, the collapse of P2P companies is not solely the fault of the founders; many times it is due to unreasonable designs or an abundance of bad debts caused by too many defaulters, ultimately leading to the platform's closure.

All these reasons boil down to one word: people.

Human emotions and desires are inherent, so despite the existence of laws regulating P2P wealth management, when human factors are involved, there can be countless ways to destroy the entire platform.

So, is there a way to solve or bypass the issue of human nature?

In 2009, the Bitcoin system design proposed by the mysterious figure Satoshi Nakamoto utilized the essence of human pursuit of profit to achieve true P2P transactions through code rules. This system eliminated dependence on third parties and did not require endorsement from the state or laws.

And as we can see, Bitcoin has successfully operated for 11 years and has grown into a behemoth with a market capitalization of nearly $200 billion.

The success of Bitcoin has prompted many to think that finance can also be decentralized. However, due to Bitcoin's extreme volatility, mainstream finance still denies its financial attributes.

This leads us to the theme of this article: Finance + Decentralization = DeFi (short for Decentralized Finance).

The Origins of DeFi

In fact, the term decentralized finance (DeFi) did not first appear in modern times. Its first recorded use dates back to the early 20th century (about 100 years ago) ^[1]^, when the Corn Belt Meat Producers' Association in the United States used this term during an annual meeting. Of course, this term originally referred to issues of fund allocation, not the DeFi we are exploring today.

So what was the first project to attempt DeFi?

Many might mention today's DeFi leader Maker, but that is not the case. The first project to attempt DeFi was actually Bitshares, created by Daniel Larimer (BM), Charles Hoskinson, and others. It was initially created under the name ProtoShares (PTS) and later renamed BitShares (BTS) ^[2]^.

Elements such as decentralized exchanges (DEX), stablecoins, and collateralized lending that we are familiar with today all originated from this project. However, having advanced ideas is one thing; being able to implement them is another.

After experiencing events such as inflation and the departure of founder BM, Bitshares did not successfully realize the concepts mentioned above.

The project that truly introduced the term DeFi to the world is the aforementioned Maker.

It essentially did two things: 1. Dai (aimed at being pegged 1:1 to fiat currency USD) and 2. lending and trading services related to stablecoins.

This leads us to the first application of DeFi—decentralized lending, which is truly P2P wealth management without third-party involvement.

What is the potential scale of this market? According to a report, the global fintech transaction volume in 2019 was nearly $5.5 trillion, with the overall scale of lending and wealth management exceeding $1 trillion.

In the world of blockchain, decentralized lending is achieved through computer protocols known as smart contracts, which allow for trustworthy transactions without third parties. Users' funds are stored in smart contracts on the Ethereum blockchain, which are responsible for management.

Although this vision sounds beautiful, achieving it is not as easy as it seems.

The Three Realms of DeFi Decentralization

In the early stages, project teams had to make some compromises. For example, the team behind the so-called DeFi star project Compound held the management key (Admin Key) for its smart contracts. What can the management key (Admin Key) be used for?

Mainly for the following:

- Pausing/freezing contracts;

- Modifying interest rates and other rules;

However, in reality, holding the management key (Admin Key) may also mean that the manager can steal all assets from the system ^[3]^.

In other words, the existence of the management key implies that the system is centralized, which has been criticized by Bitcoin purists. Thus, DeFi has also been translated by many as open finance, which implies that these projects are not truly decentralized, and that they have no entry barriers, allowing people from all over the world to use them, thereby achieving the goal of inclusive finance.

Of course, DeFi, DeFi, decentralization will still be the goal, but this will be a process. In the early stages, when contract security is not guaranteed, the Admin Key model will be prevalent. Some will set a time lock (timelock), such as 2 to 7 days, to prevent malicious or accidental rule modifications, while others will use multi-signature (Multisig) technology to reduce the risk of single points of failure in the system.

There are also some DeFi projects without a management key (Admin Key). For example, Maker decides on contract rule modifications through governance voting, and the entire process is completed on the blockchain. The rule is that the more MKR tokens one holds, the greater their voice. Of course, Maker is also gradually transferring power, and only after the control of MKR is fully handed over to the governance community can the system realize the decentralized vision of MakerDAO. ^[4]^

There are indeed projects that can truly be called DeFi, such as Uniswap. It has no management key (Admin Key), and once the contract is deployed, there is no way to upgrade, modify, or stop Uniswap's smart contracts ^[5]^. New versions of the contract, such as Uniswap V2, need to be redeployed.

