WealthBee Macro Monthly Report: The tariff bomb has arrived, and the global trade order is facing the largest reshaping wave since World War II, with the consensus on Bitcoin as "digital gold" strengthening

In March, the global market was deeply mired in policy uncertainty, urgently seeking new anchor points. The U.S. stock market accelerated its valuation reconstruction, and the crypto market was also inevitably affected by the fluctuations. With the new tariff bomb dropped on April 2, the global trade order faces deep restructuring, forcing countries to urgently adjust their economic policies. In such times, patience becomes crucial. As the new order gradually takes shape, market sentiment will also warm up accordingly.

Trump's tariff policy underwent multiple adjustments in March. On April 2, the Trump administration officially announced the implementation of a "comprehensive reciprocal tariff" policy—imposing a minimum 10% base tariff on all goods exported to the U.S., and additional tariffs on about 60 countries with significant trade deficits (such as 34% on China, 46% on Vietnam, and 49% on Cambodia)—ushering in the most severe wave of restructuring in global trade order since World War II.

Once the news was announced, the market experienced violent fluctuations. U.S. stocks and the dollar fell sharply, with the dollar index dropping below 104; Nasdaq futures plummeted over 4%, and S&P 500 futures fell by 3.5%. The stocks of the seven major U.S. tech giants saw particularly significant declines, with Apple dropping 7.5% in after-hours trading. Funds rushed into safe-haven assets, with spot gold prices soaring, breaking through $3160 per ounce, setting a new historical high.

The high tariff rates and broad scope of this increase far exceeded Wall Street's previous estimates. Investors are concerned that the tariff war will ultimately impact the foundation of U.S. economic growth. First, there is the risk of supply chain disruption. Targeted tariffs on automobiles, steel, aluminum, and technology products (with some rates reaching 25%-50%) are forcing companies to accelerate the regional restructuring of supply chains, sharply increasing the costs of the industrial chain. Secondly, there are concerns about an inflationary spiral. Estimates from JPMorgan indicate that, combined with countermeasures, the U.S. CPI could be pushed up by 2-2.8 percentage points.

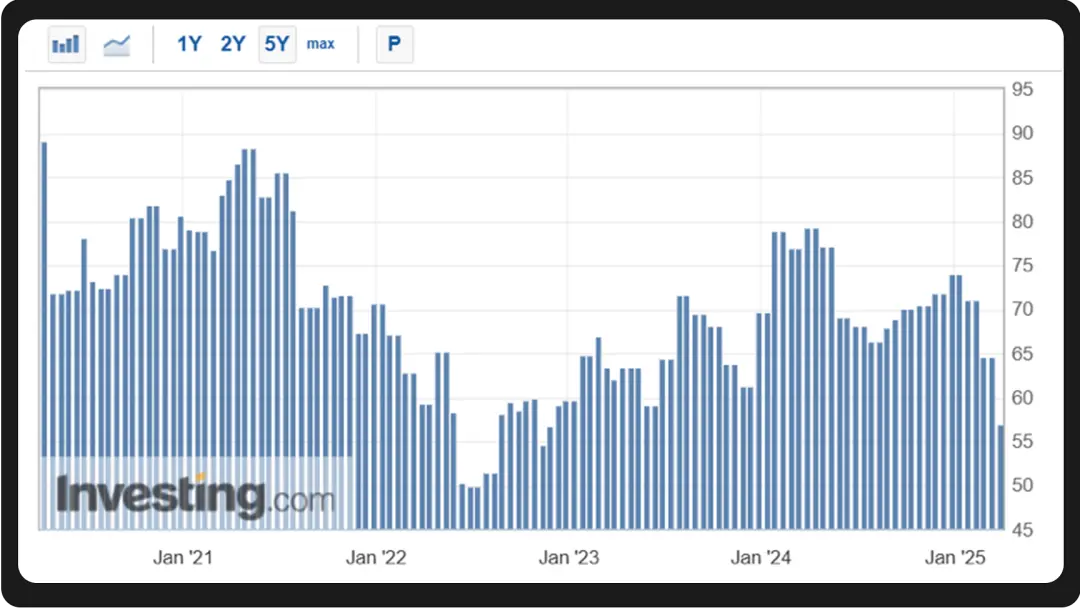

U.S. Consumer Confidence Index (Source: investing.com)

Moody's chief economist Mark Zandi raised the probability of a recession in the U.S. economy this year from 15% at the beginning of the year to 40%, while Goldman Sachs' economist team also increased the likelihood of a U.S. recession within the next 12 months to 35%. In March, some economic data indicators in the U.S. showed a decline. Although the non-farm payroll data at the end of March indicated that the current unemployment rate in the U.S. is 4.1%, the final value of the consumer confidence index for March dropped from 64.7 in February to 57, retreating from the initial value of 57.9, and falling below the median estimate of economists. Meanwhile, the core PCE price index year-on-year still reached 2.8%, confirming the dilemma of "slowing economic growth and stubborn inflation."