Therefore, if we rank DeFi projects according to their degree of decentralization, we can roughly divide them into three categories: the first is the truly trustless category represented by Uniswap; the second is the decentralized governance category represented by Maker; and the third is the pseudo-DeFi projects controlled by teams holding management keys (Admin Key). It is worth mentioning that the aforementioned Compound is also moving towards decentralized governance and has launched a governance token for this purpose ^[6]^. More and more DeFi projects are adopting this approach.

The Explosion of the DeFi World

After decentralized lending opened the curtain to the DeFi world, some pioneers gradually transplanted various components of the traditional financial world into this realm. For example, some are exploring decentralized insurance, some are developing decentralized derivatives trading markets, and others are challenging decentralized index funds ^[7]^. Anything that exists in the traditional financial world can theoretically be presented in a decentralized form through smart contracts, and some innovations that do not exist in the traditional financial world have also emerged.

As a result, more and more projects began to align with the concept of DeFi. For instance, wallets and even some centralized service providers have started to venture into this field, as participants know this is a trend of the future. DeFi is the most suitable application scenario for blockchain besides Bitcoin and also the one with the greatest imagination.

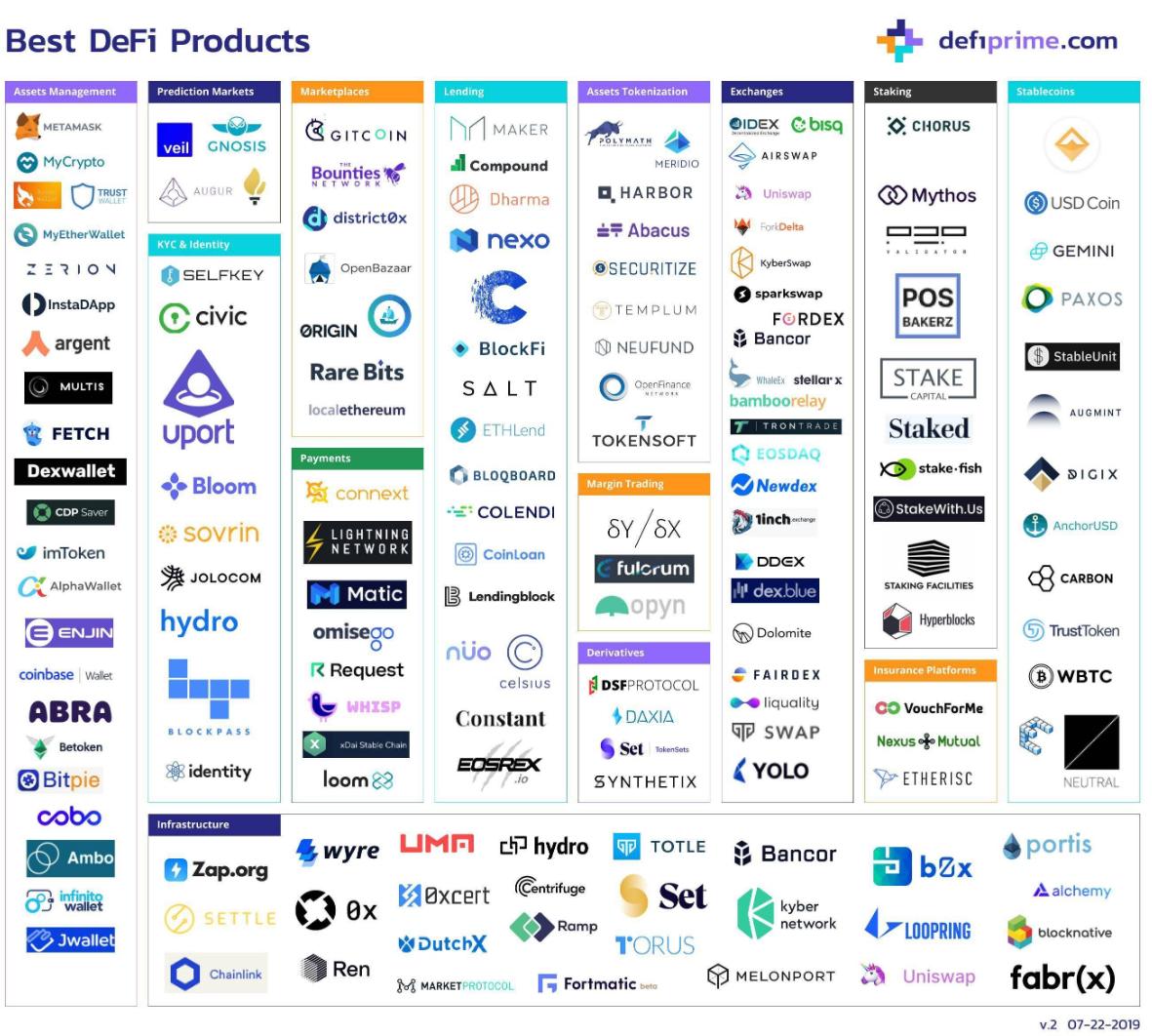

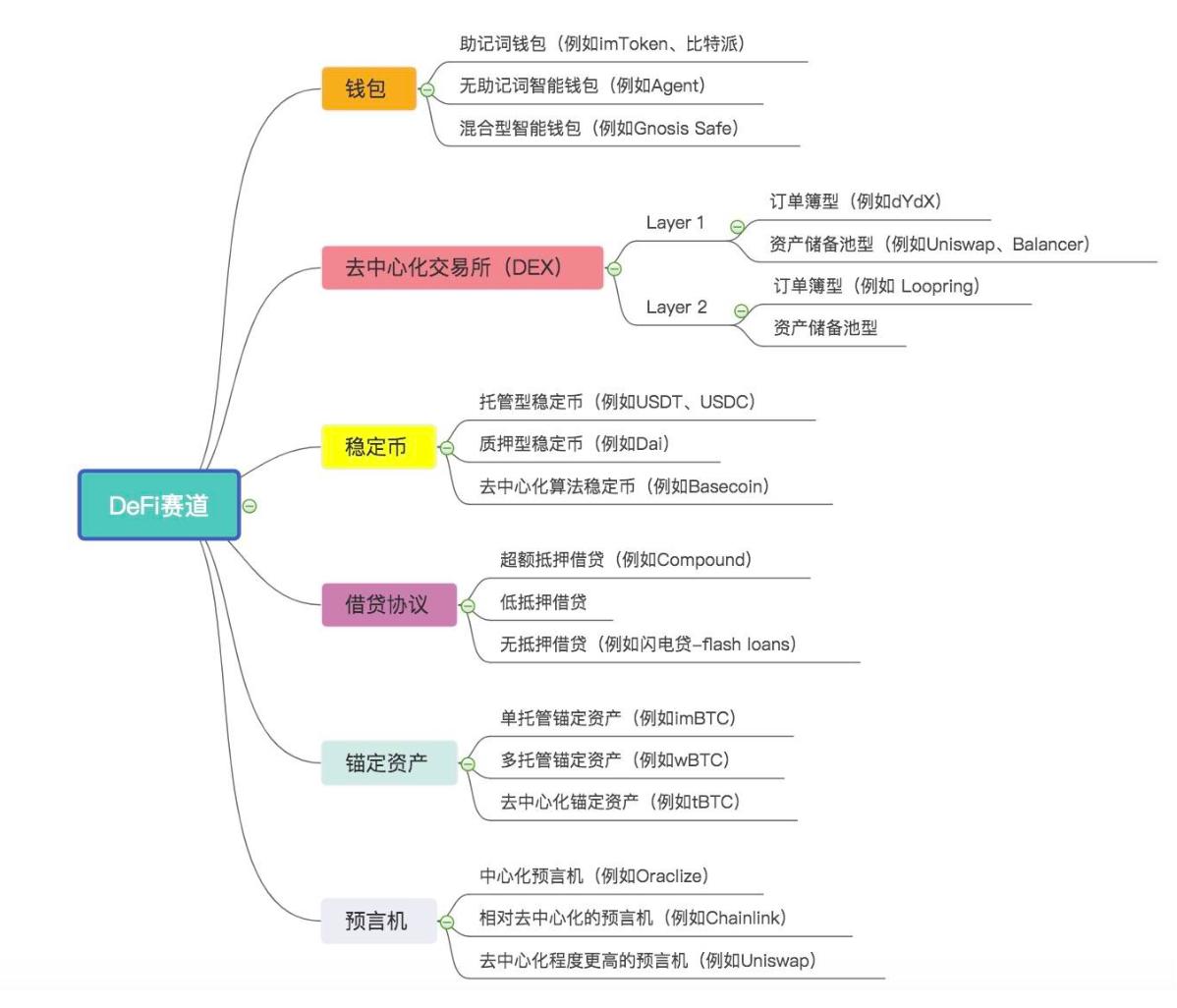

For such a multitude of projects, we can actually conduct a simple classification, categorizing different projects into a track. For example, I would first divide them into six major categories:

- Wallets, 2. Decentralized Exchanges (DEX), 3. Stablecoins, 4. Lending Protocols, 5. Asset Pegging, 6. Oracles

Then further subdivide:

(Note: The above classification is my personal understanding; you can categorize them differently based on your own thoughts.)

Currently, we can observe that in the wallet category, mnemonic wallets still dominate, while Layer 1 exchanges occupy more market share in DEX. Custodial stablecoins hold a dominant position, and the lending protocol realm is ruled by over-collateralized lending. In asset pegging, custodial types currently hold an advantage, and so on.

However, these are characteristics presented by the market in its early stages. Looking ahead, as the security of decentralized projects is proven and the related thresholds become lower, the overall degree of decentralization in the market will further increase. Only then can DeFi truly be called decentralized finance.

The potential overall market size of DeFi will be in the trillions of dollars. So what is its current scale? According to relevant statistical websites, it is currently less than $1 billion.

Therefore, in my view, DeFi will be one of the biggest opportunities for humanity in nearly a century, following Bitcoin.

Alright, the above is the part of painting a vision. Next, let's further understand the development of the DeFi world and discuss some related risks, and finally share some personal insights on DeFi projects, DeFi investment, and wealth management.

Will Ethereum Continue to Dominate DeFi or Will a Chaotic Era of Competition Arise?

As of now, the vast majority of DeFi projects are built on the foundation of Ethereum. Simply put, Ethereum's decentralization, network effects, and rich developer tools have created a moat for DeFi protocols. At this stage, these reasons have collectively placed Ethereum on the throne of the DeFi world.

Is this throne truly unshakeable? I believe many people have some doubts about this ^[8]^.

According to the Matthew Effect, the probability of Ethereum maintaining a dominant position in the DeFi world for a long time is very high.

One speculation suggests that as Ethereum transitions to Ethereum 2.0, uncertainties regarding composability will create opportunities for alternative public chains. Another viewpoint holds that the current congestion and high transaction fees on the Ethereum mainnet will also provide opportunities for other public chains.

Regarding the first speculation, the actual hope is already very slim. According to the design proposed by Vitalik ^[9]^, Ethereum 1.0 will exist as a shard of Ethereum 2.0, and the merger of the two is expected to solve the composability issue.

As for the second viewpoint, I believe it is equally untenable. Just like Bitcoin, while users have a demand for blockchain's TPS and low transaction fees, these are not the primary demands; security and decentralization are the decisive factors.

In addition, short-term solutions like ZK Rollup and Optimistic Rollup can completely resolve congestion and high transaction fees. In the long term, sharding (assuming it can be realized) can achieve better scalability.

So what are the real potential factors that could overthrow Ethereum's DeFi dominance?

Composability + Large-scale Hacking Events!

In fact, composability is Ethereum's greatest advantage, but it is also its biggest potential pitfall.

Why do I say this? Currently, DeFi projects on the Ethereum platform are like castles built with blocks. Those of us who have played with building blocks know that when certain key blocks encounter problems, the entire castle may be impacted. If the most fundamental parts have issues, the entire castle could collapse.

(Image from pexels.com)

In fact, some incidents have already served as good reminders:

- Due to the emergence of flash loans, the bZx protocol lost $640,000, and Maker, which had hundreds of millions of dollars in collateral assets within its contract, also faced a crisis. The Maker Foundation urgently changed the rules after receiving alerts from researchers ^[10]^ to prevent attackers from exploiting flash loans and governance rule flaws, thus averting disaster.

- The DeFi lending protocol Lendf.Me was hacked, resulting in the theft of $25 million in assets, due to a new security vulnerability created by the combination of the ERC777 token standard and Lendf.Me. Composability brings complexity, and complexity is at odds with security (although the hacker ultimately returned all assets, this incident undoubtedly served as a wake-up call for every DeFi user).

Given this, will there be a trend towards decoupling in the future? Just like breaking down the entire castle into multiple units, thereby dispersing the overall system's risks, so that when one part collapses, it does not affect the others?

This leaves room for thought and may present opportunities for other public chain projects focused on specific DeFi areas.