The Federal Reserve expressed concerns about economic uncertainty at its March meeting. On one hand, economic growth is showing signs of slowing, with the GDP forecast for 2025 revised down from 2.1% to 1.7%; on the other hand, inflation remains sticky. In this situation, if the Fed chooses to cut interest rates, it may further stimulate price increases; while maintaining high interest rates could exacerbate corporate debt pressure, putting the Fed, caught in the triple storm of inflation, politics, and globalization, in a dilemma regarding policy decisions, making it difficult to take action. Thus, we saw that in March, the Fed decided to keep the interest rate unchanged at 5.5%.

After the announcement of the new tariff policy on April 2, traders increased their bets that the Fed would start cutting interest rates in June, with a cumulative cut of three 25 basis points (i.e., 0.75 percentage points) before October. According to Reuters, the probability of a rate cut at the Fed's June meeting has risen to about 70%, up from about 60% before the tariff announcement.

Meanwhile, the impact of the tariff policy extends far beyond the U.S. domestic economy and the Fed's monetary policy. Trump's "reciprocal tariff" plan aims to increase fiscal revenue through tariffs while using it as leverage to force other countries to lower tariffs or make other policy changes. Are other countries willing to cooperate in negotiations? How much can Trump concede in negotiations? Currently, major economies around the world are formulating countermeasures, and some analysts believe that global trade friction is evolving from "localized conflicts" to "systemic confrontation." The future global economy and financial markets will still need to bear pressure under this uncertainty.

**(Source: ** https://www.nasdaq.com/)

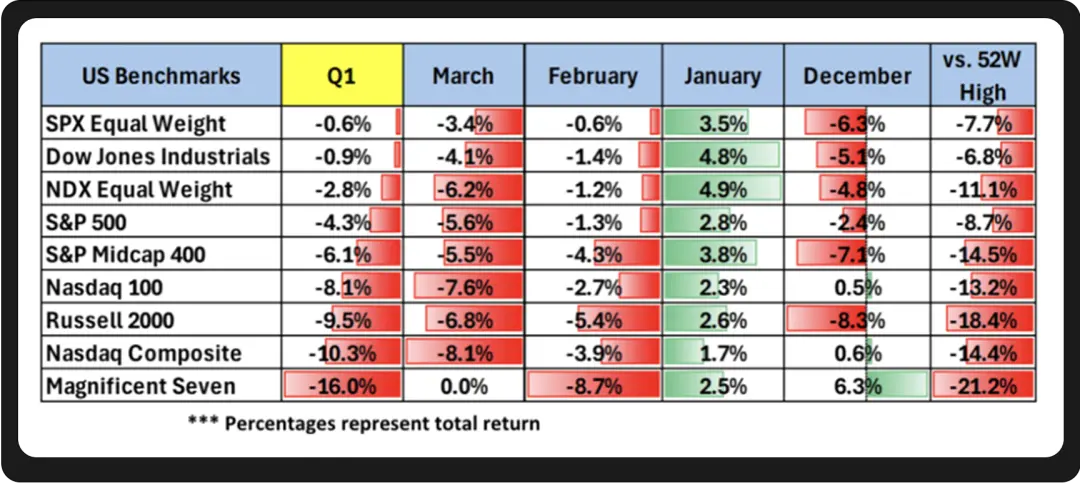

U.S. stocks continued their downward trend in March, leading to the S&P 500 and Nasdaq ending the first quarter of 2025 down 8.7% and 12.3%, respectively, marking the largest quarterly decline since 2022. Looking at a longer time frame, since Trump was re-elected as U.S. president in November 2024, the S&P 500 index has dropped from 6200 points to 5572 points, a decline of over 10%, evaporating $4 trillion from its peak.

(Source: The New York Times/Karl Russell)

Over the past two years, U.S. stocks attracted global funds due to "TINA" (There Is No Alternative to equities), accounting for more than 50% of the global stock market's market capitalization. During periods of market prosperity, investor optimism about U.S. stocks continuously pushed prices higher, ignoring potential risks. However, as the economic cycle evolves, this divergence from fundamentals has become increasingly difficult to sustain, and institutional optimism about U.S. stocks is being corrected: Goldman Sachs has lowered its year-end target for the S&P 500 from 6500 points to 6200 points, citing "tariff risks and slowing profit growth"; Morgan Stanley warned that 5500 points may be the starting point for a technical rebound, but it needs corporate earnings to hit bottom for support. This adjustment reflects the market's skepticism about the "earnings-driven" logic of U.S. stocks—expected earnings growth for the S&P 500 in 2025 has been revised down from 11% to 7%, while the earnings growth advantage of the seven tech giants is narrowing, with the gap between them and the S&P 493 shrinking from 30 percentage points to 6 percentage points.

At the same time, the confusion of U.S. policy signals further exacerbates market panic. Trump urges the Fed to cut interest rates while not ruling out the possibility of an economic recession; White House officials downplay recession risks while acknowledging transitional pains. This contradictory stance leaves investors at a loss, severely undermining market confidence, and the market quickly reacted to policy uncertainty, with the "big 7" (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, Tesla) facing a wave of sell-offs, with Tesla down nearly 36% in the first quarter and Nvidia down nearly 20%. As an important component of the S&P 500, the "big 7" has seen its market value evaporate by over $2.5 trillion since Trump's re-election, reflecting both a correction of previous valuation bubbles (S&P 500 price-to-earnings ratio of 21 times) and a "vote with their feet" against policy uncertainty.

By the end of March, U.S. stocks rebounded somewhat, with the S&P 500 rising to 5767 points, reflecting market expectations for a "softening" of policies, i.e., that the White House might adopt a phased or exemption strategy rather than a comprehensive tariff increase. However, it proved that the market's optimistic expectations at that time were unfounded.

It is worth mentioning that under the dynamic interplay of interest rate cut expectations, tariff intensity, and recession risks, some institutions have clearly pointed out that the risk-reward ratio of unidirectional bets on U.S. stocks has significantly deteriorated. For example, AQR Capital Management warned investors that in this environment, they need to rely more on diversified strategies than ever before and should not blindly bet on a one-sided rise in U.S. stocks.

**The S&P 500, Nasdaq, and the "big 7" all fell in the first quarter. Bitcoin also faced the dual impact of market fluctuations and policy uncertainty, but its performance remained resilient amid the turbulence: after experiencing severe fluctuations at the end of February, Bitcoin did not show a one-sided decline in March but exhibited a "V-shaped" oscillation, initially declining before rising. The monthly decline narrowed to 2.09%, significantly better than the Nasdaq's 8.2% decline during the same period. For a considerable time, Bitcoin's movements have closely mirrored those of tech stocks, often rising and falling together. However, during this period of market turmoil, Bitcoin charted an independent course.

(Source: investing.com)

Especially in mid to late March, as the U.S. SEC abolished SAB 121 (allowing banks to custody crypto assets) and institutions like BlackRock increased their holdings, coupled with the Fed signaling "three rate cuts within the year" on March 20, Bitcoin experienced a strong rebound. Overall, the adjustments in Bitcoin during March were more of a technical correction rather than a trend decline. Grayscale's research director Zach Pandl believes that the market has partially "priced in" the negative impacts of tariffs, and the worst phase of selling may have ended.

Although the crypto market is still shrouded in the shadow of the latest tariff policy, the U.S. government's recognition and regulatory progress in the crypto asset space have become increasingly clear, with a series of measures paving the way for the industry's long-term development: first, on March 6, Trump signed an executive order establishing a "Strategic Bitcoin Reserve" (SBR), incorporating approximately 200,000 BTC previously confiscated by the federal government into reserves, explicitly stating that they would not be sold for four years. This marks the first time the U.S. government has managed Bitcoin as a permanent national asset, establishing its status as "digital gold." Although this executive order is not legislation, it lays the groundwork for subsequent policies.

Secondly, the SEC is gradually relaxing its historically tough stance on cryptocurrencies, having held its first cryptocurrency roundtable in March and planning to hold four more roundtables in April, May, and June on trading, custody, tokenization, and DeFi, clearly shifting from "enforcement-oriented" to "cooperation and rule-making," which is seen as a key prelude to the establishment of a regulatory framework. Notably, the SEC's announcement to abolish SAB 121 means that banks can finally legally custody crypto assets. Following the repeal of SAB 121, traditional financial institutions like JPMorgan and Goldman Sachs immediately launched crypto custody services, with over $200 billion in institutional funds expected to enter through banking channels by Q2 2025.

BlackRock CEO Fink's annual letter to investors (Source: https://www.blackrock.com/corporate/investor-relations/larry-fink-annual-chairmans-letter)

Institutional investors' enthusiasm for crypto assets, especially Bitcoin, continues to rise. On March 31, Larry Fink, CEO of the world's leading asset management company BlackRock, released a 27-page annual letter to investors. In the letter, Fink issued a rare and serious warning: if the U.S. cannot effectively manage its expanding debt and fiscal deficit, the dollar's long-standing position as the "global reserve currency" could very well be replaced by Bitcoin and other emerging digital assets. Notably, Fink mentioned Bitcoin seven times and the dollar eight times in the letter, highlighting Bitcoin's importance in the current financial context and hinting at its potential key role in the evolution of the global economic landscape.

With the implementation of Trump's tariff policy on April 2, the outlook for the U.S. economy becomes increasingly murky. If the U.S. economy does not fall into a deep recession under the tariff policy and the Fed cuts rates in June, Bitcoin is expected to see a trend reversal in the second quarter. During periods of economic instability, Bitcoin's scarcity and safe-haven attributes will become increasingly prominent. Once market risk appetite rebounds, Bitcoin, as an emerging asset class, aligns with the market's potential demand for new safe-haven and value storage methods, likely breaking through key resistance levels first and welcoming a revaluation of its value.

In March, the market oscillated between "stagflation worries" and "policy easing." In the long term, if the implementation of tariffs drives up inflation and erodes the dollar's credibility, it will force funds to shift towards non-sovereign assets. BlackRock CEO Fink asked in his investor letter: "Will Bitcoin shake the dollar's hegemony?" This is not an unfounded question; he reminds us that the most disruptive variable in reshaping the global financial order has already emerged.