The Various Risks Involved in DeFi

Now let's specifically discuss the risks involved in DeFi, which I believe are very important for all participants.

- All DeFi projects face the risk of contract code vulnerabilities, which not only involves their own contracts but may also involve contracts of other projects or even other components (such as the frontend).

- For certain projects, users may face risks related to management keys (Admin Keys). Some projects do not disclose this situation to the public, but audit reports may mention it. Therefore, reading audit reports is very necessary. Projects like Compound and the recently troubled Lendf.Me both have Admin Keys. If there is no decentralized governance, it is best not to participate.

- Systemic risks brought by centralized projects, such as custodial tokens like USDT and wBTC, may have single points of failure, so they theoretically need to be guarded against.

- The risk of losing private keys. Participating in DeFi requires controlling your own private keys, so the possibility of losing them exists, and many people easily lose them. One solution is to use smart contract wallets, but this also involves the risk of contract code vulnerabilities.

- Risks introduced by oracle issues. Oracles are a crucial part of the DeFi ecosystem, so if this part encounters problems, it can also lead to user losses.

- Market risks, such as the Black Thursday on March 12, which caused a large number of DeFi collateral positions to be liquidated, resulting in significant losses for users.

For tips on DeFi risks, I recommend reading Guru's "DeFi Landmine Record" ^[11]^.

Some Personal Insights on DeFi Projects, DeFi Investment, and DeFi Wealth Management

Having discussed the observed state of DeFi, I would like to share some personal insights gained during this period of learning about DeFi. Overall, the scope of the DeFi concept has been expanding. It will not only involve components such as wallets, DEX, stablecoins, lending, and oracles, but also cross-chain and scalability.

In the context of generally limited performance in Layer 1, the market's demand for Layer 2 technology will be amplified. Therefore, I believe that doing DeFi based on Layer 2 will be a relatively clear trend.

In these aspects, Ethereum already has a significant advantage. Thus, betting on Ethereum and the top seed projects in related tracks is a viable investment strategy.

However, this does not mean that other public chains have no opportunities. In fact, as long as they effectively manage the three elements of stablecoins + cross-chain + DEX, they have a chance to win over some users, even potentially replacing Ethereum. Compared to Ethereum, DeFi projects on other public chains tend to be simpler, which may result in fewer risks. However, they do not possess the network effects that Ethereum's DeFi projects have.

In other words, another optional DeFi allocation strategy is to choose some public chain projects with relatively good underlying infrastructure outside of the Ethereum platform to hedge against the risk of a collapse in the Ethereum DeFi ecosystem.

As for which projects may have potential, I leave that for everyone to think independently.

Additionally, regarding DeFi wealth management, my view is that under the current context of high risks in DeFi projects, it is not suitable for users to participate. In contrast, the expected returns from investing in the projects themselves or their tokens, which carry the same risk of contract vulnerabilities, far exceed those of wealth management. Wealth management is actually a choice that is suitable only when the market is in a later stage of development (i.e., when systemic risks are lower).

Returning to the beginning of the article, can DeFi really devour the financial world? My view is that in the short term, the term "erode" is more appropriate, but in the long term, it is inevitable.

References:

1. It is "OpFi" rather than "DeFi," is decentralized finance a "utopia"? https://www.8btc.com/article/476716↵

2. https://zh.wikipedia.org/wiki/%E6%AF%94%E7%89%B9%E8%82%A1↵

3. Some risks regarding compound wealth management: https://medium.com/@ameensol/what-you-should-know-before-putting-half-a-million-dai-in-compound-fafdb2645f77#f7c9 ↵

4. Three cornerstones for MakerDAO to achieve complete decentralization https://blog.makerdao.com/zh/makerdao-%E5%AE%9E%E7%8E%B0%E5%AE%8C%E5%85%A8%E5%8E%BB%E4%B8%AD%E5%BF%83%E5%8C%96%E7%9A%84%E4%B8%89%E5%A4%A7%E5%9F%BA%E7%9F%B3/↵

5. https://zdl-crypto.fandom.com/wiki/Uniswap↵

6. https://www.8btc.com/article/584138↵

7. https://www.8btc.com/article/599680↵

8. https://www.8btc.com/article/499045↵

9. https://ethresear.ch/t/alternative-proposal-for-early-eth1-eth2-merge/6666↵

10. https://www.8btc.com/article/558368↵

11. https://www.8btc.com/article/585525↵